Circle Internet Group 最近宣布 其新 Arc 區塊鏈將探索可逆 USDC 交易,此舉點燃了自區塊大小之爭以來加密貨幣界最具爭議的辯論。

Circle 總裁 Heath Tarbert 坦言,公司正「考慮交易是否存在可逆的可能性」,同時強調要「維持結算最終性」——這既可被視為推動主流採納所需的務實演變,也可被認為是對加密貨幣核心理念的根本背叛。

影響不容小覷。USDC 市值 650 億美元,Goldman Sachs 預計 2027 年將增至 770 億,Circle 推動可逆穩定幣的嘗試或將決定區塊鏈技術是成為傳統金融的橋樑,還是為機構舒適度犧牲其革命潛力。這種「不可更改性」與「用戶保護」的拉鋸,正體現整個加密圈存亡的終極疑問:去中心化貨幣能否保持抗審查屬性,同時滿足機構合規?

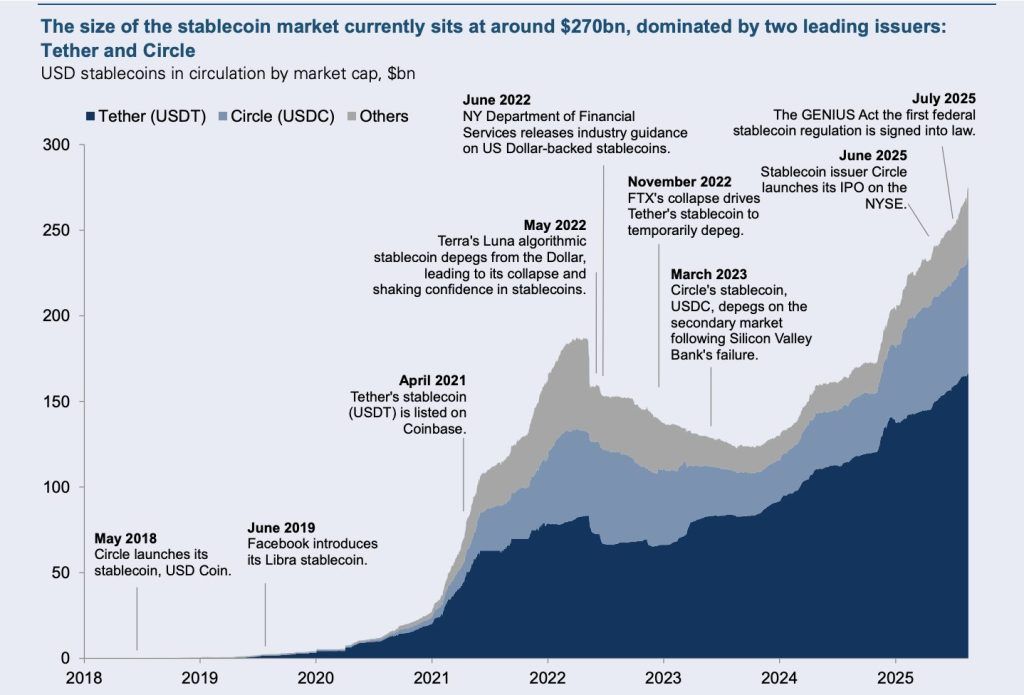

爭議正值穩定幣重要時刻。2024 年市場交易額達 27.6 兆美元,比 Visa 與 Mastercard 加總還高 7.68%;特朗普總統推出 GENIUS 法案,建立首個聯邦穩定幣監管框架。Circle 的 Arc 區塊鏈將於今秋在測試網上線,年底主網上線,主張引入「對付款」層,讓交易像信用卡退款般可逆,同時保留底層最終性。這種混合方式,質疑十年來認定「不可更改」為加密根本特性的主流觀點。

比特幣、以太坊奠定不可更改性為加密核心

不可更改性是比特幣原始設計及以太坊智能合約架構的立本原則。比特幣達到「幾乎難以逆轉」的不可更改性——3-6 個區塊(約 30-60 分鐘)後不可逆。以太坊亦然,約 12 個區塊(2-3 分鐘)即達實際最終性。

此種不可更改,成為經濟理論家所謂「金錢的第七屬性」——為六大特性之外的革命性補充(耐用性、便攜性、可分割、統一性、供應有限、可接受性)。相比傳統電子支付可在數月內被拒付、逆轉,區塊鏈交易通過密碼學獲得最終性,無單一實體能單方面推翻。

哲學根源來自 90 年代 cypherpunk 運動,如 Eric Hughes 所說:「隱私對開放社會至關重要」,「Cypherpunks 寫代碼」。這種以反抗集中控制的精神,直接促成比特幣誕生——Satoshi Nakamoto 於 cypherpunk 郵件群組首次公布白皮書。運動提倡「廣泛使用強加密和增強隱私技術」,實現「去中心化、個人自主免於中央管控」。

比特幣不可更改性,不只技術層面,更有重要經濟和社會功能。它解除交易對手風險,不會被銀行、政府、第三方隨意逆轉;確保結算可預測,適合建立依賴信任的複雜金融應用;最關鍵,抗審查,保護用戶免受權力機構無理凍結或沒收資產。

以太坊透過智能合約——即自動執行、無法被干預程式——將此推展。所謂「代碼即法律」理念相信,去中心化網路下的不可更改規則,比容易被腐敗或脅迫的人治制度更可靠。

不可更改性的經濟意涵遠超技術結構。研究顯示,區塊鏈價值主張是「攻擊成本高、難以消滅」——經濟學家稱之為可信承諾機制,即使逆轉政策對未來有利也能避免。失去不可更改性,區塊鏈就失去超越中心化系統的優勢。

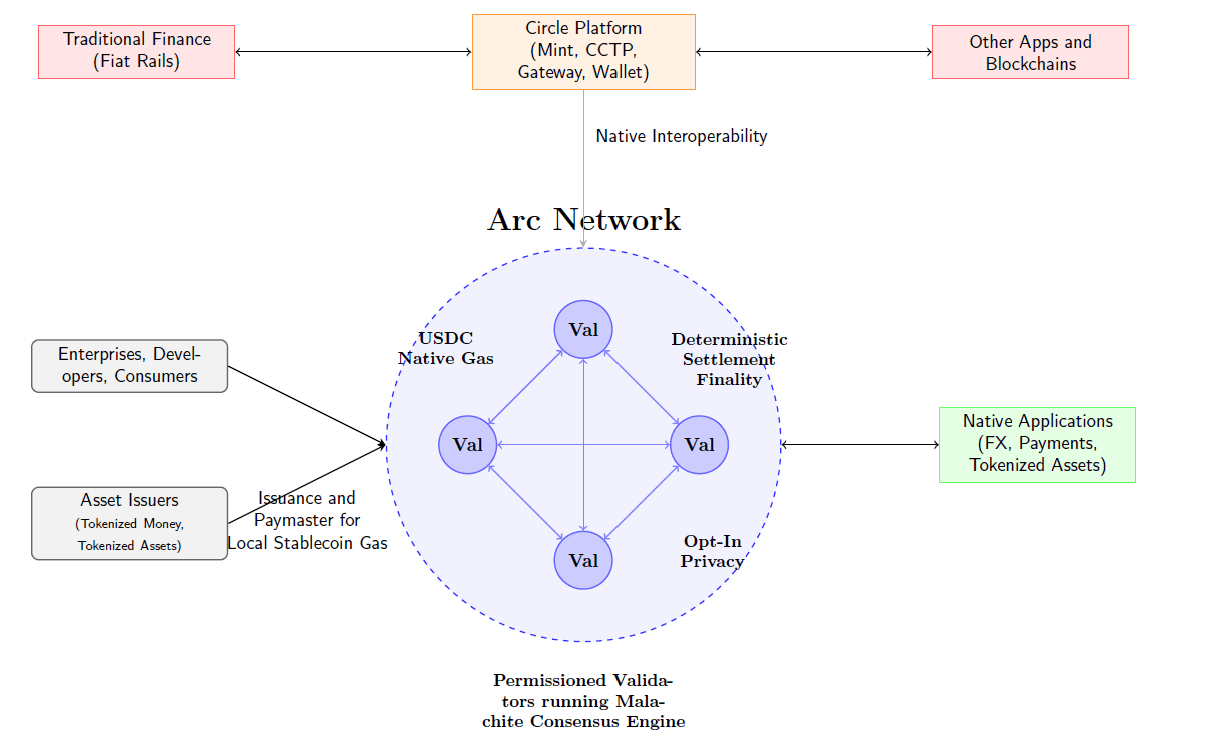

Circle Arc 區塊鏈以對付款層引入受控可逆性

Circle Arc 區塊鏈是至今最先進、嘗試協調區塊鏈不可更改性與傳統金融需求的項目。Layer-1 網路將於 2025 年秋季啟動測試網,年底主網,採全新架構:底層保持確定性最終結算,高層則可選擇性逆轉交易。

技術核心來自 2025 年 8 月從 Informal Systems 收購的 Malachite 共識引擎。此拜占庭容錯系統,在 20 個驗證者下,結算僅 350 毫秒,最多可 10,000 筆每秒(4 驗證者高效配置)。與需多次確認的概率型最終性不同,Arc 為即時、非概率性的結算,Circle 認為可同時滿足區塊鏈純粹主義者及機構需求。

Arc 最大爭議為「對付款」層——即部署於不可更改區塊鏈之上的鏈外爭議解決機制。Heath Tarbert 認為此舉令「交易可逆」同時保留「最終結算」,承認「立即轉賬」與「不可撤回」兩者間的張力。

系統設計上需雙方同意方可逆轉,與傳統單邊拒付不同。此作法希望兼顧打擊詐騙及爭議解決,並防止現有支付體系常見的隨意逆轉。所有逆轉經透明及可審計的鏈外流程完成,避免損及底層不可更改性。

USDC 是 Arc 的原生 gas 代幣,用戶無需用波動性高的加密貨幣付手續費。如此一來,機構得以運用以美元計的可預算費用,並配合「費用平滑」(指數加權移動平均)及「基礎費用上限」,防止網絡擁堵時費用爆升。

Arc 還內建適合企業的選擇性隱私功能:可加密交易金額、公開地址,實現企業金庫保密但保持監管合規。相關披露可藉 EVM 預編譯模組與可插拔密碼學後端組成,能針對不同應用調整隱私層級。

另外,Arc 支援 Circle 全產品,包括 Circle Payments Network、USDC、EURC、USYC 各穩定幣、Circle Mint、錢包、合同、跨鏈轉移協議及 Circle Gateway。如此一來,Arc 專為穩定幣應用而非通用型區塊鏈,形成人民幣基礎的金融基建。

應用場景包括自動外幣收付的跨境支付、穩定幣 FX 永續合約、結合身份與現金流記錄的鏈上信貸、具交割對付效果的資本市場結算,以及支援 AI 主導市場的代理型商業。Circle 宣布與 Fireblocks 合作機構託管,超過 100 多家金融機構跟進,並與傳統支付基建商 FIS、Fiserv 合作。

驗證者初期採用權威證明制(POA),由知名機構驗證者負責,達成運營和合規標準,日後轉為經許可實體參與的權益證明(POS)。這種受控設計重合規勝於去中心化,與比特幣無需許可共識模式形成鮮明對比,反映哲學路線分歧。

批評者認為此結構不過是將傳統金融集中化披上區塊鏈外衣,缺乏真正去中心化突破。不過,Circle 強調為推動機構採納所作的務實妥協,並以 USDC 650 億市值及監管明朗為策略背書。

幣圈激烈反彈「反加密」可逆性

可逆 USDC 交易方案一宣布,立即在加密社群引起激烈反對,批評者大呼此舉「反加密」根本背離區塊鏈核心。

反彈迅速且毫不妥協。知名幣圈人士 Aaron Day 表示:「USDC 宣布可逆交易,我們已偏離初衷。USDC 成為監控賬本上的法幣,這不是 crypto,而是 tyranny。」另一位社群成員形容 USDC 的目標是「成為首個完全中心化並可被 1000% 控制的穩定幣」,而亦有人警告 Circle「會消滅現有的優勢,令 USDC 喪失在 DeFi 的用途」。

知名區塊鏈調查員 ZachXBT 點出 Circle 的雙重標準,批評「Circle 甚至唔會主動凍結同北韓或者黑客組織有關的地址」,質疑可逆交易究竟真係為咗安全,定只係做樣畀監管睇。呢番說話之所以格外有共鳴,係因為 Circle 雖然近期強調交易可逆性,但以往對於資金被盜凍結資產的反應一向都慢。

