於 2025 年 10 月 15 日,格林威治時間下午 4:45,Coinbase Markets 發布了一則震撼全球加密社群與交易平台的公告。這家位於三藩市、以嚴謹合規著稱的交易所,將 BNB 正式納入其上市路線圖。這看似普通的業務舉動,卻蘊含極不尋常的象徵意義——BNB 是 Binance 蓬勃區塊鏈生態系統的核心代幣,也屬於 Coinbase 最強勁全球對手的「心臟」。

這則公告發佈僅僅 33 分鐘前,Coinbase 剛推出名為「藍毯計劃」的全新上市機制,旨在簡化和明確其代幣上市流程,允許發行方直接接觸 Coinbase 上市團隊,提升上市過程透明度,並強調交易所對上市及申請全免費用。公布時機絕非偶然。過去數天,加密業界正圍繞上市規則陷入激烈公開爭論,各大平台互指暗地收取不透明費用、偏袒待遇及設置關卡,這些都被普遍認為與加密核心「開放去中心化」理念背道而馳。

爭議於 CJ Hetherington(Coinbase Ventures 支持的預測市場平台 Limitless Labs CEO)公開指控 Binance 向發行方索要大量代幣配額、多次空投及數百萬美元押金作上市條件後迅速升溫。Binance 當即否認指控,批評其「失實及誹謗」,並揚言追究違反保密協議。於此高壓氛圍下,Coinbase Base Layer-2 創辦人 Jesse Pollak 在社交媒體上聲稱「交易所上市應該收費 0%」。有批評者即時反駁,指出 Coinbase 本身並未將市值超過 1,600 億美元的第三大加密貨幣 BNB 上市。

Coinbase 突然而來將 BNB 納入路線圖,似乎正面回應了批評者,卻亦帶來更多疑問。究竟這是誠意推動跨生態合作,還是公關策略以紓緩負面批評?如同許多市值以兆美元計的公司決策,答案或許兩者兼而有之。

翌日清晨,外界熟知的趙長鵬(CZ)公開就 Coinbase 公告作出回應。這位 Binance 創辦人兼前 CEO(2023 年 11 月根據與美方和解協議辭任 CEO、但依然掌控交易所多數股權)感謝 Coinbase 善意舉措,並即時促請其進一步行動。在 X(前稱 Twitter)上,CZ 呼籲 Coinbase 上市更多來自 BNB Chain 生態的項目,指出 Binance 已經上架數個 Coinbase Base 網絡項目,但 Coinbase 卻連一個 BNB Chain 項目也未納入,即使該網絡極為活躍、開發熱烈。

這場交鋒不止於某些代幣,而是一場中心化交易所應如何運作、服務對象及其對整個加密生態應負責任態度的哲學碰撞。Coinbase 與 Binance 的緊張關係已醞釀多年,偶有白熱化,但 2025 年 10 月這一役,將多年積壓的分歧推至聚光燈下,迫使整個產業正視關於權力、透明度、以及中心化基建在去中心化系統未來所扮演角色的尖銳問題。

背景:Coinbase vs. Binance——兩種截然不同的演化哲學

若要理解這則簡單上市公告何以引發巨大回響,必須認識 Coinbase 與 Binance 在創立、發展歷程及策略上的天壤之別。這些差異不僅決定兩者內部運作,亦左右其如何應對監管、用戶、開發者及更大加密生態圈。

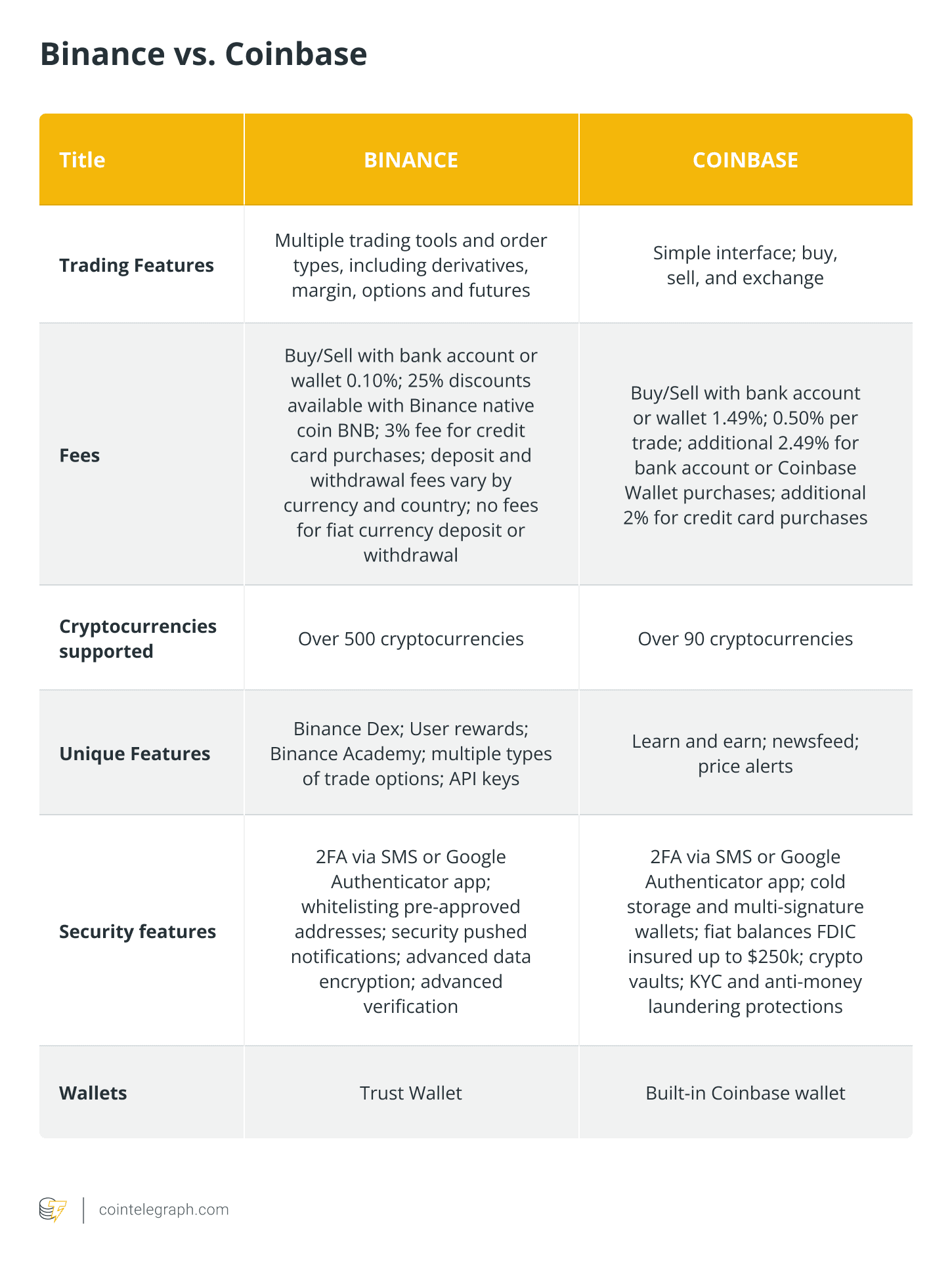

Coinbase 起步於 2012 年三藩市灣區創業文化,由 Brian Armstrong 與 Fred Ehrsam 創辦,獲 Y Combinator 及 Andreessen Horowitz 等知名風投支持。創立初期,公司定位為合規、受監管的數字資產橋樑,連繫傳統金融與加密世界。前 Airbnb 員工 Armstrong 相信,若要數碼資產被大眾接受,必須贏取用戶及機構投資者的信任,因此需有嚴密保安、合規及保險措施。Coinbase 成為首家獲紐約 BitLicense、全美多州發牌及於 2021 年 4 月成功以 COIN 為代號在納斯達克上市的加密交易所。

這種「合規優先」策略,也付出不少代價。Coinbase 的法律及合規團隊規模與工程部門媲美,所有代幣上市均需緊密盡責審查,包括技術評估、監管定性(有否證券風險)、以及聯邦及各州合規規範。交易所因此聲名審慎緩慢,不少符資格項目往往需長達數月甚至數年等待審批,令部分團隊相當沮喪。

Coinbase 歷來傾向重點上架以以太坊和比特幣為主的資產,對其他區塊鏈生態系統代表性有限。直至 2023 年,尚有分析批評交易所既選擇部分「質素成疑」項目上市,卻長期忽略高質素的非 EVM 鏈優秀項目。

Coinbase 過去多年所堅守的監管策略,於 2023 年 6 月迎來嚴峻考驗,美國證交會向 Coinbase 及其母公司提出訴訟,指控其營運未註冊證券交易所、券商及結算機構。SEC 聲稱 Coinbase 上架的 13 款代幣被認定為證券,須根據聯邦法例註冊。

這場訴訟盤旋近兩年如陰雲壓頂,讓 Coinbase 前途未卜,亦明顯拖慢其嘗試新上市或服務的意欲。直至 2025 年 2 月 27 日,SEC 以成立新加密專案小組、希望制定整合規管架構而非單靠執法為由,正式撤回訴訟,這一轉捩令人振奮,也讓 Coinbase 得以重啟更積極的擴張策略,終於將 BNB 列入可上架清單。

Binance 的發跡史則截然不同,由華裔加拿大創業者趙長鵬(CZ)於 2017 年成立,CZ 曾於 Blockchain.info 與 OKCoin 任職。Binance 經由首次代幣發行集資 1,500 萬美元,開業僅五天,中國政府即全面禁止國內加密交易所營運。面對這看似致命打擊,CZ 反其道而行,採取全球無國界模式。Binance 沒有永久總部,團隊遍及數十國,並故意不深植於單一管轄區以避免監管掣肘。

這種策略帶來驚人發展速度。開業六個月,Binance 已成全球最大交易所,幾乎一直穩佔交易量第一。Binance 上市新幣之快,多時每月數十項,覆蓋現貨、期貨、保證金市場。交易所迅速拓展衍生品,最多槓桿倍數達 125x,吸引大量高頻交易及投機用戶。平台自行打造 Binance Chain(後更名為 BNB Chain)、設立風投部(Binance Labs)、孵化初創,涉獵去中心化交易所、NFT 市場以至慈善基金。

快速創新,風險極高。多國監管向 Binance 展開調查,涉及洗錢、規避制裁及違規發售未註冊證券。英國金管局、日本金融廳及德國、泰國等發出警告或限制。2023 年 11 月,Binance 與美國司法部達成 43 億美元罰款協議,為史上少見高額企業刑事罰款。CZ 亦親自認罪... violating the Bank Secrecy Act by failing to maintain an adequate anti - money laundering program, paid a $50 million fine, and agreed to step down as CEO, serving a four - month prison sentence.

違反《銀行保密法》,未有維持足夠的反洗黑錢制度,被罰款5,000萬美元,並同意辭任行政總裁,服刑四個月。

Richard Teng, formerly Binance's regional markets head and before that a regulator at Abu Dhabi Global Market, assumed the CEO role and immediately emphasized compliance as a competitive advantage. Under Teng's leadership, Binance has invested nearly $200 million in compliance programs over two years, expanding its legal and regulatory teams dramatically while implementing enhanced know - your - customer procedures, transaction monitoring systems, and risk management frameworks. The exchange has pursued proper licensing in multiple jurisdictions, including obtaining a Virtual Asset Service Provider license in Dubai and seeking regulatory approval for re - entry into markets like India from which it had been expelled.

Richard Teng,曾任Binance考地區市場負責人,之前在阿布扎比分全球市場監管機構工作,接任行政總裁一職,並即時強調遵規守法係競爭優勢之一。喺Teng領導之下,Binance過去兩年已經喺合規制度投放近2億美元,法務同合規團隊大幅擴充,同時推行加強版「認識你的客戶」流程、交易監察系統同風險管理架構。交易所努力喺多個司法管轄區爭取正規牌照,包括喺杜拜攞到虛擬資產服務提供商牌照,亦都尋求獲印國等被趕出市場的地區批准再次營業。

These divergent paths - Coinbase's early embrace of regulation and Binance's belated compliance transformation - create a complex competitive dynamic. Coinbase can credibly claim to be the most trustworthy, institutionally acceptable exchange for users who prioritize regulatory certainty and established legal protections. Binance counters with broader global reach, deeper liquidity across more trading pairs, and a more extensive ecosystem of services and blockchain infrastructure. Neither approach is clearly superior; each serves different user segments and reflects different assessments of regulatory risk versus growth opportunity.

呢兩間公司嘅路線唔同——Coinbase早早擁抱監管,Binance則後來才著手轉型做合規——造就咗複雜競爭格局。Coinbase可以理直氣壯咁話自己係最值得信賴、最適合重視監管確定性同法律保障用戶嘅主流平台。Binance則打出全球覆蓋更廣、交易對流動性更深,以及完整服務同區塊鏈基建生態圈。兩種路線無優劣之分,各自服務唔同用戶族群,亦反映對監管風險同增長機會嘅不一樣睇法。

The token listing strategies emerging from these philosophical differences have become flashpoints for broader debates about transparency, fairness, and the proper role of centralized exchanges in nominally decentralized systems. Understanding how listings actually work - both technically and commercially - is essential for evaluating the competing claims and criticisms that erupted in October 2025.

