當 Celestia 在2023年10月推出其TIA代幣時,市場樂觀情緒高漲。這個模組化區塊鏈專案獲得主要交易所支持、募得可觀風投資金,並自詡為Web3未來的基礎建設。到2024年9月,TIA一度接近20美元。但16個月後,價格跌到1.5美元以下,較高點下跌超過90%。

問題不是技術失敗,也不是市場操縱,而是更根本的缺失:糟糕的代幣經濟設計,導致供給暴增卻缺乏對應需求。2024年10月,一次性解鎖1.76億顆代幣,流通量一夜之間幾乎翻倍。早期資方趁機出貨,價格暴跌,社群信心瓦解。

Celestia這一路線說明一個尷尬而現實的道理,現已在2024-2025加密週期中逐漸明朗:代幣發行的成敗,早在首次交易之前就已註定。曾經被忽視的發幣前階段,如今成為區分永續經營與曇花一現專案的關鍵。

這一轉變也體現產業機構化的進程。2021年的牛市講究炒作與短線操作,而2024-2025的復甦則強調紀律。歐盟的加密資產市場法規(MiCA)自2024年12月全面生效,對發幣方和服務商設下嚴格合規門檻。機構投資人以私募基金標準審視代幣經濟,散戶則在經歷週期洗禮後更加重視透明度。

在這樣的大環境下,什麼使發幣專案區分出紀律與災難?本文將分析團隊在發幣前必做的重要步驟,從設計、流動性策略、合規、社群建構到技術就緒皆不可偏廢。風險升高,容錯空間愈發狹小。

打造能經得起市場考驗的基礎

代幣經濟不是單純的分配數學,而是一種經濟架構,決定代幣是否能在發行炒作後仍有實質價值。精心設計的代幣經濟能夠讓持有者動機與協議成長一致,預測性控管通膨,並創造長期參與的實際用途而非僅誘發短期拋售。

然而,許多團隊卻把代幣經濟當成事後補救,只為迎合創投需求而倒推供給排程,而不去建立可持續的需求機制。結果可想而知。Blast這個備受矚目的Layer2專案,2024年6月一次性解鎖105億顆代幣,佔總量一半以上。流動性不堪重負,即便首日交易量傲人,價格仍跌到歷史新低。

這種狀況在多個專案重演。例如Berachain大幅度解鎖導致價格腰斬;Omni Network剛上市一天內就因早期持有人出貨,價格暴跌超過50%。這並非個案,而是系統性設計失誤:團隊本末倒置,將募資高於經濟永續,產生龐大賣壓,無論行銷多好都補不回來。

有效的代幣經濟設計首先要誠實問:為什麼會有人長期持有?答案必須具體而可驗證。治理權幾無意義,若協議根本沒重大事務可決定;質押獎勵超過協議收入,只會變成無止盡通膨;聲稱實用但用戶量遠低於流通供給,那用途純屬空談。

Messari的研究強調,成功的專案將代幣發行與網路實際活動及真實需求連動,而非隨意排發計畫。NodeOps Network於2025年6月發行NODE代幣,在累積超過370萬美元收入後,將代幣銷毀直接與服務實際使用掛鈎,形成動態供給管理,避免預設通膨曲線帶來的風險。

Messari創辦人暨執行長Ryan Selkis在2024年報告中指出:「雖然過去一年依舊充滿挑戰,但開發者已經為加密產業的下一階段鋪路。」這觀點凸顯,健康的代幣經濟來自於紀律建構,而非投機炒作。

分配設計和供給機制同等重要。例如Arbitrum於2023年3月空投,分配11.5%總量給用戶、1.1%給生態DAOs,並將44%給投資人與團隊,皆明訂解鎖排程。如此設計兼顧社群治理並保留足夠庫存以資助長期發展。反觀部分專案大量分配(如超過60%)給內部人,缺乏鎖倉規則,直接導致發行首日拋壓。

資金解鎖排程則需特別注意。一刀切式的集中解鎖會引發可預期的賣壓,私募機構提前套利,散戶慘遭割韭菜。線性長期解鎖可分散拋壓,但仍需與市場造市策略配合。設計需呼應專案需求,反之如果解鎖讓流通量一夜翻倍,顯然忽視價格穩定或根本不在意。

代幣用途是長期需求的核心。例如Optimism的OP代幣在治理雙院DAO體系中具備實質決策權,能參與協議升級、專案激勵、公共資金分配等,提供持續購入與持有誘因。而那些鏈上活動稀少或治理極度中心化的項目,其治理代幣實際毫無價值,只剩下投機炒作。

最後,團隊在發幣前必須針對多種情境模擬供需動態。若實際交易量僅為預期一半?若質押參與率高於預期,通膨會不會失控?若大戶拋售,流動性能否支撐不讓價格暴跌?這些問題需量化分析而非過度樂觀假設。將代幣經濟當成創世神諭的專案最終必然發現,市場不會為精美白皮書買單。

健全的代幣經濟不是操控價格,而是透過真實經濟運作,創造持有動機,負責任地分配,將發行與實際需求掛鈎,並預期賣方行為。在日益專業的市場裡,僅僅達標就是決勝關鍵。

規範與合規準備

2024-2025年間,代幣發行的法規環境劇變,從各國各自為政逐步走向協調一致的框架,給發行團隊帶來重大合規壓力。把法規視為選項或拖延法律準備的團隊,越來越常遇到上線延誤、被查處,甚至直接被主要市場禁止。

歐盟加密資產市場法(MiCA)於2024年12月30日全面生效,首度對27國成員帶來橫跨全體的完整加密法規。MiCA界定三大類型加密資產:多資產擔保的「資產參照型代幣」、對標單一法幣的「電子貨幣型代幣」、以及其他包含用途型Token在內的加密資產。每類都需依規接受授權、資訊揭露和持續監理。

MiCA規定,代幣發行方須在歐盟境內公募或掛牌交易前,發佈詳細白皮書,內容需載明代幣特性、發行人資料、代幣權利、底層技術與相關風險。若資訊不充分或重大失實,發行方將面臨行政處分,甚至刑責。

加密資產服務提供者,包括交易所、錢包、託管機構,必須向國家主管機關申請營業執照,證明資本額、治理架構、風險管理及合規能力達標。只有歐盟本地公司得以發行資產參照與電子貨幣型代幣,而無資產擔保之演算法穩定幣則被排除於合法範疇。

MiCA的資金轉移新規同步實施,更進一步要求反洗錢,服務方需建立發送人與收款人個資交互機制,以確保透明並防堵非法資金流動。這些規定雖借鑒傳統銀行業標準,但針對本是去中心化架構而非監控設計的區塊鏈提出極高要求。

除歐盟外,全球其他地區監管力道亦同步升級。例如美國證券交易... continued its enforcement approach, treating many tokens as unregistered securities subject to federal securities laws. Ripple's ongoing legal battle with the SEC, which began in 2020 and saw mixed rulings through 2024, illustrates the risk of launching without clear regulatory positioning. The case has cost Ripple hundreds of millions in legal fees and created persistent uncertainty about XRP's status.

