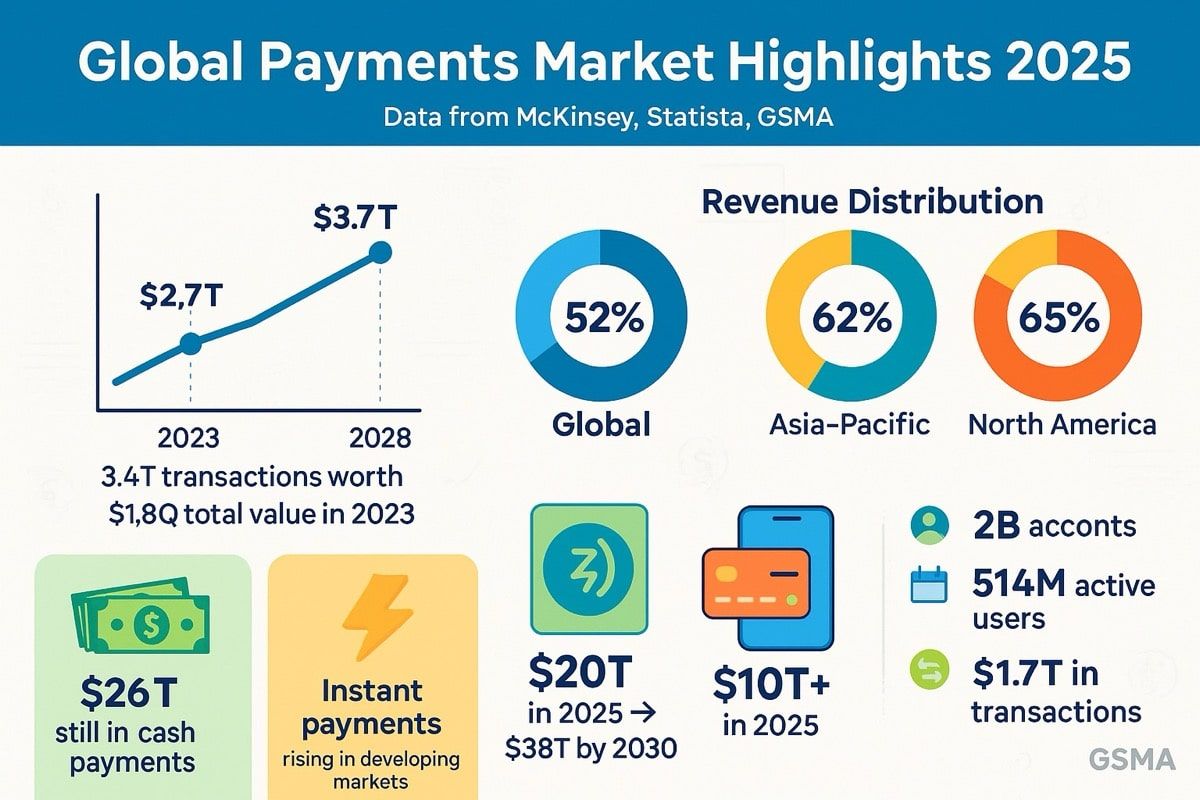

全球支付行業運作規模大到難以想像。2023年,行業大約處理咗34億宗交易,總值1.8千萬億美元,帶來2.4萬億美元收益。用個例子俾你作對比:1.8千萬億美元等於1,800萬億美金,差唔多係美國經濟總量嘅90倍。

但即使有咁龐大規模,又經歷咗幾十年科技發展,現代支付基建仍然好低效。資金需要預先注入帳戶幾日先至到賬。跨境轉帳要經過成層對應銀行好慢。結算時間分佈唔同時區,營運資金滯留喺應收帳款。成套機器雖然運作緊,但好慢、好貴。

同一時間,去中心化金融(DeFi)證明咗一樣革命性嘅嘢:資金可以即刻轉移,幾秒內結算,仲可以自動執行複雜邏輯。穩定幣成為連接傳統同新興系統橋樑,交易量2024年已經超過Visa同Mastercard全年總和,達到15.6萬億美元,仲不斷上升。去到2025年第一季,鏈上穩定幣交易量已經超過8.9萬億美元。

呢個時候,PayFi(Payment Finance)就出現咗,成為傳統支付軌道同去中心化基建嘅融合層。呢個唔淨止擺脫高昂手續費或者加快過數咁簡單,而係更加根本:將本來被鎖死喺支付流程入面嘅時間價值釋放出嚟,令結算由批量咁做變成持續串流方式,仲可以直接喺資金流動過程中編程加入金融邏輯。

Solana基金會主席Lily Liu首次界定呢個概念,重點係:而家一筆錢嘅價值始終大過將來同等金額,因為可以即時用嚟投資、賺息或消費。PayFi融合世代支付網絡嘅分銷同合規框架,再加上區塊鏈架構帶嚟嘅透明、互通同自動化,成就一個即時、無邊界、可組合、識別身份嘅資金流動層。

依家呢個機遇唔係空談。2025年年中,穩定幣市值已達到2,517億美元,USDC流通量創新高,超過560億美元,單11月USDC月交易量已經突破1萬億美金。傳統支付巨頭如Visa都展開咗試點,用USDC喺Solana同Worldpay、Nuvei等收單商做結算。大型資產管理公司如黑石同富達都參與穩定幣基礎建設。香港喺2025年5月通過穩定幣條例,美國亦於7月落實全國性穩定幣立法GENIUS Act。

以下我哋會深入探討PayFi點樣重塑支付生態——包括相關基建、開拓新應用場景、新興監管框架、以及剩餘風險。融合之勢越嚟越快,明白PayFi對喺支付、金融或數碼資產界從業嘅任何人都至關重要。

點解係依家?資金嘅時間價值同支付基建

PayFi出現絕非偶然,佢反映傳統支付長期低效同而家區塊鏈基建成熟,終於可以大規模解決問題。

低效率困局

傳統支付系統有一個核心問題:只會分批運作,唔係串流。企業收到信用卡付款,資金唔會即時到帳——而係進入要兩三日嘅結算流程。公司做國際電匯,要經好多中介銀行,多咗時間、成本同不透明度。員工發薪,提前辛苦做完都要等到月底先有人工。

呢啲延遲產生所謂「浮存金」——即係途中靜止嘅錢,對雙方都冇好處。以前金融機構賺呢啲浮存金利息(因為資金仲未結算),但對消費者嚟講,浮存金就等於鎖住咗啲錢,用唔到、投資唔到、無法履行任何承諾。

全球支付行業每年1.8千萬億美元交易產生大約2.4萬億美元收益,其中大量來自低效率——例如交換手續費、匯率差價、電匯費同停擺資本嘅機會成本。

跨境支付就係問題嘅典型例子。世銀報告,2023年全球平均200美元匯款手續費達6.2%,係聯合國可持續發展目標3%目標超過一倍。全球約1.5億外地工人匯錢返屋企,呢啲費用等於重稅。服務又慢——跨境匯款要三到五日先清算,期間匯率又浮動,資金一樣係去唔到受益人手上。

即時結算軌道缺口

知道咗低效問題,各國都開始推出即時支付系統。例如印度UPI每月處理數十億交易、巴西PIX推動電子化、聯邦儲備局2023年推FedNow做即時支付、歐洲強制推SEPA即時付款。

呢啲都帶嚟咗進步。但仲有限制:大多只覆蓋本國——PIX得巴西內部用、唔可以去墨西哥或尼日利亞;好多唔支援業務邏輯——只係快咗,但自動分賬、智能合約、即時多貨結算做唔到。一啲地方再商業化困難:印度UPI交易量雖大,但免費,未來收益增長無貢獻超過10%。

更根本地,就算即時支付,依然受傳統戶口架構規限——資金只挪動得快啲,實質資金用法唔變。例如自動分賬、履行合約前托管資金、無需預託外幣即可多幣同時結算,統統都做唔到。

區塊鏈基建成熟

傳統支付卡住之際,2020至2025年,區塊鏈基建有大躍進。早期公鏈根本跟唔上支付需求——比特幣每秒7宗,乙太坊最多30宗,都遠遠落後Visa每秒數千宗。

新架構同Layer 2解決咗問題。Solana高速支援PayFi,區塊時間只有400毫秒,流動性充裕。Base、Arbitrum、Polygon都用低成本穩定幣結算。專為跨境支付設計嘅Stellar,實現快速最終結算同低手續費。

同樣重要嘅係穩定幣終於解決區塊鏈波動性:如果媒介隨時結算內波幅10%,肯定冇人用作支付。USDT市值超過1,500億美元,USDC到2025年年中大約七八百億。呢啲美元抵押代幣有價值穩定,仲有可編程、全年無休、即時結算、全公開儲備等特點。

USDC月交易額2024年11月就高達1萬億美元,歷來總額突破1.8萬億美元。2025年初,用穩定幣交易嘅獨立地址超過3,200萬,比2022年暴增2倍以上。

時間價值全面釋放

基建成熟之下,以前做唔到嘅——即係喺支付流程之中釋放時間價值——終於有可能。傳統系統結算不透明又慢,資金運送途中唔知幾時到,根本無法以其建立貸款市場。 final value will be after fees and FX conversion.

最後金額會扣除手續費同埋外幣兌換之後先計算。

PayFi changes this. When a business knows it will receive $10,000 in revenue tomorrow, it can tokenize that future receivable today, access liquidity against it immediately, and have the smart contract automatically settle the obligation when payment arrives. When a freelancer in the Philippines has $500 in completed work pending payment, they can receive advance liquidity, have it settle automatically when the client pays, and avoid waiting weeks for international wire transfers.

PayFi徹底改變咗以往嘅做法。當一間企業知道佢聽日會收到一萬元收入,佢可以即日將呢個未來應收款項代幣化,即刻用佢嚟換取流動資金,等智能合約喺收到款項時自動結算。又比如,喺菲律賓做freelance嘅人完成咗$500嘅工作但仲未收到錢,可以提前攞流動資金,等客戶一付款即自動結算,唔使等國際電匯等成幾個禮拜。

PayFi applies the time-value principle by enabling users to utilize tomorrow's money to pay for today, a feat traditional finance struggles to match. The difference between PayFi and traditional invoice factoring or supply-chain financing is infrastructure: blockchain settlement eliminates much of the overhead, smart contracts automate the workflows, and stablecoins provide the stable value reference.

PayFi善用咗貨幣時間價值原則,等用戶可以用「明日錢」去支付今日開支,呢樣係傳統金融好難做到嘅。PayFi同傳統收帳融資或者供應鏈融資最大分別係基礎設施:區塊鏈結算可以節省大量運作成本,智能合約自動處理工作流程,而穩定幣就成為穩定價值嘅依據。

The moment has arrived not because blockchain is new - it is more than a decade old - but because the infrastructure has finally matured to payments-grade requirements while traditional payment inefficiencies have become increasingly untenable in a globalized, digitally native economy.

今日之所以時機成熟,唔係因為區塊鏈係新科技——其實已經有十幾年歷史——而係因為區塊鏈基礎設施終於發展到適合支付行業標準,亦因為傳統支付體系喺全球化同數碼新經濟下愈來愈唔可行。

Infrastructure: How PayFi Works

PayFi's technical architecture represents a deliberate fusion of traditional financial infrastructure with blockchain settlement layers. Understanding how this works requires examining the component layers, the key players providing infrastructure, and the mechanisms that enable real-time, programmable settlement.

PayFi嘅技術架構專登結合咗傳統金融基建同區塊鏈結算層。要明白運作原理,就要細睇每個組成部分、主要基建提供者,以及實現即時、可編程結算嘅機制。

Architectural Layers

The PayFi stack includes stablecoins and digital assets that serve as the medium of exchange, ensuring speed, security, and global interoperability, with protocols like the Bitcoin Lightning Network, Stellar, and Ethereum Layer-2 solutions enabling instant, low-cost transactions at scale.

PayFi技術棧涵蓋穩定幣及數碼資產作為交換媒介,確保交易快捷、安全、兼容全球。比如Bitcoin Lightning Network、Stellar同Ethereum Layer-2方案,都實現到即時又低成本、大規模嘅交易。

The architecture typically comprises four layers:

PayFi架構一般分為四層:

Settlement Layer: This is where value actually moves and final settlement occurs. It can be a Layer-1 blockchain like Ethereum, Solana, or Stellar, or a Layer-2 scaling solution like Base, Arbitrum, or Polygon. The settlement layer must provide fast finality (seconds to minutes), low transaction costs (fractions of a cent to a few dollars), and sufficient throughput (hundreds to thousands of transactions per second).

結算層:即係資金實際流動同最終結算發生嘅地方。可以係Layer-1公鏈(如Ethereum、Solana、Stellar)、亦可以係Layer-2擴容方案(如Base、Arbitrum、Polygon)。結算層必須提供快速結算(幾秒至幾分鐘)、低交易成本(幾分一美元至幾蚊)同足夠吞吐量(每秒幾百至幾千交易)。

Asset Layer: Stablecoins serve as the bridge between fiat currency and on-chain value. USDT (Tether) remains the largest stablecoin, surpassing $150 billion in market cap by mid-2025, while USDC ranks second at approximately $70-75 billion. These are not cryptocurrency speculations; they are dollar representations designed to maintain 1:1 parity with USD through reserve backing.

資產層:穩定幣用嚟連接法定貨幣同區塊鏈上嘅價值。USDT(Tether)仍然係最大穩定幣,2025年中市值超過$1,500億;USDC大約排第二,有$700-750億。呢啲唔係炒幣,而係專為保持美元1:1兌換設計,用儲備資產作支撐。

Circle's USDC reserves consist of 98.9% held in short-dated U.S. Treasuries and cash equivalents. This structure provides liquidity (Circle commits to 1:1 redemption) while generating yield from Treasury holdings. USDC is natively supported on 28 blockchain networks including Ethereum, Solana, Base, Arbitrum, Stellar, and Polygon, enabling cross-chain interoperability.