其實,哲學層面的反對理由,比純粹技術考慮更深入。B2 Ventures 的 Arthur Azizov 指出,「傳統金融機構愈來愈主導加密貨幣的討論方向」,而「cypherpunk 精神逐漸退出主舞台」。呢番說話道出社群真正恐懼:可逆穩定幣唔單止係技術妥協,更係迎合傳統機構壓力的文化投降。

「CypherMonk」宣言警告:「當這些技術走入主流,我哋會變成只執著於『程式即法律』,而唔再重視我哋最初的理想動力。」這種說法反映出大家對加密貨幣由顛覆性科技,退化到企業主導、只係把舊有金融權力結構數碼化的更深層憂慮。

技術上的反對意見則集中於實際操作問題,尤其係被批評為「熱薯仔問題」。如果黑客好快將 USDC 兌換成其他資產,返轉頭撤銷原先的 USDC 交易可能連累無辜的流動性提供者(LP)同 DEX 用戶,反而無法打擊罪犯。有分析員質疑:「如果黑客已經轉咗錢,再點 revers USDC?係咪反而害到 LP?啲交易所點算?」

有社群成員認為,可逆交易會「令去中心化金融返返去中心化」,又會「抹殺咗我哋今日享有的自由」。這個批評凸顯 DeFi 無需審批、用戶自己持幣的基本模式,與可逆穩定幣靠中心化決策的衝突。

「消費者監控和官方帳號登記完全違背咗 DeFi 的價值主張」,批評人士擔心可逆穩定幣或會成為政治審查、社會控制的工具,政府越來越想監管加密貨幣交易,令這個風險更大。

不過,亦有人為 Circle 辯護,認為呢種做法係加密貨幣必要的演變。Falcon Finance 的 Andrei Grachev 就話,完全不可逆「其實唔符合大型金融體系的運作現實」,而「設計有清晰規則、用戶同意和鏈上執行的可逆性,唔係缺陷,反而可以係實用功能。」支持者舉例 Sui 區塊鏈成功幫 Cetus hack 追回 1.62 億美元,證明受控的可逆性可以實踐,唔會損害整個體系的誠信。

呢場爭議反映咗對加密未來路向的分歧。傳統加密支持者認為「不可逆性」係不能妥協,放棄呢個原則就等於拋棄咗區塊鏈最核心的價值。機構派則主張,純粹堅持理念唔應該阻礙實際主流應用和符合法規要求。

這個文化矛盾,正如研究員所講的「不可逆悖論」——區塊鏈最大長處可能亦係最大風險。一位開發者話:「你做到系統完全不可逆,就有機會將其缺陷固定落去。你做到可升級,就要重新相信人——原本想用系統超越嘅對象。」同場亦有監管壓力,例如 GDPR 的「被遺忘權」同區塊鏈不可逆原則完全衝突。研究指出:「區塊鏈的不可逆性與 GDPR 修改或刪除資料以符合法律的假設相左」,可逆系統可能有助解決合規問題。

社群反應反映對好多加密用戶嚟講,犧牲不可逆性係禁區。有評論甚至話,呢點可以決定「去中心化究竟得唔得存,會唔會喺機構主導下消亡?」最終結果可能決定加密貨幣會否堅守 cypherpunk 初心,定係變成「區塊鏈化」的傳統數碼金融。

傳統金融要求可逆性 以保障消費者及符合法規

傳統金融機構推動可逆穩定幣交易的背後,是根深柢固的機構要求與監管架構。這些規定數十年來一直用來保障消費者、維護體系穩定,而同區塊鏈的不可逆性產生嚴重衝突,Circle 的 Arc blockchain 就試圖解決呢個矛盾。

銀行需要遵守大量監管規定,必須具備交易可逆功能。例如,Bank Secrecy Act(銀行保密法)要求對可疑活動作出舉報及持續盯緊;OFAC 制裁一律要即時凍結受制裁資產,並保留審計紀錄方便日後解封;消費者保護相關法律(如 Regulation E 及 Regulation Z)賦予消費者「提出爭議和收回款項」的權利,呢啲都變咗現代人認為基本金融權益的一部分。

對傳統銀行來講,這些規定帶來龐大利益:傳統支付系統提供客戶爭議解決機制、可暫停可疑交易之風險管理、可逆交易令合規報告流程更簡單、以及 chargeback 制度可以建立客戶信任及忠誠度。

財政部長 Scott Bessent 強調,穩定幣應該用嚟「鞏固美元全球主導地位」,但同時要喺傳統監管體系下運作。對於佢地嚟講,可逆穩定幣唔係妥協,而係加強版——數碼效率配合金融體系穩定經證明可行的消費者保護。

特朗普總統於 2025 年 7 月簽署的 GENIUS 法案,明文規定所有穩定幣發行商,要有「技術能力依法律要求查封、凍結或銷毀支付型穩定幣」。這個聯邦要求反映政策上已視保障消費者及執法為金融基建必要功能。

國際監管亦正朝這個方向收斂。歐盟《MiCA》法規、日本《支付服務法》、新加坡虛擬資產法規、瑞士加密貨幣監管等,都強調受規範的穩定幣必須具備消費者保護和可逆機制。這種全球一致做法,暗示可逆功能或會成為機構穩定幣採納的標準要求。

傳統金融界主張,不可逆系統對消費者構成無法接受的風險。加密原住民懂得不可逆交易嘅風險,但普羅消費者會預期,金融系統要提供錯誤糾正及防詐機制。銀行用每年靠可逆性追回數十億美元欺詐交易,證明呢啲功能係消費者保護的必要條件。

監管合規好處亦遠不止於保護消費者。可逆交易可強化 AML/CFT,即時介入可疑資金,合規審計紀錄容易追查,建立完善爭議解決流程,同時亦減省合規負擔,全都為穩定幣受機構採用提供巨大誘因。

聯邦監管機構公開表態支持此方向。聯儲局分析指出,穩定幣「因容易出現擠提潮而對金融穩定構成潛在風險」,促請制定全國規範制度,嚴格監察發行人。CFTC 視結構正確的穩定幣為商品,但要求設有消費者保護措施。SEC 於 2025 年 4 月創設「受規範穩定幣」分類,明文支持符合消費者保護條件的發行商。

國會聽證記錄亦見兩黨共識通過消費者保護型穩定幣監管。GENIUS 法案,眾議院以 308-122,以至 18 位參議院民主黨人跨黨投票支持,反映極罕見的兩黨共識:數碼美元基建必須包含傳統金融保護。

國際協調亦鞏固上述要求。國際結算銀行發表穩定幣結算最終性指引,稱「設計妥善並受適當監管後」的穩定幣可促進支付,同時要設消費者保障機制。財政部與主要國際組織協調推動全球標準,確保合規穩定幣體系必須具備可逆功能。

傳統機構認為不可逆的區塊鏈系統,無法履行基本信託責任。銀行對客戶有保障防詐、錯誤更正、在需要時提供協助的責任,以及...maintaining funds availability during disputes. Immutable systems make these responsibilities impossible to fulfill, creating legal and ethical conflicts that reversible stablecoins resolve.

在爭議期間維持資金可用性。不可更改系統令這些責任無法履行,產生法律同道德衝突,而可逆穩定幣就能夠解決呢啲問題。

This institutional perspective views Circle's Arc blockchain as pragmatic evolution rather than philosophical compromise, enabling digital efficiency while preserving essential consumer protections that decades of financial system development have proven necessary.

呢個機構角度將Circle嘅Arc區塊鏈視為實用主義嘅進化,而唔係哲學上嘅妥協,喺提升數碼效率同時,保留咗金融體系數十年發展證明必需嘅基本消費者保障。

Trump administration champions dollar-backed stablecoins while establishing federal oversight framework

特朗普政府一方面大力支持美元支持嘅穩定幣,同時建立聯邦監管框架

The Trump administration has positioned itself as the most crypto-friendly government in U.S. history while simultaneously establishing comprehensive regulatory frameworks that benefit both institutional adoption and American dollar dominance globally. This dual approach creates favorable conditions for Circle's reversible stablecoin experiment while maintaining strict oversight requirements.

特朗普政府定位自己係美國史上對加密貨幣最友善嘅政府,同時建立全面監管框架,既方便機構採用,又鞏固咗美金喺全球嘅主導地位。呢一個雙重策略,為Circle可逆穩定幣嘅實驗創造有利條件之餘,又保持嚴格嘅監管要求。

President Trump's Executive Order 14178, "Strengthening American Leadership in Digital Financial Technology," issued January 23, 2025, establishes core policy priorities including promoting "development and growth of lawful and legitimate dollar-backed stablecoins worldwide," providing regulatory clarity through technology-neutral regulations with well-defined jurisdictional boundaries, explicitly prohibiting Central Bank Digital Currencies, and protecting blockchain development and self-custody rights.

特朗普總統喺2025年1月23日簽發第14178號行政命令《加強美國數字金融科技領導地位》,訂立核心政策優先事項,包括推動全球「合法正規嘅美元穩定幣」發展同增長、透過科技中立式監管帶來清晰監管界線、明確禁止中央銀行數字貨幣,並保障區塊鏈發展同自主管理資產嘅權利。

The administration's Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile, established March 6, 2025, signals unprecedented government-level cryptocurrency adoption. This policy shift reflects Trump's acknowledgment that crypto support serves both economic and political purposes, stating "I also did it for the votes" while emphasizing stablecoins' role in reinforcing U.S. dollar global dominance and driving Treasury securities demand.

政府喺2025年3月6日成立戰略比特幣儲備同美國數字資產庫,標誌住政府級別首次大規模接納加密貨幣。呢個政策轉變,反映特朗普承認支持加密貨幣有經濟同政治雙重作用,佢曾親口表示:「我都係為咗選票」,同時強調穩定幣有助鞏固美金全球主導地位同帶動美債需求。

Key administration appointments demonstrate pro-innovation leadership. David Sacks serves as Special Advisor for AI and Crypto, Bo Hines directs the Presidential Council of Advisers for Digital Assets, and Paul Atkins chairs the SEC with explicitly crypto-friendly policies. These appointments ensure regulatory coordination favoring innovation while maintaining oversight requirements.

主要任命都展現咗親創新立場。David Sacks擔任AI同加密貨幣特別顧問,Bo Hines領導總統數字資產顧問委員會,Paul Atkins出任證券交易委員會(SEC)主席並推行親加密政策。呢啲安排確保監管協調有利創新,但亦保留監管要求。

The GENIUS Act represents the administration's signature cryptocurrency achievement. Passed during "Crypto Week" (July 14-18, 2025) with the Anti-CBDC Surveillance Act and Digital Asset Market Clarity Act, the legislation creates dual federal-state oversight with the Treasury Department as primary regulator, mandates 100% backing with liquid assets, establishes licensing requirements for permitted payment stablecoin issuers, provides consumer protection through priority claims in insolvency proceedings, and requires technical capability to seize, freeze, or burn stablecoins when legally required.

GENIUS法案係政府標誌性加密立法成果。喺2025年7月14-18日「加密週」同時通過,配合《反中央銀行數字監控法》和《數字資產市場明晰法》,建立聯邦與州雙重監管制度,以財政部作為主要監管機構,規定穩定幣必須有百分百流動資產支持,設立發牌要求,破產時保障消費者優先索償權,並要求合法情況下可以技術上查封、凍結或銷毀穩定幣。

The administration views stablecoins as strategic tools for American financial hegemony. Treasury Secretary Scott Bessent emphasizes using stablecoins to "cement dollar dominance globally" by increasing international demand for dollar-denominated assets and Treasury securities. This perspective treats reversible stablecoins not as compromise with crypto principles but as enhancement of American financial power projection through digital channels.

政府視穩定幣為美國金融霸權嘅戰略工具。財長Scott Bessent強調利用穩定幣「鞏固美金全球主導地位」,提升國際對美元資產同美債需求。咁嘅角度,睇可逆穩定幣唔係對加密原則妥協,而係以數碼渠道擴大美國金融實力。

Political motivations align with policy outcomes. Trump's crypto industry support during the 2024 election generated substantial political capital and financial backing. The administration leverages this support to advance policies that benefit American financial institutions while maintaining regulatory control. The resulting framework favors compliant, regulated issuers like Circle over international competitors operating outside U.S. oversight.