持續採用執法手段,將許多代幣視為未註冊證券,受到聯邦證券法律規範。瑞波(Ripple)自2020年起至2024年間,與美國證券交易委員會(SEC)持續進行的法律訴訟,伴隨著多次裁決結果不一,凸顯了在未明確定位監管合規性即發行的風險。這宗案件已讓瑞波付出了數億美元的法律費用,並使XRP的法律地位持續處於不確定狀態。

Asian jurisdictions pursued varied approaches. Singapore maintained relatively permissive rules for utility tokens while imposing strict requirements on tokens that function as securities or payment instruments. Hong Kong opened to retail crypto trading with licensing requirements. China maintained its blanket prohibition on token offerings. This fragmentation means projects cannot adopt a one-size-fits-all compliance strategy but must tailor their approach to target markets.

亞洲各司法轄區則採取了不同策略。新加坡對於功能型代幣(utility token)相對寬鬆,但對於具有證券或支付功能的代幣則設有嚴格要求。香港則透過發牌制度,對零售層面開放加密貨幣交易。中國則繼續全面禁止代幣發行。這種監管的分歧意味著專案無法採取「一體適用」的合規策略,必須針對目標市場訂定客製化方案。

Jurisdiction selection has become a critical strategic decision. Many projects incorporate in jurisdictions perceived as crypto-friendly: the British Virgin Islands, Cayman Islands, Singapore, or Switzerland. These locations offer established legal frameworks, favorable tax treatment, and reduced regulatory friction. However, incorporation location does not determine regulatory obligations in markets where tokens are sold or traded. A BVI-incorporated issuer selling tokens to EU residents must comply with MiCA regardless of where the entity is domiciled.

轄區選擇已成為關鍵的策略決策。許多專案選擇在被視為對加密友善的司法管轄區註冊公司,如英屬維京群島、開曼群島、新加坡或瑞士。這些地區提供成熟的法律架構、有利的稅務待遇及較低的監管摩擦。然而,註冊地並不決定發行人在代幣銷售或流通市場的監管責任。舉例來說,即使在英屬維京群島註冊的發行方,若銷售代幣給歐盟居民,亦需符合MiCA規範,與實際登記地無關。

Know-your-customer and anti-money laundering procedures now represent baseline requirements for any serious token launch. Major exchanges and launchpads require compliance audits before listing consideration. CoinList, a leading token sale platform, operates under U.S. money transmitter licenses and conducts extensive investor verification before allowing participation. This creates friction and excludes some retail participants, but it also provides legal defensibility and access to institutional capital that increasingly demands regulatory compliance.

了解你的客戶(KYC)以及反洗錢(AML)程序,現已成為任何嚴肅代幣發行的基本要求。主流交易所及發射平台皆要求在上架前進行合規審查。龍頭投資平台CoinList持有美國多州金流牌照,在允許投資人參與前會進行嚴格的投資人背景審查。這類流程雖然增加用戶摩擦,排除部分散戶參與,但也帶來合法抗辯力,同時可取得追求合規的機構資本青睞。

The classification question - utility versus security - remains central despite years of debate. The Howey Test, articulated by the U.S. Supreme Court in 1946, asks whether an investment contract exists based on whether someone invests money in a common enterprise with expectation of profit from others' efforts. Many token sales meet this definition during initial fundraising even if the token later evolves into pure utility. Projects that fail to address this distinction risk retrospective enforcement based on launch-phase activity.

儘管多年間討論不斷,「功能型」或「證券型」分類問題依舊是核心。美國最高法院於1946年提出的Howey 測試標準,檢視是否存在「投資契約」:即投資人是否投資資金於共同事業,並期盼由他人努力帶來收益。許多代幣發行案件在初始募資階段符合這一定義,即使其後代幣僅作為功能型產品。若專案未妥善處理分類區分,將面臨依照發行階段活動而追溯執法的風險。

Expert guidance from specialized law firms has become essential rather than optional. Firms like Coin Center, ConsenSys's legal team, and specialized blockchain practices at major law firms provide analysis of regulatory requirements, structure compliant offerings, and negotiate with regulators on novel issues. Legal costs for a well-structured token launch now routinely exceed $500,000, but this investment provides protection against enforcement actions that could cost multiples more.

專業律所的指導已成必須,而非選項。譬如Coin Center、ConsenSys法務團隊及多家國際律師事務所的區塊鏈專責部門,常協助解讀監管要求、設計合規產品及協調創新議題的監管溝通。規劃完善的代幣募資法務成本常高達50萬美元以上,但這筆投入能顯著降低未來面臨執法行動時的損失。

The compliance burden creates natural barriers to entry that favor well-capitalized projects with professional teams. This professionalization benefits the ecosystem by reducing scams and low-effort launches, but it also raises concerns about centralization and regulatory capture. Teams must balance legal defensibility against decentralization principles, recognizing that perfect decentralization may be legally infeasible in practice.

合規負擔自然形成進入門檻,有利於資本充裕、團隊專業的項目。專業化提升整體生態品質,可降低詐騙及草率項目,但同時也引發中央化與監管綁架的疑慮。團隊須在合規抗辯力與去中心化理念間取得平衡,認知到純粹去中心化在現實中可能無法完全實現。

Looking forward, regulatory frameworks will continue converging globally, creating clearer rules but also more extensive obligations. Projects that treat compliance as core infrastructure rather than unwelcome overhead will navigate this environment successfully. Those that attempt regulatory arbitrage or ignore legal requirements entirely will face escalating consequences as enforcement capabilities mature.