Circle發行嘅USDC,有98.9%儲備係美國短期國債同現金等資產。咁做可以保證流動性(Circle承諾1:1兌換),同時國債持有可產生收益。USDC原生支援28個區塊鏈,包括Ethereum、Solana、Base、Arbitrum、Stellar、Polygon等,實現跨鏈互通。

Bridging Layer: Traditional payment systems do not speak blockchain protocols natively. The bridging layer translates between worlds. This includes:

橋接層:傳統支付系統原生唔識區塊鏈協議,橋接層就用嚟連接兩者。包括:

-

On-ramps: Services that convert fiat to stablecoins (e.g., bank transfers to USDC)

- 入金通道:將法定貨幣換成穩定幣(例如銀行轉賬至USDC)

-

Off-ramps: Services that convert stablecoins to fiat (e.g., USDC to local currency cash-out)

- 出金通道:將穩定幣換回法幣(例如USDC兌換做本地現金)

-

Payment processors: Integrations with card networks, ACH, wire systems

- 支付處理商:可連接卡網、ACH、自動電匯等系統

-

Compliance infrastructure: KYC/AML verification, transaction monitoring, sanctions screening

- 合規系統:KYC/AML認證、交易監控、制裁名單篩查

Application Layer: This is where business logic lives. Smart contracts automate escrow, split payments, enforce conditional releases, route funds to multiple recipients based on pre-defined rules, and enable programmable financial products. Applications include payment widgets, treasury management dashboards, embedded finance APIs, and invoicing platforms with instant settlement.

應用層:實際業務邏輯所在。智能合約自動處理第三方託管、分帳、條件釋放資金、根據設定路由多方收款,並提供可編程金融產品。應用場景包括支付插件、資金管理面板、嵌入式金融API、以及即時結算嘅開單平台等。

Key Infrastructure Players

Several organizations have emerged as critical infrastructure providers enabling PayFi:

而家有幾間主要機構為PayFi提供基礎設施:

Circle and USDC: Circle operates as both stablecoin issuer and infrastructure provider. Beyond minting USDC, Circle provides payment APIs, cross-chain transfer protocols (Circle's Cross-Chain Transfer Protocol enables seamless USDC movement between blockchains), and compliance infrastructure. Circle's stack, including the Circle Payments Network, targets institutional-grade reliability and compliance - key for mainstream payments.

Circle同USDC:Circle不單止係穩定幣發行商,同時提供支付基建。除咗發行USDC外,亦提供支付API、跨鏈轉帳協議(Circle Cross-Chain Transfer Protocol幫USDC無縫穿梭不同區塊鏈)同合規工具。Circle Payment Network等服務針對機構級可靠性同規範,專門應付主流支付需求。

In 2025, Circle acquired Hashnote to expand into tokenized money markets, providing yield-generating opportunities for USDC holders. Circle also partnered with BlackRock (as primary asset manager for USDC cash reserves) and BNY Mellon (as primary custodian of backing assets), bringing traditional finance credibility to stablecoin infrastructure.

2025年,Circle收購Hashnote進軍代幣化貨幣市場,為USDC持有人提供收益機會。Circle同BlackRock合作管理USDC現金儲備,BNY Mellon做資產託管,引入傳統金融信譽。

Solana Foundation: Solana has positioned itself as a high-performance PayFi network. With 400-millisecond block times, Solana provides the speed necessary for near-instant settlement. Visa expanded pilots to settle with USDC on Solana with acquirers like Worldpay and Nuvei, demonstrating that PayFi can mesh with existing merchant infrastructure.

Solana基金會:Solana定位為高效能PayFi網絡。區塊時間只需400毫秒,足夠支持近乎即時結算。Visa將USDC於Solana落實試點計劃,合作機構包括Worldpay及Nuvei,證明PayFi可以同現有商戶基建整合。

The Solana ecosystem includes numerous PayFi-specific projects. These range from accounts receivable financing platforms to creator monetization tools to supply-chain settlement applications. Solana's focus on low transaction costs (typically fractions of a cent) makes it economically viable for small-value payments that would be prohibitive on higher-fee networks.

Solana生態圈有大量PayFi相關項目——由應收帳融資平台,到內容創作者變現工具,再到供應鏈結算應用等等。Solana專注極低交易成本(通常只係幾分一美元),令小額支付都變得可行,唔似傳統高手續費網絡。

Stellar Network: Stellar was designed from inception for cross-border payments. Stellar has tokenized over $400 billion in real-world assets and is the second-largest chain for asset tokenization. The network's architecture optimizes for fast finality and low cost rather than general-purpose computation.

Stellar網絡:Stellar由一開始就針對跨境支付。Stellar已經將超過$4,000億現實資產代幣化,并成為全球第二大資產代幣化區塊鏈。Stellar更注重快結算、低成本,而唔係一般計算能力。

MoneyGram's partnership with the Stellar Development Foundation enables digital wallets connected to the Stellar network to access MoneyGram's global retail platform, providing a bridge between digital assets and local currencies for consumers. The partnership provides the ability to seamlessly convert USDC to cash, or cash to USDC, revolutionizing the settlement process with near-real-time settlement using Circle's USDC.

MoneyGram同Stellar基金會合作,令Stellar網絡數碼錢包可以連接MoneyGram全球零售平台,方便用家數碼資產同本地貨幣互換。夥伴關係容許USDC與現金無縫兌換,用Circle USDC實現幾乎實時結算,徹底改革資金清結方式。

Stellar USDC has processed billions of dollars in payments, with over $4.2 billion in cumulative payment volume by mid-2023. The network sees particularly high activity in Latin America, Africa, and Southeast Asia - regions where cross-border payments are critical but expensive through traditional channels.

Stellar USDC累計結算超過42億美金支付。拉美、非洲、東南亞等地跨境支付需求大,但傳統渠道昂貴,Stellar表現尤其活躍。

Ethereum Layer-2 Networks: While Ethereum's main network can be expensive for payments, Layer-2 solutions like Base (Coinbase's network), Arbitrum, and Polygon provide Ethereum security with significantly lower costs. Base has one of the largest cumulative stablecoin transaction bases, reflecting growing adoption for payments applications.

Ethereum Layer-2網絡:雖然以太坊主網支付成本高,但Base(Coinbase網絡)、Arbitrum、Polygon等Layer-2方案提供相同安全性,同時低成本。Base穩定幣總交易量係最大之一,反映付款應用越來越受歡迎。

These networks benefit from Ethereum's established developer ecosystem, security model, and institutional comfort level. Many traditional financial institutions exploring blockchain payments begin with Ethereum-based infrastructure due to familiarity.

呢啲網絡有Ethereum龐大開發者生態、安全制度同機構級信心。好多傳統金融機構想試水區塊鏈支付,會首先揀Ethereum生態圈。

Traditional Finance Integration Partners: PayFi cannot scale without bridges to traditional finance. Key players include:

傳統金融對接夥伴:PayFi要擴展一定要連結傳統金融。主要機構包括:

-

Visa and Mastercard: Both networks have launched stablecoin settlement initiatives. Visa's crypto advisory services help clients integrate USDC settlement. Mastercard has partnered with multiple stablecoin projects for card payments.

- Visa及Mastercard:兩者都推出穩定幣結算計劃。Visa提供加密顧問服務協助客戶對接USDC。Mastercard同多個穩定幣項目合作推動卡支付。

-

Banking Infrastructure: United Texas Bank serves as a settlement bank between Circle and MoneyGram, facilitating the bridge between traditional banking and blockchain rails. Other banks including Signature Bank (before its closure) and Silvergate provided crypto banking services.

- 銀行基建:United Texas Bank係Circle同MoneyGram結算銀行,橋接傳統銀行同區塊鏈支付。啲銀行如Signature Bank(結業前)、Silvergate等都曾提供加密銀行服務。

-

Payment Processors: Companies like Stripe, Adyen, and PayPal have integrated stablecoin acceptance. PayPal operates its own stablecoin PYUSD. Stripe has explored USDC integration for merchant settlement.

- 支付處理商:Stripe、Adyen、PayPal等都加入穩定幣收款功能。PayPal仲自己發行穩定幣PYUSD。Stripe亦考慮用USDC收商戶款項。

Mechanics of PayFi Settlement

Understanding PayFi requires examining how value actually moves through the system. Consider a cross-border payment from a U.S. business to a supplier in the Philippines:

要理解PayFi點運作,需要睇資金如何實際流轉。以美國公司匯款到菲律賓供應商為例:

Traditional Process:

- Business initiates wire transfer through bank ($25-50 fee, 3-5 days)

- Correspondent banks route payment through SWIFT network

- Foreign exchange conversion occurs (spread typically 2-4%)

- Receiving bank credits supplier account (local fees apply)

- Total time: 3-5 business days. Total cost: 5-8% including fees and FX spread.

傳統方式:

- 公司透過銀行做電匯(手續費$25-$50,需要3-5日)

- 多間代理銀行經SWIFT網絡路由資金

- 做外匯兌換(匯差2-4%)

- 收款銀行入數(又有本地費用)

- 總共3-5個工作天,成條數加埋成本5-8%(連手續費同匯差)

PayFi Process:

- Business converts USD to USDC via Circle Mint or exchange (near-instant)

- USDC transferred on-chain to supplier's wallet (seconds to minutes, cost <$0.01-1)

- Supplier either holds USDC or converts

PayFi方式:

- 公司用Circle Mint或交易所將美元兑換成USDC(極速完成)

- USDC區塊鏈上即時轉帳到供應商錢包(幾秒至幾分鐘,成本少於$0.01-$1)

- 供應商可以揸住USDC或者兌換成本地貨幣

(下文如需翻譯可再補)to Philippine pesos via local off-ramp

轉換至菲律賓披索,經本地兌現通道

- Total time: Minutes to hours. Total cost: <1-2% depending on off-ramp.

總所需時間:數分鐘至數小時。總成本:小於1–2%,視乎兌現通道而定。

The difference is dramatic. But speed and cost are only part of the story. The more significant innovation is programmability.

分別非常明顯。但速度同成本只係其中一部份, 更重要嘅創新在於「可編程性」。

Programmable Payment Logic

Traditional payments can carry reference numbers or memos, but they cannot execute logic. PayFi payments can. A smart contract can:

傳統支付只可以帶有參考號碼或備註,但做唔到自動執行邏輯。而PayFi付款得。智能合約可以:

-

Split incoming payments automatically: When a creator receives $1,000 for content, the smart contract immediately splits it: 70% to creator, 20% to platform, 10% to collaborators.

自動分拆收款:例如創作者收到$1,000報酬,智能合約即時分拆:70%畀創作者、20%畀平台、10%畀合作者。 -

Escrow with conditions: When a buyer pays for goods, funds lock in escrow. Smart contract releases payment when shipping confirmation arrives on-chain or after time-based conditions meet.

有條件託管:買家付款後,款項會鎖定於託管。到物流確認上鏈或時間條件達成時,智能合約就會自動放款。 -

Cascade routing: When a business receives payment, the smart contract automatically routes portions to various obligations: supplier payments, loan repayments, treasury reserves, tax withholding accounts.

多級自動分派:企業收款時,智能合約會自動按比例分配結餘去唔同項目:畀供應商、還貸、撥入金庫、預留稅款等。 -

Time-locked releases: Investors provide capital that unlocks gradually over time, with smart contracts releasing tranches automatically as milestones meet.

分階段時間釋放:投資者提供資金,資金會依據時間或達標進度,智能合約自動分期釋放。

This programmability enables financial products that were previously impossible or too expensive to build. Invoice factoring traditionally requires extensive infrastructure: credit assessment, legal contracts, collections processes, reconciliation systems. With PayFi, much of this can be automated: smart contracts verify invoices on-chain, provide instant liquidity, and settle automatically when payment arrives.

呢種「可編程性」,令以往唔可能或者成本太高嘅金融產品變得可行。例如傳統發票貼現,要複雜設施支持:信用評估、法律合約、催收流程、對賬系統等等。用PayFi後,咩都可以自動化:智能合約負責驗證發票、即時提供流動性、收款時自動結算。

The infrastructure is complex, involving multiple layers and numerous players. But the user experience can be simple: click send, value arrives in seconds, programmable logic executes automatically. This combination - sophisticated infrastructure with simplified interfaces - is what makes PayFi viable at scale.

雖然基建好複雜,有好多層同埋參與者,但用戶體驗可以好簡單:一按發送,價值數秒鐘內到賬,所有邏輯自動執行。高端基建加簡化介面,正正就係PayFi可以大規模應用嘅原因。

Use Cases Deep Dive

PayFi's real-world applications extend far beyond simple value transfer. The combination of instant settlement, programmable logic, and reduced costs enables entirely new financial products and business models. Several use cases are already moving from pilot projects to production deployment.

PayFi喺現實生活嘅應用,唔止單純轉帳咁簡單。即時結算、可編程邏輯同低成本,令到全新嘅金融產品同商業模式成為可能。有啲案例已經由試驗轉為實際部署。

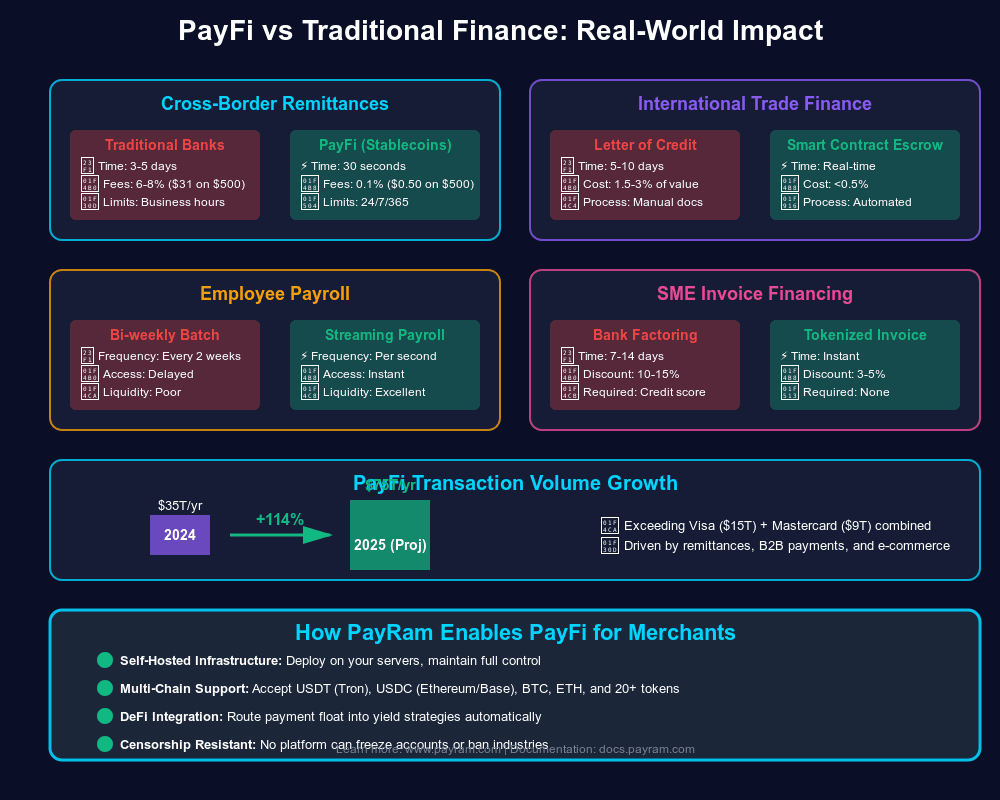

Cross-Border Remittances

Remittances represent one of PayFi's most immediate and impactful applications. Remittance flows to Southeast Asia are projected to reach nearly $100 billion in 2025, growing at more than 8% annually. For the families receiving these funds, traditional remittance costs are crushing: fees average 6.2% globally, and recipients wait days for money to arrive.