政治動機同政策結果一致。特朗普喺2024年大選期間大力支持加密行業,攞到大量政治資本同資金支持。政府利用呢股力量推政策,令美國金融機構受惠之餘繼續有監管主導權。新框架明顯有利於循規蹈矩、受監管嘅Circle等美國公司,多過不受美國監管嘅國際競爭對手。

Congressional passage required significant political maneuvering. The GENIUS Act needed 18 Senate Democrats to cross party lines despite attempts to bar presidential crypto profits and concerns about conflict of interest. The bipartisan support reflects recognition that stablecoin regulation serves national economic interests beyond partisan politics.

法案通過國會過程相當複雜。GENIUS法案要有18位參議院民主黨人跨黨投票,雖然當中有阻止總統透過加密貨幣賺錢、同擔心利益衝突嘅討論,終能得到跨黨支持,反映監管穩定幣符合國家經濟利益,超越政黨之爭。

Federal agency coordination ensures comprehensive implementation. The Working Group on Digital Asset Markets includes Treasury Secretary (Chair), Attorney General, Commerce Secretary, SEC and CFTC Chairmen, Federal Reserve officials, and banking regulators. This structure enables coordinated policy development and enforcement across traditional jurisdictional boundaries. The administration explicitly supports reversible transaction capabilities as necessary infrastructure features. Treasury's August 2025 Request for Comment on "innovative or novel methods, techniques, or strategies that regulated financial institutions use, or could potentially use, to detect illicit activity involving digital assets" signals government interest in controllable digital payment systems.

聯邦機構之間緊密協作,確保全面執行。數字資產市場工作小組包括財政部長(主席)、司法部長、商務部長、SEC及CFTC主席、聯邦儲備及銀行監管部門代表。咁嘅架構方便跨部門協調政策制定同執行。政府明確支持可逆交易功能,視為基建要素。財政部2025年8月就受監管金融機構用於偵測數字資產非法活動的「創新方法、技術或策略」徵詢意見,顯示希望發展可控數字支付系統。

International coordination amplifies American influence. The Treasury Department works with international bodies to establish global standards favoring American-regulated stablecoin issuers. This approach uses regulatory clarity as competitive advantage, enabling Circle and other compliant issuers to expand internationally while foreign competitors face regulatory uncertainty.

國際協作擴大美國影響力。財政部同國際組織合作,建立有利美國監管穩定幣發行商嘅全球標準。利用監管清晰作為競爭優勢,令Circle等守規公司可以放心拓展海外,而海外對手就要面對監管風險。

The administration frames crypto regulation as America First policy. By establishing comprehensive frameworks for dollar-backed stablecoins while prohibiting government digital currencies, Trump positions private stablecoin innovation as patriotic alternative to foreign government digital currencies. This narrative justifies regulatory requirements as necessary tools for maintaining American financial leadership. Enforcement priorities reflect political realities. The administration selectively enforces existing regulations while providing clarity for compliant actors, creating incentives for institutional adoption of approved stablecoin models. This approach benefits Circle's regulated approach while maintaining pressure on non-compliant competitors.

政府將加密監管定性為「美國優先」政策。又訂立美元穩定幣全套監管框架、禁止政府數碼貨幣,特朗普將民間穩定幣創新包裝成對抗外國政府CBDC嘅愛國方案。咁樣做合理化監管要求,保障美國金融領導地位。執法時亦會優先處理政治上重要事項,選擇性執行現有法例同時對守規企業提供指引,鼓勵機構採用認可穩定幣模式。呢套策略對Circle等守規美企有利,同時壓抑不守規對手。

The administration's strategy successfully balances crypto industry support with traditional financial system stability, creating political conditions favoring Circle's reversible stablecoin experiment while ensuring government oversight capabilities remain intact.

整體上,政府策略成功平衡加密行業發展同傳統金融體系穩定,製造有利Circle可逆穩定幣實驗嘅政經環境之餘,又保住政府監管權力。

Goldman Sachs projects trillion-dollar stablecoin markets driven by institutional adoption

高盛預測機構推動穩定幣市場達兆美元規模

Goldman Sachs' research division has issued the most bullish institutional projection for stablecoin growth, forecasting USDC expansion of $77 billion through 2027 representing 40% compound annual growth while identifying trillion-dollar market potential driven by the massive $240 trillion global payments market. This institutional endorsement provides crucial credibility for Circle's reversible transaction experiment.

高盛研究部發表歷來最樂觀機構級穩定幣增長預測,預計USDC至2027年將增長770億美元,複合年增長率達40%,並指出受全球240萬億美元支付市場帶動,穩定幣具備進入兆美元市場規模潛力。呢個機構支持,為Circle嘅可逆交易實驗提供重要認受性。

Goldman's "Stablecoin Summer" research identifies massive untapped opportunity in the global payments market, breaking down the $240 trillion annual volume into consumer payments ($40 trillion), business-to-business payments ($60 trillion), and person-to-person disbursements. Currently, most stablecoin activity remains crypto-trading focused rather than mainstream payments, suggesting enormous potential for expansion into traditional use cases that institutions prefer.

高盛《穩定幣之夏》報告認為,全球支付市場潛力極大,將每年240萬億美元分成:消費者支付(40萬億)、企業對企業(60萬億)、以及個人轉賬。現時,大部分穩定幣主要用於加密交易,未滲透主流支付,反映有巨大空間發展機構偏好嘅傳統應用場景。

The economic mechanics favor stablecoin growth through treasury demand. Bank for International Settlements research demonstrates that 2-standard deviation stablecoin inflows lower 3-month Treasury yields by 2-2.5 basis points, creating beneficial feedback loops where stablecoin growth supports government debt markets. Each stablecoin issued increases demand for backing assets, primarily U.S. Treasuries, aligning private innovation with government fiscal needs.

經濟機制利穩定幣市場壯大,更帶動對國債需求。國際清算銀行研究發現,穩定幣資金流入增長兩個標準差,令3個月美債回報率降低2至2.5點子,形成良性循環(穩定幣發展支持國債市場)。每發行一個穩定幣都增加對背後資產(主要係美國國債)嘅需求,令私人創新同政府財政需要一致。

2024 market performance validates Goldman's optimism. Stablecoins processed $27.6 trillion in annual transactions, surpassing Visa and Mastercard combined by 7.68%. Supply grew 59% reaching 1% of total U.S. dollar supply, with 70% of transaction volume automated and reaching 98% on emerging networks like Solana and Base. These metrics suggest stablecoins are transitioning from experimental technology to essential financial infrastructure.

2024年市場表現印證高盛樂觀預測。全年穩定幣處理嘅交易額達27.6萬億美元,比Visa同Mastercard總和多7.68%。穩定幣供應量增長59%,佔美元總供應約1%;自動化交易量佔70%,新興網絡如Solana同Base用戶自動化交易比率高達98%。呢啲數據反映穩定幣由實驗技術變成重要金融基建。

USDC specifically demonstrates institutional preference patterns. Despite Tether's larger market capitalization ($165 billion vs. Circle's $74 billion), USDC captures 70% of total stablecoin transfer volume, suggesting institutional users prefer Circle's compliance-focused approach over Tether's trader-optimized model. This volume preference supports Goldman's projection that regulated stablecoins will capture institutional growth.

USDC亦表現出機構選擇喜好。雖然Tether市值較大(1,650億美元對Circle嘅740億),USDC卻佔穩定幣總傳送量七成,顯示機構用戶更偏好Circle守規合格、專注合規嘅模式而非Tether偏重炒家取向。呢種趨勢印證高盛對守規穩定幣將吸引機構市場增長嘅預測。

Regulatory clarity accelerates institutional adoption. The GENIUS Act's federal framework and SEC guidance creating "Covered Stablecoin" categories eliminate regulatory uncertainty that previously constrained institutional participation. Circle's full regulatory compliance contrasts with competitors facing enforcement uncertainty, creating competitive advantages that Goldman's analysis incorporates into growth projections.

監管清晰推動機構用戶採納。GENIUS法案建立聯邦監管框架,SEC亦將「受保穩定幣」類別列明,消除咗以往令機構卻步嘅監管不確定性。Circle完全守規,與其他面臨執法風險嘅競爭對手形成對比,呢隻優勢都被高盛納入增長預期。

Circle's financial performance supports aggressive growth targets. Q2 2025 results showed $658 million revenue with 53% year-over-year growth, USDC circulation growth of 90% year-over-year to $61.3 billion, reserve income of $634 million representing 50% year-over-year increase, and adjusted EBITDA of $126 million with 52% year-over-year growth. These metrics demonstrate operational scalability supporting Goldman's expansion forecasts.

Circle財政表現亦支撐住高速增長目標。2025年第二季收入達6.58億美元,按年增長53%;USDC發行量按年增長90%至613億美元;準備金收入6.34億,上升50%;調整後EBITDA 1.26億美元,按年飆升52%。說明公司具可複製經營模式,有利高盛預期嘅增長。

International expansion creates additional growth vectors. Circle achieved MiCA compliance in Europe with EURC, becoming the only major compliant stablecoin in EU markets after Tether chose non-compliance. This regulatory arbitrage creates market opportunities that Goldman's analysis factors into global growth projections.

國際拓展帶嚟進一步增長動力。Circle旗下一歐元穩定幣EURC已合乎歐盟MiCA監管,喺Tether選擇唔合規後,成為歐洲市場唯一受監管主要穩定幣。呢種監管套利打開新市場機會,高盛分析亦已列入全球增長預測。Institutional partnership pipelines validate market demand. Circle announced relationships with over 100 financial institutions, partnerships with traditional payment infrastructure providers FIS and Fiserv, integration with Corpay for cross-border solutions, and cooperation with Standard Chartered/Zodia Markets for institutional trading. These partnerships provide distribution channels supporting Goldman's growth assumptions. Arc blockchain infrastructure addresses institutional requirements that Goldman identifies as adoption barriers. Dollar-denominated gas fees, deterministic finality, built-in FX engines, and regulatory compliance features create institutional-grade infrastructure that current blockchain platforms lack. Goldman's analysis suggests these capabilities could accelerate adoption beyond current market expectations.

機構合作夥伴渠道可以驗證市場需求。Circle 宣布已與超過 100 間金融機構建立合作關係,並與傳統支付基礎設施供應商 FIS 及 Fiserv 建立夥伴協議,與 Corpay 整合跨境解決方案,以及與渣打/Zodia Markets 合作處理機構級交易。這些合作為戈德曼(Goldman)的增長預期提供了分銷渠道。Arc 區塊鏈基礎設施解決了 Goldman 指出的機構採納障礙。以美元計價的 gas 費、確定性終局、內置外匯引擎及合規功能,提供了現時區塊鏈平台所缺乏的機構級基建。 Goldman 的分析顯示,這些功能有可能推動採納速度超出現時市場預期。

Competitive positioning favors Circle's institutional strategy. While Tether earned $13 billion in 2024 compared to Circle's $156 million, Tether's trader-focused approach limits institutional penetration. Circle's compliance-first model accepts lower profitability for broader institutional access, aligning with Goldman's thesis that regulated stablecoins will capture mainstream growth. Economic incentives support Goldman's projections. Federal Reserve research on stablecoin "runs" suggests properly regulated systems with reversibility mechanisms could achieve systemic importance without threatening financial stability. This creates policy conditions supporting massive scale expansion that Goldman incorporates into trillion-dollar market projections.

業務競爭形勢有利 Circle 的機構策略。雖然 Tether 在 2024 年賺取了 130 億美元利潤,而 Circle 只賺取了 1.56 億美元,但 Tether 偏重交易員客群,限制了其機構滲透度。Circle 採用「合規優先」模式,雖然盈利較低,但可以接觸更廣泛的機構客戶,這亦符合 Goldman 所預測:「受監管穩定幣將帶動主流增長」。經濟誘因亦支撐 Goldman 的預測。美聯儲針對穩定幣「擠提」的研究指出,若系統有適當監管及可逆機制,穩定幣有機會達到系統性重要層面,而不會威脅至金融穩定。這創造了有利政策條件,推動穩定幣大規模擴張,因此 Goldman 亦將之納入萬億美元市場預測中。

Technology adoption patterns favor institutional stablecoins. Historical analysis of financial technology adoption shows institutions prioritize compliance and reversibility over decentralization and immutability. Goldman's research suggests stablecoins following this institutional preference pattern will capture disproportionate growth from mainstream financial system integration. Cross-border payment disruption drives adoption. Stablecoin technology reduces remittance costs by 60% compared to traditional methods in markets like Nigeria while providing near-instant settlement versus days for wire transfers. Goldman's analysis identifies these efficiency gains as drivers for institutional adoption across international payment corridors.