展望未來,全球監管架構將持續趨於一致化,規則將更為明確,但義務也將更加冗長嚴格。將合規視為核心基礎建設,而非額外包袱的專案,將能更順利在新環境中運作。反之,試圖透過監管套利或完全漠視法律要求者,將隨著執法演進而面臨加劇後果。

As Alexander Ray, CEO and co-founder of Albus Protocol, emphasized in his compliance analysis: "Launching a token involves numerous regulatory considerations, from understanding how tokens are classified to ensuring proper KYC/AML compliance. By following this checklist and seeking legal advice where necessary, projects can navigate the complex regulatory landscape and launch their tokens with confidence."

正如Albus Protocol的執行長兼共同創辦人Alexander Ray在其合規分析中強調: 「發行代幣涉及大量監管考量,從釐清代幣分類到完善的KYC/AML流程。遵循檢查清單並在必要時尋求法律意見,有助於團隊順利穿越複雜的監管格局,自信發行代幣。」

Launchpads: Visibility vs. Vulnerability

發射平台:曝光度與風險間的取捨

Launchpads emerged as critical infrastructure for token distribution, offering projects access to engaged crypto communities, built-in liquidity, and credibility through association with established platforms. Yet launchpad selection involves complex trade-offs between visibility, cost, control, and risk that teams often underestimate until contracts are signed and launch mechanics are immutable.

發射平台已成為代幣發行關鍵基礎設施,為專案帶來活躍的加密社群、預設流動性及與知名平台掛鉤所帶來的公信力。然而,不同平台間在曝光度、成本、主控權與風險間的取捨極為複雜,常被團隊低估,直到合約簽訂、流程定案後才難以回頭。

Binance Launchpad, the category leader, provides unmatched exposure to the world's largest exchange user base. Since 2019, it has facilitated more than 100 token launches raising over $200 million in combined funding, with six million all-time unique participants. Projects like Axie Infinity, Polygon, and The Sandbox achieved breakout success following Binance listings, benefiting from immediate liquidity across multiple trading pairs and sustained marketing support.

Binance Launchpad作為產業領頭羊,能直接接觸全球最大交易所的龐大用戶群。自2019年以來,該平台協助超過一百次代幣發行,合計募資超過兩億美元,累積參與人數達六百萬。像Axie Infinity、Polygon及The Sandbox等知名專案,皆在上幣後一舉成名,受益於多元交易對的即時流動性及持續的市場行銷力道。

But Binance's dominance comes with stringent requirements. The vetting process is notoriously selective, with acceptance rates below five percent. Binance charges competitive fees - typically one percent of total raise - but maintains significant control over launch timing, token allocation, and post-launch liquidity management. Geographic restrictions prevent participants from certain jurisdictions, including parts of the EU, from accessing offerings. For projects that make the cut, Binance Launchpad represents the gold standard. For the vast majority, it remains aspirational.

但Binance的領先同時伴隨高門檻。審查流程極為嚴格,通過率低於5%。啟動費用相對競爭力,通常為募資總額的1%,但Binance掌握發行時機、代幣配置及後續流動性管理的決定權。部分地區(包括部分歐盟)用戶受限於地理封鎖,無法參與。能進入Binance Launchpad的項目堪稱業界金標準,但對絕大多數團隊而言仍屬遙不可及。

CoinList positions itself as the compliance-focused alternative for established projects with institutional ambitions. Founded in 2017, CoinList operates under U.S. money transmitter licenses and has hosted launches for Algorand, Solana, Filecoin, and other major protocols. The platform provides investor verification, cap table management, vesting administration, and advanced token economics controls - services that appeal to projects navigating complex regulatory requirements.

CoinList則定位為合規導向、深受機構認可的代幣發行替代方案。自2017年成立,持有美國金流牌照,已協助Algorand、Solana、Filecoin等多個主流專案發行。該平台提供投資人實名審核、權益表管理、解鎖期安排,以及精細的代幣經濟學管理工具,吸引需應對複雜監管需求的團隊。

CoinList's strength is also its constraint. The extensive KYC process creates friction and excludes participants from restricted jurisdictions. Token allocations follow a karma-based point system that rewards platform activity, meaning even approved participants face no guarantee of receiving desired allocation. For projects willing to accept these trade-offs in exchange for regulatory defensibility and access to institutional capital, CoinList offers unmatched infrastructure. For projects prioritizing broad retail distribution or rapid launch velocity, the process may feel bureaucratic.

CoinList的優勢同時也是限制。繁瑣的KYC程序增加參與門檻,並排除特定地區用戶。代幣分配依循「業力點數」制度,獎勵活躍平台行為,即使通過審核者也不保證能獲期望名額。若團隊願意以監管抗辯力與機構資本渠道換取上述限制,CoinList堪稱無可匹敵。但倘若重視廣泛散戶分布或追求快速上市,則可能覺得流程官僚繁瑣。

DAO Maker pioneered the Strong Holder Offering mechanism, designed to give retail investors access to early-stage opportunities previously reserved for venture capital. The platform has facilitated more than 130 initial DEX offerings raising over $72 million, with projects including Orion Protocol, My Neighbor Alice, and Sweat Economy. DAO Maker's social mining approach rewards community participation in project development, theoretically aligning incentives between investors and founders.

DAO Maker首創Strong Holder Offering機制,讓過去僅屬於創投機構的早期機會開放給散戶參與。平台已孵化超過130場初始DEX發售,總募資超過7200萬美元,包括Orion Protocol、My Neighbor Alice與Sweat Economy等知名專案。DAO Maker透過「社群挖礦」獎勵專案社群參與,理論上促進投資人與創辦人利益一致。

The tiered system requires participants to stake DAO tokens to access allocations, with higher tiers receiving guaranteed slots while lower tiers enter lottery systems. This creates economic moat around the platform but also concentrates benefits among large token holders. Critics argue the model replicates venture capital dynamics it claims to disrupt, simply substituting DAO staking for institutional connections. Supporters counter that transparent, blockchain-based allocation beats opaque venture processes.