跨境匯款係PayFi即時又有影響力嘅應用之一。去到2025年,東南亞地區匯款流預計會接近一千億美元,每年增長超過8%。但對收款家庭嚟講,傳統渠道成本高昂 — 全球平均收費達6.2%,收款更要等幾日。

PayFi offers a superior alternative. Consider the typical remittance corridor from the United States to the Philippines. Traditional services like Western Union or MoneyGram charge 5-8% in combined fees and FX spreads. PayFi alternatives can reduce this to 1-2%, with funds arriving in minutes rather than days.

PayFi提供咗一個更好嘅選擇。例如美國去菲律賓的匯款通道,傳統服務如Western Union或MoneyGram加埋收費同外匯差價高達5-8%。PayFi方案只需1-2%,而且款項以分鐘計到賬,唔使等幾日。

MoneyGram's partnership with Stellar provides the ability to seamlessly convert USDC to cash or cash to USDC, increasing the utility and liquidity of digital assets while enabling more consumers to participate in the digital economy. By connecting to the MoneyGram network, users can now withdraw USDC on Stellar and pick up cash at any participating MoneyGram location, creating a direct bridge between global digital dollars and local economies.

MoneyGram同Stellar嘅合作,令USDC同現金可以無縫兌換,提升咗數碼資產嘅實用性同流動性,令更多用戶參與數碼經濟。透過連接MoneyGram網絡,大家可以喺Stellar提取USDC,再去任何MoneyGram門市換現金,直接令全球數碼美元同本地經濟接軌。

The MoneyGram integration launched initially in key remittance markets including Canada, Kenya, Philippines, and the U.S., with global cash-out functionality available by June 2022。而家MoneyGram覆蓋超過180個國家,為穩定幣上落款提供極大彈性。

In September 2025, MoneyGram partnered with Crossmint to launch stablecoin-powered cross-border payments initially in Colombia。過去四年,哥倫比亞披索貶值超過40%,用美元計價儲蓄變得好重要。呢個服務允許美國用戶用USDC匯款,收款人可以將USDC存入智能錢包,需要現金時再兌換成披索,有效抵抗匯率貶值。

This model addresses multiple pain points simultaneously:

- Speed: Near-instant settlement versus 3-5 days

速度:幾乎即時結算,唔再等3-5日 - Cost: 1-2% fees versus 5-8%

費用:1–2%手續費,相比之前5-8%大大降低 - Currency protection: Recipients can hold USD-backed stablecoins rather than immediately converting to depreciating local currency

貨幣保值:收款人可以選擇持有美元穩定幣,唔使即時兌換成易貶值嘅本地錢 - Accessibility: MoneyGram's cash network provides last-mile access even for recipients without bank accounts

普及度:MoneyGram兌現網絡,即使冇銀行戶口都攞到現金

The remittance use case demonstrates PayFi's potential scale: even capturing 10-20% of the approximately $700 billion global remittance market would represent $70-140 billion in annual volume.

跨境匯款呢個場景,證明PayFi潛力巨大:若只攞到全球約7,000億美元匯款市場10-20%份額,即每年都有700-1,400億美金流量。

Supply-Chain Finance and Invoice Factoring

Supply chains run on credit. Small manufacturers need to purchase raw materials before they receive payment for finished goods. Suppliers ship inventory to retailers who pay 30, 60, or 90 days later. This creates a working capital gap: businesses have completed work and incurred costs but cannot access revenue until payment arrives.

供應鏈靠信用運作。細廠家要先買原材料,做妥貨品賣畀零售商,但對方通常要30、60甚至90日先俾錢。咁樣生意明明做完又有成本,但錢要遲遲先攞到,現金流會出現缺口。

Traditional invoice factoring addresses this by having businesses sell receivables to specialized firms at a discount. The factor provides immediate cash (typically 70-90% of invoice value), then collects the full amount when it arrives. This works, but it is expensive (annual rates often exceed 15-30%) and slow (application, credit review, underwriting, documentation).

傳統做法係賣出發票債權畀專業機構,貼現即收現金(通常收回發票價值70-90%),機構之後再搵原本買家收夠全款。呢個程序成日都好貴(年息成日超過15-30%),申請又慢,要批核、審查、文件一大堆。

PayFi transforms this model. PayFi use cases include accounts receivable financing, where businesses can access capital by tokenizing future receivables and receiving instant liquidity when smart contracts automatically settle obligations upon payment arrival.

PayFi徹底改變呢一格局。PayFi可以自動化賬款融資,企業可將未來收款權利代幣化,到收款日,智能合約自動執行清算,即時收到現金。

Projects like Arf Financial and Huma Finance are deploying such systems. Arf demonstrates this with over $1.6 billion in default-free on-chain transactions, offering 24/7 USDC settlements without requiring pre-funded accounts。關鍵優勢:

- Automation: Smart contracts verify invoices, assess creditworthiness using on-chain history, and provide instant liquidity

自動化:智能合約驗證發票、根據鏈上紀錄評估信貸,仲即時放款 - Cost reduction: Overhead is dramatically lower when workflows are automated, enabling rates of 5-10% rather than 15-30%

成本低:大量程序自動化,融資年利率降至5-10%,對比傳統15-30% - Accessibility: Small businesses that traditional factors would ignore can access financing based on verified transaction history

易接觸:以往傳統機構唔理細企,但而家只要有交易紀錄就批得 - Speed: Approval and funding occur in minutes rather than days or weeks

快:批核同放款以分鐘計,唔洗等幾日或幾星期

Consider a practical example: A small manufacturer in Vietnam produces goods for a U.S. retailer. The retailer's payment terms are Net 60. Traditionally, the manufacturer must either:

- Wait 60 days for payment (losing time-value, unable to take new orders)

- Factor the invoice at 20% annual rate through a traditional lender (expensive)

- Use working capital loans with strict covenants (restrictive)

以越南一間細廠家為例,佢替美國零售商生產貨品,條款係60日付款。以前,工廠要麼:

- 等60日先收錢(失去資金時間值,新訂單又唔敢接)

- 傳統貼現機構收20%年利率,非常昂貴

- 借運營資金貸款,但會有限制

With PayFi, the manufacturer tokenizes the invoice as an NFT or on-chain asset representing the receivable. A liquidity pool or lender reviews the on-chain verified purchase order and the retailer's payment history. If approved, the manufacturer receives 90% of invoice value in USDC immediately. When the retailer pays 60 days later, the smart contract automatically settles the obligation, paying the lender principal plus interest. The effective rate might be 8-10% annualized - expensive relative to bank loans but far better than traditional factoring, with instant availability.

用PayFi後,廠家可將應收發票token化成NFT或鏈上資產,流動資金池或借貸方就用鏈上訂單同過去紀錄去批核。批出就即收發票面值90%嘅USDC。60日後美國零售商付款,智能合約自動還清本+息俾借款方。實際利率8-10%年化,對銀行貸款嚟講都唔平,但同傳統貼現比已經平好多,即時有錢用。

PayFi could streamline capital access for SMEs by automating receivables financing and eliminating complex regulatory hurdles and lengthy risk assessments. The availability of faster funds helps businesses maintain safety cushions and expand growth opportunities without the constraints of delayed payments.

PayFi可以為中小企自動化賬款融資程序,唔使煩複雜監管和風險審核,加快資金到位,有錢就可更彈性經營,減少被慢收款拖住發展。

Real-Time Wage Access

The traditional payroll model is fundamentally mismatched with how people work and live. Employees earn wages daily but receive payment biweekly or monthly. This creates financial stress: bills arrive continuously, but income arrives in lumps. Workers facing emergencies often resort to expensive payday loans or credit card advances because they cannot access money they have already earned.

傳統出糧模式根本跟現實脫節。打工仔每日賺錢,但出糧要兩星期甚至一個月先有一次。賬單日日都有,人工就一輪先有,搞到大家財政壓力好大。遇著突發,要搵快錢只好借高息短期貸或者用信用卡預支,明明自己已經賺咗都拎唔到。

PayFi enables "earned wage access" - the ability for workers to receive payment for work as soon as it is completed. Real-time wages through PayFi allow content creators to finance their video production by receiving funds beforehand, which they can return automatically based on streaming revenue, enabling creators to continuously deliver content without waiting.

PayFi令「即時放糧」成真——打工仔一做完野就即收糧。內容創作者甚至可以預收影片製作資金,之後按收入流自動還錢,變相可以不斷創作唔使等。

The mechanics are straightforward: An employer maintains a treasury of USDC. As employees complete work (verified by time-tracking systems, milestone completion, or other metrics), smart contracts automatically stream payment to their wallets. Workers receive value continuously rather than in batches.

方法都簡單:僱主預先準備一筆USDC儲備。每當員工完成工作(可以用打卡、達標紀錄等認證),智能合約就自動將工資流入對方錢包。出糧唔再分期,而係不斷供應。

This has several benefits:

- Financial stability: Workers can access earned wages when needed, reducing reliance on predatory lending

財政穩定:員工可隨時拎返賺到嘅人工,唔駛靠高利貸或信用卡過渡 - Employer benefits: Companies can attract workers by offering better payment terms

吸引人才:公司提供更好出糧條件,對招聘有幫助 - Reduced overhead: Payroll processing occurs automatically via smart contracts rather than manual batch processes

降低成本:出糧自動化,唔駛人手批量處理 - Global accessibility: Works seamlessly for remote workers in any country with internet access

全球適用:任何有網絡嘅地區,兼職遠端工都得公司如 Zebec 及 Sablier 已經喺 Solana 同 Ethereum 上面建構咗串流付款協議。呢啲協議容許持續進行價值轉移——即係每一秒都有部分薪金根據已過時間同協議好嘅率,由僱主流向僱員。僱員嘅錢包結餘會實時上升,隨時可以提取。

對於「零工經濟」(gig economy)嚟講,呢個係革命性嘅改變。好似一個自由職業設計師,幫一個外國客戶完成項目。以前要等客戶確認收貨、會計部門通過、再啟動國際匯款,然後等結算——成個流程可能要兩個星期,而家設計師做緊工時已經持續收到錢,完工後幾分鐘內完全結算。

商戶結算同繞過卡組織

信用卡收款對商戶嚟講要付出 2-3.5% 嘅交換費(interchange fees)再加處理費。對一間利潤率只得 5-10% 嘅餐廳,卡費已經係一大支出。不過信用卡又係必須——消費者要求付款方式靈活。

PayFi 為商戶提供另一選擇:收穩定幣,即時結算,手續費低於 1%。比較如下:

信用卡付款:

- 顧客付款 $100

- 交換費及處理費:$2.50-3.50

- 商戶實收:$96.50-97.50

- 結算:2-3 日

- 退款爭議風險:6-12 個月

穩定幣付款:

- 顧客用 USDC 付款等值 $100

- 處理費:$0.50-1.00

- 商戶實收:$99.00-99.50

- 結算:即時(鏈上幾秒完成)

- 退款爭議風險:無(區塊鏈交易一經確認就不可撤銷)

商戶得到嘅好處好明顯:

- 成本更低:0.5-1% 對比 2.5-3.5%

- 即時資金流:即入戶口,而唔使等幾日

- 無退款爭議:防止假爭議帶嚟的詐騙損失

- 營運資金優化:即時結算,有效管理現金流

但係客戶採用比較慢。依家大部分消費者未持有穩定幣或者用加密錢包。不過現況緊慢慢轉變。2023年全球電子商貿中,電子錢包佔49%交易金額,預計2026年增加到54%。當愈來愈多錢包支援穩定幣,商戶收穩定幣都會愈來愈普及。

有啲方案會融合兩者:顧客用慣常方式付款(例如信用卡或者銀行轉帳),但後台其實用穩定幣做清結算。表面上消費者仲係刷卡,背後收單銀行同發卡行已經用 USDC 結算,又快又平。

新興應用場景

除咗以上提過類型,PayFi 仲開創咗新玩法:

可編程訂閱:服務可以按用戶實際使用情況動態收費,智能合約自動計數,按比例扣款。以前過份複雜而做唔到嘅用量型收費,依家自動化搞掂。

條件式支付:代管(escrow)服務直接寫落支付流程——例如貨運確認後自動放款、達到里程碑自動付款,或者多人批准後先付款。

生息型收款:收款人可以將入帳錢自動轉到生息協議,不用嘅結餘都可以幫你賺被動收入。

跨境發薪:全球團隊可隨時出糧,用穩定幣支付,員工可以兌換做本地貨幣或者當美元儲蓄。

呢啲應用有共同特點:去中介、減摩擦、成本低、速度快、功能可編程。唔係慢慢改良,而係顛覆性質變——徹底改變支付點樣運作,可以做到乜。

亞洲 PayFi 崛起:地區格局與創新

亞洲近年成為 PayFi 熱點,因多種因素共同推動:支付數碼化急速發展、大量跨境匯款、未充分受銀行服務人口多、擔心貨幣波動、部分市場監管開放。

亞洲支付生態

亞洲嘅支付發展路線同西方唔同。歐美花咗幾十年砌建信用卡網絡,亞洲好多地方直跳手機電子支付。

印度嘅 統一支付介面(UPI) 每月處理數十億宗交易,用 QR code、手機號即時點對點過錢。雖然現金支出仍佔印度消費 60%,但電子支付過去三年已翻倍。但 UPI 只限本地、無收費,難以國際化同獲利。

東南亞情況唔同。2025 年匯款流入預計接近 1,000 億美元,菲律賓每年就有超過 300 億美元。數百萬工人海外做野寄錢返鄉。傳統匯款渠道收費高昂。

中國支付生態由 Alipay 同 WeChat Pay主導,證明手機主導支付可產生龐大規模。但兩者屬封閉系統、外匯限制嚴,跨境用有限制,比較多替代方案機會。

MoneyGram–Stellar 支付走廊:案例分享

MoneyGram 夥拍 Stellar 展示咗 PayFi 實際落地點樣推動亞洲支付創新。

2021 年 10 月宣佈合作,連接 Stellar 網絡數碼錢包去 MoneyGram 全球零售網,幫用戶通過數碼資產同本地貨幣互通。聚焦美國-菲律賓、美國-肯亞及東南亞多個匯款走廊。