由於兩者理念唔同,導致嘅代幣上架策略成為晒更大規模關於透明度、公平性,及中心化交易所在「去中心化系統」入面扮演咩角色嘅社會大辯論焦點。要判斷2025年10月爆發嘅各種聲稱同批評,理解實際上架流程——無論技術還是商業層面——係必要嘅。

Anatomy of a Listing: How Tokens Get on Exchanges

上架解構:代幣點樣可以上交易所?

For outsiders to the cryptocurrency industry, the process by which a digital asset gains listing on a major exchange can seem opaque and perhaps even arbitrary. Why does one token with modest adoption and unclear use cases receive prominent placement while another with substantial user bases and real - world utility remains absent? The answer involves a complex interplay of technical requirements, commercial considerations, legal compliance, and strategic positioning that varies significantly between exchanges.

對圈外人嚟講,數碼資產俾大交易所上架個過程好似極為黑箱、甚至有啲隨機。點解有啲用戶少、用途唔清楚嘅幣可以上架,反而有啲其實好多用家、實體價值明顯嘅幣反而無得上?其實答案涉及技術要求、商業考慮、法律合規同策略部署,各個交易所標準幾乎完全唔同。

At the most fundamental level, listing a token on an exchange requires technical integration. The exchange's infrastructure must be able to communicate with the relevant blockchain, monitor for deposits and withdrawals, handle transaction signing and verification, manage wallet security for potentially millions of users, and provide reliable pricing data feeds. For tokens on major blockchains like Ethereum or Bitcoin, this integration is relatively standardized. Ethereum - based ERC - 20 tokens, for instance, can be added to an exchange with modest engineering effort once the initial Ethereum infrastructure is in place. However, tokens from alternative blockchain ecosystems - Solana, Cardano, Cosmos, or BNB Chain - require more substantial work. The exchange must run full nodes for these networks, implement chain - specific security measures, develop appropriate wallet infrastructure, and ensure adequate technical support for any unique features or upgrade mechanisms.

最基本嘅一點,代幣要上架交易所,首先係要技術對接。交易所技術架構要可以同相關區塊鏈溝通,識得監控入金出金,處理交易簽署驗證,要為幾百萬用戶保障熱錢包安全,同時提供穩定價格數據。主鏈如Ethereum、Bitcoin上面啲代幣,對接較標準化——例如Ethereum ERC-20代幣,只要初步Ethereum架構齊全,加新代幣工程量唔太大。不過如果係Solana、Cardano、Cosmos或BNB Chain咁嘅另類生態圈,工程多得多,交易所要行足全節點,為個別鏈實施特定安全措施,砌合適的熱錢包基建,以及準備技術支援,以應對特別升級或者鏈上功能。

Beyond technical feasibility lies market - making infrastructure, which is absolutely critical for a successful listing. A token that trades with wide bid - ask spreads, low liquidity, or high price slippage will frustrate users and generate negative sentiment regardless of the project's underlying quality. Professional market makers - specialized firms like Jane Street Digital, Jump Crypto, or Wintermute - provide continuous buy and sell quotes that enable smooth trading even during periods of volatility or low retail activity. These market makers evaluate potential listings based on expected trading volumes, volatility profiles, the token's circulating supply and distribution characteristics, and the presence of adequate price discovery mechanisms on other venues.

嶄露技術可行性之後,更關鍵係做市生態。上一隻幣,如果交易時買賣差價闊、流動性低或者滑點高,無論幣本身質素幾好用戶一樣會唔滿意、形成負面觀感。專業做市商,例如Jane Street Digital、Jump Crypto、Wintermute等,負責持續報價,確保即使波動大或零售參與唔多嘅時候都能暢順交易。佢哋會根據預期成交量、代幣波動幅度、流通量及分配,仲有其他平台價發現機制,去評估上架可行性。

Exchanges typically work with projects to ensure sufficient market - making commitments before launching trading. This often involves matching projects with market - making firms, establishing initial liquidity requirements (such as maintaining a minimum spread within certain volume thresholds), and sometimes negotiating technical integrations with specific market - making APIs and systems. The standards vary dramatically. Coinbase has historically demanded substantial market - making depth before listing any asset, contributing to its reputation for slow onboarding but also ensuring that users can trade with minimal slippage. Smaller exchanges may list tokens with far less liquidity support, leading to choppy trading experiences but faster time - to - market for emerging projects.

交易所一般會同項目方協調,等有充足做市承諾先開市。有時係配對項目同做市商、訂立基本流動性條件(例如在某成交量範圍維持最小價差),有時要整合定制API同系統。標準千差萬別。Coinbase一向要求極高做市深度先至會上架,變咗入市慢但用戶易出入、滑點小。細規模交易所則上架前幾乎唔審流動性,方便新項目快出街但成日爆大滑點、成交唔穩。

Regulatory compliance represents perhaps the most complex and consequential aspect of exchange listings, particularly for U.S. - based platforms like Coinbase. The fundamental question hanging over cryptocurrency markets since Bitcoin's inception is whether specific digital assets constitute securities under federal securities laws. The U.S. Supreme Court's 1946 decision in SEC v. W.J. Howey Co. established a test for identifying investment contracts: a transaction involves an investment of money in a common enterprise with profits expected from the efforts of others. Whether a given cryptocurrency meets this test depends on nuanced factors including how it was initially distributed, what representations were made to purchasers, whether there is an identifiable group working to increase its value, and whether purchasers reasonably expect profits from those efforts.

合規係上架最複雜同影響最大部分,特別對美國平台如Coinbase。自從Bitcoin誕生以來,大家都問:到底某啲數碼資產係咪屬於美國聯邦法例下嘅證券?美國最高法院1946年SEC vs. W.J. Howey Co. 案定咗一個標準(Howey Test):投資係咪涉及投資金錢於一個共同事業、依靠他人努力帶來嘅利潤。加密貨幣符合與否,視乎分發方式、賣家對購買者的宣傳、背後有無團隊推動幣價,買家又是否合理預期他人努力會帶來升值。

For Coinbase, the stakes of misclassifying a token as a non - security when the SEC might view it as a security are existentially high. The exchange must conduct legal analysis of each potential listing, often commissioning external opinions from securities law experts, reviewing marketing materials and development roadmaps from project teams, analyzing the token's distribution and governance mechanisms, and assessing precedents from previous SEC enforcement actions or court decisions. This process can take months and sometimes results in the exchange declining otherwise appealing projects due to securities law uncertainty. Binance, operating primarily outside U.S. regulatory reach until its 2023 settlement, historically took a more permissive approach, though it now faces similar constraints given its commitment to proper licensing and regulatory cooperation.

Coinbase如果錯誤將實屬證券資產定義成「非證券」,但SEC又覺得係,就會面臨极高存亡風險。佢哋上架前需要法律分析每個幣,請證券律師外判意見,審查項目方宣傳同發展規劃,研究代幣分配治理細節,仲要對比SEC執法先例,判斷風險。有時這流程可以拖數月,甚至最後只因法律爭議太大,連明顯受歡迎的幣都唔上。Binance之前一直喺美國監管視野外操作,上架寬鬆得多,但自從2023年達成和解,如今都要靠合規同適當牌照,標準更趨嚴格。

Then comes the commercial question: the controversial matter of listing fees and what projects must provide in exchange for exchange access. Here the opacity and inconsistency that characterize the industry become most apparent. Some exchanges explicitly charge listing fees, openly published rate cards that might range from $50,000 for smaller platforms to hundreds of thousands or even millions of dollars for premium placement on major exchanges. Other exchanges claim to charge no listing fees at all but may expect token allocations, marketing partnerships, or other forms of value transfer that accomplish similar ends.

再嚟到商業利益爭議:上架費用同項目方要用乜交換自家資產入場券。呢度最能反映圈內不透明同各行其是。有啲交易所明碼收上架費,小型平台可能五萬美金起,大平台甚至數十萬到百萬美金一個「黃金位」。有啲話唔收費,但實際上收取代幣配額、合作推廣、送貢品之類等值交換,作用一樣。

The public disputes in October 2025 brought these dynamics into sharp relief. CJ Hetherington of Limitless Labs alleged that Binance had requested substantial token allocations and deposits as conditions for listing, claims that Binance vehemently denied while pointing to its long - standing policy of accepting only charitable donations rather than direct listing fees. Meanwhile, prominent figures including Tron founder Justin Sun and Sonic Labs co - founder Andre Cronje claimed that Coinbase had requested listing fees in the tens or hundreds of millions of dollars for their respective projects, contradicting CEO Brian Armstrong's public statements that Coinbase lists assets free of charge. Both exchanges pointed to the other as the true offender, while mid - tier platforms like MEXC, OKX, and Bitget generally avoided the controversy by maintaining quieter stances.

2025年10月嘅公開爭議完全將矛盾拎晒出嚟。Limitless Labs 嘅CJ Hetherington指控Binance要求大額代幣配額同押金先至肯上架,Binance否認,強調自己一向只接受慈善捐款、而唔係正規上架費。另一方面,波場創辦人孫宇晨同Sonic Labs聯合創辦人Andre Cronje都聲稱Coinbase曾要求對佢哋項目徵收數千萬到上億美元上架費,與CEO Brian Armstrong公開話「免費上架」相違。兩大平台互指對方係罪魁禍首,反而MEXC、OKX、Bitget等中型交易所就低調避過風頭。

What emerges from these contradictory accounts is a picture of an industry still finding its way toward standardized, transparent practices. Some patterns seem clear enough. Projects with substantial market capitalizations, proven track records, and strong community demand face favorable listing conditions because exchanges compete to capture their trading volumes and associated fee revenues. Emerging projects with modest user bases face less favorable terms, sometimes involving significant payments or token allocations whether those are labeled as listing fees, marketing partnerships, liquidity provisions, or charitable donations. The specific terms can vary wildly based on individual negotiations, leaving project founders uncertain about what they might encounter and creating opportunities for favoritism or corruption.

種種矛盾爆出一個事實:行業離標準化透明仲有好遠。某啲模式都逐漸固定——市值夠大、歷史業績好、社群用戶需求強嘅項目,交易所有競爭動力搶生意,條件較厚道。相反新興小型項目,面對條件差好多,即使名義唔係「上架費」,但可能要出大筆現金、送配額、做推廣合作、注入流動性或者「慈善捐款」。真正商業條款全靠逐單傾,搞到項目方永遠未知要面對啲咩,變成官商勾結、偏私腐敗溫床。

The absence of standardization reflects crypto's position between worlds. Traditional securities exchanges operate under strict regulations that mandate transparent, non - discriminatory listing standards and prohibit exchanges from making listings contingent on payments from issuers. Commodity exchanges follow similar principles. But cryptocurrency exchanges, operating in regulatory gray zones until very recently, developed more ad hoc approaches that borrowed elements from securities markets, commodity exchanges, traditional financial market - making, and consumer internet platform businesses. The result is a patchwork of practices that sometimes serves users well but frequently generates confusion and controversy.

無標準化正好反映咗Crypto發展介乎兩頭唔到岸。傳統證券交易所規例嚴,必須非歧視式公開上架標準,唔准收項目發行人錢來換上架。商品交易所標準相若。加密交易所一直處於監管灰區,混合證券、商品、做市、互聯網平台業務諸家之長,各自發明野蠻成行,最後變一盤大雜燴,有時用戶得益,有時滿佈混亂同爭拗。

Understanding these technical, commercial, and regulatory dimensions

理解以上呢啲技術層面、商業角力同監管底線—— helps clarify what was actually at stake when Coinbase added BNB to its roadmap in October 2025. This was not simply a matter of technical integration, though that would require work given BNB's role on a non - Ethereum blockchain. It carried symbolic weight about inter - exchange relationships, commercial signaling about zero - fee listing policies, and strategic implications for the competitive positioning of both Coinbase and Binance's respective blockchain ecosystems.

有助於釐清當Coinbase於2025年10月將BNB加入其發展路線圖時,實際涉及的是甚麼利害關係。這不僅僅是技術整合的問題,雖然由於BNB運行於非Ethereum區塊鏈,確實需要作出一些技術工作。這亦具有象徵意義,關乎交易所之間的關係、對零手續費上幣政策的商業信號,以及對Coinbase和Binance各自區塊鏈生態競爭定位的戰略影響。

The BNB Listing Debate: Strategy, Symbolism, and Suspicion

BNB上幣爭論:策略、象徵與疑慮

When Coinbase Markets posted its announcement about adding BNB to the listing roadmap, the crypto community immediately recognized both what was said and what was carefully left unsaid. The announcement specified that actual trading would only commence once "market - making support and sufficient technical infrastructure" were in place, with a separate launch notice to follow. This is standard language for Coinbase's roadmap process, but it matters because roadmap inclusion is far from a guarantee of actual listing.