科技採納模式支持機構型穩定幣。歷史回顧金融科技採納歷程時發現,機構普遍優先考慮合規及可逆性,重於去中心化及不可更改性。Goldman 的研究指,願意迎合這些機構偏好的穩定幣,有望在主流金融系統整合過程中搶佔不成比例的增長。跨境支付創新推動採納。以穩定幣進行支付,於如奈及利亞等市場可比傳統匯款方法減低 60% 成本,同時提供幾乎即時的結算(對比傳統電匯需時數日)。Goldman 分析顯示,這些效率提升會成為國際支付渠道機構採納的驅動力。

Goldman's trillion-dollar market projection reflects institutional recognition that compliant, reversible stablecoins represent inevitable evolution toward digitized traditional finance rather than revolutionary decentralized alternatives, providing economic validation for Circle's approach.

Goldman 對萬億美元市場的預測,反映出機構層認同「合規且可逆」的穩定幣是傳統金融數碼化的必然發展方向,而非革命性的去中心替代方案,為 Circle 的路線提供經濟驗證。

Privacy features balance institutional confidentiality with regulatory transparency requirements

Circle's Arc blockchain introduces sophisticated privacy mechanisms designed specifically for institutional use cases while maintaining the regulatory compliance capabilities that traditional financial institutions require. This approach represents a middle ground between cryptocurrency's privacy-maximizing technologies and the transparency demands of institutional oversight.

Circle 的 Arc 區塊鏈引入一系列先進私隱機制,專為機構應用場景而設,同時保持現有金融機構要求的合規能力。這種做法介乎主打極致私隱的加密貨幣技術與機構監管強調透明度之間,走中庸路線。

Arc's selective disclosure architecture enables "confidential but compliant" transactions through encrypted transaction amounts while keeping addresses visible. This design allows corporations to conduct private treasury operations and business payments without revealing sensitive financial information to competitors or unauthorized observers, while ensuring regulatory authorities retain oversight capabilities when legally required.

Arc 採用選擇性披露架構,能讓交易金額加密,但保留地址可見,做到「機密但合規」的交易。這種設計容許企業進行保密財資操作或商業付款時,避免敏感財務資料暴露予競爭對手或未授權人士,同時保證監管機構在有法律要求時,仍可保留監督權限。

The technical implementation uses EVM precompiles with pluggable cryptographic backends, providing flexibility for different privacy requirements across various use cases. Unlike privacy-maximizing cryptocurrencies that obscure all transaction details, Arc's approach enables surgical privacy protection for specific data elements while preserving auditability and compliance functionality.

技術上,Arc 採用 EVM 預編譯配合可插拔加密組件,針對不同應用場合提供多樣化私隱需求。與將所有交易資料完全隱蔽的極隱私加密幣不同,Arc 可針對單一數據元素實施精細級別的私隱保護,同時保留審計及合規功能。

Enterprise use cases drive privacy feature development. Corporate treasury operations require confidentiality for inter-company transfers to prevent competitors from analyzing business relationships and financial flows. Banking operations need privacy for settlements between financial institutions to maintain client confidentiality and competitive positioning. Capital markets demand discretion for large-scale transactions that could move prices if publicly observable. Supply chain finance requires protected vendor payment information to prevent supply chain intelligence gathering.

私隱功能設計由企業應用場景主導。企業財資操作需要對集團內部轉賬保密,防止競爭對手分析業務關係和資金流;銀行之間清算則要保留客戶私隱及競爭優勢;資本市場大額交易若被公眾看到,可能影響市場價格,需要足夠隱密度;供應鏈金融亦要保護供應商收款資料,避免被利用作商業情報分析。

Arc's privacy model contrasts sharply with existing cryptocurrency privacy technologies. Zero-knowledge proof systems like those used in Zcash or privacy coins like Monero aim for maximum privacy protection, often creating regulatory compliance challenges. Circle's approach deliberately balances privacy with oversight requirements, enabling institutional adoption while satisfying regulatory frameworks that demand transaction visibility when legally required.

Arc 的私隱模型與現有加密幣私隱技術形成鮮明對比。像 Zcash 的零知識證明系統、Monero 等私隱幣主張極致保護私隱,但經常令合規變得困難。Circle 則有意平衡私隱及監管要求,令機構可安心採納,同時滿足需法定可查的交易透明度框架。

Regulatory compatibility drives design decisions. GDPR's "right to be forgotten" conflicts with blockchain immutability, but Arc's privacy features could potentially address these concerns through selective data encryption rather than immutable public records. AML/CFT compliance requires transaction monitoring capabilities that Arc maintains through controlled privacy mechanisms rather than complete anonymization. The privacy implementation supports graduated disclosure levels based on user requirements and regulatory jurisdiction. Basic transactions can operate with full transparency, while institutional users can opt into amount encryption for sensitive commercial operations. This granular approach enables compliance with varying international regulatory requirements without compromising functionality.

合規兼容性主導設計原則。歐洲 GDPR 的「被遺忘權」與區塊鏈不可更改性有衝突,但 Arc 私隱功能可以透過選擇性加密資料來回應這些疑慮,而非全部資料公開不可改。反洗錢及打擊恐怖分子資金需要追蹤交易,Arc 採用可控式私隱設計,避免完全匿名。其私隱執行方案支援按用戶需求及地區監管作分級披露:一般交易可全透明,機構用戶可選擇對敏感商業金額加密。這種細緻調控方法,可因應不同國際監管要求做調整,同時不損功能。

Circle's privacy philosophy differs from cypherpunk approaches that view surveillance resistance as fundamental human rights. Arc's privacy features serve commercial confidentiality rather than political protection, focusing on business use cases rather than censorship resistance. This institutional orientation reflects Circle's broader strategy of bridging traditional finance and blockchain technology. Compliance-first privacy design maintains regulatory oversight capabilities. Unlike privacy coins that prevent external monitoring, Arc's privacy features include mechanisms for authorized access by regulatory authorities. This "privacy with accountability" model enables institutional adoption while satisfying government oversight requirements that pure privacy systems cannot meet.

Circle 的私隱理念與 cypherpunk(密碼龐克)流派倡議的抗監察人權有所分野。Arc 私隱功能重點是商業保密性,而非常以政治抗審查為訴求,只聚焦於商用場景。這種機構取向,反映 Circle 強調連接傳統金融與區塊鏈的策略。「合規先行」的私隱設計保留監管機構有權管控。與完全杜絕外部監察的私隱幣不同,Arc 私隱功能內建合法監管存取渠道,這種「可問責私隱」模式,讓純商業用戶合規也能享有定制化私隱,而非一刀切的全黑箱。

The technical architecture enables selective revelation for dispute resolution. Arc's reversible transaction mechanisms require access to transaction details for legitimate dispute resolution, creating natural integration points between privacy features and reversal capabilities. This design supports institutional requirements for both confidentiality and dispute resolution without requiring complete privacy sacrifice. Competitive advantages emerge from regulatory-compliant privacy. While privacy-maximizing cryptocurrencies face increasing regulatory scrutiny and potential bans, Arc's measured approach positions Circle to capture institutional users requiring confidentiality within regulatory frameworks. This creates market differentiation from both transparent public blockchains and completely private systems.

技術架構支援有選擇解密,以便爭議解決。Arc 支援交易可逆機制時,需要合法渠道存取交易明細,使私隱功能與可逆特性自然融合。這種設計同時滿足機構對保密及解紛需要,無須放棄全部私隱。合規私隱亦成為競爭優勢。當市面最極隱私的加密幣面對越來越多合規審查甚至禁令,Arc 的中庸路線協助 Circle 捕捉希望在合規下保障資料私隱的機構客戶,亦與徹底開放或徹底封閉的平台區隔開來。

International regulatory frameworks influence privacy feature design. MiCA in Europe, GENIUS Act in the United States, and similar regulations globally require balance between user privacy and regulatory oversight. Arc's architecture enables compliance across multiple jurisdictions through configurable privacy levels rather than one-size-fits-all approaches. Privacy features address institutional security concerns beyond regulatory compliance. Corporate financial flows provide competitive intelligence that privacy protection helps secure. Treasury operations revealing working capital positions could disadvantage companies in negotiations or market positioning. Banking settlement information could enable front-running or market manipulation if publicly observable.

各國監管框架強化了私隱功能設計。歐洲 MiCA、 美國 GENIUS Act 及其他地區法規要求在用戶私隱與監管透明間取得平衡。Arc 架構可因應不同法域設定私隱級別,而非一套通用。私隱功能不僅解決監管合規,更涵蓋企業資訊安全層面。企業資金流屬競爭情報,私隱保護有助守住商業機密。若財資操作透露運作資金狀況,可能令企業於談判或市場定位上處於劣勢;銀行結算資料若全公開,或被人利用作提前交易甚至市場操控。

The integration with traditional financial infrastructure requires privacy considerations that pure public blockchains cannot provide. Banks cannot operate with completely transparent transactions due to client confidentiality requirements and competitive concerns. Arc's privacy model enables blockchain integration while preserving necessary business confidentiality. Circle's approach represents pragmatic evolution of blockchain privacy toward institutional requirements rather than maximal privacy protection, creating tools for commercial confidentiality within regulatory frameworks rather than surveillance resistance technologies favored by cryptocurrency purists.

要整合入傳統金融基建,必須加入純公鏈難以提供的私隱設計。銀行受制於客戶保密規定和市場競爭,根本無法全面透明。Arc 的私隱模式可以保留業務保密所需,配合區塊鏈介接。Circle 的方法是務實地將區塊鏈私隱技術朝機構實際需求演變,不以極致抗監為目標,而是在合規框架下為商業客戶打造專屬的資金流保護工具。

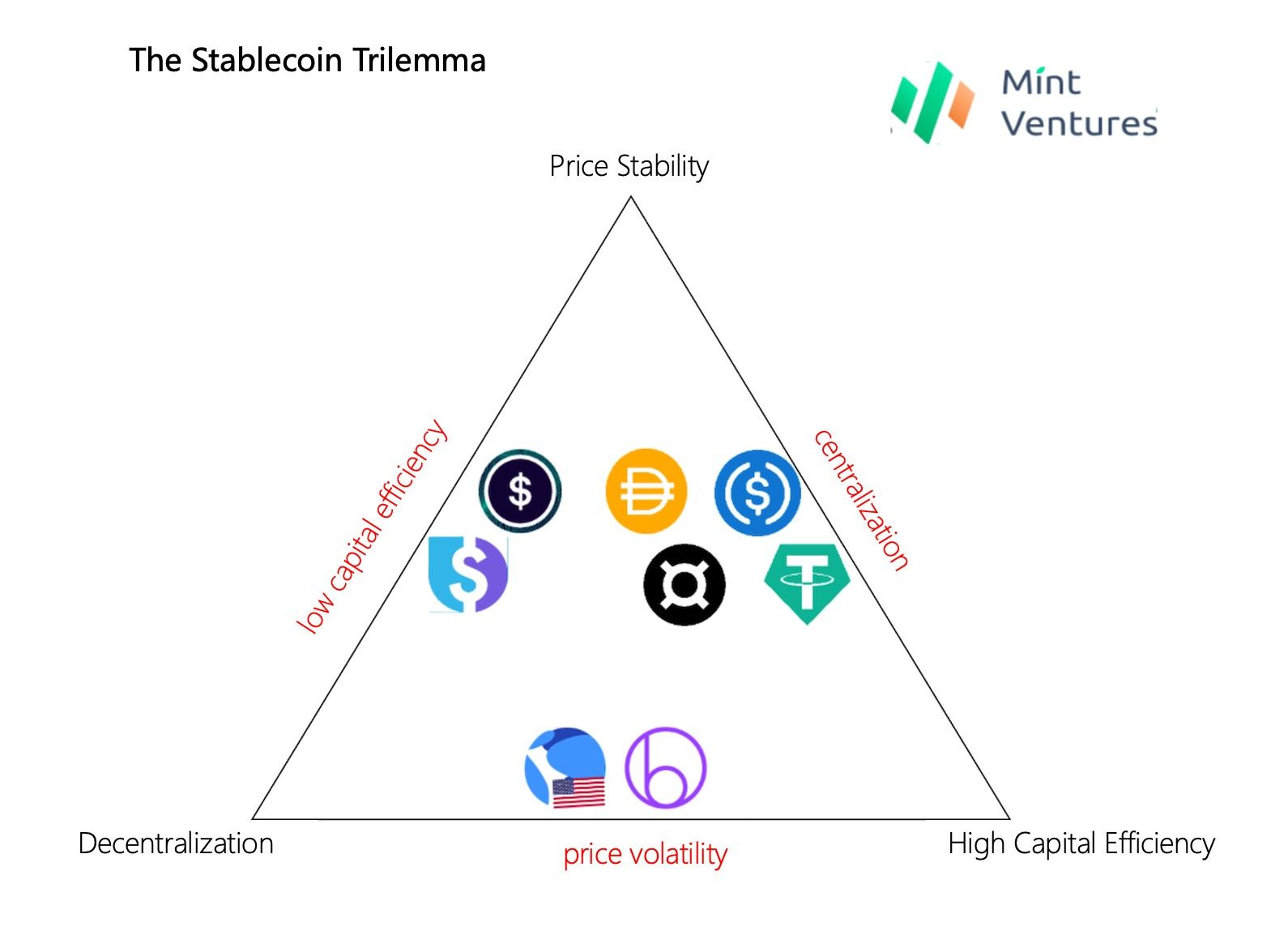

Decentralized stablecoins maintain immutability principles despite institutional pressure

Decentralized stablecoin protocols represent the philosophical counterpoint to Circle's reversible transaction experiment, maintaining blockchain's original immutability principles even as institutional pressure mounts for controllable alternatives. These systems demonstrate alternative approaches to stability and governance that preserve cryptocurrency's censorship resistance while serving major portions of the DeFi ecosystem.