服務率先喺加拿大、肯亞、菲律賓、美國推出,2022 年 6 月實現全球現金提領。用 Harm Vibrant、LOBSTR 等 Stellar 錢包可將 USDC 兌換現金,或現金兌回 USDC 匯出國外。

運作流程突顯 PayFi 原理:

- 現金上鏈:匯款人喺美國 MoneyGram 門市俾現金,收 USDC 入 Stellar 錢包

- 鏈上轉賬:匯款人將 USDC 經 Stellar 發送到菲律賓收款人(3-5 秒完成,手續費低於一美分)

- 加密貨幣兌現:收款人喺本地門市或流動錢包,將 USDC 兌換做披索

整個流程,結算幾乎即時(用 Circle USDC),大幅加快資金到位、提升效率同降低風險。

2025年底,Hana電子錢包於東南亞全面接入 MoneyGram Ramps,進一步擴大可用性。市民、自由業、小生意都可以即時用穩定幣提現,令穩定幣真正普及到生活應用。

影響唔止單一交易。即時、成本低嘅新匯款渠道大大推動普惠,收款人唔一定要有銀行賬戶,只要有 MoneyGram 門市就得。佢地仲可以收埋做「數碼美元」儲值對抗本地貨幣貶值,需要錢時先兌現。

監管環境與創新

亞洲規管情況幾參差。有啲地區積極開放,有啲則較嚴謹。

新加坡 建立咗數字資產中心形象,金管局(MAS)對支付服務、穩定幣發行商同數字資產交易所提供清晰牌照框架。多間大型加密公司如 Coinbase、Gemini、Crypto.com 都設立持牌實體。

香港 2025 年 5 月通過穩定幣條例,所有港元穩定幣發行方都要向金管局申請牌照。穩定幣必須有高質素、流動儲備,市值等於市面發行穩定幣面值。監管清楚同時支持創新。

日本 向來審慎但漸進,認可加密貨幣為財產、對交易所有嚴格規管。2023 年已落實穩定幣法,持牌機構可發日圓數碼貨幣。亞洲 Liquid 交易所(日本/新加坡)率先支持 Stellar USDC 提現,顯示機構層面肯接受。

印度 情況較複雜。雖然 UPI 推動本地數碼支付,但加密貨幣監管未明朗。政府提出過加密貨幣稅同監管 frameworks but has not banned usage. This creates opportunity - India's large diaspora sends substantial remittances home, creating demand for low-cost alternatives.

框架上並未禁止使用。這帶來了機會——印度龐大的海外僑民每年會匯送大量款項回國,因此對低成本替代方案有強烈需求。

The Philippines is particularly receptive. The Bangko Sentral ng Pilipinas has licensed several cryptocurrency exchanges and remittance platforms. Given the country's dependence on overseas worker remittances (exceeding $30 billion annually), there is strong motivation to facilitate lower-cost channels.

菲律賓 對此特別受落。菲律賓中央銀行(Bangko Sentral ng Pilipinas)已經發牌給多間加密貨幣交易所及匯款平台。鑑於國家非常依賴海外勞工匯款(每年超過三百億美元),所以有強烈誘因推動更低成本的渠道。

Local Innovations and Adaptations

本地創新及適應

Asian PayFi implementations often reflect local conditions and needs:

亞洲的 PayFi 實施方案往往反映本地狀況和需求:

Mobile-First Design: Given high smartphone penetration and limited desktop usage, Asian PayFi solutions prioritize mobile interfaces. Wallets like Hana, designed specifically for Southeast Asian users, emphasize simplicity and local currency support.

以手機為主的設計:由於智能手機滲透率高,桌面電腦使用有限,亞洲的 PayFi 解決方案優先考慮手機介面。像 Hana 這類專為東南亞用戶設計的電子錢包,着重簡單易用以及支援本地貨幣。

Cash-Bridge Integration: Recognizing that cash remains dominant in many markets, successful implementations integrate with cash networks. The MoneyGram partnership exemplifies this - enabling cash-in and cash-out maintains accessibility for populations without bank accounts.

現金橋接整合:考慮到現金在多個市場仍佔主導地位,成功的方案會與現金網絡整合。MoneyGram 的合作就正正體現這點——既可現金入帳又可現金提取,確保冇銀行戶口的人都用到。

Local Currency Stability: Many Asian currencies experience volatility relative to the dollar. This creates natural demand for dollar-denominated stablecoins as savings vehicles. In Colombia, where the peso has lost over 40% of its value in four years, similar dynamics exist - this pattern appears across numerous emerging markets globally, including many in Asia.

本地貨幣穩定性:亞洲不少貨幣相對美元波動較大,因此自然對美元計價的穩定幣有儲蓄需求。哥倫比亞比索四年間貶值超過四成,出現類似情況——這種模式係全球多個新興市場出現,亞洲唔少國家同樣如此。

Merchant Adoption: Asian merchants, particularly in tourism-dependent areas, increasingly accept stablecoins. This reflects both customer demand (tourists avoiding currency conversion fees) and merchant benefits (lower costs, instant settlement).

商戶採納度:亞洲商戶,尤其依賴旅遊業地區,越來越多接受穩定幣付款。既反映客戶需求(遊客可避免兌換手續費),亦令商戶得益(成本低、結算即時)。

Cross-Border Corridors

跨境通道

Asia's PayFi growth centers on specific corridors where need and infrastructure align:

亞洲的 PayFi 發展重點集中於需求和基建吻合的特定跨境通道:

Middle East to South Asia: Labor flows from Pakistan, India, Bangladesh, and the Philippines to Gulf states create massive remittance volumes. Cross-border B2B settlements using Tether surged in the Middle East and Southeast Asia, with $30+ billion settled in Q1 2025 alone. PayFi solutions targeting these corridors can capture significant market share from traditional services.

中東至南亞:巴基斯坦、印度、孟加拉、菲律賓等地有大量勞工前往海灣國家,造成巨量匯款需求。僅 2025 年第一季,Tether 在中東及東南亞跨境 B2B 結算額就突破三百億美元。針對這些通道的 PayFi 解決方案有潛力奪取傳統服務不少市場份額。

Intra-ASEAN Flows: Trade and labor mobility within the Association of Southeast Asian Nations (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, Vietnam) generates substantial payment flows. PayFi can enable near-instant settlement for cross-border trade that currently requires days and significant banking fees.

東盟內部流動:東南亞國協(即汶萊、柬埔寨、印尼、老撾、馬來西亞、緬甸、菲律賓、新加坡、泰國、越南)國家之間的貿易和勞工流動,產生巨量付款需求。PayFi 可以做到幾乎即時結算,而家跨境貿易要等幾日又要俾不少銀行費。

China Outbound: While domestic Chinese payment rails are advanced, moving value out of China faces capital controls and regulatory constraints. Stablecoins provide an alternative channel, though regulatory risk remains significant.

中國對外:中國國內支付系統先進,但資金流出受到資本管制及監管限制。穩定幣成為一個替代渠道,不過相關監管風險仍然相當大。

The Path Forward

未來發展方向

Asia's PayFi trajectory suggests several developments:

亞洲 PayFi 發展路徑預示住以下幾個方向:

Increasing Corridor Connectivity: As more countries establish clear regulatory frameworks, additional corridors will open. Each new jurisdiction that licenses stablecoin operations enables connections to the global network.

跨境通道連接增加:隨着愈來愈多國家訂立明確監管框架,會有更多通道開放。每新增一個頒發穩定幣牌照的司法管轄區,就令全球網絡多一條連接。

Integration with Regional Payment Systems: Future iterations may bridge PayFi rails with systems like UPI, PIX (Brazil), and SEPA (Europe), enabling seamless value flow between instant payment systems regardless of underlying infrastructure.

與地區支付系統整合:未來發展有可能將 PayFi 鐵路同 UPI、PIX(巴西)或 SEPA(歐洲)等系統打通,實現不同即時支付系統間無縫價值流動,無論底層基建係咩都冇問題。

Central Bank Digital Currency Interaction: As Asian central banks pilot CBDCs (China's digital yuan, Singapore's Project Orchid), questions arise about how stablecoins and CBDCs will interact. Likely outcome: coexistence, with stablecoins serving international flows and CBDCs serving domestic use.

中央銀行數碼貨幣(CBDC)互動:隨着亞洲多個央行測試 CBDC(例如中國數碼人民幣、新加坡 Project Orchid),穩定幣同 CBDC 之間點樣互動成為新命題。最可能情況係共存:穩定幣用於跨境,CBDC 專注本地消費。

Mobile Money Convergence: Mobile money services like GCash (Philippines) and M-Pesa (Kenya, expanding regionally) may integrate stablecoin functionality, combining their extensive distribution networks with blockchain settlement.

流動錢包融合:GCash(菲律賓)、M-Pesa(肯亞並逐漸擴展至其他地區)等流動錢包有機會整合穩定幣功能,結合佢哋廣泛分銷網絡同區塊鏈結算優勢。

Asia's combination of need (expensive remittances, currency volatility, financial inclusion gaps), receptivity (mobile-first populations comfortable with digital payments), and progressive regulation (in key markets) positions the region as a PayFi growth center. The innovations emerging here may eventually flow back to influence Western market implementations.

亞洲擁有迫切需要(昂貴匯款、貨幣波動、金融服務缺口)、高度接受度(習慣數碼支付、以手機為主)同進取監管(部分市場),成為 PayFi 增長樞紐。呢度冒起嘅創新最終甚至可能影響返西方市場實踐。

Institutional Adoption and Economic Implications

機構採用及經濟影響

PayFi's progression from cryptocurrency enthusiasts to mainstream finance marks a critical inflection point. When major financial institutions, payment processors, and asset managers deploy capital and build infrastructure around stablecoin-based payments, it signals a shift from experimentation to production deployment. This institutional embrace carries profound economic implications.

PayFi 由加密愛好者滲透至主流金融業界,正值一個重要轉捩點。當大型金融機構、支付處理商和資產管理人開始重投資金,圍繞穩定幣支付建立基礎設施,標誌住由試驗階段邁向大規模實用。這波機構入場,對經濟有深遠影響。

The Institutional Shift

機構轉型

Traditional financial institutions are recognizing that programmable payments represent not just a technological upgrade but a structural change in how money moves through the global economy.

傳統金融業界開始認清到,可編程支付唔淨係技術升級,仲係全球資金流動模式的結構性轉變。

Asset Manager Involvement: Circle received $400 million in funding with participation from BlackRock, Fidelity, Fin Capital, and Marshall Wace LLP. This was not passive investment - BlackRock entered into a broader strategic partnership with Circle to explore capital market applications for USDC and serves as primary asset manager of USDC cash reserves, while BNY Mellon serves as the primary custodian of assets backing USDC stablecoins.

資產管理人參與:Circle 獲 BlackRock、富達、FIN Capital、Marshall Wace LLP 等參與投資 4 億美元。呢啲唔係純粹被動投資——BlackRock 更與 Circle 建立更廣泛戰略合作,探索 USDC 在資本市場應用,並成為 USDC 現金儲備主要資產管理人,同時 BNY Mellon 就係 USDC 穩定幣資產的主要託管人。

Fidelity is preparing to launch its own stablecoin, tentatively named "Fidelity Token", aiming to provide a stable and secure medium of exchange leveraging Fidelity's reputation in traditional finance.

富達準備推出自家穩定幣,暫名為 "Fidelity Token",希望憑着富達在傳統金融的信譽,提供穩定安心的交換媒介。

Banking Sector Entry: Despite regulatory uncertainty, banks are exploring stablecoin offerings. Several major financial firms are seeking banking charters to hold customer deposits, manage stablecoin reserves, and offer banking services under regulatory oversight. Stripe is seeking a special banking charter to reduce costs and broaden business models, motivated by processing transactions directly.

銀行界入場:雖然監管環境仍有變數,銀行已經開始研究並試推穩定幣產品。多間大型金融機構正申請銀行牌照,以便持有客戶存款、管理穩定幣儲備,及在監管下營運銀行服務;Stripe 亦爭取特別銀行牌照,希望大幅降低成本之餘,擴展直接處理交易的新業務模式。

Payment Network Integration: Visa expanded pilots to settle with USDC on Solana with acquirers like Worldpay and Nuvei, demonstrating that card networks see value in blockchain settlement even while maintaining existing customer-facing rails.

支付網絡整合:Visa 已將 USDC 在 Solana 區塊鏈結算的試點擴展到 Worldpay、Nuvei 等收單方,顯示咗卡網絡樂意利用區塊鏈優點,而同時維持現有客戶接觸渠道。

Treasury Management: Corporations are beginning to use stablecoins for treasury operations. The benefits include:

- 24/7 Liquidity: Unlike bank accounts (limited by operating hours), stablecoin holdings can be deployed instantly at any time

- Programmable Treasury: Smart contracts can automate sweeping, rebalancing, and allocation across multiple accounts and purposes

- Yield Generation: Circle's acquisition of Hashnote enables yield-generating opportunities for USDC holders through tokenized money market funds

- Simplified Multi-Entity Management: Companies with subsidiaries in multiple countries can manage global treasury using stablecoins rather than maintaining numerous bank accounts across jurisdictions

財資管理應用:企業開始用穩定幣管理財資,優點包括:

- 全年無休流動性:唔同銀行戶口受辦公時間限制,穩定幣儲備可隨時即時運用

- 可編程財資:用智能合約自動化掃帳、再平衡,同多個賬戶或用途分配

- 生息機會:Circle 收購 Hashnote,令 USDC 持有人可透過代幣化貨幣市場基金等新機制賺息

- 簡化跨國管理:有多個國家子公司既企業,用穩定幣代替多國銀行戶口管理全球財資更方便

Economic Impacts: The Disappearing Float

經濟效應:浮存金(Float)的消失

Traditional payments generate revenue from multiple sources: interchange fees, processing charges, FX spreads, and float. Of these, float is perhaps the most fundamental yet least visible to end users.

傳統支付靠多個渠道賺錢:手續費、處理費、匯價差、浮存金等。其中浮存金(float)可能最基本、但用戶最唔覺眼。

Float occurs whenever money is in transit but not yet settled. When you swipe a credit card, the merchant does not receive funds immediately. The payment processor holds the money for 2-3 days before settlement. During that time, the processor earns interest on the aggregate balance - millions or billions of dollars sitting across thousands of transactions.