當Coinbase Markets發佈將BNB加入上幣路線圖的公告時,加密社群立即意識到公告中所講的內容以及刻意避而不談的部分。公告中指出,實際交易只有在“市商支援及足夠技術基礎”到位後才會開始,之後會再有獨立公佈啟動交易。這種措辭屬於Coinbase路線圖流程的標準操作,但這點之所以重要,是因為進入路線圖絕不等同保證真正上幣。

Coinbase's roadmap mechanism serves several purposes simultaneously. It signals to the market that the exchange is evaluating a particular asset, potentially affecting price discovery and generating positive sentiment for the token in question. It provides transparency to projects and users about what might be coming while giving Coinbase flexibility to delay or decline if circumstances change. And it allows the exchange to gauge community interest and gather feedback before making final commitments. Historical precedent shows that tokens can remain on the roadmap for extended periods - sometimes months or even years - while the exchange works through technical integration, liquidity arrangements, or compliance reviews. Some tokens listed on roadmaps have ultimately never launched for trading at all when Coinbase determined they failed to meet evolving standards.

Coinbase的路線圖機制同時有多重作用。它向市場發出訊號,表明交易所正在評估某一資產,或會影響價格發現,亦能為該Token帶來正面氛圍。這一機制為項目方及用戶增加未來預期的透明度,同時讓Coinbase在情況轉變時可選擇押後或終止上幣。再者,Coinbase可以利用這階段收集社群意見及評估市場反應,然後才作最終決定。有過往例子顯示,有些代幣會在路線圖上停留很長時間——有時甚至以年計——期間交易所需處理技術整合、流動性安排或合規審查。有些放在路線圖上的代幣最終從來都沒有在Coinbase正式上架交易,因其未能通過不斷更新的標準。

For BNB specifically, the technical challenges are non - trivial. Unlike most major cryptocurrencies available on Coinbase which exist on Ethereum or Bitcoin's networks, BNB functions as the native gas token for BNB Smart Chain, an independent blockchain that uses a Proof of Staked Authority consensus mechanism. Coinbase would need to implement full node infrastructure for BNB Chain, develop appropriate wallet systems, ensure adequate transaction monitoring and security controls, and potentially integrate with Binance's ecosystem more broadly. These technical requirements, while certainly manageable for an exchange of Coinbase's sophistication, require dedicated engineering resources and thorough security audits before launch.

針對BNB,本身的技術挑戰並不簡單。不同於Coinbase上大多數主流加密幣都存在於Ethereum或Bitcoin網絡,BNB則是BNB Smart Chain的原生燃料代幣,該鏈本質上是獨立運作,並使用權益委託證明(Proof of Staked Authority)共識機制。Coinbase需要建立BNB Chain的完整節點基礎設施、開發相應的錢包系統、確保交易監控及安全措施,甚至可能需要更全面地與Binance生態整合。儘管這些技術挑戰對Coinbase這類大型交易所而言可以應付,但都需要專責工程團隊資源及完善的安全審核。

The market - making requirement introduces additional complexity. BNB trades with enormous liquidity on Binance itself, obviously, where it serves as the base trading pair for hundreds of markets and benefits from the exchange's vast user base. But its liquidity on other major exchanges has been more limited, partly because competitive dynamics discouraged rivals from providing Binance's token with prominent placement. When Kraken listed BNB in April 2025, that represented a significant shift in inter - exchange dynamics, signaling that major platforms were increasingly willing to cross - list competitor tokens when user demand justified it. For Coinbase to follow suit required arranging for market makers willing to provide competitive quotes without the natural liquidity advantages Binance enjoys.

市商機制的要求又再增加技術層面的複雜性。BNB在Binance本身當然具有極高的流動性,作為數百個市場的基礎交易對,配合龐大用戶基礎。但在其他主流交易所的流動性則相對有限,部分原因是競爭格局令其他交易所不願明顯地為Binance的代幣提供高曝光度。當Kraken於2025年4月上架BNB時,就反映出交易所之間關係出現明顯變化,顯示主流平台在面對用戶需求時,愈來愈願意跨所上幣競爭對手的Token。Coinbase若要跟隨,必須部署能夠提供具競爭力報價的市商,而沒有Binance自然享有的流動性優勢。

CZ's public response to Coinbase's announcement revealed the strategic thinking underlying his request for more BNB Chain listings. His statement thanked Coinbase for adding BNB but immediately pivoted to urging broader ecosystem support. The logic was straightforward: if Coinbase truly believes in openness and zero - fee listing policies, merely adding the base token BNB represents only a token gesture - pun intended. What would demonstrate genuine commitment to cross - ecosystem collaboration would be listing the applications, protocols, and projects built on BNB Chain, treating that ecosystem with the same seriousness and openness that Coinbase presumably applies to Base, its own layer - 2 network.

CZ對Coinbase公告的公開回應,顯示出他呼籲擴大BNB Chain生態應用上幣的戰略盤算。他發聲感謝Coinbase加入BNB,但即時轉而促請Coinbase支持更廣泛的生態。他的理據很直接:若Coinbase真相信開放及零上幣費政策,僅僅加上了平台Token BNB,其實只是「做個樣」——語帶雙關!真正展示跨生態合作誠意,是要讓在BNB Chain上開發的各種應用、協議及項目可以上架,把BNB Chain生態視為與Coinbase自家Layer 2 Base同樣重要、同樣開放來對待。

The comparison CZ drew was pointed. Binance had indeed listed several prominent Base ecosystem projects, providing trading access for tokens from Coinbase's own blockchain platform. Yet Coinbase had not reciprocated by listing projects from BNB Chain, despite that network's substantially larger total value locked, greater developer activity, and longer operational history compared to Base which only launched in August 2023. This asymmetry, CZ suggested, revealed something about Coinbase's stated commitment to openness. Was the exchange truly neutral in its listing standards, or did competitive considerations influence which ecosystems received support?

CZ的對比相當尖銳。事實上Binance確實上架了多個Base生態主要項目,為Coinbase自家公鏈項目提供交易渠道。反觀Coinbase卻遲遲未將BNB Chain相關項目上架,即使該網絡在總鎖定價值、開發者活動和運作資歷上遠超只於2023年8月啟動的Base。這種不對稱,CZ認為其實反映Coinbase聲稱的開放原則,是否真的在執行——交易所的上幣標準真有中立性?抑或競爭考慮已經決定了哪些生態獲得支援?

Public and expert commentary on this exchange reflected the deep divisions within the crypto community about exchange power and responsibility. Some observers praised Coinbase's BNB listing as a mature, industry - minded decision that recognized users should have access to major digital assets regardless of which exchange originally promoted them. This perspective held that exchanges serve users best by maximizing choice rather than engaging in petty rivalries that artificially segment markets and reduce competition. Listing BNB, by this logic, acknowledged that the token's $160 billion market capitalization and genuine utility within DeFi applications made its absence from Coinbase unjustifiable.

各界及專家對這一來回論戰的評論,反映出加密貨幣圈內對交易所權力與責任的巨大分歧。有些人稱讚Coinbase納入BNB是成熟且以產業發展為本的決定,肯定用戶應有權接觸主流資產,不論當初屬於哪一交易所主導。這種看法認為,平台應致力於令用戶選擇最多化,而不是陷入小圈子競爭、將市場人為分割、降低整體競爭。以這種邏輯,BNB無論市值有$1,600億美元,還是在DeFi應用上具有實用性,都令其缺席於Coinbase難以合理解釋。

Others viewed the move more cynically as calculated public relations designed to deflect criticism during the heated October 2025 debate about listing transparency. Coinbase faced accusations that its stated zero - fee policy masked other barriers to listing including slow processing, stringent requirements that effectively excluded many qualified projects, and potential bias toward its own ecosystem. By suddenly adding BNB to its roadmap hours after launching the Blue Carpet initiative, Coinbase could claim it practiced the openness it preached. But whether this would translate into actual BNB trading availability or meaningful support for BNB Chain ecosystem projects remained unclear.

亦有不少人認為,這純粹是精心計算的公關操作,旨在2025年10月熱烈討論交易所公開透明度時,將更多批評引導開去。Coinbase被指雖自稱零上幣費,但其實設有其他障礙,例如審核慢、要求嚴格到將許多有質素的項目排除在外,甚至在上幣上偏袒自家生態。Coinbase在藍地毯(Blue Carpet)計劃公佈後幾小時就把BNB加進路線圖,即時就有「以行動證明我們很開放」的PR效果。但最後這舉動能否落實BNB交易開放、或實際提升BNB Chain項目上幣,仍然成疑。

A third perspective, perhaps the most cynical, suggested both exchanges engaged in strategic theater for competitive positioning without genuine commitment to openness. Under this view, Binance's listing of Base projects served its own interests by capturing trading volumes and demonstrating ecosystem neutrality while the actual projects selected remained relatively small and non - threatening. Similarly, Coinbase's BNB roadmap listing provided PR benefits while the careful hedging about market - making and technical requirements preserved flexibility to delay indefinitely if Coinbase concluded that providing premium support for a competitor's token was strategically unwise.

還有第三個觀點,或許是最為冷淡的一種,認為兩間交易所都是「策略性演技」,純粹為了競爭定位而在做場面,對開放態度毫無真正承諾。照這種說法,Binance讓Base項目上架,其實是穩包額外交易量而顯示好像生態開放,然而上架的項目相對細規模、威脅性有限;同樣地,Coinbase將BNB納入路線圖獲取正面宣傳,但又用大量條件限制(例如流動性及技術要求)來預留「彈性」,實際上如判斷不利自身利益,隨時可以無限期拖延或取消。

The debate also intersected with broader concerns about the concentration of power in centralized exchanges and whether their increasing gatekeeping influence contradicted cryptocurrency's original vision. Coinbase and Binance together control the vast majority of global cryptocurrency trading volume across spot and derivatives markets. Their listing decisions can make or break projects, influence token prices dramatically, and determine which blockchain ecosystems gain mainstream adoption. This power creates natural incentives to favor vertically integrated ecosystems - Base for Coinbase, BNB Chain for Binance - even when they claim to apply neutral, merit - based standards.

這場爭論同時涉及外界對中心化交易所權力高度集中的深層憂慮,即這些平台在把關上的日益壟斷是否違背加密貨幣的原初理念。Coinbase與Binance合共掌控全球大部分現貨及衍生品市場的交易量。他們的上幣決策足以成就或摧毀項目、對Token價格造成劇烈波動,並主導哪些公鏈生態得以主流化。擁有這種權力,自然會誘使平台偏袒本身垂直整合生態——Coinbase有Base,Binance有BNB Chain——不論他們聲稱的標準多中立或按質論。

As October 2025 progressed, the BNB price action following the Coinbase announcement told its own story. The token initially jumped approximately 2% on the news, reflecting immediate positive sentiment. But this gain quickly evaporated as BNB fell back and actually declined over subsequent days, down more than 11% from its all - time high of $1,370 reached just days before the Coinbase announcement. Some analysts attributed this decline to profit - taking after the news. Others suggested that investors recognized the gulf between roadmap listing and actual trading availability, tempering their enthusiasm. Whatever the explanation, the muted market response underscored how the symbolic significance of the announcement outweighed its immediate practical impact.

及至2025年10月,Coinbase公佈消息後BNB的價格走勢亦自有說法。消息公布當下Token一度升約2%,反映市場即時正面情緒,但升幅瞬間消失,BNB之後回落,更在數日內從公佈前不久創下的$1,370歷史高位下跌超過11%。一些分析認為這是「利好出貨」獲利回吐所致;另有意見認為,投資者很快意識到「加進路線圖」與「真正可以交易」之間仍有重大落差,因而態度保守。無論原因如何,這種淡靜市況也反映,消息背後的象徵意義遠大於短期實際效果。

Transparency vs. Gatekeeping: Competing Listing Philosophies

透明度對守門人:兩大上幣理念之爭

The October 2025 controversy brought to the surface competing visions of how cryptocurrency exchanges should make listing decisions and what obligations they bear toward openness and fairness. These visions reflect broader ideological tensions within the crypto space about the proper balance between decentralization ideals and practical realities of building sustainable businesses.

2025年10月的爭議暴露出業界對加密貨幣交易所如何決定上幣,以及他們在開放與公平上的責任,有著根本不同的理念。這背後其實反映整個加密圈一直盤旋不去的矛盾——去中心化理想與建立可持續企業的現實如何平衡。

Binance's critics focus on allegations of high or undisclosed listing fees, preferential treatment for projects willing to provide substantial token allocations, and centralized control that allows the exchange to pick winners and losers based on opaque criteria. The accusations from CJ Hetherington of Limitless Labs, while vigorously denied by Binance, fit a pattern of complaints from projects that have described feeling pressured to provide payments or tokens in exchange for listing consideration. Some projects allege that Binance demanded up to 15% of total token supply, amounts that could run into tens or hundreds of millions of dollars in value for successful projects. Even if Binance labels these arrangements as marketing partnerships, community airdrops, or charitable donations rather than listing fees per se, critics argue the economic substance remains the same: projects must transfer substantial value to gain exchange access.