該平台採分級質押制,須質押DAO代幣方能參與申購,高等級者保證配額,低等級者進入抽籤。此機制築起經濟護城河,同時也將利益集中於大額持幣者。批評者認為,這種分配本質上只是將傳統創投關係轉換為DAO質押,實際未打破舊有壁壘;支持者則認為,鏈上公開透明的分配優於傳統創投「黑箱」。

For blockchain gaming and NFT projects, Seedify has established dominance through specialized infrastructure including Initial Game Offerings, playtesting support, and customizable sale structures. More than 75 launches have used the platform, with tiered staking systems similar to DAO Maker's approach. The gaming focus provides valuable network effects as projects gain exposure to communities specifically interested in blockchain games rather than generic crypto investors.

在區塊鏈遊戲及NFT領域,Seedify以專業基礎設施(如初始遊戲發射、遊戲測試支援及彈性銷售結構)建立主導地位,累積超過75場專案發射。其分級質押設計亦與DAO Maker相似。遊戲垂直聚焦帶來強大網絡效應,有助專案迅速獲得真正對鏈遊感興趣的社群支持,而非單純尋求加密投機的泛用戶。

Fjord Foundry and Polkastarter represent the decentralized launchpad category, using liquidity bootstrapping pools and algorithmic pricing rather than fixed-price sales. These mechanisms allow market forces to determine token valuation rather than relying on team-set prices that often overshoot or undershoot fair value. The model reduces price volatility post-launch by distributing tokens more efficiently based on genuine demand curves. However, it also introduces complexity and requires sophisticated understanding of bonding curve mechanics.

Fjord Foundry與Polkastarter則屬去中心化發射平台代表,利用流動性啟動池(LBP)、演算法定價等機制,讓市場動態自然調節代幣價格,而非僅由團隊設定固定售價(常導致高估或低估)。此模式能依真實需求曲線有效分配代幣,降低上市初期價格劇烈波動。然而,其設計較為複雜,需深入理解彎道曲線、流動池等原理。

The performance metrics tell sobering stories. DAO Maker remains the only major launchpad showcasing positive average return on investment across all historical token sales, according to comprehensive platform analysis. Most others, including well-regarded options like TrustSwap and BSCPad, show negative current average ROI when measured from launch prices to subsequent trading. This reflects both general market conditions and the challenge of launching tokens at valuations that leave room for appreciation.

平台績效數據令人省思。依據統計,截至目前DAO Maker是唯一所有歷史發售案平均投資報酬為正的大型平台。包括TrustSwap、BSCPad等知名平台則多數發行案平均ROI呈現負值,反映大盤環境低迷及代幣發售評價過高、缺乏後續漲幅空間的現實。

Launchpad contracts contain crucial clauses that teams often overlook during negotiation. Performance-based refund mechanisms allow investors to recover funds if projects fail to meet specified milestones - engagement targets, development deadlines, or liquidity thresholds. While investor-friendly, these provisions create

發射平台合約中的權益條款常被團隊在洽談時忽略。例如依表現退費條款,若專案未達成預定目標(如社群互動、開發進度或流動性門檻),投資人可申請退款。這種條款雖對投資人友好,卻也帶來...ticking time bombs for teams that underestimate implementation complexity or encounter unexpected delays. A single missed milestone can trigger mass refunds that crater the project before it properly launches.

對於低估執行複雜性或遇到意外延誤的團隊來說,這些就像未爆彈。一旦有任何一個重要里程碑未達標,就可能引發大規模退款,讓項目還沒正式啟動就已經崩盤。

Fee structures extend beyond upfront costs to include ongoing obligations. Some platforms take ongoing percentages of token supply, require listing on specific exchanges, or impose minimum liquidity commitments that drain treasuries. Teams should model total launch costs including these contingent obligations, not just headline numbers.

費用結構不僅止於前期成本,還包括後續持續性的義務。有些平台會持續抽取代幣供應量的一定比例,要求在特定交易所上市,或施加最低流動性義務,造成資金庫的大量消耗。團隊應該將這些附帶性義務納入總啟動成本的模型,而不是只看表面數字。

Due diligence on launchpad reputation has become essential. Past project success rates, token retention periods, community quality, and founder testimonials provide insight into whether a platform delivers genuine value beyond token distribution mechanics. Platforms with histories of failed projects or communities dominated by short-term speculators offer questionable value regardless of headline participation numbers.

對 Launchpad 平台聲譽的盡職調查已經變得必不可少。過去項目的成功率、代幣鎖倉時長、社群質量以及創辦人證言,都能判斷該平台是否真的能提供超越代幣分發機制的價值。擁有失敗項目紀錄或由短線投機者主導社群的平台,不論表面參與數多高,其實際價值都值得懷疑。

The optimal launchpad strategy depends on project specifics. High-quality infrastructure projects with strong fundamentals benefit from tier-one platforms like Binance or CoinList despite higher barriers. Gaming and NFT projects find specialized value in Seedify. Experimental DeFi protocols may prefer decentralized options that attract more sophisticated, risk-tolerant participants. Regional projects should prioritize platforms strong in target markets rather than chasing global reach.

最佳的 Launchpad 策略須依專案特性而定。基礎體質強、質量高的基礎建設專案,即使門檻較高,仍適合選擇 Binance 或 CoinList 等一級平台。遊戲及 NFT 專案則能從 Seedify 獲得專屬價值。實驗性 DeFi 協議則可能更偏好能吸引高風險承受度及更複雜參與者的去中心化選項。區域型專案則應優先選擇在目標市場強勢的平台,而非盲目追求全球曝光。

Some projects eschew launchpads entirely, conducting direct community sales or liquidity bootstrapping on decentralized exchanges. This approach maximizes control and minimizes fees but sacrifices the built-in distribution and credibility that established platforms provide. The calculus depends on whether the project has sufficient organic community to ensure successful distribution without platform support.

部分專案則完全不依賴 Launchpad,選擇由團隊直接進行社群銷售或在去中心化交易所進行流動性啟動。這種做法最大化專案方的主控權並降低費用,但同時失去了平台內建的分發及信譽加持。關鍵在於專案本身是否有足夠的原生社群,能不靠平台仍然順利分發。

Launchpads should be evaluated as partners, not just distribution channels. The best platforms provide strategic guidance, connect projects with market makers and exchanges, offer post-launch support, and maintain engaged communities beyond the initial sale. The worst extract maximum fees while providing minimal value beyond basic token distribution infrastructure.