所謂「浮存金」即指資金處於「已付款但未結算」中途。用信用卡消費,商戶唔會即時收到錢,支付處理商通常 hold 幾日(2-3 日)先清算。呢段時間,處理商拿着成千上萬宗交易疊加的資金拿利息——隨時以百萬億計。

Similarly, when businesses hold operating accounts at banks, they typically receive minimal or no interest while the bank deploys those deposits profitably. When companies maintain pre-funded nostro accounts for international payments, that capital sits idle, earning nothing while waiting to facilitate future transactions.

另外,公司在銀行的營運戶口通常無乜利息,銀行卻將存款拿去放貸賺錢。企業開 nostro 戶口預留資金做國際支付,這啲資金長期閒置,一樣無息又冇效率。

PayFi eliminates much of this float:

PayFi 解決咗大部分浮存金問題:

-

Instant Settlement: Merchants receive funds in seconds, not days. No float exists during settlement because settlement is immediate.

-

即時結算:商戶幾秒內收到錢,而唔係等幾日。即時結算期間根本冇浮存金產生。

-

No Pre-Funding Required: Arf Financial demonstrates this with 24/7 USDC settlements without requiring pre-funded accounts, eliminating capital tied up in anticipation of future transactions.

-

毋須預存資金:Arf Financial 展示全天候 USDC 結算,毋須預存戶口資金。完全唔使預夾錢等交易用。

-

Transparency: All balances are visible on-chain in real-time. Companies know exactly what they have available at any moment.

-

透明度高:所有結餘即時 on-chain 睇到,企業可以實時掌握自己有幾多錢用。

This represents a massive shift in working capital efficiency. A retailer processing $10 million monthly in credit card sales previously had $600,000-900,000 perpetually in transit (2-3 days of sales volume). With instant settlement, that capital becomes immediately available for inventory purchases, debt service, or investment.

呢個改革令營運資金效率大幅提升。以往做緊每月一千萬美金信用卡營業額的零售商,平均會有六十到九十萬流動資金被凍結(等於 2-3 日營業額)。而家即時結算,這筆資金可以隨時用落進貨、還債或投資。

Aggregate this across the global payments industry's $1.8 quadrillion in annual transaction value. Even a small percentage shifting to instant settlement represents trillions of dollars in working capital that becomes more productive.

將之推廣到全球支付行業每年 1.8 千萬億美元的交易總額,即使只有極小部分轉為即時結算,都已等於數萬億美金營運資金釋放變得更高效。

New Economic Models

新經濟模式

As traditional revenue sources (float, slow settlement) diminish, PayFi creates opportunities for new monetization models:

隨着傳統盈利來源(如浮存金、慢結算)縮減,PayFi 為新型商業變現模式帶來機會:Liquidity Provision: DeFi 風格的流動性池可以為商戶即時結算、賺取提供資本的費用,讓同日結算成為可能。這類似傳統的商戶現金預付,但過程自動化,而且價格透明。

智能合約費用: 開發人員設計自動支付邏輯,可向用家收取合約使用費。供應鏈金融協議或會對即時發票貼現收取 0.5% 費用,遠低於傳統融資公司,但因營運成本低,具規模時仍獲利可觀。

財資服務: 金融機構可以提供收益優化服務;自動將閒置穩定幣結餘投入最高收益的協議,根據風險參數作再平衡,並提供以往只有大型企業才能用到的現金管理方案。

數據服務: 區塊鏈支付數據具透明度(雖然通常是化名制)。分析服務可提供商業智能,例如現金流預測、根據鏈上支付紀錄作信貸評估,以及應用模式分析的欺詐偵測。

嵌入式金融: 企業可透過 PayFi 基建,將支付功能嵌入應用程式內。SaaS 平台能即時向用戶撥款,市場平台可提供自動託管和結算,內容平台可以實時分成——全靠嵌入式 PayFi 服務及收益分成模式。

競爭與顛覆

機構級採用並不平均。這過程會出現贏家、輸家與新競爭格局。

支付處理商: 好像 Stripe 和 Adyen 這類採用穩定幣結算的公司,在成本結構及功能上或會有優勢。只依附傳統支付軌道者則有機會被顛覆。

銀行: 傳統跨境對應銀行制度面臨生存壓力。如果 匯款成本由 6.2% 跌至 1-2%,原本賺這筆差價的銀行將會收入大跌。若銀行轉型去提供穩定幣服務(託管、出入金、合規),則可開拓新收入來源。拒絕轉型者則有失去市場相關性之虞。

卡組網絡: Visa 和 Mastercard 面臨兩難。他們的互換費商業模式依靠 2-3% 手續費。如果穩定幣支付成本只有 0.5-1%,商戶勢必轉投新方案。組網的回應,是試行穩定幣結算,而用戶仍可保持舊有卡類體驗,務求在轉型中保住分銷優勢。

新進入者: 好像 Circle 這類公司,擁有穩定幣基建和合規經驗,其角色會變得舉足輕重。如果 USDC 成為全球支付基礎設施,即使不向用戶收費,Circle 亦能獲得巨大價值。

規模與前景預測

其潛在規模十分可觀。2025 年麥肯錫全球支付報告顯示,支付行業來自 2000 萬億美元的流量產生 2.5 萬億美元收入。即使未來十年只有 10-20% 流量轉投 PayFi 支付軌道,都已代表每年 200–400 萬億美元的交易價值。

預計到了 2030 年,鏈上資產值將增至 10–25 萬億美元,這將由實時結算和資產代幣化創新所推動。2025 年年中,穩定幣市值已達 2,517 億美元,而五年前近乎零。增長走勢預示未來發展仍會十分迅速。

機構採用能驗證技術可靠、提供流動性、確保合規,並推動主流普及。愈多金融機構部署 PayFi 基建,網絡效應愈強:更多商戶接受穩定幣,更多消費者持有,更多開發者創作應用,資本也會進一步投入這個生態。這種良性循環正好反映平台更替時的特性——說明 PayFi 機構階段其實只是剛開始。

法規與合規環境

PayFi 處於支付法規、銀行法律、證券監管與新興數碼資產規範的交界地帶。2023 至 2025 年間,監管環境變化急速,美國已通過針對穩定幣的全面立法或會成為全球範本。無論是建設或使用 PayFi 基建,了解相關法規都屬必要。

GENIUS 法案:美國穩定幣監管架構

2025 年 7 月 18 日,特朗普總統簽署《美國穩定幣引領與創新法案(GENIUS Act)》,為支付穩定幣訂立監管架構,這是美國史上首部直接針對數字資產的聯邦法規。

定義架構: GENIUS 法案將支付穩定幣界定為一種為支付或結算而發行,且可按預定固定價值兌換的數字資產。最重要是,該定義排除了國家貨幣、銀行存款和證券,讓穩定幣自成監管類別。

儲備要求: 發行人必須以每 1 美元穩定幣對應最少 1 美元准許儲備支持。可接受的儲備包括現金與硬幣、受保銀行及信用合作社存款、短期國債、國債回購協議、政府貨幣市場基金、中央銀行儲備和監管當局認可的其他類似政府資產。

此規定確保穩定幣有高度流動性和低風險的資產完全支持。法例亦防止市面出現靠套利維持掛鈎(非儲備支持)的算法穩定幣——正是針對 2022 年 TerraUSD 崩盤損失 400 億美元的事件。

發行人牌照制度: 銀行及信用合作社可通過子公司發行穩定幣,或由非銀行金融公司發行——但需財政部長、美聯儲及 FDIC 主席一致認為不會造成系統風險,方可放寬限制。

這建立了雙層結構:銀行可向其現有監管機構申請批准,由子公司發行;非銀行則需向貨幣監理署 (OCC) 申請聯邦牌照或依州制度而發行。

州級監管選項: 新法允許未發行超過 100 億美元穩定幣的非銀行發行人在州層面監管,只要該州監管安排基本等同聯邦法,由穩定幣認證審查委員會認定。

這聯邦-州混合結構,在容許創新(州政府可批小型發行人)和保障安全(大型發行人由聯邦監管)之間取平衡。

資訊透明與匯報: 發行人須設立並公開穩定幣贖回指引,並定期公布在外流通穩定幣及儲備組成,報告須由發行人高層確認,並由註冊會計師事務所“查核”。如在外流通超過 500 億美金資產,更需提交經審計的年度財報。

Circle 早已 每月由四大會計師事務所證實儲備,證明高透明度是可行的。GENIUS 法案把這做法法制化。

反洗錢與制裁合規: 新法授權 FinCEN 制定“嶄新方法查緝涉及數字資產的不法活動”,並要求發行人須證明已實施反洗錢及制裁合規政策。所有發行人必須有能力在合法情況下凍結、收回或銷毀支付穩定幣,並能依法律命令執行。

這回應執法部門對穩定幣或會包庇洗黑錢或規避制裁的疑慮,要求發行人維持即時控制權,是在創新與安全之間取平衡。

證券法豁免: 只要由合資格發行人發行,支付穩定幣不屬於美國聯邦證券法下的“證券”,亦不屬商品交易法規下“商品”,因此不受 SEC 或 CFTC 監管。

這一條十分關鍵。一直以來穩定幣是否屬於證券存有不確定風險,GENIUS 法案明確將合資格穩定幣排除於證監監管範疇,但其他數碼資產則仍受規管。

落實時間表: 法案生效後現有發行人有約 18 個月作出符合調整。不過,對於託管或買賣穩定幣的其他機構,則寬限期更長——生效三年內,所有交易或託管穩定幣者只可處理經批准發行人的合資格支付穩定幣。

全球監管環境

GENIUS 法案建立了美國本土監管框架,但 PayFi 屬全球業務。其他地區作法亦有差異:

歐盟 – MiCA: 歐盟的市場加密資產法(MiCA)透過電子貨幣代幣(EMT)和資產參照代幣(ART)規管穩定幣。EMT 指—— (未完,原文戛然而止)tokens backed by a single fiat currency, while ARTs are backed by a basket of assets. Under MiCA, only e-money institutions or credit institutions can issue EMTs, while ART issuers must be EU-based and authorized by regulators.

以單一法定貨幣作為擔保的代幣,而ART則由一籃子資產作為擔保。在MiCA下,只有電子貨幣機構或信貸機構可以發行EMT,而ART的發行人必須是設於歐盟並獲得監管機構授權的。

MiCA provides comprehensive regulation earlier than the U.S., with enforcement beginning in phases through 2024-2025. However, its approach is more restrictive - limiting issuers to regulated financial institutions from the start rather than creating a pathway for nonbank innovation.

MiCA比美國更早實施全面監管,並將於2024至2025年分階段執行。然而,其方法相對更保守——由一開始就將發行人限制為受監管的金融機構,並無特別為非銀行創新打開大門。

Hong Kong: Hong Kong's Stablecoin Ordinance, passed in May 2025, requires all issuers of stablecoins backed by the Hong Kong dollar to obtain a license from the Hong Kong Monetary Authority, with all stablecoins backed by high-quality, liquid reserve assets and the market value of the reserve pool equal to the par value of the stablecoins in circulation.

香港:香港於2025年5月通過的《穩定幣條例》,規定所有以港元作為擔保的穩定幣發行人,必須向香港金融管理局申請牌照,同時所有穩定幣都必須由高質素、具流動性的儲備資產作全額支持,而且儲備池市值需等同於流通中穩定幣的面值。

Hong Kong's approach targets local currency stablecoins specifically, positioning Hong Kong as a digital asset hub while maintaining monetary sovereignty.

香港的監管方針專門針對本地貨幣穩定幣,藉此確立香港作為數字資產樞紐的定位,同時維持貨幣主權。

Singapore: The Monetary Authority of Singapore (MAS) has established licensing frameworks through its Payment Services Act. Major stablecoin issuers including Circle and Paxos have obtained licenses. Singapore balances innovation support with consumer protection, requiring license holders to maintain capital adequacy, technology risk management, and AML/CFT controls.

新加坡:新加坡金融管理局(MAS)已透過《支付服務法》設立牌照框架。主要穩定幣發行商如Circle及Paxos已取得相關牌照。新加坡在支持創新與消費者保障之間取得平衡,要求持牌者維持資本充足、科技風險管理及反洗錢/反恐融資控制。

United Kingdom: The UK is developing stablecoin regulation through its Financial Services and Markets Act, treating certain stablecoins as regulated payment instruments. The approach focuses on systemic stablecoins that could impact financial stability, with proportionate regulation based on scale and usage.

英國:英國透過《金融服務及市場法案》制定穩定幣監管規例,將部分穩定幣視為受監管的支付工具。英國的方針鎖定有系統性風險、或足以影響金融穩定的穩定幣,並按規模及用途施加相應監管要求。

Compliance Challenges

Despite regulatory clarity improving, significant compliance challenges remain for PayFi participants:

儘管監管趨於明晰,PayFi參與者仍須面對重大合規挑戰:

Cross-Border Complexity: Payments are inherently cross-border, but regulations are jurisdictional. A stablecoin issuer must comply with regulations in every country where its stablecoin is used. This creates compliance complexity: KYC requirements differ across jurisdictions, reporting obligations vary, and sanctions lists are not uniform.

跨境複雜性:支付本質上跨越國界,但監管依然是按司法管轄區劃分。穩定幣發行人在其穩定幣流通的每一個國家都必須遵守當地規例,導致種種合規難題:不同司法區的KYC(認識你的客戶)規定、申報義務及制裁名單都不盡相同。

The GENIUS Act attempts to address this through provisions for foreign stablecoin issuers. The Act allows foreign payment stablecoin issuers to offer or sell in the United States under certain circumstances, with Treasury authorized to determine whether a foreign regime for regulation and supervision of payment stablecoins is comparable to requirements established under the GENIUS Act.

GENIUS法案嘗試通過制訂相關條文來處理外國穩定幣發行人問題。該法案在特定情況下允許外國支付穩定幣發行人於美國提供或銷售產品,並授權美國財政部決定外國有關穩定幣規管制度,是否與GENIUS法案規定的要求相當。

This "comparability" framework could enable mutual recognition: if the EU's MiCA regime is deemed comparable, MiCA-licensed stablecoin issuers could operate in the U.S. without separate licensing. However, comparability determinations involve complex policy negotiations.