Binance的批評者,集中在對其高昂或不公開上幣費、對願意分配大量Token的項目有優惠待遇,以及中心化流程可按不透明標準選出“贏家與輸家”這些指控。Limitless Labs‘ CJ Hetherington 的公開指責(雖被Binance強烈否認),其實與不少項目「感受到被壓力要求支付Listing贊助或Token」的指控如出一轍。有項目方更稱Binance曾要求高達15%代幣總供應,對成功項目來說動輒值幾千萬、甚至過億美元。即使Binance把安排包裝成市場合作、社群空投、或慈善捐贈而非直接上幣費,批評者認為本質一樣——項目必須向平台轉讓可觀價值,才能登上交易所。

Binance's defense rests on several pillars. First, the exchange maintains that it charges no mandatory listing fees and bases decisions on rigorous due diligence evaluating projects' technical quality, team credentials, market potential, and compliance with regulatory requirements. Any token allocations or airdrops, according to this framing, are voluntary arrangements that many projects propose themselves for marketing purposes rather than requirements imposed by the exchange. Second, Binance points to its track record of listing numerous projects including many that provided no payments or allocations whatsoever, demonstrating that commercial considerations are not determinative. Third, the exchange emphasizes that its listing pace - historically adding dozens of new tokens monthly - far exceeds competitors like Coinbase, suggesting that if anything Binance errs on the side of inclusiveness rather than restrictive gatekeeping.

技術質素、團隊資歷、市場潛力,以及合規監管要求。根據呢個角度,任何代幣分配或空投都係自願安排,係好多項目自己提出作為推廣用途,而唔係交易所設下嘅強制要求。其二,Binance 指出佢有上架大量項目,而入面好多野冇俾過任何費用或分配,證明商業考慮唔係決定性因素。其三,Binance 強調,佢一向每個月都加幾十隻新代幣,速度遠超似 Coinbase 嘅對手,反映 Binance 寧願包容多啲,而唔係設立高門檻限制入場。

Co - founder Yi He has been particularly vocal in defending Binance's practices, arguing that the exchange maintains transparent policies and that rumors about exorbitant fees constitute FUD - fear, uncertainty, and doubt - designed to damage Binance's reputation. She notes that Binance has accepted charitable donations since 2018, with project teams determining contribution amounts voluntarily rather than Binance imposing minimums. The exchange also points to its extensive compliance investments following the 2023 settlement with U.S. authorities, suggesting that current policies reflect reformed practices aligned with regulatory expectations.

聯合創辦人何一就更加積極出聲為 Binance 辯護,指出交易所政策透明,關於高昂上幣費嘅傳言只係 FUD(恐懼、不確定、懷疑)——目的係抹黑 Binance 嘅聲譽。佢又提到 Binance 從 2018 年開始接受慈善捐款,每個項目團隊都可以自願決定捐多少,而 Binance 並無設下最低金額。交易所同時強調自 2023 年與美國當局達成和解後,已大幅投資加強合規,現行政策係配合監管期望嘅改革措施。

Yet even sympathetic observers note tensions within Binance's position. The exchange operates different listing tracks including spot markets, futures contracts, and innovation zones with varying requirements and visibility. This complexity creates opportunities for preferential treatment even if Binance denies that fees determine outcomes. Projects report vastly different experiences, with some encountering smooth processes and others describing protracted negotiations over financial arrangements. The lack of published, standardized criteria makes it impossible for outsiders to verify whether listings truly reflect merit - based assessments or whether commercial factors play determinative roles.

即使係同情 Binance 嘅觀察者都認為其中存在矛盾。Binance 有多種上架渠道,例如現貨市、期貨合約同創新區,每種都有唔同要求同曝光度。呢種複雜性,令偏袒個別項目成為可能,儘管 Binance 否認費用決定上架。唔同項目團隊對上架體驗反應差距好大,有啲流程順利,有啲就話要傾長時間,尤其係財務安排。因為冇公開同標準化嘅上架規則,局外人根本唔知審核到底係根據實力,定其實一樣睇商業利益。

Coinbase faces a distinct set of criticisms despite its claims to transparency and zero - fee listing. The exchange's slow pace of new token additions frustrates projects that believe they meet Coinbase's quality standards but find themselves waiting months or years for evaluation outcomes. Coinbase has listed fewer than 500 cryptocurrencies total across its history, compared to the thousands available on Binance. This selectivity might reflect rigorous quality control and compliance diligence, or it might reflect excessive caution bordering on gatekeeping that privileges established projects over innovative upstarts.

Coinbase 即使標榜透明同零申請費,亦避免唔到唔同批評。佢上新代幣嘅步伐極慢,唔少認為符合 Coinbase 標準嘅項目都要等好耐先有結果,有曾等足幾個月甚至幾年。過去 Coinbase 總共只上架咗唔夠 500 隻幣,比起 Binance 幾千隻少得多。呢啲嚴選可能代表高質量及合規,但亦可能係過度謹慎,變成設門檻屏蔽新創項目,令已建立地位嘅更易入場。

The limited chain diversity on Coinbase represents another common complaint. For years, the exchange focused overwhelmingly on Ethereum - based tokens and Bitcoin, with modest representation from other blockchain ecosystems. Projects from Solana, Cardano, Cosmos, and other platforms struggled to gain Coinbase listings even when they achieved substantial market capitalizations and user adoption elsewhere. Critics attributed this to Coinbase's technical conservatism and regulatory risk aversion rather than principled quality assessments. Some suggested that Coinbase deliberately maintained higher barriers for ecosystems that might compete with Ethereum, reflecting the exchange's close alignment with the Ethereum ecosystem.

Coinbase 缺乏鏈多樣化亦係常見批評。多年嚟,佢主要集中上架 Ethereum token 同埋 Bitcoin,其他公鏈出現得極少。Solana、Cardano、Cosmos 等平台嘅項目,就算外面市值大、用戶多,都好難入 Coinbase。批評認為,呢種情況主因係 Coinbase 技術保守,對監管風險過度敏感,而唔係真係從項目質素出發。有啲人甚至質疑 Coinbase 有意針對同 ETH 競爭嘅公鏈設置更高門檻,顯示佢與 Ethereum 生態關係密切。

Furthermore, allegations that Coinbase requests substantial listing fees directly contradict CEO Brian Armstrong's public statements but persist from credible sources. Justin Sun's claim that Coinbase requested $330 million in various fees to list TRX, and Andre Cronje's statement that Coinbase sought $60 million for FTM, paint a picture inconsistent with zero - fee rhetoric. Coinbase has not publicly responded to these specific allegations with detailed rebuttals, leaving the contradictions unresolved. Even if the exchange technically charges no listing application fees, if it demands other forms of payment or commercial arrangements, the practical effect remains the same for projects seeking access.

另外,坊間流傳 Coinbase 索取巨額上幣費用嘅指控,雖然與 CEO Brian Armstrong 標榜免費上架言論矛盾,但不少可信來源都曾爆料。孫宇晨聲稱 Coinbase 要求 TRX 各種費用加埋高達 3.3 億美元,而 Andre Cronje 就話 FTM 上架要 6,000 萬美元。呢啲講法同 Coinbase 零費用嘅宣傳格格不入,但 Coinbase 一直都冇公開詳細反駁。即使技術上唔收申請費,如最終需要透過其他方式俾錢,對項目實際效果都一樣。

Third - party research from firms like Messari, CoinGecko, and The Block has attempted to analyze listing practices more systematically, but perfect transparency remains elusive. These organizations track which tokens appear on which exchanges, price impacts around listing announcements, and liquidity characteristics, but they cannot directly observe internal decision - making processes or commercial negotiations. What emerges is a picture of an industry where stated policies and actual practices sometimes diverge, where individual negotiations produce highly variable outcomes, and where competitive pressures create incentives for opacity rather than transparency.

第三方分析機構如 Messari、CoinGecko、The Block 等有嘗試系統化分析上幣情況,但完全透明仍然好難做到。佢哋會追蹤邊隻幣上咗邊間交易所、公告前後幣價變化、流動性等等,但內部決策同商業談判過程始終唔能夠查核。結果就係,行業表面政策同實際執行常常唔一致,每個項目嘅談判結果都好唔同,而競爭壓力會令唔透明成為優勢而唔係弱點。

The fundamental question underlying these debates is whether either model - Binance's rapid onboarding approach or Coinbase's selective gatekeeping - truly serves users' and projects' interests optimally. Rapid listing provides projects with market access and gives users more trading options but potentially exposes them to lower - quality assets with inadequate due diligence or poor liquidity. Slow, selective listing protects users from problematic projects but may exclude worthy innovations and reduce competitive pressure that could benefit consumers through lower fees or better services.

呢啲爭論背後嘅根本問題係:究竟 Binance 快速上架模式定 Coinbase 嚴選把關政策,邊個對用戶同項目最好?快速上架可以令項目儘早進入市場,用戶選擇多啲;但同時有機會帶嚟佢質素唔高、審查唔足、流動性差嘅資產。慢慢選,雖然保障用戶避免踩中地雷,但會排除好項目入場,弱化競爭,令服務創新和收費難以優化。

Some analysts suggest that the optimal solution lies not in perfecting centralized exchange listing processes but in reducing dependence on centralized exchanges altogether. Decentralized exchanges like Uniswap, PancakeSwap, and others allow any project to create liquidity pools and begin trading without gatekeepers, though at the cost of reduced protections and sometimes shallow liquidity. As DEX technology improves and captures larger market shares, the power of centralized exchanges to determine which projects succeed may diminish. But given that centralized exchanges still handle the vast majority of trading volume and provide the primary onramps from fiat currency into crypto assets, their listing policies will remain consequential for the foreseeable future.

有分析認為,最好方法唔係令中心化交易所嘅上幣流程更完美,而係減低對中心化交易所嘅依賴。去中心化交易所如 Uniswap、PancakeSwap 等,任任何項目都可以自己加資金池開始交易,唔使經過任何守門人,但同時保護減少,有時流動性都會較少。隨住 DEX 技術成熟同佔市場越多,中心化交易所分配勝負嘅權力可能會減少,但只要主流交易量都還係由中心化交易所處理,而法幣入場口仲靠佢哋,佢哋嘅上幣政策一定對市場有重大影響。

Market - Making, Liquidity, and Power Dynamics

做市、流動性與權力分配

To fully grasp why Coinbase conditioned BNB's listing on market - making readiness, one must understand the central role that professional market - making plays in modern cryptocurrency markets and how exchanges use liquidity requirements to manage competitive dynamics. Market - making represents one of the least visible but most influential forces shaping how digital assets trade and what user experiences look like when buying or selling tokens.

要明白點解 Coinbase 上架 BNB 要求做好做市安排,就要理解專業做市商喺現代加密貨幣市場中嘅核心角色,亦即係交易所用流動性規定去控制競爭格局。做市係一種最唔為人見但極有影響力嘅力量,佢決定加密資產點樣成交,亦會直接影響用戶買賣體驗。

Market makers are specialized trading firms that continuously offer to buy and sell assets at quoted prices, profiting from the bid - ask spread - the small difference between buy and sell prices - while providing liquidity that enables smooth trading even when natural buyers and sellers are temporarily imbalanced. For major assets like Bitcoin or Ethereum, market - making is highly competitive with numerous firms competing to offer tighter spreads and deeper liquidity. For smaller or newer tokens, fewer market makers may be willing to commit capital, leading to wider spreads, higher price slippage, and more volatile trading experiences.

做市商係專業交易公司,會不斷報價買入、賣出資產,靠買賣價差(買入價同賣出價之間嘅細微差額)賺錢,同時為市場提供流動性,即使暫時買賣雙方唔平衡,都唔會影響成交順暢。大幣如比特幣、以太坊,競爭激烈,有好多間做市公司,不斷壓低差價拉高流動性。細幣或新幣就唔同,做市商投入資本少,價差闊、滑點高,交易體驗波動大得多。

Professional crypto market makers like Jane Street Digital, Jump Crypto, Wintermute, and GSR deploy sophisticated algorithmic trading systems that monitor prices across dozens of exchanges simultaneously, automatically adjusting quotes based on orderbook dynamics, recent trades, and cross - exchange arbitrage opportunities. These systems can quote prices, execute trades, and manage inventory risk at speeds measured in milliseconds. For exchanges, securing commitments from reputable market makers represents an essential precondition for successful listings because poor liquidity generates user complaints and damages exchange reputations.

專業加密做市如 Jane Street Digital、Jump Crypto、Wintermute、GSR 都用高度自動化系統同步監控幾十間交易所,根據訂單簿、最新成交、跨所套利情況自動調整報價。一切買賣、價格調整、倉位管理,全部都係以毫秒計速度完成。對交易所嚟講,搵到夠份量、信譽好嘅做市商應承支持新幣上架,係成功上新市嘅必要條件,如果冇流動性就會引起用戶不滿,損害交易所口碑。

When Coinbase noted that BNB trading would be contingent on market - making support, it referenced this fundamental requirement. Despite BNB's enormous market capitalization and substantial liquidity on Binance, establishing adequate market - making on Coinbase requires arranging for firms willing to commit capital, manage inventory risk, and provide competitive quotes. Market makers evaluate this based on expected trading volumes - higher volumes justify more committed capital and tighter spreads - and on the costs of maintaining positions including funding costs, hedging expenses, and technical infrastructure. Because BNB trades heavily on Binance but less actively on other major exchanges, market makers must assess whether Coinbase users would generate sufficient volume to justify their commitments.