衡量 Launchpad 時,應視其為夥伴關係,而非單純的分發渠道。最好的平台能提供策略建議、協助專案方與造市商及交易所接洽、提供後續支持,並維護活躍的社群關係。最差的平台則只抽取高額費用,卻只提供基礎分發基礎設施,價值有限。

Teams should negotiate aggressively and compare multiple platforms before committing. The excitement of launchpad acceptance should not prevent careful contract review and scenario modeling. What happens if crypto markets crash during the launch window? If engagement metrics fall short? If development timelines slip? Clear answers to these questions should exist before signing, not after problems emerge.

團隊應積極談判並多方比較平台,審慎決定前不可草率承諾。獲選 Launchpad 的興奮不應掩蓋合約細節及各種情境的審慎推演。如果發生上市窗口期間加密市場大跌怎麼辦?如果參與度指標不如預期?開發進度延遲怎辦?這些問題都應該在簽約前就有明確答案,而不是等出現問題才補救。

Exchange Listings: Smart Sequencing and Cost Management

Exchange listings represent crucial milestones that provide liquidity, visibility, and trading infrastructure. Yet the listing process involves substantial costs, complex negotiations, and strategic decisions that significantly impact token performance. Teams that chase tier-one exchanges without clear strategy often drain treasuries while securing listings that deliver minimal incremental value.

交易所上市是一項關鍵里程碑,能為專案帶來流動性、能見度及交易基礎設施。然而,上市過程涉及大量成本、複雜談判及重大的策略抉擇,對代幣表現產生深遠影響。沒有明確策略地盲目追求一級交易所上市,常見結果是耗盡資金庫,所換來的上市卻幾乎無助於專案價值成長。

Binance, Coinbase, and OKX dominate trading volume among centralized exchanges, collectively accounting for the majority of spot and derivatives activity. A Binance listing provides instant exposure to millions of users, deep liquidity across multiple trading pairs, and powerful signaling that institutional investors and other exchanges monitor closely. But Binance selectivity means most projects have no realistic path to listing, and even those that succeed pay substantial fees - often multi-million dollar ranges including listing costs, liquidity commitments, and marketing packages.

Binance、Coinbase、OKX 等是中心化交易所中交易量的主導者,合計佔據現貨及衍生品大多數交易活動。在 Binance 上市能立刻獲得數百萬用戶曝光、多交易對的深厚流動性,並發出強烈訊號吸引機構投資人及其他交易所的高度關注。但 Binance 的篩選極嚴,絕大多數專案根本沒有實際上市機會。即便成功獲准,費用也非常可觀──往往高達數百萬美元,包括上市費、流動性承諾及行銷配套等。

Coinbase emphasizes regulatory compliance and focuses on assets likely to satisfy U.S. securities law requirements. The exchange maintains stricter listing criteria than most competitors, resulting in a more curated but smaller asset universe. For projects with strong legal positioning and U.S. market focus, Coinbase provides premium access to institutional capital and retail traders in the world's largest economy. For projects with regulatory ambiguity or international orientation, other options may better serve needs.

Coinbase 強調法規合規,專注於符合美國證券法標準的資產。其上市標準比其他交易所更為嚴格,資產池較小但較有企圖心。對於法律基礎穩健且主攻美國市場的專案,Coinbase 是接觸全球最大經濟體機構及散戶資金的絕佳管道。對於法規不明確或聚焦國際市場的專案,其他選擇則可能更合適。

Regional and second-tier exchanges - MEXC, Bitget, Gate.io, Bybit - offer more accessible listing pathways with lower fees and fewer requirements. These platforms provide genuine liquidity in specific geographic markets or for certain asset classes. However, they also carry risks including fake volume through wash trading, limited user bases outside core markets, and less rigorous due diligence that may associate projects with lower-quality listings.

區域型及二線交易所如 MEXC、Bitget、Gate.io、Bybit,提供更易於進入的上市門檻、較低費用及較少的要求。這些平台在特定地區或特定類別資產具有真正流動性。但同時也有風險,包括透過洗盤偽造的虛假交易量、在核心市場外用戶規模有限,及盡職調查標準較低導致與低品質項目混淆的可能。

The sequencing question looms large. Should projects pursue tier-one listings immediately or build liquidity on smaller exchanges first? The answer depends on project maturity and resource availability. Launching directly on Binance creates maximum impact but requires substantial preparation and capital. Sequencing through progressively larger exchanges allows teams to refine tokenomics, build community, and demonstrate traction before approaching top-tier platforms. Neither approach is universally superior.

上市排序的問題至關重要。專案應該直接追求一線交易所,還是先在小型交易所建立流動性?答案取決於專案成熟度及資源狀態。直接在 Binance 上市效益最大,但需極高準備度與資本。採漸進式上市則讓團隊有時間優化經濟模型、培養社群、展現成績後再進軍一線平台。兩種做法沒有絕對優劣,必須因應專案實際情況調整。

Liquidity distribution across exchanges matters as much as which exchanges list the token. Concentrating liquidity on a single platform creates fragility - if that exchange experiences technical issues, regulatory problems, or reputational damage, the token's entire trading infrastructure collapses. Distributing liquidity across multiple exchanges and both centralized and decentralized venues provides resilience but requires more sophisticated market making and inventory management.

流動性分布於各交易所與上市平台數量同等重要。將流動性集中於單一平台會造成脆弱性──如果該平台遭遇技術問題、法規挑戰或聲譽損害,該代幣的整體交易支持就會土崩瓦解。將流動性分散於多平台(含中心化及去中心化渠道)則較具韌性,但同時對造市與存貨管理提出更高要求。

Exchange negotiations involve more than listing fees. Teams must commit to providing liquidity, often through dedicated market-making arrangements or direct capital deposits. Some exchanges demand ongoing marketing activities, exclusive first listing windows, or equity stakes in the project. Understanding total obligations and evaluating whether they align with project goals requires careful analysis beyond headline listing costs.