此「相當性」框架可能促進監管互認:若歐盟MiCA制被視為「相當」,則獲MiCA牌照的穩定幣發行人便可於美國營運而無須另行申請牌照。然而,何謂「相當」屬複雜政策協商範疇。

Transaction Monitoring: AML compliance requires monitoring transactions for suspicious activity. With blockchain's transparency, this is theoretically easier than traditional banking - every transaction is publicly visible. However, identifying beneficial owners behind wallet addresses remains challenging.

交易監控:反洗錢合規需要對可疑交易進行監測。由於區塊鏈具備透明度,理論上比傳統銀行更易追蹤——所有交易均公開可見。然而,要查出錢包地址背後的實益擁有人仍具挑戰。

Solutions are emerging: blockchain analytics firms like Chainalysis, Elliptic, and TRM Labs provide transaction monitoring tools that identify high-risk wallets, trace funds, and flag suspicious patterns. Elliptic provides MoneyGram with blockchain analytics solutions for their Stellar integration.

解決方案陸續出現:如Chainalysis、Elliptic及TRM Labs等區塊鏈分析公司提供交易監控工具,可識別高風險錢包、追蹤資金流及標記可疑動態。Elliptic就為MoneyGram的Stellar整合提供了區塊鏈分析方案。

Sanctions Compliance: The GENIUS Act explicitly subjects stablecoin issuers to the Bank Secrecy Act, thereby obligating them to establish effective anti-money laundering and sanctions compliance programs with risk assessments, sanctions list verification, and customer identification.

制裁合規:GENIUS法案明確將穩定幣發行人納入《銀行保密法》監管,令發行人必須建立有效的反洗錢及制裁合規計劃,包括風險評估、制裁名單驗證及識別客戶身份。

Sanctions compliance is particularly complex for stablecoins because they can move globally without intermediaries. Traditional correspondent banking allows sanctions screening at multiple points. With stablecoins, enforcement depends on issuers and on-ramps/off-ramps implementing controls.

對於穩定幣,制裁合規尤其複雜,因其可在全球無中介情況下流轉。傳統國際匯款可於多個環節篩查制裁名單,而穩定幣則主要依賴發行人及進出資通道實施相關監控。

Circle demonstrated this capability in 2022 by freezing USDC associated with addresses sanctioned by the U.S. Treasury. This ability - built into the smart contract - ensures issuers can comply with lawful orders. However, it creates tension with blockchain's censorship-resistance ideals.

Circle於2022年展示了其凍結被美國財政部制裁地址相關USDC的能力。這種能力已寫入智能合約層面,可確保發行人遵守合法指令。但同時,也與區塊鏈抗審查的原則產生張力。

Privacy Considerations: Transaction monitoring and sanctions compliance require identifying users. This conflicts with cryptocurrency's privacy culture. The compromise emerging is selective disclosure: users provide identity to regulated on/off-ramps and issuers but can transact pseudonymously on-chain, with issuers retaining ability to freeze wallets when required by law.

私隱考慮:交易監控及制裁合規涉及用戶身份識別,與加密貨幣一向講求私隱的文化產生衝突。現時有一種折衷方案開始浮現:選擇性披露——用戶只在受規管的進/出資通道及發行人處提供身份,每當在鍊上轉賬仍可使用假名式地址,但如有法定需要,發行人仍有權凍結錢包。

Regulatory Risks

Despite progress, regulatory uncertainty remains in several areas:

雖然取得進展,但部分領域尚存監管不確定性:

Algorithmic Stablecoins: The GENIUS Act focuses on fiat-backed payment stablecoins. Endogenously collateralized stablecoins - digital assets pegged to the value of another digital asset rather than fiat - are not explicitly banned but the Treasury Secretary must conduct a study on non-payment stablecoins within one year.

算法穩定幣:GENIUS法案對象為以法定貨幣作擔保的支付型穩定幣。那些以其他數字資產(非法幣)擔保的穩定幣未被明文禁止,但法案要求財政部長於一年內就非支付型穩定幣展開研究。

This leaves open questions about algorithmic stablecoins like DAI (backed by crypto collateral) and other non-payment stablecoins. The House's competing STABLE Act proposed a two-year moratorium on such stablecoins. Future regulation may restrict or ban them.

這使關於如DAI(以加密資產擔保)之類的算法穩定幣及其他非支付型穩定幣的去向存疑。美國眾議院的STABLE法案版本曾建議對這類穩定幣設兩年禁令,未來監管可能進一步限制或禁止其發展。

DeFi Integration: Many PayFi use cases integrate with DeFi protocols: liquidity pools, lending markets, yield aggregators. How do AML obligations extend to these interactions? Can a compliant stablecoin issuer allow its tokens to be used in DeFi protocols that lack KYC? These questions remain unresolved.

DeFi整合:許多PayFi應用場景都會與DeFi協議聯動,如流動性池、借貸市場及收益聚合器。反洗錢合規責任如何延伸至這些互動?合規穩定幣發行人可否容許其代幣於欠缺KYC的DeFi協議上使用?這些問題尚未有定案。

Taxation: Cryptocurrency taxation is notoriously complex. Does converting USD to USDC create a taxable event? What about on-chain transfers? The answer varies by jurisdiction. In the U.S., stablecoins are generally treated as property, meaning each conversion could technically trigger capital gains reporting even if gains are negligible (due to 1:1 peg).

稅務問題:加密貨幣的稅務規定極為複雜。將美元兌換成USDC是否構成應稅行為?鍊上轉帳又如何?不同司法區有不同答案。在美國,穩定幣通常被視為資產,即每次兌換理論上都須申報資本利得,即使因與美元一對一掛鉤而實質利得微乎其微。

The GENIUS Act directs Treasury to address tax issues, but implementation rules are still being developed. Clearer guidance is needed to avoid turning every stablecoin payment into a complex tax reporting event.

GENIUS法案要求財政部處理有關稅務問題,但具體細則仍待制訂。現時亟需更明確指引,以免每次穩定幣支付均釀成複雜的稅務申報事件。

Global Coordination: Without international coordination, regulatory arbitrage becomes possible. If the U.S. imposes strict requirements but offshore jurisdictions do not, issuers may charter elsewhere. The GENIUS Act's comparability framework attempts to address this by requiring foreign issuers to meet equivalent standards.

全球協調:若無國際協調,監管套利現象隨時湧現。例如美國規定嚴格,而離岸地區寬鬆,發行人便可能選擇在海外設立。GENIUS法案的相當性框架嘗試要求外國發行人須達到等同標準去解決這一問題。

However, achieving global regulatory harmonization is notoriously difficult. Payments historically operated within fragmented national regimes. Blockchain's borderless nature makes this fragmentation more problematic - but also creates pressure for coordination.

但真正推動全球監管協調極其困難。傳統支付歷來服務於割裂的國家體制,而區塊鏈的無國界特性令這種割裂更顯問題,同時也為協調施加了壓力。

The Path Forward

Regulatory clarity has improved dramatically with the GENIUS Act and similar frameworks globally. This clarity enables institutional adoption: banks and asset managers can build PayFi infrastructure knowing the regulatory parameters.

GENIUS法案及全球類似框架極大提升了監管明晰度,令機構投資者能安心涉獵——銀行及資產管理等可在已知監管邊界下建立PayFi基礎設施。

However, regulation will continue evolving as use cases emerge and risks materialize. Key areas to monitor include:

然而,隨著應用場景不斷湧現及風險逐步明朗,監管仍會不斷演變。值得關注的重點包括:

- CBDC Interaction: How will regulations treat interactions between stablecoins and central bank digital currencies?

- 中央銀行數字貨幣(CBDC)交互:監管會如何處理穩定幣與CBDC的交互?

- Cross-Border Frameworks: Will major economies achieve mutual recognition of regulatory regimes?

- 跨境框架:主要經濟體能否實現監管互認?

- DeFi Integration Rules: How will regulators address stablecoins used in decentralized protocols?

- DeFi整合規則:監管機構會如何規範在去中心化協議內使用的穩定幣?

- Privacy Technologies: How will regulations treat privacy-preserving technologies like zero-knowledge proofs if applied to stablecoins?

- 私隱技術:監管會如何看待如零知識證明這類應用於穩定幣的保密技術?

- Insurance Requirements: Should stablecoin issuers be required to carry insurance protecting holders if reserves are compromised?

- 保險要求:穩定幣發行人會否須購買保險,以保障持有人在儲備失守時的利益?

The regulatory landscape is stabilizing, but not static. PayFi participants must maintain active compliance programs, monitor regulatory developments globally, and engage constructively with policymakers to shape frameworks that protect consumers while enabling innovation.

監管環境雖逐漸穩定,卻仍然處於不斷變化之中。PayFi參與者必須積極維持合規措施,密切留意全球監管動態,並與政策制定者正面交流,促成既保障消費者又推動創新的框架。

Risks and Challenges

PayFi's promise is significant, but so are the risks. Technical vulnerabilities, economic instabilities, regulatory uncertainties, and adoption barriers all threaten to slow or derail the convergence between payments and DeFi. A balanced assessment requires examining these challenges honestly.

PayFi潛力巨大,但風險亦不容忽視。無論是技術漏洞、經濟不穩、監管不確定性,還是採用障礙,都可能減慢甚至中斷支付與DeFi的融合。要作出平衡評估,須誠實面對這些挑戰。

Technical Risks

Scalability and Congestion: Blockchain networks have finite capacity. When demand spikes, transaction fees rise and confirmation times slow. Ethereum experienced this during the 2021 NFT boom, with transaction fees reaching $50-200 for simple transfers. Such fees make small payments economically unviable.

可擴展性與擁塞:區塊鏈網絡容量有限。當需求暴增時,交易費升高,確認時間變慢。以太坊在2021年NFT熱潮期間,單次簡單轉帳費用高達50至200美元,如此高昂費用令小額支付難以成立。

Layer-2 solutions and high-performance Layer-1 chains address this, but risks remain. If a payment processor builds on a specific blockchain and that network experiences congestion or outages, payment flow interrupts. Solana has experienced network disruptions multiple times, though reliability has improved significantly.

Layer-2方案和高效能Layer-1鏈可以緩解問題,但風險並未根除。若支付服務商建基於特定公鏈,而該網絡遇上擁塞或故障,支付流即時受阻。Solana就曾多次出現網絡中斷,雖然可靠性已大幅提升。

Smart Contract Vulnerabilities: Bugs in smart contract code can be catastrophic. Once deployed, many smart contracts are immutable - bugs cannot be easily fixed. The history of DeFi includes numerous exploits: reentrancy attacks, flash loan exploits, governance hijacks. If PayFi infrastructure contains vulnerabilities, attackers could steal funds or disrupt operations.

智能合約漏洞:智能合約代碼中的漏洞可造成災難性後果。部署後的智能合約往往不可更改,漏洞難以後補。DeFi歷史上不乏漏洞利用:重入攻擊、閃電貸漏洞、治理劫持等。若PayFi基礎設施存有安全隱患,攻擊者可趁機盜走資金或癱瘓業務。

Mitigation requires rigorous security practices: formal verification, multiple independent (下文未完,如需繼續,請告知。)audits、漏洞懸賞計劃,以及逐步推出並限制初期存款。但即使是經過詳細審計的合約,也可能存在只會在實際運作時才顯現的微妙漏洞。

跨鏈橋風險:許多 PayFi 用例涉及跨區塊鏈穩定幣轉移——例如 Ethereum 去 Polygon、Solana 去 Base 等。橋樑漏洞是加密歷史上損失最慘重的事件之一,曾有數十億資金被盜。Circle 的跨鏈轉移協議 (CCTP) 提供原生解決方案,但不是所有轉移都會用上,而且橋樑安全依然是持續的隱患。

密鑰管理:區塊鏈安全靠私鑰控制。用戶遺失私鑰,資金無法追回。企業熱錢包若被盜,資金可即時失竊、無法追討。傳統銀行有恢復及詐騙逆轉機制,區塊鏈則沒有。

可行解決方案包括多簽錢包(多把匙批准交易)、硬件保安模組,以及帳戶抽象(具備社交恢復功能的智能合約錢包)。但這些方案增添複雜性,尚未成主流使用。

經濟風險

穩定幣掛鈎風險:穩定幣靠贖回承諾與儲備支撐來維持價值。但掛鈎可失效。2023年3月,Circle 部份儲備於倒閉的矽谷銀行,USDC 一度跌至 $0.87,事後 Circle 證實儲備安全才回復掛鈎。

若主要穩定幣於危機中脫鈎,建立於其上的 PayFi 系統可遭遇巨大動盪。商戶預計收取$10,000 結算,若脫鈎,實收或只有$8,000 等值。這類波動直接削弱支付應用場景。

儲備透明度與審計:Circle 每月公佈 USDC 儲備證明報告,確保透明。但證明不等同全面審計。Tether 的儲備成份曾屢受質疑,雖然透明度有所提升。

GENIUS 法案要求大型發行人需詳細申報及審計,有助提升透明度。但若發行人失實陳述儲備(如部份演算法穩定幣),正式發現前或已造成重大損失。

流動性危機:即使儲備充足的穩定幣也可出現流動性錯配。若儲備投放美債(幾日才可變現),贖回突增(即時要現金),發行人便可能無法履行承諾。這正是傳統銀行危機的典型情境:資產長期穩健、短期卻缺乏流動性。

Circle 和 Tether 曾成功處理過數十億美元的大規模贖回。但若真正恐慌——所有人同時申請贖回——現時規模下仍未經歷過。

息差競爭:傳統銀行給存戶利息極低,靠放貸與存款利息差賺取收益。GENIUS 法案明確禁止穩定幣發行人向持有人支付利息或收益。

這令競爭格局出現變化。用戶持有 USDC 沒利息,可將美元存入貨幣基金取4-5%回報,又憑甚麼持有 USDC?發行人不能靠息口競爭,只能拼效用(即時結算、可編程性、全球覆蓋等)。這是否足以驅動大規模採用仍是未知之數。

法規及政治風險

法規逆轉:GENIUS 法案由兩黨支持及總統背書下通過。但政局風雲變幻,未來政府或國會可能增設限制、提高儲備要求、限制跨境用途,甚至試圖禁制被視為威脅貨幣主權的穩定幣。

中國2021年已禁加密貨幣買賣。印度亦曾考慮類似舉措。美國雖然有 GENIUS 法案,長遠來說,法規風險不會完全消失。

制裁及執法過當:要求穩定幣發行人能凍結資金,帶來新管控風險。若政府要求凍結不限於明確違法——例如用於打壓政治異見、未經批准交易、或單純因涉及某制裁地區而非特定人士——穩定幣或淪為審查工具。