去中心化穩定幣協議正正代表著 Circle 推動交易可逆這類方案的哲學對立面,堅守區塊鏈原初「不可更改」原則,即使機構加強推動可監可控的替代方案依然不改初衷。這類協議展示了在維持加密貨幣抗審查屬性的前提下,如何以不同方式實現穩定性及治理,同時服務 DeFi 生態圈的核心需求。

MakerDAO's DAI exemplifies the immutable approach with approximately $3.4-3.5 billion market capitalization maintained through over-collateralization with Ethereum-based assets. The protocol's governance through MKR token holders provides decentralized control over stability parameters without enabling transaction reversals. DAI successfully maintained its 1:1 USD peg despite an 80% ETH price decline during its first year, demonstrating that immutable systems can achieve stability

以 MakerDAO 的 DAI 為例,其不可更改機制體現在以以太坊為主的超額抵押模式下,市值維持約 34 至 35 億美元。該協議由 MKR 持有人去中心治理,控制穩定參數,但並不容許交易逆轉。即使在成立第一年以太幣價格曾暴瀉八成,DAI 仍能維持 1:1 美元錨定,證明不可更改系統亦可達致穩定性。

(如需翻譯後續段落請再提出!)through economic mechanisms rather than centralized control.

透過經濟機制,而唔係集中式控制。

The DAO's governance model contrasts sharply with Circle's institutional approach. MKR holders vote on collateral types, stability fees, and protocol parameters through on-chain governance rather than corporate decision-making. This distributed control prevents any single entity from reversing transactions or freezing funds, maintaining the censorship resistance that cryptocurrency advocates view as fundamental to the technology's value proposition.

DAO 嘅治理模式同 Circle 嘅機構式做法有好大分別。MKR 持有人通過鏈上治理,投票決定抵押品類型、穩定費同協議參數,而唔係公司決策。呢種分散式控制防止任何單一實體可以反轉交易或者凍結資金,保住咗加密貨幣支持者認為最核心嘅抗審查性,呢個都被視為科技最重要嘅價值主張之一。

Recent controversy within MakerDAO illustrates the community's commitment to immutability. The proposed transition to Sky Protocol's USDS token faced significant community resistance specifically because it included freeze functions that many users viewed as compromising DAI's immutable principles. This rejection demonstrates that even economically rational upgrades may be rejected when they compromise core philosophical commitments.

近期 MakerDAO 入面嘅爭議反映咗社群對不可更改性嘅堅持。建議轉用 Sky Protocol 嘅 USDS 代幣時,就因為入面有凍結功能,唔少用戶覺得破壞到 DAI 唔可更改嘅原則,所以引起強烈反對。呢個拒絕顯示,即使經濟上合理嘅升級,只要損害到核心理念,社群都可能唔會接受。

FRAX Protocol represents innovation within immutable frameworks through its hybrid fractional-algorithmic design combining collateral backing with market-driven seigniorage mechanisms. The protocol maintains dynamic collateralization ratios based on market conditions (currently 96% USDC backing, 4% burned FXS tokens) while preserving transaction immutability. FRAX's broader ecosystem includes decentralized exchanges, lending protocols, and liquid staking offerings that create multiple use cases without requiring centralized control.

FRAX Protocol 喺不可更改框架下創新,佢用混合分數—算法設計,結合抵押資產同市場驅動嘅增發機制。協議根據市場情況動態調整抵押率(目前係 96% USDC 擔保,4% 燒毀咗嘅 FXS 代幣),同時保障交易不可更改。FRAX 更大嘅生態包括去中心化交易所、借貸協議,仲有流動質押服務,全部都唔需要集中式控制就可以實現多元用途。

The technical architecture of decentralized stablecoins enables immutability through algorithmic governance. Automated market operations, liquidation mechanisms, and stability fee adjustments occur through smart contracts rather than human intervention. This automation eliminates discretionary decision-making that could enable transaction reversals while maintaining system stability through economic incentives. Decentralized stablecoin users actively choose immutability over convenience. Despite Circle's USDC offering better regulatory clarity and institutional integration, DAI and other decentralized alternatives maintain substantial market share among users who prioritize censorship resistance over compliance features. This user preference suggests significant market segments will resist reversible alternatives.

去中心化穩定幣嘅技術架構,透過算法治理實現咗不可更改。自動化市場操作、清算機制同穩定費調整全部靠智能合約,而非人手干預。自動化減少咗因酌情決策導致交易有機會被反轉嘅風險,同時用經濟誘因維持系統穩定。用去中心化穩定幣嘅用戶,主動揀咗不可更改,高於方便。雖然 Circle 嘅 USDC 喺監管上更清晰、易乎機構接入,但 DAI 同其他去中心化選擇依然攞到唔少注重抗審查用戶嘅市佔率。呢個用戶傾向顯示,好多市場用家會抗拒可逆轉選項。

DeFi protocol integration favors immutable stablecoins because transaction finality enables complex automated operations without counterparty risk. Lending protocols, yield farming, automated market makers, and other DeFi applications require predictable transaction outcomes that reversible systems could potentially disrupt. The $200+ billion DeFi ecosystem largely depends on immutable stablecoins for operational reliability.

DeFi 協議集成,更加偏好用不可更改穩定幣,因為交易終局性可以支持複雜、全自動操作,無對手風險。借貸協議、收益農場、自動化做市商,同其他 DeFi 應用,全部都要可預測嘅交易結果,如果系統可逆,反而會干擾運作。現時二千億美元 DeFi 生態,絕大部份營運穩定性都依賴著不可更改穩定幣。

Governance token mechanisms provide decentralized oversight without enabling transaction reversals. Token holders can modify protocol parameters, add collateral types, and adjust fee structures through transparent on-chain voting rather than centralized corporate control. This distributed governance maintains community oversight while preserving transaction immutability. Economic incentives align community interests with protocol stability. Governance token holders benefit from protocol success through token appreciation and fee collection, creating market-driven incentives for responsible parameter management. These economic mechanisms replace institutional oversight with decentralized market forces that maintain stability without requiring centralized control.

治理代幣機制提供分散監督,又唔會讓交易可以被反轉。代幣持有人可以通過公開鏈上投票,更改協議參數、加新抵押品、調整費率,而唔會被單一機構壟斷。呢種分布式治理保持咗社群監督,同時保住交易不可更改。經濟誘因令社群利益同協議穩定性一致。治理代幣持有人,因協議成功會受益(如代幣升值、收費分成等),令大家都傾向負責任咁管理參數。呢啲經濟機制用分散市場力量去維持穩定,唔使靠機構監管或集中控管。

Cross-chain expansion of decentralized stablecoins demonstrates continued demand for immutable alternatives. DAI operates across multiple blockchain networks, FRAX has expanded to various chains, and new decentralized stablecoin protocols continue launching despite regulatory pressures favoring centralized alternatives. This expansion suggests robust market demand for immutable options. Technical innovation continues within immutable frameworks. Liquity's LUSD uses algorithmic liquidations without governance tokens, providing stability through purely economic mechanisms. Olympus DAO's OHM experiments with reserve-backed models that maintain decentralization. These innovations demonstrate that immutable stablecoins can evolve technically without compromising philosophical principles.

去中心化穩定幣跨鏈擴展,證明市場對不可更改選擇依然有強勁需求。DAI 支援多條區塊鏈,FRAX 都已經擴展到唔同鏈,而新嘅去中心化穩定幣協議都繼續湧現,即使監管壓力偏向集中式模式都無阻。呢類擴張反映市場對不可更改選項有持續需求。技術創新都無停過:如 Liquity 嘅 LUSD 用純經濟機制進行算法清算,無治理代幣都可以提供穩定性;Olympus DAO 嘅 OHM 則試驗持有儲備,同時保留去中心化。呢啲創新證明不可更改穩定幣一樣可以技術升級,無需犧牲原有理念。

Community resistance to centralized alternatives strengthens over time. As traditional financial institutions increase involvement in cryptocurrency through regulated stablecoins, crypto-native users increasingly value alternatives that maintain original blockchain principles. This cultural preservation creates persistent demand for immutable stablecoins regardless of institutional preferences. Interoperability between immutable and reversible systems remains possible through bridge technologies and atomic swap mechanisms that enable users to choose transaction finality models based on specific use cases. This technical compatibility suggests market segmentation rather than winner-take-all competition between approaches.

社群對集中式選擇嘅抗拒,隨時間只會加強。當傳統金融機構透過監管穩定幣加入市場,本地加密用戶就愈來愈重視維護最初區塊鏈理念嘅可選擇。呢種文化保育,造就唔可更改穩定幣持續有需求,唔受機構口味左右。不過,其實透過橋接技術同原子交換,用戶都可以根據用途,自由揀交易終局性。咁樣唔同模式喺市場可以共存,唔會係贏家通吃。

The philosophical commitment to immutability extends beyond technical implementation to community values, governance structures, and development roadmaps that prioritize censorship resistance over institutional adoption. These deep cultural commitments suggest decentralized stablecoins will persist as alternatives regardless of regulatory or institutional pressures favoring reversible systems. Decentralized stablecoins thus represent the preservation of cryptocurrency's original vision within evolving market conditions, maintaining immutable principles through economic mechanisms and distributed governance rather than institutional compliance and centralized control.

不可更改原則嘅堅持,唔只係技術執行,仲貫穿咗社群價值觀、治理架構同發展藍圖,一切以抗審查放喺機構接納之前。呢啲深層文化承諾解釋到,去中心化穩定幣唔論監管、機構幾咁偏重可逆模式,都會繼續生存。去中心化穩定幣就係市場變化中,保存加密貨幣初心,用經濟機制與分散治理來守住不可更改,而非靠機構合規或中央控制。

Tether maintains market dominance through trading-focused strategy and regulatory arbitrage

Tether 憑着以交易為主策略同監管套利,穩佔市場領導地位

Tether's strategic approach to stablecoin markets contrasts sharply with Circle's institutional compliance model, maintaining overwhelming market dominance through trader-focused services, aggressive international expansion, and selective regulatory engagement that prioritizes market access over comprehensive compliance.

Tether 喺穩定幣市場嘅策略,同 Circle 嘅機構型合規做法有明顯區別。佢靠提供交易員為主嘅服務、進取國際擴張同有選擇性咁應對監管,重點在於市場開放多過全面合規,因此得以繼續壟斷市場。

Tether's market position remains formidable with $165 billion market capitalization compared to Circle's $74 billion USDC circulation, despite Circle's active efforts to gain market share through regulatory compliance. Tether's business model generates substantially higher profits - $13 billion in 2024 versus Circle's $156 million - through more aggressive investment strategies including Bitcoin holdings, commercial loans, and gold reserves that regulatory frameworks increasingly restrict.

Tether 市值依然強橫,市值達到 1,650 億美元,而 Circle 嘅 USDC 只流通咗 740 億。雖然 Circle 積極通過合規搶市,但 Tether 依然嚴重領先市場。Tether 嘅營運模式極高利潤——2024 年有 130 億美元盈利,比 Circle 嘅 1.56 億多得多。呢背後係因為佢投資策略較進取,包括持有比特幣、做商業貸款同黃金儲備—而啲監管規定就愈嚟愈多限制咁做。

The competitive battle reflects different philosophical approaches to stablecoin utility and governance. While Circle actively lobbies for stricter regulations favoring U.S.-based, audited issuers, Tether utilizes political connections and market positioning to resist restrictive legislation. Treasury Secretary nominee Howard Lutnick's role as CEO of Cantor Fitzgerald - Tether's primary banking partner - provides Tether with high-level political access that could influence regulatory outcomes.