Coinbase 指 BNB 上架必須有做市配套,正正就係提緊呢個基本條件。雖然 BNB 喺 Binance 上市值大、流動性強,但要喺 Coinbase 做到同樣規模,就要新搵做市公司投入資本、管理倉位風險及持續報價。做市商會睇預期成交量決定投入幾多錢,量愈大,價差可以收窄;同時考慮資金成本、對沖開支及技術基礎設施等。BNB 喺 Binance 交易活躍,但其他平台成交少,做市商自然要衡量 Coinbase 其實能不能吸引到足夠成交量,先會決定落唔落力。

Binance's approach to market - making reflects its integrated ecosystem advantages. Because Binance itself maintains the largest BNB orderbook and trading volume, it can provide exemplary liquidity through its own market - making operations and preferred partners. For other tokens, Binance works with a network of market - making firms that benefit from the exchange's enormous user base and trading volumes. The exchange has been known to facilitate introductions between projects and market makers, sometimes as part of the listing process. Critics argue this gives Binance excessive influence over which projects receive adequate liquidity support and which face challenging trading conditions that hamper their growth.

Binance 嘅做市安排反映到佢生態一體化優勢。Binance 擁有最大嘅 BNB 訂單簿同成交量,可以靠自己同合作做市商確保流動性。對其他代幣,都係靠大網絡嘅做市公司從用戶基礎同成交量分一杯羹。有時 Binance 甚至會幫項目介紹做市商,有啲直接納入上架流程。批評者就話,咁樣會令 Binance 得到太大權力 —— 決定邊隻幣可以有幫手做市、有流動性,邊隻又得自己硬食冷清局面,影響增長。

The power dynamics embedded in these arrangements extend well beyond technical market - making functions. When exchanges serve as gatekeepers not just for listing decisions but for liquidity provision that determines whether listings actually succeed, they accumulate influence that can be wielded for competitive advantage. An exchange might provide premium market - making support for tokens from favored

呢啲安排入面嘅權力分佈,已經唔係淨係機械式做市咁簡單。如果交易所唔淨係決定邊隻幣可以上架,甚至主導流動性分配(而流動性會唔會搞得掂,直接影響上架成敗),咁佢哋累積咗更大權力,可以喺行業爭拗中搵著數。某些交易所仲可能會俾偏愛項目特別市值支援,增加競爭優勢。 ecosystems while offering minimal support for potential competitors. It might condition liquidity arrangements on commercial terms that benefit the exchange financially. Or it might use market - making relationships as leverage in negotiations over other issues including marketing partnerships, revenue sharing, or integration with exchange - specific features.

不同生態系統之間,往往只會為潛在競爭對手提供最低限度的支援。有時候,它們可能會將流動性安排,綁定於一些有利於交易所自身的商業條款上。亦可能會利用做市商合作關係,作為談判其他議題(例如市場推廣夥伴關係、收益分成,或是與交易所專屬功能的整合)的籌碼。

Coinbase's emphasis on market - making readiness, therefore, serves multiple purposes. At face value, it ensures quality user experiences by preventing listings with inadequate liquidity. But it also provides Coinbase with discretion over timing and terms, allowing the exchange to manage competitive considerations. If Coinbase concluded that providing premium market - making support for BNB was strategically unwise given BNB's association with Binance, it could delay listing indefinitely while technically maintaining that market - making support had simply not materialized to required standards. Conversely, if Coinbase decided that listing BNB promptly would generate positive PR and trading revenue that outweighed competitive concerns, it could prioritize market - making arrangements and accelerate the timeline.

因此,Coinbase 強調做市準備度,其實別具多重意義。表面上,這確保了良好用戶體驗,防止上架流動性不足的幣種。但同時,亦賦予 Coinbase 對上架時機和條款的靈活掌握,使交易所能因應競爭形勢自主調控。如果 Coinbase 認為,考慮到 BNB 屬於 Binance 旗下,上架時提供額外做市支援並不符合戰略利益,它就可以無限期拖延上架,同時技術上可以聲稱做市支援仍未達到要求。相反,如果 Coinbase 判斷即時上架 BNB 能帶來正面宣傳及交易收入,足以抵銷競爭憂慮,便可優先配合做市安排,並加快上架進度。

Liquidity depth and spreads themselves function as competitive moats between exchanges. Traders gravitate toward venues offering the best prices and deepest liquidity because even small differences in execution quality compound over time into meaningful cost advantages. For major trading pairs like BTC/USDT or ETH/USDC, the exchanges with the most committed market - making infrastructure capture disproportionate volumes, creating self - reinforcing advantages. Binance's dominant position across numerous trading pairs reflects decades of investment in market - making relationships, fee structures that incentivize liquidity provision, and the sheer scale effects from servicing hundreds of millions of users globally.

流動性深度和買賣差價本身已是各交易所之間重要的競爭護城河。交易員自然傾向選擇價格最優、流動性最深的平台,因為執行品質哪怕只差一點點,長遠來看都足以帶來顯著成本優勢。以 BTC/USDT 或 ETH/USDC 等主要交易對為例,那些深耕做市商基建的交易所,往往能搶佔最大成交量,形成自我強化的優勢。Binance 在多個交易對上的領先地位,正是多年來對做市商關係、鼓勵流動性的收費機制,以及服務全球數以億計用戶所帶來的規模效應的體現。

When Coinbase contemplates listing BNB, it necessarily considers not just whether it can provide adequate liquidity but whether doing so might inadvertently strengthen Binance's competitive position. If significant trading volume migrates to Coinbase for BNB, that could reduce Binance's strategic advantage from exclusive control of its token's primary market. But if Coinbase provides only mediocre liquidity, users may continue trading BNB primarily on Binance while viewing Coinbase's listing as an afterthought, failing to generate meaningful volume or revenue for Coinbase while consuming engineering and operational resources.

當 Coinbase 考慮是否上架 BNB,不但要評估自身能否提供足夠流動性,更要計算這是否會無意中增強 Binance 的競爭優勢。如果大量 BNB 交易量轉移至 Coinbase,可能令 Binance 喪失對自家代幣主要市場的獨有戰略優勢。反之,若 Coinbase 只能提供一般般的流動性,投資者依然大部份在 Binance 進行 BNB 交易,而將 Coinbase 上架視為一種「有也可,無也可」的次要選項,最終無法為 Coinbase 帶來明顯成交量或收益,反而消耗了工程及營運資源。

These competitive calculations extend to broader questions about ecosystem integration. Listing BNB might logically lead to requests or expectations that Coinbase should also support BNB Chain deposits and withdrawals, enabling users to move tokens between Coinbase and BNB Chain - based applications. This would require additional technical integration and would effectively position Coinbase as supporting infrastructure for Binance's blockchain ecosystem. While such integration could benefit users who want flexibility to access different blockchain ecosystems from a single exchange account, it also commits Coinbase to maintaining compatibility with a competitor's technology stack and creates dependencies that might complicate future strategic decisions.

這些競爭考慮,進一步引伸至生態系統整合的更大範疇。上架 BNB,自然會引來市場對於 Coinbase 是否亦應支援 BNB Chain 充提的訴求──讓用戶可把代幣由 Coinbase 轉進 BNB Chain 生態應用等。這就涉及額外技術整合,某程度上也等於 Coinbase 成為 Binance 區塊鏈生態的基礎設施。雖然此舉可為希望從單一交易所賬戶靈活觸達多個生態圈的用戶帶來好處,但同時亦代表 Coinbase 必須長期兼容競爭對手技術棧,並產生日後戰略決策上的依賴性和複雜性。

The broader industry trend appears to be toward greater interoperability and cross - listing despite competitive tensions. As CZ noted in his response to Coinbase, Binance has listed projects from Base and other exchange - affiliated chains, recognizing that users expect access to diverse ecosystems. Kraken's April 2025 listing of BNB preceded Coinbase's move and faced similar questions about why exchanges would support competitors' tokens. The answer seems to be that user demand and competitive pressure from decentralized alternatives are gradually overcoming the instinct to maintain exclusive control. If users can easily trade any asset on decentralized exchanges, centralized exchanges risk losing relevance by refusing to list popular tokens regardless of which platform originally promoted them.

整個行業大勢似乎正朝着更高互通性及交叉上架發展,儘管競爭壓力猶在。正如 CZ(趙長鵬)於回應 Coinbase 時指出,Binance 亦已上架 Base 及其他交易所自家鏈的項目,承認用戶期待能簡單接觸多元生態。Kraken 於 2025 年 4 月率先上架 BNB,比 Coinbase 更早,亦被問過為何要支援競爭對手的代幣。答案大致是:用戶需求及去中心化替代選項的競爭壓力,正逐步削弱各交易所壟斷獨有控制權的本能。若用戶可隨時於去中心化交易所自由買賣任何資產,中心化交易所有如拒絕給熱門幣種上架,不論該幣來自哪個平台,最終只會流失市場地位。

This evolution toward openness, however incomplete and strategically motivated, represents meaningful progress from the earlier exchange landscape where deliberate exclusion of competitive tokens was standard practice. Whether it proves sustainable or merely constitutes a temporary phase before new forms of competitive segmentation emerge remains uncertain.

這種開放趨勢,雖然尚未徹底落實,部分亦出於策略考慮,但與過往業內有系統地排除競爭對手項目的做法相比,已屬重大進步。至於這種現象能否持久,抑或只是新一輪競爭陣營劃分前的暫時過渡,其實仍未有定論。

Cross - Chain Ecosystem Rivalries

Behind the Coinbase - Binance listing dispute lies a deeper competition between Base and BNB Chain - two blockchain platforms with profoundly different origins but increasingly overlapping ambitions. Understanding this ecosystem rivalry helps explain why token listing decisions carry implications far beyond simple trading access.

在 Coinbase 和 Binance 的上架爭議背後,其實是 Base 和 BNB Chain 這兩大區塊鏈平台更深層次的生態競爭。雖然兩者出身和基礎截然不同,但彼此的野心越來越重疊。理解這段生態競爭,有助解釋為何代幣上架決策所牽涉的意義,遠不止於普通買賣通道。

BNB Chain, originally launched as Binance Chain in 2019 and subsequently rebranded following the merger with Binance Smart Chain, represents Binance's effort to build a comprehensive blockchain ecosystem that extends well beyond simple exchange operations. The platform uses a Proof of Staked Authority consensus mechanism with a limited set of validators - currently 21 active validators selected from a pool of 45 candidates based on stake amounts - enabling high transaction throughput of roughly 2,000 transactions per second and three - second block times. This makes BNB Chain substantially faster and cheaper than Ethereum mainnet, with average transaction fees around $0.11 compared to Ethereum's $2.14.

BNB Chain 原名 Binance Chain,於 2019 年推出,後來與 Binance Smart Chain 合併後重塑品牌,反映了 Binance 布局更全面區塊鏈生態,遠超簡單交易所業務。該鏈採用 Proof of Staked Authority 共識機制,驗證者數量有限,目前由 45 個候選者中選出 21 個活躍驗證者,根據質押額排名。此架構讓 BNB Chain 可實現約每秒 2,000 筆交易和每區塊 3 秒速度,明顯較以太坊主網快得多、成本亦低得多──平均手續費只需約 0.11 美元,相比以太坊主網高達 2.14 美元。

The BNB Chain ecosystem has achieved remarkable scale across multiple dimensions. Total value locked in DeFi protocols on BNB Chain approached $6.7 billion as of mid - 2025, making it the third - largest blockchain by this metric behind Ethereum and Solana. The network processes over 4.1 million transactions daily, roughly double Ethereum's daily transaction count. PancakeSwap, the dominant decentralized exchange on BNB Chain, accounts for approximately 91% of the chain's DEX volume and recently achieved record - breaking monthly trading volume of $325 billion in June 2025. In March 2025, PancakeSwap briefly surpassed Uniswap in daily trading volume, a symbolic milestone signaling BNB Chain's growing importance in DeFi.

BNB Chain 生態規模,在多個層面有顯著增長。至 2025 年中,DeFi 協議 TVL(鎖倉總額)達 67 億美元,僅次於以太坊及 Solana,排行第三。全網每日交易筆數逾 410 萬,約為以太坊每日交易量的兩倍。鏈上主導 DEX PancakeSwap 佔據約 91% 市場佔有率,單是 2025 年 6 月的單月交易額已創下 3250 億美元紀錄。2025 年 3 月期間,PancakeSwap 曾一度日交易量超越 Uniswap,象徵 BNB Chain 在 DeFi 領域的重要性正不斷攀升。

Developer activity remains robust with 78 protocols actively building on the network and regular hackathons, grant programs, and incubation initiatives supported by Binance Labs and the BNB Chain Foundation. Recent technical upgrades including the Pascal hard fork introduced smart contract wallet support and improved EVM compatibility, making it easier for developers to port applications from Ethereum. The ecosystem has deliberately targeted areas like gaming, NFTs, and meme coins where transaction speed and low costs provide clear advantages over more decentralized but slower alternatives.