絕非假設傳統銀行已被要求凍結帳戶,即使無明確違法。如穩定幣沿用傳統銀行的管控點,也會複製此等易受政治壓力的弱點。

碎片化:若各司法區各自訂立不兼容的規例,最終只會導致穩定幣市場碎片化。合乎美國 GENIUS 法案的穩定幣或無法在歐洲使用,合乎歐盟 MiCA 的穩定幣又或會被亞洲限制。這與 PayFi 提倡的無縫全球支付背道而馳。

GENIUS 法案的可比性框架亦試圖解決這一問題,但國際協作仍殊不容易。如協調不成,PayFi 只會碎片化為不同地區間互不兼容的系統,與其全球願景背道而馳。

普及障礙

用戶體驗:即使技術已改善,區塊鏈系統對普羅大眾依然複雜。私鑰、gas 手續費、網絡選擇、錢包管理等,令非技術用戶困惑。若 PayFi 仍要用戶了解區塊鏈運作原理,大規模普及毫無可能。

解決方法有帳戶抽象(將複雜性隱藏)、直接整合支援法幣存取閘道於應用內、以及託管服務(用戶不用自主管理私鑰)。不過,每種方案在用戶友善與區塊鏈去中心化價值間都有取捨。

商業慣性:現存支付系統,即使低效,總算可用。企業早已接入信用卡處理、會計軟件、薪資支出等。轉用 PayFi 需重新整合、員工培訓和承受新風險。許多商戶認為暫無足夠誘因抵消這筆過渡成本。

波動印象:即使穩定幣在掛鈎,整體加密貨幣波動形象令部分用戶卻步。即使財政人員對公司有信心,對加密貨幣投機與高風險特質仍抱有戒心。教育和長期穩定表現可慢慢扭轉觀感,但這不容易。

網絡效應:支付系統講求網絡效應——參與者愈多,愈具價值。USDC 已可用於逾 5 億錢包產品,但這尚不到全球網民一成。PayFi 未達主流滲透率前,必遇「雞生蛋、蛋生雞」問題:商戶見用戶未用不敢收,用戶見商戶未收又懶用。

存在性問題

除以上風險外,PayFi 長遠前景亦有更根本性疑問:

央行數碼貨幣競爭:央行如推出具類似屬性的官方數碼貨幣(即時結算、可編程),屆時穩定幣還有無存在價值?CBDC 具監管優勢(無儲備風險、政府背書、強制接受),足以排擠私營穩定幣。

但 CBDC 未必覆蓋所有穩定幣優點。政府或因資本管制限跨境用途、因規監避規而限可編程性。穩定幣與 CBDC 或能共存,各自填補不同需要。

傳統支付系統進化:傳統支付系統也不會原地踏步。FedNow、PIX、即時 SEPA、UPI 等說明傳統基建一樣可實時結算,毋須區塊鏈。若傳統系統解決結算速度問題,PayFi 優勢又何在?

答案在於可編程性與組合彈性——這難以為舊系統加入。但如舊有系統陸續具備編程功能,界線即將模糊。

安全與去中心化取捨:真正去中心化的系統更難監管,也更易淪為非法用戶溫床,一旦出錯亦難以追回。合規 PayFi 系統則為了符合法規和保障用戶,犧牲部份去中心化。這實際或令其變成「換湯不換藥」的傳統金融——只不過更快更便宜,實質分別有限。

如何於促進創新、減少單點失敗的去中心化與合規、用戶保障的中心化之間取到平衡,仍是未解難題。

風險應對

了解風險,才可積極應對:

- 技術層面:投資安全審計、漏洞懸賞、嚴格驗證及循序上線

- 經濟層面:保持保守儲備、提供透明報告、針對流動危機嚴格壓力測試

- 法規層面:主動與政策制定者良好互動,前置構建合規架構,協助促進國際協作

- 普及層面:簡化用戶體驗、展現強大價值、投資教育和生態建設

風險雖然真切,但絕非不能克服。傳統支付在其發展歷程同樣面對過:支票詐騙、信用卡盜竊、電子銀行安全、跨境監管等。各種難題最終都靠技術、regulation, and best practices. PayFi will likely follow a similar path, with risks being managed as the ecosystem matures rather than eliminated entirely.

監管同最佳做法。PayFi 好可能都會行一條類似嘅路線,風險會隨住生態系統成熟而被管理,而唔係完全消除。

The Macro Picture and Future Outlook

宏觀圖景同未來展望

PayFi is not merely an incremental improvement in payments technology. It represents a structural shift in how value moves through the global economy. Understanding its macro implications and future trajectory requires examining the convergence at multiple scales: technical infrastructure, economic incentives, regulatory evolution, and behavioral adoption.

PayFi 唔只係支付技術上嘅一個小改良。佢代表住價值點樣喺全球經濟中流動嘅一個結構性轉變。要明白佢嘅宏觀影響同未來路向,需要喺多個層面觀察其匯聚情況:技術基建、經濟誘因、監管演變同用戶行為嘅採納。

Five-Year Outlook: 2025-2030

五年展望:2025-2030

By 2030, PayFi infrastructure is likely to have matured significantly. Key developments to watch include:

到 2030 年,PayFi 嘅基礎設施好可能已經相當成熟。幾個值得留意嘅關鍵發展包括:

Mainstream Stablecoin Adoption: By 2030, on-chain value is projected to grow to $10-25 trillion. This would represent roughly 1-2% of global financial assets. While small by traditional finance standards, it would mark an inflection point where stablecoins become standard treasury management tools, not exotic alternatives.

Stablecoin market cap reached $251.7 billion by mid-2025. If growth continues at current trajectory (doubling every 2-3 years), market cap could reach $500 billion-$1 trillion by 2027-2028. At that scale, stablecoins would rival many national currencies in circulation.

穩定幣主流化:到 2030 年,鏈上價值預計會升到 10 至 25 萬億美元左右。呢個大約係全球金融資產嘅 1-2%。雖然以傳統金融標準嚟講算細,但會係一個分水嶺——屆時穩定幣會變成標準嘅財資管理工具,而唔只係另類選擇。

穩定幣市值到 2025 年中已經去到 2,517 億美元。如果增長勢頭保持(每兩三年翻一番),市值到 2027-2028 年就有機會升到 5,000 億到 1 萬億美元。呢個級別嘅流通量,穩定幣已經足以同好多國家貨幣媲美。

Institutional Treasury Integration: Large corporations already maintain complex treasury operations: multi-currency accounts, hedging strategies, liquidity management. PayFi enables:

- 24/7 Operations: No waiting for banking hours or settlement windows

- Programmable Cash Management: Automated sweeps, rebalancing, and allocation via smart contracts

- Global Liquidity Pools: Single stablecoin treasury deployed instantly to any subsidiary or obligation worldwide

- Yield Optimization: Automated routing to highest-yield protocols within risk parameters

機構財資整合:大型企業本身已經有複雜嘅財資運作,包括多種貨幣賬戶、對沖策略、流動性管理。PayFi 可以做到: - 全天候 24/7 運作:無需等待銀行營業時間或結算窗口

- 可編程現金管理:透過智能合約自動化資金調度、再平衡同分配

- 全球流動資金池:同一個穩定幣資金庫即時支援全球各地分公司或者任何應付責任

- 收益優化:自動將資金流向風險範圍內最高回報嘅協議

By 2030, treasury management software will likely integrate blockchain settlement as a standard feature alongside traditional banking. The question won't be whether to use stablecoins, but how much of the treasury to hold on-chain.

到 2030 年,財資管理軟件好可能會將區塊鏈結算列做同傳統銀行一樣嘅標準功能。屆時,問題已經唔係用唔用穩定幣,而係應該有幾多資金放上鏈。

Cross-Border Payment Transformation: Global remittances exceed $700 billion annually, with fees averaging 6.2%. If PayFi captures even 30% of this market by 2030, it would represent $200 billion in annual flows, saving remittance senders approximately $10-12 billion annually in fees.

跨境支付革新:全球每年匯款超過 7,000 億美元,平均手續費有 6.2%。如果 2030 年時 PayFi 佔到 30% 市場份額,每年就有 2,000 億美元係經 PayFi 流動,可以幫寄款人一年慳返差唔多 100 至 120 億美元手續費。

More significantly, the speed improvement transforms lives. Workers supporting families abroad can send money that arrives in minutes, not days. Recipients can hold dollar-stable value rather than immediately converting to depreciating local currency. The economic impact in developing nations could be substantial.

更重要係,速度提升會改變好多人嘅生活。外地工作嘅工人可以即刻畀家人收款,唔再等幾日先收到錢。收款人仲可以持有美元穩定價值,唔使即刻換成會貶值嘅本地貨幣。呢個對發展中國家嘅經濟影響可以好大。

Embedded Finance Proliferation: Today, most embedded finance (payments integrated directly into platforms) runs on traditional rails. Stripe, PayPal, and Adyen power checkout flows, but settlement remains slow and expensive.

嵌入式金融普及:而家大部分嵌入式金融(即平台直接內置支付)都係用緊傳統系統。Stripe、PayPal 同 Adyen 雖然主導結賬流程,但結算依然好慢同貴。

By 2030, embedded PayFi could be standard: e-commerce platforms settling merchants instantly, creator platforms splitting revenue automatically, marketplaces providing programmatic escrow without third-party trust services. The user experience looks similar, but the backend transforms.

到 2030 年,嵌入式 PayFi 有機會變做新標準:電商平台即時清結商戶資金,創作者平台自動分帳,市集自動安排合約托管而唔需要第三方信託服務。用戶睇落好似冇咩分別,但背後運作已經完全唔同。

Regulatory Maturation: The GENIUS Act provides a U.S. framework, but global coordination remains incomplete. By 2030, expect:

- Mutual Recognition Agreements: Major economies accepting each other's stablecoin licenses, similar to financial passporting

- CBDC-Stablecoin Coexistence Frameworks: Regulations clarifying how private stablecoins interact with central bank digital currencies

- Standardized Reporting: Unified formats for reserve attestations, transaction monitoring, and tax reporting across jurisdictions

- International Coordination: G20 or similar bodies establishing baseline standards for stablecoin issuance and operation

監管成熟:「GENIUS 法案」為美國提供咗一個框架,但全球性協調仍未完善。到 2030 年,有機會見到: - 互認協議:主要經濟體互相承認穩定幣牌照,好似金融護照一樣

- CBDC 同穩定幣共存框架:法規界定私人穩定幣同央行數字貨幣點樣共存互動

- 標準化報告:全球統一儲備證明、交易監察同稅務申報格式

- 國際協調:G20 或類似組織制定穩定幣發行及營運基線標準

This regulatory maturity will reduce uncertainty and enable broader institutional adoption.

監管成熟後,市場不確定性會大大減低,更有利機構入場。

Ten-Year Vision: 2025-2035

十年展望:2025-2035

Looking further out, PayFi could fundamentally reshape several aspects of the global financial system:

望遠啲,PayFi 好有可能徹底改變全球金融系統嘅多個層面:

Real-Time Global Economy: Today, the global economy operates in batches. Stock markets close. Banks have operating hours. Settlement takes days. PayFi enables a truly 24/7/365 economy where value moves continuously. The implications are profound:

實時全球經濟:依家全球經濟做嘢都係分批進行,股票市場要收市,銀行有營業時間,結算要等幾日。PayFi 可以實現真真正正全年無休、24/7/365 不停運作嘅經濟——價值流動唔停。影響係好深遠:

- Capital Efficiency: If settlement happens instantly, less capital sits idle. A business can receive payment and redeploy it within seconds rather than days.

- Global Coordination: Teams in different time zones can transact without waiting for overlapping business hours.

- Market Liquidity: Financial markets can operate continuously without the daily close that creates liquidity gaps and price discontinuities.

- 資本效率:如果結算可以即時完成,就唔使咁多資金閒置。一間公司可以即收即用,而唔使等幾日先可以再調動。

- 全球協作:唔同時區嘅團隊交易都唔使再等共同營業時間。

- 市場流動性:金融市場可以 24 小時不停運作,唔會因每日收市產生流動性斷層或者突然大幅波動。

Programmable Monetary Policy: This is highly speculative, but consider: if a significant portion of the economy operates on programmable money (stablecoins, CBDCs with smart contract logic), monetary policy could become more precise. Instead of blunt tools like interest rate changes, central banks could:

- Target stimulus to specific sectors or demographics via conditional transfers

- Implement negative interest rates on hoarded cash to encourage spending

- Create time-limited money that expires if not used, forcing circulation

可編程貨幣政策:呢個比較前瞻但值得諗——如果大部分經濟用可編程貨幣(穩定幣、CBDC 配合智能合約邏輯)運作,貨幣政策可以更精細。中央銀行可以唔再只用加減息呢啲「大錘」工具,而係: - 用有條件轉帳針對唔同行業或者特定人群紓困

- 對閒置現金施加負利率,鼓勵消費

- 發行限時消費貨幣,唔用會自動作廢,強制資金流通

These capabilities raise profound questions about government power, individual freedom, and economic structure. They are not inevitable - they depend on political choices. But they become technically possible in ways they were not before.

呢啲技術能力帶嚟巨大嘅討論空間,包括政府權力、個人自由同經濟結構。唔一定會實現,視乎政治決定,但技術上已經可行,以前唔得嘅而家變得有可能。

Supply Chain Revolution: PayFi combined with IoT and smart contracts could automate supply chains comprehensively:

- Manufacturer ships goods → Smart contract releases payment when GPS confirms delivery

- Quality sensors detect defect → Payment withheld automatically

- Inventory drops below threshold → Smart contract places order and transfers payment

供應鏈革命:PayFi 加埋物聯網同智能合約,可以令供應鏈自動化得更徹底: - 生產商出貨 → GPS 確認送到貨,智能合約自動放款

- 質量感應器發現有問題 → 付款自動被扣起

- 庫存低於臨界點 → 智能合約自動落單同埋付款

This requires integration far beyond payments (IoT devices, oracles providing real-world data, dispute resolution mechanisms), but the foundation is programmable money that can respond automatically to external events.

呢個要整合唔止支付(仲要有物聯網裝置、現實數據預言機、爭議解決機制等等),但基石係可編程貨幣可以自動回應外部事件。

Creator Economy Transformation: The creator economy is expected to surpass $500 billion by 2030, with PayFi helping content creators finance production by providing funds beforehand and returning them automatically based on streaming revenue.