呢場競爭反映出兩種穩定幣喺用途同治理上截然不同嘅理念。Circle 積極遊說取締更嚴監管,支持美國本土、有審計嘅發行商。Tether 就靠政治網絡同市場定位,對抗嚴苛立法。舉例話,候任財長 Howard Lutnick 同時係 Cantor Fitzgerald(Tether 主要銀行夥伴)嘅 CEO,提供咗 Tether 高層次政府人脈,有機會影響監管走向。

Geographic market segmentation benefits Tether's strategy. EU MiCA regulation created regulatory advantages for Circle's compliance model, leading to EURC becoming the dominant compliant stablecoin in European markets after Tether chose non-compliance. However, Tether's continued operation in non-regulated jurisdictions maintains global market access that Circle's compliance-focused approach cannot match. This regulatory arbitrage enables Tether to serve crypto-native users while Circle pursues institutional markets.

地域市場分流對 Tether 策略有利。歐盟 MiCA 規管為 Circle 呢種合規穩定幣帶來優勢,令 EURC 喺歐洲市場成為最大規模合規穩定幣,Tether 則選擇唔配合監管。但 Tether 持續喺未受規管地區運作,令佢有全球市場滲透力,而 Circle 嘅合規策略做唔到。監管套利令 Tether 可以專注服務本地加密用戶,Circle 則針對機構市場。

Trading volume patterns favor Tether's approach. USDT captures 79.7% of stablecoin trading volume on average, demonstrating strong preference among crypto traders for Tether's model over Circle's institutional focus. Ethereum-based USDT reserves surged 165% year-over-year, indicating continued growth in Tether's core market segment despite regulatory pressures and compliance concerns.

交易量方面,Tether 明顯佔優。USDT 平均佔穩定幣交易量 79.7%,反映加密貨幣交易者明顯更偏好 Tether 模式多過 Circle 嘅機構取向。以太坊鏈上 USDT 儲備一年內增長咗 165%,即使有監管壓力同合規疑慮,Tether 嘅核心市場仲係持續壯大。

Enforcement activity demonstrates different risk tolerance levels. Tether has blacklisted 1.5 billion tokens across 2,400+ addresses compared to Circle's 100 million across 347 addresses, suggesting more aggressive enforcement of regulatory requirements. However, critics argue that both issuers respond slowly to freezing stolen funds, questioning whether reversibility mechanisms would improve security outcomes or merely create compliance theater.

執行監管方面,亦見風格唔同。Tether 已經喺 2,400 多個地址封鎖咗 15 億個代幣,而 Circle 只係 347 個地址,1 億個代幣。Tether 相對激進執行合規。不過,批評者指出兩間公司都被指對凍結被盜資金反應慢,令大家質疑是否設有可逆機制就能夠改善安全,定只係合規表演。

Tether's reserve structure provides higher yields but creates regulatory vulnerabilities. The company's investment approach includes riskier assets that generate superior returns compared to Circle's conservative cash and Treasury bill strategy. However, these investments face increasing regulatory scrutiny as governments demand full collateralization with liquid assets, potentially forcing reserve restructuring that could reduce profitability. Network distribution strategies reflect different market priorities. Tether operates across multiple blockchain networks with particular strength on Tron and emerging networks where transaction costs remain low for retail users. Circle's multi-chain expansion through Cross-Chain Transfer Protocol focuses on institutional networks and regulated environments, creating complementary rather than directly competitive market positioning.

Tether 儲備結構帶來較高回報,同時增加監管風險。公司嘅投資策略包括較高風險資產,回報自然比 Circle 嘅現金同國債保守策略高。不過,政府對儲備要求愈嚟愈嚴格,要求全數流動資產擔保,有機會逼 Tether 變更儲備結構,影響獲利。再睇分銷策略,Tether 支援更多區塊鏈,以 Tron 同新興低費用網絡最強,方便散戶;Circle 則透過 Cross-Chain Transfer Protocol,多鏈擴展針對機構暨受監管市場,市場定位互補多於直接競爭。

International expansion approaches diverge significantly. Tether's strategy emphasizes emerging markets, particularly in Latin America, Asia, and Africa where regulatory frameworks remain developing and dollar access is limited. Circle's expansion focuses on regulated jurisdictions with established financial infrastructure, targeting institutional customers rather than retail users seeking dollar access. The competitive dynamics suggest market bifurcation rather than winner-take-all outcomes. Tether's trader-focused, yield-maximizing approach serves crypto-native users prioritizing efficiency

國際擴張上,兩者做法大相逕庭。Tether 著重開發中國家市場,特別係拉美、亞洲、非洲嗰啲監管未成熟、美元難接觸嘅地區;Circle 就專注有現成金融體系同監管市場,針對機構客戶,多過搵散戶滿足美元需求。成個競爭局面其實越趨分化,而唔係一方橫掃晒——Tether 嘅交易員取向、極力追求回報策略,更貼近本地加密社群重視高效率。over compliance. Circle's institutional-grade, reversible transaction model targets traditional finance integration. These different value propositions create distinct market segments with limited direct competition.

過度合規。Circle 的機構級、可逆交易模式針對與傳統金融的整合。這些不同的價值主張形成了各自獨立的市場分段,直接競爭有限。

Political developments could reshape competitive positioning. The Trump administration's crypto-friendly policies benefit both issuers but may favor different aspects of their strategies. Tether's political connections through Lutnick could provide regulatory protection, while Circle's compliance model aligns with the administration's emphasis on dollar-backed stablecoin promotion and Treasury demand generation. Market evolution trends suggest continued coexistence. Rising yield-bearing stablecoin adoption (414% surge reaching 3% of stablecoin markets) creates opportunities for both issuers' approaches. Tether's higher-yield strategy could capture yield-seeking users, while Circle's regulatory compliance could access institutional yield opportunities through traditional finance integration.

政治發展可能會重新塑造競爭格局。特朗普政府對加密貨幣友好的政策對兩家發行人都有利,但可能會傾向於它們不同的戰略重點。Tether 透過 Lutnick 的政壇人脈可能獲得監管保護,而 Circle 的合規模式則符合政府鼓勵以美元作為後盾的穩定幣及創造國債需求的方向。市場發展趨勢顯示兩者將繼續共存。收益型穩定幣的採用率急升(大升414%,佔穩定幣市場3%),為兩家的策略都帶來機會。Tether 的高息策略吸引追求收益的用戶,而 Circle 的監管合規則有望透過傳統金融整合開拓機構級收益機會。

Technological differentiation becomes increasingly important. Tether's focus on low-cost transactions across diverse networks serves retail users prioritizing accessibility. Circle's Arc blockchain with reversible transactions, privacy features, and institutional integration serves enterprise users prioritizing compliance and risk management. These technical differences support market segmentation rather than direct competition. Long-term sustainability depends on regulatory evolution. Tether's model assumes continued regulatory arbitrage opportunities and international market access despite compliance costs. Circle's approach assumes regulatory requirements will expand globally, creating competitive advantages for early compliance. The success of each strategy depends on regulatory trajectory and institutional adoption rates.

技術上的分野變得愈來愈關鍵。Tether 專注於在多個網絡提供低成本交易,服務著重無障礙的零售用戶。Circle 的 Arc 區塊鏈主打可逆交易、私隱功能及機構整合,針對重視合規與風險管理的企業客戶。這些技術分別支持市場分段多於直接競爭。長遠可持續性得看監管發展。Tether 的模式假設即使有合規成本,仍有持續的監管套利空間及國際市場准入;Circle 的策略則假設監管要求會全球擴展,令早著先機的合規者有競爭優勢。兩者成敗關鍵在於監管走向及機構採納速度。

The Tether-Circle competition thus represents broader tensions in cryptocurrency evolution between maintaining crypto-native principles and achieving mainstream institutional adoption, with market outcomes likely depending on regulatory developments and user preference evolution rather than technical superiority of either approach.

Tether 與 Circle 的競爭,反映著加密貨幣發展中,堅守原生精神與追求主流機構採納之間的更大矛盾。市場的最終結果,極可能取決於監管變化與用戶偏好如何演變,而未必是單靠任何一方的技術優勢。

Systemic risks emerge from centralization, censorship, and trust vulnerabilities

Circle's reversible stablecoin experiment introduces unprecedented systemic risks to cryptocurrency infrastructure through centralization mechanisms, censorship vulnerabilities, and trust dependencies that could fundamentally undermine blockchain's value propositions and create new attack vectors for malicious actors.

系統性風險源自於中心化、審查及信任依賴漏洞

Circle 推出的可逆穩定幣,透過中心化機制、審查風險及信任依賴,引入前所未有的系統性風險,或會徹底破壞區塊鏈原有價值,並為惡意行為者產生全新攻擊向量。

Centralization risks concentrate power in ways antithetical to blockchain design principles. Arc's permissioned validator set chosen by Circle creates single points of failure where corporate decisions or external pressure could compromise network integrity. Unlike Bitcoin's global distributed mining network or Ethereum's proof-of-stake validators, Arc's institutional validators could face coordinated coercion from governments, regulators, or other powerful entities seeking to control transaction reversals.

中心化風險帶來與區塊鏈設計理念背道而馳的權力集中。Arc 的驗證人由 Circle 挑選,屬於許可制,造成單點故障,一旦企業決策或外部壓力介入,即可損害網絡完整性。與比特幣的全球分散式挖礦或以太坊的權益證明相比,Arc 的機構級驗證人有機會被政府、監管者等有權勢者聯手施壓,以操控交易被否決與否。

The authority to determine transaction reversals creates unprecedented power concentration in Circle's corporate structure. While traditional blockchains distribute consensus across thousands of participants, reversible systems require centralized arbitration for disputed transactions. This arbitration power could become a tool for political control, corporate censorship, or discriminatory enforcement that undermines cryptocurrency's promise of neutral, permissionless finance.

交易是否可逆權力集中於 Circle 公司架構內,達到前所未有的程度。傳統區塊鏈由數千個參與者去分散共識,而可逆系統卻必須集中仲裁爭議交易。這種仲裁權有可能淪為政治操控、企業審查,甚至歧視執法的工具,完全違背加密貨幣無國界、無需許可中立金融的承諾。

Technical attack vectors multiply with reversible transaction mechanisms. Security researchers have identified nearly 200 blockchain-specific vulnerabilities, with approximately half undocumented in public databases. Adding reversibility layers creates additional smart contract complexity and potential failure points including reentrancy attacks on reversal mechanisms, oracle manipulation affecting reversal triggers, governance token attacks targeting reversal decisions, and novel time-based exploits during reversal windows.

可逆交易機制帶來更多技術攻擊向量。資安專家已識別近200個區塊鏈專屬漏洞,當中約一半未有公開記錄。加入可逆層將進一步複雜化智能合約,帶來更多潛在故障點,包括可逆機制的重入攻擊、預言機操控帶來錯誤觸發、針對決定可否逆轉的治理權杖攻擊,甚至創新的時序性利用於可逆期間。

"Reversal gaming" represents entirely new attack classes where malicious actors could exploit reversal mechanisms for double-spending or transaction manipulation. Unlike traditional blockchain attacks that require enormous computational resources or capital, reversal gaming could exploit social engineering, legal manipulation, or bureaucratic processes to achieve unauthorized transaction changes.

「逆轉博弈」帶來全新攻擊類型,惡意用戶可利用可逆機制實行雙重支付或操控交易結果。與傳統區塊鏈攻擊需龐大算力及資本不同,可逆博弈甚至可單靠社交工程、法律及官僚程序去達成未經授權的交易更改。

Government and corporate censorship abuse becomes systematically possible through reversible stablecoin infrastructure. The Federal Reserve Bank of New York's analysis of Tornado Cash sanctions demonstrates how easily blockchain systems face compliance pressure. Reversible stablecoins would be exponentially more susceptible to government-mandated reversals, corporate pressure for politically motivated changes, sanctions enforcement through transaction manipulation, and authoritarian applications enabling political transaction censorship and retroactive punishment through fund seizure.