開發者活動同樣活躍,現時有 78 個協議正於 BNB Chain 積極開發,Binance Labs 及 BNB Chain Foundation 經常舉辦 hackathons、資助計劃及孵化項目。最近的 Pascal 硬分叉引入智能合約錢包和提升 EVM 兼容性,方便開發者將應用由以太坊移植過來。該生態刻意針對遊戲、NFT、Meme 幣等範疇,因這些應用對交易速度和低成本需求尤甚,較去中心化但緩慢的平台有明顯優勢。

Base launched in August 2023 as Coinbase's layer - 2 scaling solution built on Optimism's OP Stack technology. Unlike BNB Chain which operates as an independent layer - 1 blockchain, Base functions as a layer - 2 rollup that settles transactions on Ethereum, inheriting Ethereum's security properties while achieving much higher throughput and lower fees than Ethereum mainnet. Base has attracted over 25,000 developers as of September 2025 and achieved total value locked approaching $12 billion on its path toward ambitious targets of $20 billion in TVL and one billion transactions by October 2025.

Base 於 2023 年 8 月正式推出,是 Coinbase 基於 Optimism 的 OP Stack 技術所構建的 Layer 2 擴容方案。跟運行於獨立 Layer 1 區塊鏈的 BNB Chain 不同,Base 作為 Layer 2 Rollup,所有交易最終仍回到以太坊結算,既可享有以太坊安全性,又能達到比主網更快速度與更低手續費。截至 2025 年 9 月,Base 已吸引逾 25,000 位開發者進駐,TVL 亦逼近 120 億美元,目標於 2025 年 10 月前達至 200 億 TVL 及 10 億筆交易。

The platform benefits from seamless integration with Coinbase's infrastructure, providing direct access to approximately 25 million monthly active users on Coinbase and enabling easy onboarding from fiat currency into Base applications. This represents a substantial competitive advantage over ecosystem chains like BNB Chain which require users to navigate more complex paths from traditional finance into crypto applications. Base has also emphasized EVM compatibility and low fees, positioning itself as developer - friendly infrastructure that reduces barriers to building decentralized applications.

該平台最大優勢是全面打通 Coinbase 既有基建,用戶可直接連接約 2,500 萬名每月活躍 Coinbase 客戶,法幣入金亦一站式流入 Base 生態,遠勝於如 BNB Chain 等需要曲折過橋自傳統金融進入加密應用的鏈。Base 亦重視 EVM 相容及低手續費,定位為開發者友善、極大降低門檻的 DeFi 應用基礎設施。

Where BNB Chain leverages Binance's massive global user base and trading volumes, Base leverages Coinbase's regulatory compliance, institutional relationships, and integration with traditional finance. Where BNB Chain has a seven - year operational history and established ecosystem of protocols, Base represents newer infrastructure with less proven resilience but more modern technical architecture. Where BNB Chain operates independently with its own consensus mechanism and validator set, Base remains tied to Ethereum's base layer and participates in the broader Ethereum ecosystem and the emerging "Superchain" vision of interconnected layer - 2 networks.

BNB Chain 倚賴 Binance 本身龐大的用戶群及交易量優勢;Base 則以 Coinbase 的合規監管、機構級合作及與傳統金融的無縫銜接為主打。BNB Chain 運營歷史達 7 年,協議生態穩健成熟;Base 屬新派基建,履險能力仍待驗證,但技術架構較為現代。BNB Chain 擁有獨立共識和驗證者設計,Base 則維繫於以太坊底層,參與更大範圍的以太坊生態及新興的多 L2「超級鏈」網絡理想。

The competition between these ecosystems manifests most directly in the race to attract developers and their applications. Both platforms offer grant programs, technical support, and visibility for promising projects. Both emphasize low transaction costs and high throughput as advantages over Ethereum mainnet. Both seek to build network effects where more applications attract more users which in turn attract more developers in a virtuous cycle. But they differ significantly in their go - to - market strategies and target audiences.

兩大生態最直接的競爭,就是瘋狂搶奪開發者及應用上鏈。兩邊均有資助計劃、技術支援及市場曝光,強調低手續費和高吞吐量遠勝以太坊主網。大家都希望憑借應用吸納更多用戶,繼而推動更多開發者加入,形成良性循環的網絡效應。不過,兩者在市場推廣策略和定位目標上有明顯分別。

BNB Chain has historically focused on retail users, particularly in regions outside North America and Europe where Binance maintains dominant market share. The chain has supported numerous consumer - facing applications including gaming, NFTs, yield farming, and recently meme coins which drive substantial transaction activity even if critics question their long - term value. The ecosystem tolerates higher risk and more experimental projects, accepting that some will fail or behave problematically in exchange for rapid innovation and growth.

BNB Chain 一向主攻零售市場,尤其在北美及歐洲以外地區更是 Binance 強勢地帶。該鏈支援大量面向用戶應用,橫跨遊戲、NFT、挖礦種地、甚至近年大熱 meme 幣等,雖常被質疑缺乏長遠真正價值,卻成功帶動超大量交易活躍。其生態對風險和實驗性項目包容度極高,容許部分項目失敗甚至出現問題,但換來創新速度與規模增長遠超同儕。

Base has targeted more institutional and regulatory - conscious developers, positioning itself as the compliant, trustworthy infrastructure 原文未完,斷至此for building the future of decentralized finance. The platform has attracted attention from traditional finance institutions exploring blockchain applications and from developers who value the legitimacy and integration that Coinbase's involvement provides. Base's growth strategy emphasizes quality over quantity, selective support for applications that demonstrate clear utility, and alignment with Coinbase's broader vision of bringing digital assets to mainstream adoption.

為建立去中心化金融的未來鋪路。這個平台已吸引了來自傳統金融機構的關注,他們正積極探索區塊鏈應用,同時也受到看重Coinbase參與所帶來合法性及整合性的開發者注視。Base的增長策略重質不重量,精挑細選真正有實用價值的應用項目,並且與Coinbase更廣泛將數碼資產推向主流採納的願景保持一致。

When Coinbase adds BNB to its listing roadmap but has not yet listed projects from BNB Chain, this asymmetry reflects the competitive tension between these ecosystems. Supporting BNB Chain applications directly would help grow a rival blockchain platform that competes with Base for developers and users. Yet refusing to list any BNB Chain projects appears hypocritical given Coinbase's statements about openness and Binance's willingness to list Base projects. This tension has no easy resolution because genuine user service and competitive strategy point in opposite directions.

當Coinbase將BNB納入其上架路線圖,但遲遲未有上架來自BNB Chain的項目時,這種不對稱正好反映兩大生態系統之間的競爭張力。若直接支持BNB Chain的應用,實際等於協助對手平台增長,搶奪開發者及用戶,與Base形成直接競爭。然而,若完全拒絕任何BNB Chain項目上架,又會與Coinbase聲稱開放包容的立場及Binance願意上架Base項目的做法背道而馳,顯得雙重標準。這種矛盾難有簡單解決方法,畢竟真誠服務用戶和競爭策略本身就是對立方向。

Some industry observers anticipate that cross - chain interoperability will eventually reduce the importance of these competitive dynamics. Technologies enabling seamless transfer of assets and data between blockchain ecosystems could allow users and developers to participate across multiple chains simultaneously without forced choices between exclusive platforms. Initiatives like Wormhole Bridge, LayerZero, and Axelar are building infrastructure for cross - chain communication and asset transfers. If these succeed, the Base versus BNB Chain competition might evolve from zero - sum rivalry toward coexistence where both platforms serve distinct niches within a more interconnected ecosystem.

部分行業觀察者預料,跨鏈互通的成熟,最終會減低這種競爭張力的重要性。允許資產及數據無縫跨生態系統流轉的技術,有望令用戶及開發者毋須被迫在專屬平台中二選一,能同時跨多條鏈參與。像Wormhole Bridge、LayerZero及Axelar等項目正致力建立跨鏈通訊及資產轉移的基建。若這些計劃取得成功,Base與BNB Chain之間的競爭或可由零和競逐,演變成互相共存,在更互聯的生態中各自服務不同細分市場。

However, powerful incentives toward vertical integration and ecosystem lock - in may limit how much interoperability materializes in practice. Both Coinbase and Binance benefit from network effects that concentrate activity within their respective ecosystems. Developers who build on Base gain access to Coinbase's user base but potentially sacrifice reach to users on other chains. Projects on BNB Chain benefit from Binance's marketing support and listing opportunities but might find adoption elsewhere more difficult. These platform dynamics resemble historical patterns in consumer internet where ostensibly open platforms frequently evolved toward proprietary ecosystems with high switching costs.

然而,強大的垂直整合及生態鎖定誘因,或會實質限制跨鏈互通發展的程度。Coinbase及Binance皆能因網絡效應,吸引生態內活動愈趨集中。選擇在Base上開發的團隊,雖可接觸Coinbase龐大用戶群,但有機會削弱對其他鏈用戶的觸及;而BNB Chain上的項目則可受惠於Binance的宣傳推廣及上市優勢,但在其他鏈的用戶接受度或遇阻力。這些平台動態,與過去消費互聯網中表面開放,最終卻朝高轉換成本的專有生態演變的現象十分相似。

For users, the proliferation of ecosystem chains creates both opportunities and complications. More blockchain platforms competing for users and developers could drive innovation and keep fees low. But fragmentation across multiple incompatible chains with different bridging requirements, wallet software, and application landscapes increases complexity and may reduce the seamless user experiences necessary for mainstream adoption. How the industry resolves this tension between competitive ecosystem differentiation and user - friendly interoperability will profoundly shape cryptocurrency's evolution over the coming years.

對用戶而言,大量生態鏈湧現同時帶來新機會及複雜性。更多區塊鏈平台競逐用戶及開發者,有助推動創新並壓低成本;但多條彼此不互通、橋接要求、錢包軟件及應用生態各異的鏈會令行業更加碎片化,提升門檻,減弱主流採用所需的無縫體驗。行業如何處理競爭生態差異與用戶友好跨鏈互通之間的矛盾,將深遠影響加密貨幣未來數年的發展走向。

Regulatory Pressure and Strategic Signaling

監管壓力與策略性訊號

The October 2025 listing controversy unfolded against a backdrop of dramatic regulatory shifts that have fundamentally altered the environment in which both Coinbase and Binance operate. Understanding these regulatory changes helps explain both exchanges' strategic positioning around transparency, compliance, and listing practices.

2025年10月的上架爭議,正值監管格局劇烈轉變,徹底改變了Coinbase和Binance營運的整體環境。理解這些監管變化,有助於解釋兩家交易所於透明度、合規以及上架制度上的策略定位。

For Coinbase, the February 2025 dismissal of the SEC's enforcement action marked a watershed moment after nearly two years of uncertainty. The lawsuit filed in June 2023 had threatened Coinbase's core business model by alleging that the exchange operated as an unregistered securities exchange by offering trading in tokens that the SEC deemed unregistered securities. The case raised existential questions about whether Coinbase could continue operating lawfully given the SEC's expansive interpretation of what constitutes a security under the Howey test.

對Coinbase而言,2025年2月美國證券交易委員會(SEC)撤銷對其執法行動,是歷時近兩年不明朗後的分水嶺。該訴訟於2023年6月提出,指控Coinbase經營非註冊證券交易所,讓用戶交易SEC認為屬於非註冊證券的代幣。這宗官司令外界質疑Coinbase在SEC對Howey測試(何為證券)的廣泛詮釋下,能否繼續合法經營,甚至動搖其商業根基。

The SEC's decision to dismiss the case did not represent a victory on the merits but rather reflected the agency's policy shift toward developing comprehensive regulatory frameworks rather than pursuing enforcement - first strategies against platforms themselves.

SEC撤案,並非Coinbase實質勝訴,而是反映監管機構政策重心已由單靠執法取締,轉為着手建立更全面的監管框架,暫緩直接針對平台的強硬行動。

This shift resulted from broader political changes with the incoming Trump administration's more favorable posture toward cryptocurrency and the SEC's formation of a Crypto Task Force led by Commissioner Hester Peirce to develop clear regulatory guidance. The Task Force's ten focus areas include clarifying which digital assets qualify as securities, establishing registration pathways for compliant platforms, addressing custody and broker - dealer requirements, and providing relief for token offerings that previously existed in regulatory gray zones. This represents a fundamental departure from former SEC Chair Gary Gensler's approach of declining to issue new rules while aggressively enforcing existing securities laws through litigation.

這種轉向與更宏觀的政治轉變密不可分,包括新一屆特朗普政府對加密貨幣持更開放態度,SEC亦由委員Hester Peirce領頭成立加密特別小組,促進制定清晰監管規範。小組十大重點包括:釐清哪些數碼資產屬證券、規劃合規平台註冊途徑、交代資產託管及經紀要求,以及為原本處於監管灰色地帶的代幣發售提供豁免指引。這些舉措與前SEC主席Gary Gensler「拒訂新規則、濫用舊法執法」的策略,有根本分別。

The dismissal removed an enormous cloud hanging over Coinbase and emboldened the exchange to expand its token offerings, international operations, and experimental products including staking services that had previously faced regulatory scrutiny. Coinbase also became the first U.S. - based cryptocurrency exchange to obtain a full license under the European Union's Markets in Crypto - Assets regulation, enabling it to offer services throughout the EU single market under comprehensive regulatory framework. This international expansion reflects Coinbase's assessment that clear regulatory frameworks, even if burdensome, provide better operating environments than ambiguous situations where enforcement risk remains unpredictable.