Imagine a creator economy where:

- Artists receive micro-payments in real-time as their content streams (not lump sums quarterly)

- Collaborative projects automatically split revenue based on smart contract terms

- Fans invest directly in creators via tokenized stakes in future earnings

- Platforms pay creators instantly rather than accumulating balances that pay out monthly

創作者經濟變革:到 2030 年,創作者經濟規模預計會超過 5,000 億美元,PayFi 可以協助內容創作者提前籌集製作資金,再根據內容播放收入自動還款。

想像一個咁嘅創作者經濟:

- 藝術家可以即時收到按播放量計算嘅微支付(唔使一季結一次)

- 多人合作項目自動根據智能合約條款分賬

- 粉絲直接用代幣化股份參與創作者未來收益

- 平台即時畀錢創作者,唔係要等平台累積結餘後一個月先出糧

This fundamentally changes creator business models. Instead of chasing brand deals and sponsorships (which favor large creators), smaller creators could build sustainable income from direct audience support distributed efficiently via programmable payments.

呢個會根本改變創作者收入模式。細規模創作者唔使靠搵品牌合作或者贊助(通常只係大戶先攞到),可以靠觀眾直接支持、効率分配嘅可編程支付,建立持續穩定收入。

Scale Implications

規模影響

The $1.8 quadrillion in annual global payment flows provides context for PayFi's potential scale. If only 10-20% shifts to PayFi rails, that's $180-360 trillion annually - truly massive volume.

每年全球支付金額有 1,800 萬億美元,用嚟比較 PayFi 的增長潛力。如果有 10-20% 嘅流量轉到 PayFi,已經係一年 180-360 萬億美元——真係天文數字。

However, that metric may be misleading. PayFi is not purely about shifting existing flows. It's about enabling new flows that were previously impossible or uneconomic:

不過呢個數字其實可能會有誤導。PayFi 唔淨係將現有支付搬過嚟,更重要係可以開啟以前唔可能或者不經濟嘅新支付流:

- Micro-payments for content (previously unviable due to transaction costs)

- Instant freelancer payments (previously delayed by international wire processing)

- Programmable splits and cascades (previously requiring complex intermediaries)

- Real-time treasury operations (previously constrained by banking hours)

- 內容微支付(以前因手續費太貴唔可行)

- 即時自由職業者收款(以前要國際電匯、成日遲到)

- 可編程分賬、層疊分配(以前要好多中介系統)

- 實時財資操作(以前銀行時間限制)

These new flows could ultimately exceed traditional payment volumes because programmability enables use cases that don't fit traditional payment models.

呢啲新型支付模式,最終可能連傳統支付總量都會超越,因為可編程性令到好多以前唔可能嘅應用變得可行。

Indicators to Monitor

需要觀察嘅指標

To assess whether PayFi is achieving its potential, monitor these metrics:

想知道 PayFi 有冇達到佢預期潛力,可以睇下以下幾個指標:

Stablecoin Circulation and Velocity: USDC circulation has grown to approximately $70-75 billion by mid-2025. Track growth rate - is it accelerating, steady, or decelerating? Also monitor velocity (how frequently stablecoins change hands). High velocity indicates active use for payments, not just holding as savings.

穩定幣流通量同周轉率:USDC 流通量到 2025 年中已經去到 700-750 億美元。要追蹤增長速度——係加快、持平定減慢?仲要睇穩定幣周轉率(幣喺網絡上流轉幾頻密),周轉得快代表真係有用作支付,而唔止係用嚟儲。

Transaction Volume vs. Speculation: Blockchain transaction data is public but requires interpretation. High volumes might indicate speculation (trading) rather than payments use. Look for metrics like stablecoin payment volumes, which reached $19.4 billion year-to-date in 2025, distinguished from total transfer volumes.

交易量同投機分野:區塊鏈交易數據係公開嘅,但要分辨清楚。高交易量有時係炒賣,未必代表支付。要睇下例如穩定幣支付總額,2025 年至今達到 194 億美元,區分總轉帳量同實際支付量。

Merchant Adoption: How many merchants accept stablecoin payments? Are major payment processors enabling stablecoin settlement? Merchant acceptance is a leading indicator of mainstream adoption.

商戶接受程度:有幾多商戶收穩定幣支付?大型收單商支唔支援穩定幣結算?商戶接受度係主流普及嘅風向標之一。

Institutional Announcements: Monitor corporate treasurers, asset managers, and banks announcing stablecoin integration. Each major institution entering the space validates the infrastructure and drives further adoption.

機構動向:觀察下企業財資、資產管理公司、銀行有冇宣布試行穩定幣業務。每一間大機構入場,都係對基建嘅認同,進一步推動普及。

Regulatory Developments: Track international coordination efforts. Are more countries passing frameworks similar to the GENIUS Act? Are mutual recognition agreements emerging? Regulatory clarity accelerates adoption.

監管進展:要睇下各國有冇參與國際協調,有冇更多地方立類似 GENIUS 法案?有冇互認協議?規則愈清晰,普及步伐愈快。

Cost and Speed Metrics: Compare traditional payment costs and speeds to PayFi alternatives. If the gap widens (PayFi gets faster and cheaper while traditional payments remain static), migration will accelerate.

費用同速度比較:比較傳統支付同 PayFi 喺成本、速度上有幾大分別。如果差距愈嚟愈大(PayFi 又平又快,傳統手續費冇變),換車速度會好快。

Potential Failure

潛在失敗Here is the requested zh-Hant-HK translation, following your formatting guidelines (skipping translation for markdown links):

Modes

樂觀情境假設持續進步,但PayFi亦有可能未能發揮其潛力。主要失敗模式包括:

監管限制:如果主要經濟體禁止或嚴格限制穩定幣(美國於GENIUS法案後情況不大,但其他地區亦有可能),PayFi增長將會停滯。

安全漏洞:PayFi主要基礎設施(穩定幣發行商、大型跨鏈橋、主導智能合約平台)遭受重大攻擊,或會動搖信心並引發監管打擊。

CBDC取代:若中央銀行發行具備優越功能的數碼貨幣,並以法規強制或禁止其他替代品,私人穩定幣或被擠出市場。

用戶體驗失敗:如果區塊鏈支付對普羅大眾來說依然過於複雜,普及程度只能停留於加密愛好者層面,無法走向主流。

傳統機構適應:如傳統支付系統能在不採用區塊鏈的情況下(如升級ACH、設置API層的即時支付網絡、或集中式結算所)成功整合PayFi最優秀的特性(即時結算、可編程性),去中心化基礎設施的獨特價值將會削弱。PayFi的優勢就只剩下對去中心化的意識形態偏好,而非實際上的優越性。

協作失敗:若區塊鏈生態系仍然支離破碎(鏈之間不兼容、穩定幣不能互通、標準各自為政),無縫全球支付的願景無法實現。網絡效應需要網絡對標準的共識。

最可能的結果既非全面成功,也非徹底失敗,而是呈現混合格局:PayFi覆蓋部份應用場景(如跨境匯款、司庫操作、嵌入式金融),傳統系統保留其他場景(如消費者信用卡、本地零售等)。問題只在於每套系統可以佔據1.8萬萬億美元年度支付流量的百分比多少。

超越支付:更廣泛的轉變

最終,PayFi體現了一場更大的轉型:互聯網、金融及可編程邏輯的融合。互聯網讓資訊流動即時並全球化。PayFi正嘗試為價值做到同樣事。互聯網推動新商業模式(搜尋引擎、社交網絡、電子商貿),這些在紙媒/廣播時代是不可能的。PayFi或可實現我們尚未全面構想過的新型金融模式。

當金錢變得可編程 — 即能根據條件自動移動、按既定規則自動分拆、或因事件而鎖定自我 — 金融的本質就會轉變。它不再只關於交易流程,而是編碼人際關係和自動化協議。

這遠不止支付變快變便宜。它意味著二十億名無銀行戶口、但有智能手機的成年人能夠被金融服務覆蓋。意味著創作者及小企業毋須門檻即可獲得資金。意味著貨幣流動透明、可審計,減少貪污腐敗。意味著新型經濟組織形式出現,我們只剛剛開始想像。

宏觀層面來看,我們正處於一個根本性基礎設施轉變的早期階段。就像由支票轉向電子ACH、由現金轉向信用卡、由櫃台銀行服務過渡到手機應用程式,以區塊鏈為基礎的可編程支付轉型也需要時間。它將面對阻力、經歷挫折、並需持續調整。

但大方向是清晰的。即時結算、可編程性、全球化、透明操作等組合,明顯優勝於為互聯網時代之前設計的系統。不論是完全用區塊鏈、還是傳統與去中心化混合架構,甚至傳統系統借鑒區塊鏈原則,2035年的支付格局都會與2025年大相徑庭。

這條1.8萬萬億美元的大問題,不是會否改變,而是變化有多快、怎樣變、以及誰會領先、誰會落後。

最後思考

PayFi — 支付與去中心化金融的融合 — 超越了技術創新範疇。它標誌著全球經濟價值流動結構的演變,動力來自傳統支付流程中被困的時間價值的釋放、金錢本身的可編程性、以及區塊鏈基礎設施與主流金融的融合。

全球支付行業每年處理1.8萬萬億美元、34億億筆交易,產生2.4萬億美元收入。儘管規模龐大、數碼化持續數十年,效率瓶頸依然存在:結算延遲、昂貴的跨境匯款、流動資本被鎖、流程不透明。PayFi以即時結算、低成本基建、自動化可編程邏輯,針對這些基本掣肘。

基建亦正飛速成熟。穩定幣市值於2025年中達到2,517億美元,而USDC單在2024年11月的月度交易量已達1萬億美元。高性能區塊鏈網絡如Solana、Stellar及Ethereum L2方案,提供即時結算基礎。BlackRock、Fidelity、Visa、MoneyGram等傳統金融機構已投資或與穩定幣基建合作。美國於2025年7月實施了全面穩定幣法例—GENIUS法案,提供監管清晰度,助力主流採用。

應用不只簡單的資金轉移。跨境匯款費用從6%及多日延誤,下調至1-2%並幾乎即時到賬。供應鏈融資及發票貼現自動化、容易、平價地通過智能合約實現。即時工資可讓員工隨完工即提薪無需等月結。商戶可用即時結算且費用低於1%,遠低於信用卡2-3.5%。

亞洲已成PayFi採用的活躍區域。東南亞匯款流於2025年預計接近1,000億美元。MoneyGram與Stellar合作,於超過180個國家提供現金<->加密幣雙向入口,使穩定幣可以在全球數碼美元和本地經濟間搭橋。新加坡、香港、日本等地的進步監管架構,既鼓勵創新亦保障消費者。

機構採用是對基建的肯定。資產管理人、支付平台、銀行,不僅僅是試驗,而是真正投放資本、建設基礎設施、將PayFi納入生產系統。這種機構擁抱有經濟意義:浮存資金解放釋放萬億美元工作資本;圍繞流動性供應、可編程服務的新盈利模式湧現;競爭格局轉變,舊勢力要適應否則被淘汰。

風險仍然存在。智能合約技術漏洞、穩定幣若脫錨所致經濟風險、各司法區監管不明朗、用戶體驗障礙等都是挑戰。GENIUS法案針對不少監管疑慮,但全球協調、CBDC互動、DeFi整合等問題仍未完全解決。

展望未來,市場預測鏈上價值有望於2030年增長至10-25萬億美元。這將是拐點:穩定幣成為標準司庫工具、跨境支付徹底革新、嵌入式金融在數碼平台遍地開花。2035年,支付格局也許面目全非—全球即時運作、貨幣智能自動流轉、供應鏈可即時反應狀況、創作者經濟收入源源不絕不再「分批」派發。

整體體量雖重要但具誤導性。年度1.8萬萬億美元支付流量只反映市場規模,PayFi的影響遠不只讓既有流動搬家。它釋放了全新、原本不現實的流量:內容微支付、全球自由工作者即時收款、可編程收入分拆、即時司庫操作。這些新能力最終可超越傳統支付體量。

要追蹤PayFi發展,請觀察這些指標:穩定幣流通和交易速度、商戶採納率、機構發布消息、重要司法區監管進展,以及傳統支付與PayFi速度成本差距。這些數字會反映PayFi是正突破潛力,還是在面對難以跨越的阻礙。

支付與去中心化金融的融合,不只是交易更快更平,只是這些改進也很重要。它是從根本上轉變金錢的本質,將金錢由被中介搬運的靜態價值存儲,轉化成可編程、可組合、有智能的介質,可以自動執行邏輯、響應條件、無需授權或延遲地在全球無縫運作。This is not a crypto story. This is a payments infrastructure story - one that happens to utilize blockchain technology because that technology solves problems traditional infrastructure could not address. The relevance extends to anyone working in finance, payments, treasury management, or commerce. The questions are no longer whether this convergence will occur, but how rapidly it will progress, which use cases will achieve mainstream adoption first, and which participants will lead versus lag the transition.

這唔係一個加密貨幣故事。呢個係一個支付基礎設施嘅故事——只不過啱啱用到區塊鏈技術,因為呢啲技術解決咗傳統基建解決唔到嘅問題。呢個議題同凡係做金融、支付、財資管理或者商業嘅人都息息相關。問題已經唔再係會唔會出現融合,而係融合嘅速度有幾快、邊啲應用場景最早成為主流、同埋邊啲參與者會帶頭轉型,邊啲會跟唔切。

PayFi is bridging payments and DeFi by unlocking the time-value of money trapped in traditional flows, enabling instant programmable settlement, and connecting the global economy in ways that were previously impossible. For the millions who depend on remittances, the businesses seeking working capital, the treasurers managing global operations, and the creators building sustainable income - PayFi is not abstract technology. It is infrastructure that makes financial services more accessible, efficient, and powerful.

PayFi 正喺連接支付同去中心化金融(DeFi),解放咗傳統資金流程中被困住嘅資金時間價值,實現即時、可編程嘅結算,仲以前所未有嘅方式連繫全球經濟。無論係要靠匯款維生嘅數百萬人、想搵營運資金嘅企業、管理全球業務嘅財務主管,定係建立可持續收入模式嘅創作者——PayFi 唔係咩虛無縹緲嘅技術。佢就係令金融服務更易接觸、更有效率、更有力嘅基礎設施。

The revolution is not coming. It is already here, building momentum, and reshaping the foundations of how value moves through the global economy. The only question that remains is how quickly the transformation will unfold - and who will be prepared to benefit from the change.

革命唔係即將發生,而係已經喺度發生,愈滾愈大,改寫緊價值流動喺全球經濟中嘅基本規則。剩返落嚟嘅問題,就只係轉變會有幾快發生——同埋邊啲人準備好從呢場轉變中得益。