交易所的談判不僅僅是上市費用。團隊經常還必須承諾流動性供給,透過專屬造市協議或直接注資。有些交易所還要求進行不斷行銷推廣、獨家首發上市窗口,甚至參與公司股權。明確了解所有義務並評估其是否符合項目目標,須超越表面上市費的精密分析。

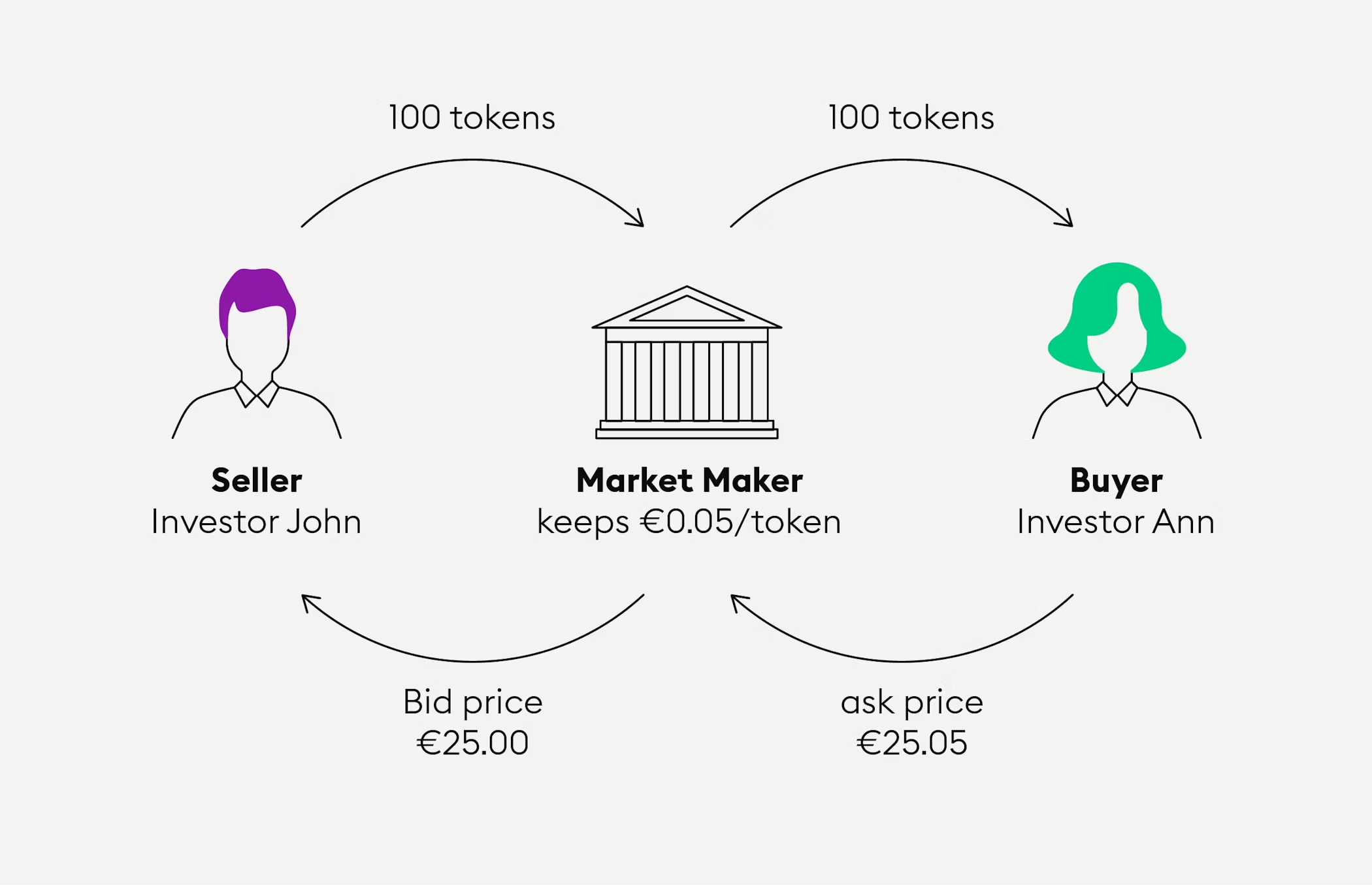

The wash trading problem deserves mention. Some exchanges inflate reported volumes through fake activity - either internally or through arrangements with affiliated market makers. Reported $10 million daily volume may represent $1 million genuine trading and $9 million circular wash trades. This misleads projects about actual liquidity and creates false impressions of market interest. Teams should evaluate real order book depth, executed trade sizes, and bid-ask spreads rather than headline volume when assessing exchanges.

洗盤造假交易問題值得特別留意。有些交易所會內部操作或與關聯造市商合作,虛增日報交易量。例如,標榜 1,000 萬美元日交易量,可能只有 100 萬實際成交,其餘 900 萬皆為人為對敲循環單。這會誤導項目對於實際流動性的判斷,並造成市場熱度的假象。評估交易所時,應關注實際訂單簿深度、單筆成交量及買賣價差,而非僅依總成交額。

Celestia's listing strategy illustrates sophisticated multi-exchange coordination. The project secured day-one listings on Binance and Coinbase, providing immediate liquidity in major markets. Simultaneous listings on multiple tier-two exchanges ensured geographic coverage and prevented arbitrage opportunities that often emerge when listings are staggered. While tokenomics problems ultimately undermined price performance, the exchange strategy itself executed well.

Celestia 的上市策略體現了高階多交易所協調。專案於首日即同步在 Binance 與 Coinbase 上市,立刻涵蓋主要市場流動性,同時也在多家二線交易所同步首發,確保區域覆蓋並防範因分批上市而導致的套利機會。雖然最終因代幣經濟問題而影響價格,但其上市策略本身執行得當。

Sui and Wormhole adopted similar approaches, launching across multiple exchanges simultaneously to maximize liquidity and prevent fragmented markets. This strategy requires extensive preparation and coordination but delivers cleaner launches with less price volatility during the critical initial trading period.

Sui 與 Wormhole 也採取類似策略,在多家交易所同步上市,以放大流動性並避免市場碎片化。這需要大量準備及協同,但能帶來更順暢、波動較低的啟動期。

Some projects take the opposite approach, initially listing exclusively on decentralized exchanges to maintain decentralization principles and minimize corporate entanglements. Uniswap, SushiSwap, and other DEXs provide permissionless listing pathways that bypass centralized gatekeepers. However, DEX liquidity typically starts thin and requires significant incentivization to attract liquidity providers. The trade-off between decentralization ideals and practical liquidity concerns has no easy resolution.