政府、企業濫用審查更可系統性實現於可逆穩定幣架構。紐約聯儲分析 Tornado Cash 制裁已展示了區塊鏈在合規壓力下的脆弱。可逆穩定幣對政府強制逆轉、企業藉政治施壓、制裁透過交易操作執行,以及威權應用下的政治審查與追溯懲罰(如充公資產等)風險倍增。

Analysis of government surveillance systems, particularly in authoritarian contexts, demonstrates how centralized financial controls enable oppression. Reversible stablecoins could facilitate social credit system integration, political opposition defunding, and retroactive punishment mechanisms that transform financial infrastructure into tools of social control.

分析多國政府監控,特別是在威權情境下,顯示金融中心化可用於壓制人民。可逆穩定幣或使社會信用體系接軌、削資政治異見人士、追溯式懲罰等成真,令金融基建淪為社會管控工具。

Trust dependencies undermine blockchain's fundamental value proposition. Blockchain technology's primary innovation eliminated the need to trust centralized intermediaries through cryptographic verification and distributed consensus. Reversible systems reintroduce trust requirements where users must rely on corporations, governments, and arbitrators to make fair, consistent, and non-political reversal decisions.

信任依賴動搖區塊鏈根本價值。區塊鏈原意是憑密碼學和分布式共識,擺脫對中央中介信任;可逆機制卻重啟了信任需求——用戶要相信公司、政府或仲裁者會作出公平、一致且非政治性的逆轉判斷。

Moral hazard creation represents significant economic risk. Financial analysis identifies that "giving users the sense that transfers can be undone creates moral hazard" that could reduce transaction certainty and encourage riskier behavior. This psychological shift may reduce user diligence in transaction verification, increase fraud attempts by bad actors expecting reversibility, and undermine the careful security practices that blockchain systems require.

道德風險帶來重大經濟危機。學者指出,「讓用戶覺得轉帳可以逆轉會產生道德風險」,降低交易確定性,鼓勵更冒險行為。這種心理變化令用戶驗證交易時變得大意,亦增加壞人利用可逆性行騙的動機,動搖區塊鏈一貫謹慎安全的基本運作。

Systemic risk cascades could amplify throughout interconnected DeFi protocols. Research demonstrates how "a failure of a major stablecoin could trigger cascading liquidations across interconnected protocols." Reversible stablecoins could amplify these risks through uncertainty about transaction finality affecting automated protocols, reversal decisions creating unexpected market volatility, and loss of institutional confidence in cryptocurrency infrastructure reliability.

系統性風險可於互聯 DeFi 協議間層層放大。研究證明「主要穩定幣崩潰可觸發協議連鎖清算」。可逆穩定幣會因交易最終性存疑,影響自動化協議運作;逆轉決定引發意外市場波動,或令機構對加密基建信心大減。

Implementation complexity creates multiple failure modes similar to those observed in algorithmic stablecoin collapses. Complex reversal decisions could deadlock governance systems or be captured by malicious actors. Smart contract bugs in reversal mechanisms could be exploited for large-scale theft. Oracle failures providing data for reversal triggers could be manipulated by sophisticated attackers. Legal and regulatory weaponization risks emerge from reversible infrastructure. Once reversal capabilities exist, governments and corporations may pressure for increasingly broad usage covering political dissent, competitive disputes, or ideological disagreements rather than genuine fraud cases. The precedent of transaction reversibility could expand government financial surveillance and control beyond current capabilities.

實施複雜度亦出現多種失效模式,類似算法穩定幣崩潰。複雜逆轉決定可導致治理死鎖或被黑客奪權;逆轉相關智能合約漏洞可釀大型盜竊;提供逆轉觸發數據的預言機一旦失靈或被操控,後果嚴重。另外,法律與監管被濫用的風險也會因可逆架構而升高。只要逆轉能力存在,政府與企業隨時可推動更廣泛用途,由打擊詐騙擴展至打壓異見、商業糾紛甚至意識形態,交易可逆的先例或會推高政府的財務監控與干預權力。

Privacy violations become systematic through reversal mechanisms. Investigating transaction disputes requires examining private financial information, potentially compromising user privacy for unrelated parties involved in complex transaction chains. This surveillance capability could be abused for non-financial monitoring and control purposes. Market fragmentation and user confusion could destabilize broader cryptocurrency adoption. If some stablecoins allow reversals while others remain immutable, users may make incorrect assumptions about transaction finality, leading to losses and reduced confidence in cryptocurrency systems generally. This confusion could slow mainstream adoption rather than accelerating it.

私隱侵犯亦因逆轉機制變成系統性風險。處理交易爭議時需翻查大量私人財務資料,或令複雜交易鏈中的無關人士私隱受損。這種監控功能甚至可被濫用作非金融性監察與操控。市場分裂與用戶混亂亦削弱加密普及;當部分穩定幣可逆部分不可逆,易令用戶對交易最終性誤判,招致損失,由此降低整體加密貨幣信心,不但無助主流採納,反而拖慢步伐。

International regulatory conflicts could create operational chaos as different jurisdictions demand conflicting reversal requirements. Circle might face situations where reversing transactions to comply with one government creates violations in another jurisdiction, creating impossible compliance situations that threaten operational viability. Long-term trust erosion represents the greatest systemic risk. Cryptocurrency's success depends on users' confidence that the system operates according to transparent, predictable rules rather than arbitrary human judgment. Introducing reversibility mechanisms, even with safeguards, signals that these systems can be changed retroactively, potentially undermining confidence in all blockchain-based financial infrastructure.

國際監管衝突或造成營運大混亂——不同司法管轄區對逆轉交易要求各異,Circle 隨時遇到為了遵從一方法律而違反另一方規則,出現無解的合規困局,嚴重威脅公司存續。更嚴重的是,信任長遠流失才是最大的系統風險。加密貨幣之所以成功,靠的是用戶相信系統按公開、可預期規則運作,而非任意人治。即使設有防線,但一旦引入逆轉機制,意味系統可被追溯性更改,動搖整個區塊鏈金融基建信心。

These systemic risks suggest that reversible stablecoin experiments, while potentially solving some institutional adoption challenges, could create far larger risks to cryptocurrency's foundational value propositions and long-term viability as trustless, censorship-resistant financial infrastructure.

這些系統性風險顯示,可逆穩定幣即使有望解決部分機構採納問題,其實或帶來更大威脅——有可能徹底危害加密貨幣作為去信任、抗審查金融基建的本質價值與長遠可行性。

Future scenarios range from market bifurcation to regulatory capture

The long-term implications of Circle's reversible stablecoin experiment extend far beyond single company strategy, potentially reshaping the entire cryptocurrency ecosystem through market segmentation, regulatory evolution, and technological precedent-setting that could determine whether blockchain technology maintains its decentralized foundations or evolves toward institutionally controlled infrastructure.

Circle 推出可逆穩定幣的長遠影響遠超單一公司策略,隨時重塑整個加密生態。不但涉及市場分裂、監管發展、技術立下先例,更會決定區塊鏈究竟能否保住去中心化根基,抑或走向機構主導的新模式。

Market bifurcation represents

[請註明:「Market bifurcation represents」後全部內容未給出,若需繼續翻譯請提供剩餘英文本。]the most likely near-term outcome with institutional capital flowing toward reversible stablecoins for regulatory compliance while crypto-native users gravitate toward immutable alternatives for censorship resistance. This division would create parallel financial ecosystems serving different user bases with distinct values and requirements. McKinsey research suggests "early coexistence" between TradFi-compatible reversible systems, crypto-native immutable protocols, and hybrid models offering conditional reversibility with strict governance mechanisms.

在可見的未來,最有可能發生的情況,是機構資金為了符合法規要求而流向可逆的穩定幣,同時加密原生用戶則會傾向選擇不可逆、強調審查阻力性的代幣。這樣的分化會造就平行存在的金融生態系,各自服務於擁有不同價值觀及需求的用戶群。麥肯錫的研究指出,與傳統金融兼容的可逆系統、加密原生的不可逆協議及設有嚴格治理機制的有條件可逆混合模式,會出現「早期並存」的局面。

The institutional adoption pathway could accelerate mainstream integration if Goldman Sachs' $77 billion USDC growth projection materializes alongside regulatory requirements mandating consumer protection features. EU MiCA regulations and U.S. GENIUS Act requirements already create framework precedents that could spread globally, effectively mandating reversibility for regulated stablecoin operations. This regulatory forcing function could make reversible features standard requirements rather than optional innovations.

如果高盛對 USDC 成長到七百七十億美元的預測能夠兌現,同時又配合法規對消費者保障功能的強制要求,機構採用穩定幣的路徑將能加速主流整合。歐盟的 MiCA 規管以及美國 GENIUS 法案,已經設下可作全球參考的監管框架,實際上等同強制要求受規管的穩定幣運作必須具備可逆性。這種監管「壓力功能」可能令可逆特性變成標準要求,而非可有可無的創新。

Technical interoperability solutions could enable ecosystem coexistence through bridge protocols supporting both immutable and reversible stablecoins, atomic swap mechanisms allowing users to choose finality models based on specific transactions, and universal stablecoin standards accommodating different settlement characteristics. These solutions could prevent winner-take-all competition by enabling users to access both system types as needed.

技術上的互操作性方案,例如能夠支援不可逆及可逆穩定幣的橋接協議、容許用戶根據不同交易選擇最終性模式的原子兌換機制,以及兼容不同結算特性的通用穩定幣標準,都有助於令兩種生態系共存。這些方案可以避免贏者通吃的局面,用戶可因應自身所需,同時接觸兩種系統。

Regulatory capture scenarios pose significant risks to cryptocurrency's foundational principles. Success of reversible stablecoins could establish precedent for broader blockchain control mechanisms including programmable compliance features in all cryptocurrency applications, government backdoors in smart contract systems, and centralized governance override capabilities across decentralized protocols. This precedent could transform blockchain technology from trustless infrastructure into government-controllable financial surveillance systems.

監管俘獲的情景會對加密貨幣的根本原則構成重大風險。可逆穩定幣一旦取得成功,將有可能為更廣泛的區塊鏈監控機制立下先例,包括:所有加密應用內強制編程合規功能、智能合約系統預留政府後門,以及去中心化協議被中央治理機制越權篡改。這樣的先例,有機會把區塊鏈由無信任基礎設施,扭曲成政府可控的金融監控系統。

International regulatory conflicts could create operational complexity as different jurisdictions establish competing requirements for transaction reversibility, privacy protection, and surveillance access. Circle and similar issuers might face impossible compliance situations where satisfying one government's reversal demands creates violations in another jurisdiction, potentially fragmenting global stablecoin markets along regulatory boundaries.

國際間的監管衝突會大大增加運作複雜度,因為不同司法管轄區可能就交易可逆性、私隱保障及監控權限設有互相衝突的要求。Circle 及相類發行商可能會面對「無法兼容」的法規困局 —— 滿足某地政府的逆轉要求,卻成為另一地區的違規行為,最終可能令全球穩定幣市場按監管邊界分裂。

Technological evolution precedents suggest broader industry transformation. Circle's approach could inspire similar "practical" compromises with blockchain principles across the ecosystem. Other cryptocurrency applications might adopt centralized override mechanisms, compliance-focused governance structures, and institutional-friendly features that prioritize regulatory approval over decentralization. This trend could fundamentally alter blockchain technology's value proposition.

技術進化的先例顯示,整個行業可能會被帶向更大的轉型。Circle 這種做法,或會啟發業界出現更多與區塊鏈原則妥協的「務實」方案。其他加密應用有可能引入中央越權機制、以合規為核心的治理結構,以及各種優先考慮機構需求而非去中心化的特性。這股趨勢,或會從根本上改變區塊鏈技術的價值主張。

Economic incentive realignment could reshape developer and user behavior. If institutional capital flows predominantly to compliant, reversible systems, developers may focus innovation on regulated protocols rather than censorship-resistant alternatives. Users seeking financial services might accept reversibility trade-offs for institutional integration benefits, gradually shifting ecosystem incentives away from decentralization priorities.

經濟誘因的重新分配會改變開發者及用戶的行為模式。如果大多數機構資金傾向投向合規、可逆系統,開發者可能將創新重點放在受監管協議,而非審查阻力型的替代方案。用戶為了可以接入機構級金融服務,也可能接受可逆性帶來的權衡,令生態系統的誘因逐步遠離去中心化這個優先理念。

Cultural transformation risks accompany institutional adoption success. Cryptocurrency's cypherpunk origins emphasized individual sovereignty, privacy protection, and resistance to centralized authority. Mainstream success through institutional compliance could erode these cultural values, transforming cryptocurrency from revolutionary technology into digitized traditional finance with blockchain characteristics rather than fundamental alternatives to existing systems.