此案撤銷,讓盤旋在Coinbase頭頂的巨大陰霾一掃而空,促使交易所加快擴展代幣上架、國際業務及此前受監管壓力限制的質押服務等創新產品。Coinbase更成為首間獲得歐盟「加密資產市場規例」(MiCA)全牌照的美國交易所,可於歐盟單一市場合法運營。這種全球擴展,反映Coinbase認為即使合規要求繁重,有清晰監管框架總比曖昧不明、風險隨時降臨的環境為佳。

Public listing policies serve as crucial regulatory signals in this environment. When Coinbase announced the Blue Carpet initiative emphasizing zero listing fees, transparent processes, and enhanced disclosure requirements for token issuers, it positioned the exchange as a leader in responsible self - regulation that anticipates and exceeds forthcoming regulatory requirements. This creates competitive advantages if and when regulators impose standardized listing requirements on all exchanges. By implementing robust practices early, Coinbase can claim it already operates at higher standards than less compliant competitors.

在這種環境下,公開上架政策也變成重要監管信號。Coinbase宣布「Blue Carpet」計劃,主打零上架費、流程公開、及加強發行方資料披露等,塑造其為自律先鋒,搶步超前落實甚至高於日後法規門檻的負責任營運模式。一旦監管機構統一索取嚴謹上架要求,Coinbase早着先機,自可主張本身標準高於其他欠規管對手,從而建立競爭優勢。

For Binance, the regulatory journey has followed a much more turbulent path. The November 2023 settlement with the U.S. Department of Justice, Financial Crimes Enforcement Network, and Commodity Futures Trading Commission imposed $4.3 billion in penalties - primarily for anti - money laundering violations - and required CZ's permanent departure from executive management. The settlement resolved criminal and civil charges related to operating an unlicensed money transmitting business, facilitating transactions involving sanctioned jurisdictions including Iran, and failing to implement adequate know - your - customer and anti - money laundering programs.

至於Binance,合規之路波濤洶湧。2023年11月與美國司法部、金融犯罪執法局、商品期貨交易委員會達成和解,須繳納43億美元巨額罰款(主要因涉及反洗黑錢違規),並要求創辦人CZ永久退出高層。此和解一次過解決多宗刑事和民事指控,包括經營無牌金錢服務業務、促成受制裁地區(如伊朗)交易、以及未有完善落實KYC及反洗錢措施。

Since the settlement, Binance has undergone dramatic internal transformation. The exchange invested approximately $200 million in compliance programs over two years, expanding legal and regulatory teams from a few dozen to several hundred employees. New CEO Richard Teng positioned compliance as a competitive advantage, arguing that Binance's financial resources enable it to implement controls that smaller exchanges cannot match. The exchange established proper money services business licenses in numerous U.S. states where it previously operated in regulatory gray zones. It pursued full regulatory licenses in key international markets including obtaining a Virtual Asset Service Provider license in Dubai and seeking approval to re - enter markets like India from which it had been expelled for compliance deficiencies.

和解後,Binance經歷了大規模內部轉型,兩年間投資約2億美元推動合規改革,法律及規管人手由數十人大幅增至數百人。新任CEO Richard Teng把合規定位為競爭優勢,並指擁有強大財力令Binance可落實比小交易所更多嚴格措施。平台亦於多個美國曾處灰色地帶的州份補領金錢服務業執照,在國際上則於杜拜取得虛擬資產服務供應商牌照,並積極申請重返因不合規而被逐的印度等市場。

This compliance transformation affects listing decisions profoundly. Where Binance previously added dozens of tokens monthly with limited due diligence, the post - settlement exchange faces pressure to demonstrate rigorous evaluation processes. Regulators expect exchanges with proper licenses to conduct adequate due diligence on listed assets, monitor for potential securities law violations, screen for sanctioned persons or entities, and maintain records that enable regulatory oversight. Projects seeking Binance listings now encounter longer timelines and more intrusive due diligence than during the exchange's earlier rapid - growth phase.

這次合規轉型對於上架審批影響尤深。以往Binance每月可上架數十個新幣,盡職審查有限;但自和解後需展現更嚴謹的審核機制。持牌交易所需對上架資產嚴格盡職查核、遏止違反證券法的風險、篩查受制裁人士或團隊、並保留充分紀錄供監管審查。尋求Binance上市的項目,現時需再三接受盤查,輪候期更長,遠比過往爆發式增長時嚴苛。

Binance's defense against allegations of problematic listing practices increasingly emphasizes regulatory compliance rather than simply denying that fees exist. The exchange points to its screening procedures, risk assessments, and rejection of projects that fail compliance reviews as evidence of responsible practices. Yi He's statements about rigorous evaluation processes speak directly to regulatory concerns about exchanges serving as gatekeepers against problematic assets. By emphasizing that no amount of payment or token allocation can secure listing for projects that fail compliance reviews, Binance positions itself as responsible infrastructure consistent with regulatory expectations rather than a purely commercial enterprise maximizing revenue regardless of asset quality.

Binance就指控存有問題的上架做法時,愈來愈強調合規,而非只是否認收費。平台以嚴格審查程序、風險評估、及拒絕不合規項目作證,證明自己重視責任。何一公開提及嚴謹審查制度,正欲回應監管機關擔心交易所淪為問題資產「守門人」的憂慮。強調即使再多金錢或代幣分配,不合規亦絕不會上架,Binance把自己定位為合乎監管預期、負責任的基礎設施,而非單純為收入最大化、資產質素不理會的商業機構。

The ongoing SEC case against Binance adds complexity to this regulatory picture. Unlike the comprehensive criminal settlement with the Justice Department, the SEC's civil action filed in June 2023 remains ongoing as of October 2025, though the parties have requested multiple 60 - day pauses to negotiate potential resolution. The SEC alleges that Binance operated as an unregistered securities exchange, offered unregistered securities including BNB and BUSD tokens, and provided unregistered staking services. The case's outcome could significantly impact Binance's ability to serve U.S. customers and the broader regulatory framework for

SEC目前對Binance的訴訟令整體監管格局更為複雜。有別於已經全面和解的刑事案件,SEC於2023年6月提出的民事訴訟,截至2025年10月依然懸而未決,期間雙方多次申請暫緩聆訊,以便協商和解方案。SEC指控Binance涉嫌無牌經營證券交易所、發售包括BNB及BUSD等非註冊證券,並提供未經登記的質押服務。案件結果,將對Binance服務美國用戶的能力及整體監管框架產生深遠影響。cryptocurrency exchanges.

全球監管協調的努力令情況更加複雜。歐盟的《加密資產市場法規》(Markets in Crypto-Assets),於2025年全面生效,為在歐盟成員國運作的交易所訂立了全面的發牌要求。這些要求包括最低資本標準、營運韌性措施、利益衝突管理、市場推廣和披露標準,以及消費者保障要求。類似的監管框架已經在多個司法管轄區出現或仍在發展中,包括英國、新加坡、日本和南韓。

美國國會於2025年通過的《GENIUS法案》為穩定幣建立了聯邦監管框架,要求完全儲備支持和每月審計。由於兩間交易所均從穩定幣相關活動(包括交易費用和與穩定幣發行人的分成安排)獲取大量收益,此舉對它們產生直接影響。該法案的通過,顯示美國正朝著全面的聯邦數碼資產監管邁進,有望取代現時各州貨幣轉移牌照和按機構分散執法的碎片狀態。

在這個不斷演變的監管環境下,透明度及有紀錄的合規程序為交易所提供了有力的防守姿態。當Coinbase或Binance因為上架政策受到質疑時,能夠指向已發表的標準、有紀錄的評估程序及一致執行的公開準則,有助證明其真誠履行合規責任。即使因為商業敏感度及競爭考慮,不可能做到完全透明,但達到足以讓監管機構滿意的透明度,同時保持一定策略彈性,已是務實最佳方案。

兩間交易所都明白,他們的長遠生存有賴於在主要市場獲得並維持監管合法性。這一現實越來越主導其公開聲明和政策選擇,就算這些與短期利潤最大化或競爭地位相衝突也是如此。因此,2025年10月的上架爭議,不僅是交易所間的競爭,更是一次公開展示彼此對透明度和負責任做法的承諾,希望藉此影響未來監管取態。

爭奪注意力的生意:公關、影響力與社群反應

2025年10月Coinbase與Binance公開爭拗,反映加密貨幣交易所不僅為用戶和交易量爭奪,還爭奪敘事主導權和社群情緒。在一個聲譽可以左右市場,社交媒體參與直接影響營運成果的行業,能夠塑造公眾討論就變成一項重要競爭資產。

整個事件證明了交易所對「注意力經濟」的高度理解。Jesse Pollak提出「上架應該收零費」這句口號,原本是回應Binance被指要收高昂上架費,但很快成為推動交易所透明度的號召。Pollak將議題絕對化,把Coinbase定位成堅持原則的代表,令其他交易所都要作出回應。

CZ(趙長鵬)的應對則展現了他多年間透過與加密社群直接溝通建立Binance品牌的社媒操作技巧。他不是透過正式企業聲明,而是在X以個人身份發帖,混合幽默、直接與策略訊息。他以笑臉emoji對批評作回應,顯示自信無懼;同時提出Binance上架Base項目,令Coinbase的批評者出現「認知失調」。他呼籲Coinbase上架BNB Chain項目,將話題由防守Binance轉化為攻擊Coinbase是否自圓其說。

Coinbase極速回應,將BNB列入上架路線圖,顯示敏捷反應,但同時亦反映對敘事動態的高度關注。原本可以花數天甚至數星期,從技術、造市及合規角度仔細評估BNB才宣布,但實際於Blue Carpet發布幾小時內便行動,顯示聲譽考慮壓過運營審慎。這舉動即時帶來正面關注,令Coinbase成為回應社群意見的例子,但同時也帶來約束及期望,限制未來彈性。

社群在社交媒體上的反應反映出加密文化內部分歧和部落意識。幣安支持者批評Coinbase偽善,指控其收取巨額上架費(如Justin Sun和Andre Cronje所言),認為BNB上架純粹是被公眾壓力所逼,不是真心支持開放。Coinbase支持者則反駁Binance防守上架費指控時顯得心虛,而CZ要求互相上架,純粹是策略性轉移公眾焦點。

參與指標可見端倪。圍繞上架爭議的貼文有過百萬瀏覽、數千留言、廣泛引用及轉發,引發整個加密社群討論哪一方行為更差,以及揭示交易所集中權力的問題。CoinDesk、The Block、Decrypt等媒體的報導,令爭議從社交媒體擴散至主流加密話語圈。甚至平時並不關注交易所運作及上架流程的用戶,都被捲入討論正確標準的爭論中。

代幣價格波動亦反映有市場參與者認為事件有財務意義。Coinbase宣布上架BNB後BNB價格一度飆升,反映正面情緒,但隨後下跌,可能因為獲利回吐或確認路線圖上架不等於真正開放交易。BNB交易量亦在多間交易所提升,印證敘事可以直接影響市場活動。

這一模式與以往公開進行的加密爭議相似,包括比特幣區塊大小辯論、以太坊硬分叉爭拗,以及多個項目的治理與發展路線之爭。加密社群一向積極參與技術和政策議題,這些在傳統金融市場甚少引起關注的問題,在這裏卻能激起巨大反應。這種參與反映業界起源於強調透明度、社群治理、反對中心化權力的cypherpunk文化。

然而有評論指這些爭拗更像作秀而非原則之爭,主要為爭奪競爭優勢。一種較為憤世嫉俗的看法認為,兩間交易所都在做策略性戲碼:Binance以還擊Coinbase「雙重標準」來轉移自己所受嚴重指控,Coinbase則通過象徵性舉動產生正面公關,但根本運作未有改變。從這視角看,最終受益的不是任何一家交易所,而是加密媒體和社交媒體指標,真正關於上架透明度的實質問題則依然懸而未決。

這些注意力動態亦顯示各交易所著重的不同受眾。Binance的訊息對亞洲市場的零售交易者特別有號召力,尤其CZ本身有明星效應,而Binance在這些地區有主導地位。CZ這種直接、非正式、樂於社媒對話的風格,正好吸引重視親民和反感傳統官腔的社群。

Coinbase則傾向較為克制、機構化,專注監管合規、機構採納和主流可見度。Blue Carpet計劃強調框架、標準與程序,是針對成熟項目及監管觀察家設計的語言,而非零售社交媒體群體。即使Coinbase加入BNB,亦強調如造市及技術基礎設施等營運需求,而非即時回應競爭壓力。

當2025年10月的爭議逐漸淡出聚焦,其對交易所行為和行業規範的長遠影響仍不明朗。公眾壓力究竟有沒有實質影響未來上架決策,還是只帶來象徵性改動而維持本質不變?只有持續觀察,才可看出Coinbase是否加快BNB開放實際交易、是否更歡迎BNB Chain生態項目,及其他交易所會否為回應競爭壓力而提升自身透明度。

更廣泛的意義:交易所競爭的未來

Coinbase-Binance的上架爭議,為檢視加密貨幣演變和中心化交易所競爭未來的多個關鍵問題,提供了透視角度。無論這場爭拗本身會否載入史冊,其揭示的深層矛盾都將影響行業未來的發展。operate and compete in coming years.