亦有部分專案則反其道而行,首發僅選擇去中心化交易所,以維持去中心化原則並盡量避免公司資本介入。Uniswap、SushiSwap 及其他 DEX 提供無須審核的上市管道,能跳過中心化守門者。然而,DEX 初期流動性普遍不足,需要大量誘因才能吸引流動性供應者。理想的去中心化與現實的流動性需求之間,並無簡單答案。

Teams should model exchange costs across the full listing lifecycle, not just initial fees. Ongoing market-making expenses, liquidity maintenance, potential delisting risks, and opportunity costs of capital locked in exchange wallets all factor into total cost. A tier-one exchange charging $2 million for listing but providing $50 million daily volume may deliver better value than a tier-two exchange charging $200,000 with $2 million daily volume, depending on project needs.

團隊應從整個上市週期評估總成本,而非只考量初始費用。持續造市費、流動性維護、潛在下市風險,以及資本鎖定於錢包的機會成本,皆須納入總體預算。對部分專案而言,一級交易所雖然上市費高達 200 萬美元,但若能帶來 5,000 萬日交易量,相較於二線交易所 20 萬美元上市費但僅 200 萬日交易量,其實仍可能更具性價比。

The maxim bears repeating: listing is a tool, not validation. The exchange announcement creates a one-time price impact that quickly dissipates if underlying fundamentals are weak. Sustainable value accrues from protocol usage, revenue generation, and community growth - factors that listings facilitate but cannot substitute. Teams that understand this distinction allocate resources appropriately rather than treating exchange listings as the ultimate success metric.

應再次強調:上市只是工具,不是認證。交易所公布上市常會帶來一次性價格波動,但若專案體質不足,這股行情也會很快消散。真正持久的價值取決於協議使用度、營收成長及社群壯大──上市能輔助,但不能取代。懂得這一點的團隊會適當分配資源,而不會將上市視為唯一成功指標。

Market Makers: Stability, Not Spectacle

Market makers provide the liquidity infrastructure that enables trading by continuously offering to buy and sell tokens at publicly quoted prices. High-quality market making tightens bid-ask spreads, reduces price volatility, absorbs large orders without catastrophic slippage, and creates the appearance of genuine trading interest that attracts additional participants. Poor market making amplifies volatility, creates the appearance of manipulation through artificial volume, and ultimately destroys trust.

造市商是交易市場流動性的基礎,其工作是持續以公開報價買賣代幣,提供流動性。高品質的造市能縮小買賣差價、降低價格波動、吞吐大額訂單不產生極端滑價,並營造出真正的市場活躍度,進而吸引更多參與者。反之,劣質的造市往往帶來劇烈波動,藉由人為交易量營造操控假象,最終損害市場信任。

The distinction between legitimate and predatory market making has become increasingly important as the industry professionalized through 2024 and 2025. Reputable firms like Wintermute, GSR, and Flowdesk operate with transparency, provide genuine two-sided liquidity, and align incentives with project success over multi-year timeframes. Predatory

隨著行業在 2024-2025 年加速專業化,合法與掠奪性造市的區別變得越來越重要。Wintermute、GSR、Flowdesk 等知名公司以透明原則運作,真正提供雙邊流動性,並在多年時程上將自身激勵與專案成功綁定。而掠奪性...Here is the translation according to your instructions (skipping translation for markdown links):

業者產生虛假交易量,進行搶先交易或其他操縱策略,並將短期套利置於長期價值創造之上。

市場狀況對於發行時機有重大影響。巴黎市市場做市商 Flowdesk 的執行長 Guilhem Chaumont 在 FTX 崩盤後觀察到:「FTX 事件後,我們發現主要幣種的流動性萎縮多達 50%。小市值項目的流動性下降甚至更加嚴重。」Chaumont 當時建議項目將發行延期三到六個月,直到流動性條件改善。

Wintermute 代表市場做市資深業者,其終身交易量逾 6,000 億美元,並已整合超過 50 家中心化和去中心化交易所。該公司在如 Coinbase、Kraken、Uniswap 和 dYdX 等主要平台上持倉,同時提供中心化及鏈上流動性。專有演算法讓 Wintermute 能在波動劇烈時維持高效率市場,而在此情況下,低階做市商則會撤出。該公司的可靠性和規模,使其成為大型項目的預設合作夥伴,雖然其收費標準也反映此定位。

GSR 總部設於倫敦,業務遍及全球,擁有十年經驗並接入 60 多家交易所。該公司強調透明度,每日報告為客戶提供包括訂單簿深度、滑點率和交易量在內的詳細 KPI 指標。此開放做法確保項目團隊了解市場狀況,並能評估做市安排是否達成預期效果。GSR 著重在公平價格發現與窄價差,而非一味追求交易量,並將真實流動性置於表面數字之上。

Flowdesk 專注於新興數位資產,並運用技術協助新專案迅速擴展。該公司規模相較產業巨頭更小,因此能靈活調整策略以因應不同客戶需求及市場變化。對於沒有龐大預算但有專業做市需求的項目來說,Flowdesk 可作為高階公司與低價但風險較高業者之間的理想選擇。

Cumberland 是傳統金融巨頭 DRW Trading 旗下部門,自2014年進入加密領域,提供機構級做市服務,特別著重於大宗交易與場外交易。該公司專為對沖基金、交易所與有大量交易需求但又不想引起市場波動的項目而設。Cumberland 的傳統金融背景帶來成熟風險管理及營運紀律,這是純加密原生公司有時所缺乏的。

做市合約多包含數個要素。公司會獲得用以部署在交易所的代幣庫存,藉此建立可雙向報價的資本基礎。合約目標會明確訂出最低價差、最大訂單回應時間及運作時數。收費則包含固定月費、依交易量或價格穩定度浮動的結構。有些合約包含期權型報酬,做市商能以折價購入代幣,既將利益對齊價格升值,也有可能導致做市方為追求期權價值犧牲客戶利益而產生利益衝突。

應注意的紅旗包括:保證回報、利潤分成或極低的費用。正規做市涉及資本風險與營運成本,因此需合理報酬。若有業者承諾不切實際低費用下也能保證成果,要不是打算造假交易量、操縱幣價,就是缺乏實力。團隊應對過度美好的承諾保持懷疑,應選擇有紀錄、可查驗客戶推薦及提供清楚價值創造流程之公司。