若機構成功大規模採用,伴隨而來將會是文化上的轉變風險。加密貨幣原初的Cypherpunk理念重視個人主權、私隱保護,以及抗拒中心化權力。若加密貨幣靠向機構合規而邁向主流,這些文化價值或漸被侵蝕,加密貨幣將由革命性創新淪為內含區塊鏈元素的傳統金融電子化,而非現有體系的根本性替代方案。

Network effects could determine long-term outcomes. If major institutions adopt reversible stablecoins for business operations, smaller users might be pressured to use compatible systems for interoperability. Conversely, if privacy-focused and DeFi applications maintain immutable requirements, institutional systems could face adoption limitations that reduce their competitive advantage.

網絡效應可能會決定長遠的局面。如果大型機構在營運上普遍使用可逆穩定幣,其他用戶或會因為互操作壓力而被迫採用相容系統。相反,若注重私隱及 DeFi 生態持續堅持不可逆需求,機構主導系統的採用率就會受限,競爭優勢相對減弱。

Failure scenarios remain significant possibilities. Technical implementation challenges, governance failures, security vulnerabilities, or loss of community trust could cause reversible stablecoin experiments to collapse. These failures might discredit institutional crypto adoption attempts while validating immutable alternatives, potentially strengthening rather than weakening decentralized systems.

失敗的可能性仍然存在,例如技術實現困難、治理失靈、保安漏洞,或社群信任流失,都可能導致可逆穩定幣的實驗以崩潰告終。這些失敗不單會打擊機構參與加密的努力,反之還會為不可逆替代品增加正面例證,進一步鞏固去中心化系統的地位。

Hybrid evolution could produce compromise solutions combining elements of both approaches. Time-limited reversibility windows providing fraud protection without permanent controllability, opt-in reversal mechanisms requiring explicit user consent, or layered architectures maintaining base-layer immutability while enabling higher-level dispute resolution could satisfy both institutional requirements and crypto principles.

混合型演化也可能出現,產生結合兩種方案元素的折衷解決方式。例如:設有時限的可逆窗口(僅於短期內提供詐騙防護但不實現永久可控)、必須經用戶明確同意才可逆轉的自選可逆機制、或採用分層結構(基層保持不可逆但上層容許糾紛處理),都能夠同時回應機構需求與守護加密原則。

Global geopolitical factors could influence adoption patterns. Countries seeking financial sovereignty might prefer immutable stablecoins resistant to foreign government control, while nations prioritizing international integration might mandate reversible systems compatible with traditional banking. These geopolitical preferences could create regional adoption patterns that fragment global cryptocurrency markets.

全球地緣政治因素亦將影響採用模式。希望維持金融主權的國家或會偏好抗外國控制的不可逆穩定幣,但以國際接軌為先的國家則可能強制使用與傳統銀行兼容的可逆系統。這些地緣選擇可能導致加密貨幣在全球出現區域碎片化的採用格局。

Technological advancement could render current trade-offs obsolete. Zero-knowledge proofs, advanced cryptographic protocols, or novel consensus mechanisms could potentially provide consumer protection without sacrificing decentralization. These innovations could make current reversibility debates temporary challenges rather than permanent feature requirements.

技術發展可望令現時的權衡變得過時。零知識證明、高階加密協議,或全新共識機制,有機會實現既保障消費者,又無須犧牲去中心化的效果。這些創新可能令現時圍繞可逆性的辯論只是暫時性難題,而並非區塊鏈永久性的必備功能。

The ultimate outcome likely depends on user preference evolution rather than technical or regulatory factors alone. If mainstream users prioritize convenience and institutional protection over sovereignty and censorship resistance, reversible systems could dominate through market demand. However, if users value blockchain's original promises of financial independence and trustless operation, immutable systems could maintain competitive advantage despite institutional pressure.

最終結果,很有可能取決於用戶偏好的演變,而非僅僅由技術或監管因素主導。如果主流用戶更重視便利與機構保護,勝於主權與審查阻力,可逆系統就有機會憑市場需求取得主導。反之,假如用戶堅持區塊鏈本來對財務自主與免信任的承諾,雖然機構壓力大增,不可逆系統仍然有力保持競爭優勢。

The next 24-36 months will prove critical as Circle's Arc blockchain launches, regulatory frameworks solidify, and market participants vote with capital allocation between reversible and immutable alternatives. The cryptocurrency ecosystem's future structure - centralized or decentralized, compliant or resistant, institutional or sovereign - hangs in the balance of this fundamental choice between blockchain principles and mainstream adoption requirements.

未來廿四至三十六個月將成關鍵時期 —— Circle 的 Arc 區塊鏈將會推出,監管框架逐步落實,而市場參與者會以資本投入去「投票」選擇可逆或不可逆方案。加密貨幣生態未來是更加中心化定更加去中心化、以合規為主還是堅持抗爭、偏向機構還是偏向主權,以至區塊鏈原則能否對抗主流採用要求,全看這場抉擇。

The defining choice between crypto principles and institutional adoption

加密原則與機構採用之間的抉擇

Circle's reversible USDC experiment represents cryptocurrency's most consequential crossroads since Bitcoin's creation, forcing the ecosystem to choose between preserving its foundational principles of immutability and censorship resistance or compromising those values for institutional adoption and regulatory approval. This choice will determine whether blockchain technology fulfills its revolutionary potential as trustless, sovereign financial infrastructure or evolves into digitized traditional finance with programmable control mechanisms.

Circle 推出的可逆 USDC 實驗,是比特幣誕生以來加密圈最具分水嶺意義的十字路口之一,迫使生態系選擇:是要維護不可逆與抗審查這些根本價值,還是為了機構採用和合規審批而作出妥協。這一場選擇,將會決定區塊鏈技術能否發揮革命性、去信任、主權型金融基建的潛力,抑或最終只會淪為可編程的數碼傳統金融。

The technical innovation behind Arc blockchain demonstrates sophisticated engineering that addresses legitimate institutional concerns through deterministic finality, enterprise privacy features, and dollar-denominated transaction costs. Circle's approach acknowledges that pure immutability creates genuine challenges for error correction, fraud recovery, and consumer protection that traditional financial institutions cannot ignore. The company's success in achieving regulatory compliance and maintaining $65 billion in USDC circulation validates institutional demand for controlled, auditable digital dollar infrastructure.

Arc 區塊鏈背後的技術創新展現精密工程能力,能以確定性最終性、企業私隱功能及以美元計價的交易成本,回應機構的合法顧慮。Circle 的做法承認,純粹不可逆會對糾錯、詐騙處理和消費者保障帶來現實挑戰 —— 這些都是傳統金融不能忽視的問題。公司能成功合規並令 USDC 流通量維持六百五十億美元,亦反映機構對受控、可稽核數碼美元基建的真實需求。

However, the crypto community's visceral negative reaction reflects deeper concerns about sacrificing cryptocurrency's core value propositions for mainstream acceptance. The cypherpunk movement that birthed Bitcoin sought to create alternatives to centralized financial control, not more efficient versions of existing systems. Reversible transactions, regardless of sophisticated implementation, reintroduce the trust dependencies and centralized authority that blockchain technology was designed to eliminate.

然而,加密社群強烈反彈,其實反映更深層次的憂慮:為追求主流採納而犧牲加密貨幣的核心價值。催生比特幣的 Cypherpunk 運動,本意是打造對抗中心化金融管控的替代方案,而不是為現有系統升級效率。無論設計多精密,可逆交易最終都會將區塊鏈本來要剷除的信任依賴及中心化權力重新引入系統。

The regulatory landscape clearly favors systems enabling transaction control through the GENIUS Act's reversibility requirements, MiCA's compliance frameworks, and international regulatory convergence around consumer protection mandates. Traditional financial institutions operate within these frameworks successfully and view reversible capabilities as essential risk management tools rather than philosophical compromises. The Trump administration's support for dollar-backed stablecoins creates political conditions favoring Circle's institutional approach.

現時監管環境明顯傾向支持能實現交易可控的系統,不論是 GENIUS 法案要求可逆、MiCA 的合規架構,還是國際監管趨向在消費者保障上趨於一致。傳統金融機構能在這些體制下有效運作,並不認為可逆是價值妥協,而是必要的風險管理工具。特朗普政府對美元穩定幣的支持,更在政治上強化了 Circle 這種機構方案的優勢。

Market forces suggest bifurcation rather than winner-take-all outcomes. Goldman Sachs' trillion-dollar market projections validate institutional stablecoin demand while decentralized alternatives like DAI maintain strong user bases among sovereignty-focused users. The $27.6 trillion in annual stablecoin transactions demonstrates massive scale that could support multiple approaches serving different market segments with distinct value propositions.

市場力量顯示,更可能是分流而非贏者通吃。高盛對萬億級穩定幣市場的預測,證明機構有真實需求,而去中心化代幣如 DAI 亦在重視主權的用戶群裏保持龐大規模。每年二十七萬六千億美元的穩定幣交易額,也反映市場可同時容納多種方案,各有不同價值主張服務不同的細分市場。

The systemic risks of centralized reversibility mechanisms cannot be dismissed through technical safeguards alone. History demonstrates that financial control tools, once created, inevitably expand beyond their original purposes through political pressure, regulatory mission creep, and authoritarian abuse. Reversible

依賴中心化可逆機制所帶來的系統性風險,不可能僅憑技術保護予以消除。歷史經驗告訴我們,一旦創建了金融監控工具,最終總會因政治壓力、監管範圍不斷擴大或專權濫權,而不斷超越原來的合理用途界線。可逆——stablecoins could become infrastructure for financial surveillance and political control that transforms cryptocurrency from liberation technology into oppression tools.

然而,機構採用方面所面對的挑戰同樣真實。不可逆轉的交易為慣於糾錯同防詐騙機制的銀行、企業同消費者帶嚟不可接受的風險。如果唔透過技術創新或者規管調適去回應呢啲憂慮,加密貨幣可能只會係一種小眾技術,無法成為能夠服務數以十億計用戶的全球金融基礎設施。

哲學層面的影響唔止限於穩定幣市場,更影響加密貨幣嘅文化身份同長遠發展路線。如果可逆交易系統成功,可能會為更廣泛嘅去中心化原則妥協樹立先例,令區塊鏈技術逐步變成政府可以控制嘅基礎設施。如果失敗,就會令堅守原則嘅立場得到認可,但同時限制咗加密貨幣推動者長期承諾嘅主流普及潛力。

根據技術發展、監管演變、用戶偏好變化等等,多種共存嘅情景仍然有可能出現。橋協議可以令不可逆同可逆系統之間實現互通。時限性可逆方案有機會為消費者提供保障,而唔會造成永久性可控。國際監管分裂可能會帶嚟地區性市場區隔,迎合唔同主權偏好。

未來十八個月將會係關鍵期,當Circle嘅Arc區塊鏈推出,各種競爭方案成熟,機構需要作出根本技術選擇,有可能影響生態體系走向以至未來數十年。結果好大程度上會決定,加密貨幣到底能否實現其最初對「無需信任、抗審查」貨幣嘅願景,定還是會發展成為只服務於傳統金融系統目標嘅受監管數字基礎設施。

呢個抉擇其實反映出現代金融體系演化過程裡,個人主權同集體安全、創新同穩定、全球可及同監管合規之間更大嘅張力。Circle今次試驗,測試到底呢啲矛盾可唔可以靠技術創新解決,定係本質上要作出明確價值選擇嘅根本取捨。加密貨幣社群正面臨重要時刻——究竟係接受方便機構採納嘅妥協,抑或堅持極致原則,將決定區塊鏈技術係成為新金融體系基礎,定只不過係提升現有權力結構效率。呢個選擇,關乎金錢未來嘅命運。

Circle推出可逆USDC方案,或者可以成功連結傳統同去中心化金融,推動主流普及同時保留區塊鏈關鍵能力。又或者,呢一刻正正係加密貨幣為咗博取機構認可而失去革命精神。歷史會評價今次務實演化定還是哲學背叛更為正確,但係喺呢個關鍵時刻所作出嘅選擇,將會對未來數十年金融體系發展產生深遠迴響。

今次選擇所帶嚟嘅影響,遠遠超出穩定幣市場本身,涉及人類社會究竟可唔可以創造真正去中心化、抗審查嘅金融基礎設施,抑或任何貨幣體系終究都會被機構同政府集中控制。Circle今次試驗,將會為如何解答呢條攸關文明金融未來的終極問題,提供重要依據。