首先,這一事件突顯出,儘管加密貨幣本來強調去中心化,但中心化交易所仍然是極具權力的守門人。當Coinbase把BNB加入其上幣路線圖,市場價格立即有反應。當CZ呼籲上架BNB Chain項目時,媒體報導也大增。這些平台影響哪些代幣能進入主流、哪些區塊鏈生態能吸引用戶和開發者,甚至哪些項目能獲得成長所需的流動性。這種權力難免令交易所傾向偏幫自身的垂直整合生態,從而產生交易所作為中立基礎設施與其商業競爭利益間的矛盾。

這種權力集中於兩大主導平台——Coinbase與Binance——為整個生態帶來系統性風險。如果交易所以上幣決策打壓潛在競爭者,或對想上市的項目收取過高費用,這會窒息創新,影響加密領域引人入勝的活力。監管介入雖可處理最嚴重的濫用情況,但過度規管亦可能限制創新甚至令行業僵化。最佳情況應是交易所明白,長遠成功需要維護信任和站在用戶利益一方,即使這有時與短期極大化利潤目標相衝突。

其次,交易所附屬的區塊鏈生態間的競爭——例如Base對BNB Chain——也可能與底層技術革新一樣深刻地塑造加密貨幣的未來。這些平台嘗試複製蘋果、Google、亞馬遜在Web2時代利用網絡效應及垂直整合優勢的成功。如果成功,將為用戶帶來更佳體驗、更低成本及更無縫的交易、託管及應用通路。但這同時有機會在加密世界重現平台優勢及用戶鎖定效應,而這些正是業界本來意圖擺脫的局面。

至於互通性能否發展到足以阻止「贏家通吃」的局面,仍然未明。跨鏈通信及資產轉移的技術已有明顯改善,有各式橋接技術、包裝代幣和通用兌換協議,讓用戶有能力跨生態轉移。但由於每條鏈共識機制、編程語言、錢包軟件及開發工具各異,根本仍有摩擦。這些技術障礙,加上交易所為維持自身優勢而有的商業動機,都可能限制生態的互通程度。

第三,這場上幣風波也反映了透明度作為競爭策略的力量與局限。Coinbase強調公布標準、零上架費及Blue Carpet框架,賺取宣傳及樹立負責任基建形象。但透明同時產生新漏洞:路線圖公開增加外界期望與義務;既定政策限制靈活度,難以根據個別情況作彈性處理;完全透明的評審流程更容易給對手有機可乘,或者洩露商業情報。

Binance較封閉的做法雖然避免了上述漏洞,但卻引起其他風險。在沒有明確標準指引下,項目對上市機會及條款無把握,進而減少申請意欲,或轉向其他更加清晰的平台。同時,缺乏透明也容易引來偏私、貪污、武斷等非議,即使並不屬實也會損害聲譽。最佳平衡很可能是在公正與彈性之間取中庸,既要有足夠透明度以建立信任,又保留一定靈活應對競爭與個案的空間。

第四,這次事件也說明合規要求越來越主導交易所經營決策與市場定位。無論Coinbase還是Binance,如今都需接受重大監管,雖然分屬不同司法區,規定亦有異。這種監管碎片化,對要在全球一致經營的交易所造成挑戰,也為交易所在較寬鬆地區營運、在限制嚴格地區縮減服務提供了套利空間。

歐美MiCA(歐盟),美國新法例、新加坡及香港最新規定等監管趨勢,都指向主要市場將有越來越統一的高要求,涵蓋資本充足、營運韌性、上幣標準及資料披露等範疇。這些規定有利大規模、資源充裕的交易所,令他們能負擔合規投入。規模較小的平台則可能難以競爭,或只能專注於資源有限但有差異化優勢的小眾市場。

第五,日趨成熟的去中心化替代方案,已對中心化交易所在中至長線構成威脅。去中心化交易所已做到可觀規模,單是Uniswap每日橫跨多鏈的成交額已經達到數十億美元。雖然DEX現時佔總交易量為次,但他們在流動性集中、自動做市、跨鏈功能、交易費用等技術領域大幅進步,正逐步縮窄與中心化交易所的質量差距。當DEX的用戶體驗及專業級功能愈趨完善,有望侵蝕目前保護中心化交易所的「護城河」。

中心化平台最有力的防線,很可能是持續優化DEX難以複製的服務,例如法幣出入金、機構級資產託管、複雜衍生品、槓桿交易,以及讓傳統金融參與的合規方案。只要中心化交易所將自己定位為連接傳統金融與去中心化協議的關鍵基礎設施,而非僅僅與DEX正面競爭,他們即使純交易功能日益去中心化,也依然能維持存在價值。

第六,本次風波也顯示,以往純零和對抗的競爭正轉向綜合競爭與合作混合的新局面。例如Binance上架Base項目、Coinbase把BNB納入路線圖,都是承認讓用戶經心儀平台接觸更多生態的好處。這與傳統金融逐步成熟時,交易所互掛證券、券商互開資產池的趨勢類似。隨著加密產業進入成熟階段,對互通性及全面資產接入的需求可能壓倒壟斷及生態自閉的本能反應。

但合作仍受限於根本的競爭矛盾。交易所由網絡效應驅動,流動性與用戶愈集中於同一平台,平台收入就愈高。只要用戶能在一個生態內完成交易、質押、借貸、支付等活動,平台就賺得愈多。而當交易所支持對手代幣或鏈,其實損害了自身優勢——即使同時造福用戶。如何調和這些矛盾,將取決於監管壓力、競爭模式及平台自身對行業未來定位的判斷。

結論:從上幣之爭得到的啟示

2025年10月Coinbase與Binance關於上幣規則之爭,也許只是加密貨幣歷史中的一個小插曲,卻反映出未來數年行業演變的關鍵張力。這場爭拗揭示了中心化交易所身兼產業 核心基礎設施與競爭企業的尷尬定位:既是中立平台,又有商業利益,同時向用戶負責,又需追求最大化利潤。

圍繞「是否收上幣費、評審流程應否完全透明、交易所是否需要主動促進跨生態流通」等問題,或許永遠難以討好所有人的期望。市場現實、競爭壓力及個案特徵,時時會在理想透明度與實務操作之間產生矛盾。當交易所必須兼顧技術可行性、合規要求、商業可持續性及戰略定位並服務多元持份者時,絕對一致性基本上難以實現。

但討論本身已具啟發價值。這些爭議迫使交易所公開闡述其上幣理念,承受質疑與監察,從而產生原本可能欠奉的問責。這讓項目方和用戶有更多資訊選擇信任與合作的平台,也推動交易所日益透明——即使仍做不到完美。更為監管部門提供是否業界自律成功或失敗的訊號,有助未來規範制訂。

行業各方可汲取幾個要點,作為加密基礎設施繼續發展時的重要參考。對交易所而言,最重要的啟示是:透明度及一致性並非...merely ethical principles but competitive assets in an environment where trust remains fragile and reputation effects are powerful. Exchanges that can demonstrate fair, predictable practices while maintaining appropriate flexibility will likely attract higher - quality projects and more loyal users than those operating in opacity. The short - term advantages of discretion and case - by - case flexibility may be outweighed by long - term costs to reputation and regulatory relationships.

僅僅作為道德原則,而不單只是在一個信任仍然脆弱、聲譽效應極為強大的環境下的競爭資產。能夠展示公平、可預測做法,同時保持適當彈性的交易所,很大可能會比那些運作不透明的交易所吸引到質素更高的項目及更忠誠的用戶。雖然短期內靈活處理及個別酌情的好處看似明顯,但長期來看,這些做法可能會因為聲譽和與監管機構的關係受到損害而得不償失。

For projects seeking listings, the lesson involves realistic assessment of what exchanges can reasonably provide and careful consideration of which platforms align with their values and user bases. The dream of completely neutral, purely merit - based listing decisions conflicts with commercial and competitive realities. Projects should expect some degree of negotiation and selectivity while remaining alert to truly abusive practices that cross the line from reasonable business judgment into exploitation.

對於尋求上線的項目來說,當中得到的經驗就是要實事求是地評估交易所實際能夠提供的支援,並小心考慮哪些平台與他們的價值觀及用戶群體最為契合。完全中立、純粹按實力作出上線決定的理想,往往與商業及競爭現實發生衝突。項目方應預期需要一定程度的協商和篩選,同時亦要警覺真正不當甚至剝削性的行為,這些行為會越過合理商業判斷的界線。

For users and investors, the controversy underscores the importance of maintaining perspective about centralized exchanges' role and limitations. These platforms provide valuable services including liquidity, security, regulatory compliance, and convenient access to diverse assets. But they remain centralized points of control whose interests do not perfectly align with users' interests. Diversification across multiple platforms, increasing comfort with self - custody and decentralized alternatives, and healthy skepticism about exchanges' neutrality claims all represent prudent approaches.

對用戶以及投資者而言,這場爭議更加突顯出認清中心化交易所自身角色和限制的重要性。這些平台確實為市場帶來流動性、安全性、合規性,以及便利地接觸多元資產等寶貴服務。但它們始終是集中的掌控樞紐,其利益與用戶的利益始終無法完全一致。跨多平台分散風險、提升自己對自我託管與去中心化方案的接受程度,以及保持對交易所「中立聲稱」的理性懷疑,都是審慎的選擇。

For regulators, the episode highlights the need for clear frameworks that define acceptable exchange practices without micromanaging every decision. The absence of comprehensive regulation creates uncertainty that harms both legitimate businesses and users while enabling truly problematic actors to exploit ambiguity. Well - designed regulation could establish baseline transparency requirements, conflict - of - interest management standards, and consumer protection measures while leaving exchanges appropriate discretion on specific listing decisions.

對監管機構來說,這次事件反映出有需要制定清晰的框架去界定交易所可接受的行為標準,同時避免對每個決策都進行微觀管理。欠缺全面監管的情況只會製造不確定性,既損害合法企業和用戶,又給予不良分子可乘之機利用模糊地帶。妥善設計的監管框架可以劃定基本披露要求、利益衝突管理標準及消費者保障措施,同時也容許交易所在個別上線決定上有合理酌情空間。

Looking forward, the most significant question may be whether centralized exchanges can adapt successfully to an increasingly decentralized ecosystem where their gatekeeping power erodes. If DEXs continue improving user experiences and capturing market share, if interoperability enables users to access diverse ecosystems without dependence on any single platform, and if regulatory frameworks provide clarity that reduces the compliance advantages of centralized intermediaries, the moats protecting current market leaders may prove temporary.

展望未來,最大問題可能是中心化交易所能否適應一個日益去中心化、自己守門力量正被削弱的生態體系。如果去中心化交易所(DEX)不斷提升用戶體驗並搶佔市佔率,如果跨鏈互通讓用戶毋須依賴單一平台就可以接觸不同生態,又或者新的監管框架削弱了中心化中介的合規優勢,那麼現有市場領導者的護城河都可能只屬於過渡性質。

The exchanges that thrive will likely be those that recognize this future and position themselves as complementary to decentralized infrastructure rather than competing directly with it. By focusing on services that genuinely require trusted intermediaries - fiat on - ramps, custody for institutions uncomfortable with self - custody, sophisticated derivatives and structured products, and regulatory compliance that bridges traditional finance and crypto - centralized exchanges can sustain relevance even as pure trading functionality becomes increasingly decentralized.

能夠持續發展的交易所,很可能會是那些看清未來趨勢,選擇把自己定位成為去中心化基礎設施的補充而非直接對抗的公司。它們會專注於真正需要可信中介的服務:法幣出入金通道、不願意自主管理資產的機構託管、複雜衍生產品及結構性金融產品,以及連結傳統金融與加密世界的合規配套。即使純粹交易功能愈趨去中心化,這些中心化服務都可保持其市場重要性。

Ultimately, the Coinbase - Binance listing wars of October 2025 functioned less as definitive confrontation than as one more chapter in cryptocurrency's ongoing negotiation of how to balance its decentralization ideals with the practical realities of building functional financial infrastructure. That tension has existed since Bitcoin's genesis and will persist as long as cryptocurrency serves real users with real needs that sometimes conflict with ideological purity. The industry's ability to navigate these tensions thoughtfully, with appropriate humility about the difficulty of getting everything right, may determine whether cryptocurrency achieves its transformative potential or remains perpetually trapped between irreconcilable visions.

最終,2025年10月Coinbase與Binance的上幣「大戰」並非一次決定性的對決,反而只是加密貨幣行業持續探索如何在去中心化的理想與打造可用金融基建的現實之間取得平衡的又一章。這種張力自比特幣誕生起一直存在,只要加密貨幣仍然要服務有實際需要、而這些需求有時與至純主義理念抵觸的用戶,這種矛盾就不會消失。業界能否以謙遜的心態去正視「沒有完美答案」的挑戰,並有智慧地處理矛盾,可能正是決定加密貨幣能否發揮變革潛力、還是永遠卡在各種無法調和願景之間的關鍵。