庫存管理問題值得細心規劃。團隊應向做市商提供多少代幣庫存?給太少會限制流動性,給太多若公司管理失誤或遭駭則風險極高。大多數安排都有獨立帳戶設計、明確風險限額及每日對賬。團隊絕不應給予做市商無限制動用庫存權限,也應拒絕不透明的資產運用報表。

去中心化交易所之做市有其特別考量。DEX 流動性池需直接將代幣存入智慧合約,只有提出才可領回。無常損失──即資產價格偏離初始比例時的機會成本──會影響報酬,必須透過再平衡策略來管理。有些項目會自行管理 DEX 流動性而非委外做市,以保持直接主控權,但這需要高度技術專業和持續關注。

做市商與交易所上架的關係也值得一提。有些交易所會要求項目必須聘用特定做市商或達到最低流動性標準後,才會批准上架。提前了解這些要求可避免上架談判時產生意外。此外,協調多家交易所的做市部署也能保持流動性穩定,避免出現套利機會,造成代幣價格不必要的波動。

整合進度很重要。專業做市商需數週時間來接洽新客戶、分析代幣經濟、部署基礎建設並開始交易。團隊應在發行前數月就啟動做市洽談,而不是發行前幾週才來規劃。臨時安排效果往往不佳,還可能被迫接受不利條款或次級合作夥伴。

發行後的表現監控極為關鍵,但經常被忽略。團隊應定期審查報告,確認是否如承諾交付指標,並於表現偏離預期時主動溝通。最佳合作是雙方持續交換市場情報,並依市況共同調整策略。最糟的是雙方置之不管,導致結果無人問責。

做市應視為長期合作夥伴關係,而非短期交易。真正重視項目成功的公司會提供策略建議,不僅止於流動性服務,還能協助引薦交易所及投資人,且能持續參與不同市場週期。僅以快速套利為目的業者則只會在市況良好時進場撈一筆,一旦市場轉壞則立刻消失。這些差別只有長期合作下才會浮現出來,因此一開始選對夥伴極為關鍵。

社群與溝通:先建立信仰,再追價格

社群凝聚力比大多數其他因素更能預測發行後之韌性。擁有積極參與、知識豐富且誠心相信協議使命的社群,能跨過代幣經濟設計失誤、熊市與市場競爭等難關。那些僅靠空投投機吸引的傭兵型社群,一旦獎勵結束流失得也最快。

建立真實用戶社群需及早啟動 ── 最理想是在代幣設計定稿前動手。這點乍看違反直覺,當團隊正專注於技術開發時,卻要同步納入社群意見,但代幣經濟設計階段的社群參與會創造長期的心理認同,這種歸屬感會持續到發行之後。參與意見回饋者與只是匿名接收空投的人,行為模式完全不同。

2024-2025 年流行的「分數農耕」玩法展現了遊戲化參與的力量與風險。Blast、LayerZero、Kamino 等項目都設計了分數機制,在代幣生成活動前就回饋鏈上活躍度。此舉的確成功吸引了用戶,並推升協議數據成長。但結果也吸引了無數純投機資本,分數兌換成代幣後隨即離場。挑戰在於如何區分信仰用戶與農夫。

有效的分數計畫應精細設計,誘因著重於反映長期承諾的行為,而非短期套利。以連續數月的活躍度而非單週交易量來計分,有助於篩選具耐心的參與者。要求空投後仍要持續活躍才能領取全額配發,可塑造持續參與動機。對於一收到分數或代幣就立刻轉帳者施加扣分,能降低純套利吸引力。雖然沒有一種機制能完美區隔信仰者與套利者,但這些設計有助提高認真用戶的比例。

教育內容比炒作更能建設社群。詳盡說明協議原理、代幣經濟動機、治理流程與路線圖的文件,能吸引真正瞭解自己在持有什麼及為何持有的支持者。淺薄的行銷手法若只是炒作幣價、吹捧「登月」前景,只會聚集一群下跌時一哄而散的投機者。雖然優質教學內容製作成本高,但最終社群質量將有天壤之別。

大使計畫可將社群動員規模擴大到團隊力有未逮的程度。有效的大使計畫會招募積極社群成員,給予其資源及訓練,對具體貢獻給予獎勵,並設計明確晉升路徑。劣質計畫則只是付錢請人社交媒體刷評論,根本沒有產生實際價值。評斷關鍵在於大使是真心認同項目,還是只是利用粉絲群炒短線。

AMA(即問即答)能促進團隊與社群直接對話。當 AMA 做得好時,可展現透明度、主動回應疑慮,還能建立人際連結between founders and supporters. When done poorly, they become echo chambers where softball questions receive marketing responses while difficult questions go unasked or unanswered. Teams should welcome challenging questions and provide honest, thoughtful responses even when answers are "we don't know yet" or "we made mistakes and here's how we're fixing them."

在創辦人與支持者之間。若執行不當,這些空間會變成回音室,只剩下輕鬆問題獲得行銷式回應,而困難問題要嘛沒人問,要嘛沒人答。團隊應該歡迎具有挑戰性的問題,即使答案是「我們還不知道」或「我們犯了錯,現在積極改進」,也要給予坦率且深思熟慮的回應。

Discord and Telegram channels require active moderation to prevent scams, manage FUD (fear, uncertainty, doubt), and maintain productive conversations. Understaffed channels become spam-filled wastelands. Over-moderated channels suppress legitimate criticism and create cultish environments where only cheerleading is tolerated. The balance requires clear community guidelines, consistent enforcement, and moderators empowered to use judgment rather than following rigid rules.

Discord 與 Telegram 頻道需要積極管理,以防止詐騙、控管 FUD(恐懼、不確定、懷疑),並維持有建設性的討論。人手不足的頻道很快淪為洗版的荒地;管理過度則壓抑合理批評,營造成只能鼓掌叫好的教派氛圍。拿捏平衡需要明確的社群規範、一致的執行,以及讓管理員有權運用判斷力,而非墨守成規。

Twitter/X remains dominant for crypto communication despite platform chaos and changing ownership. Projects need consistent voice, regular updates, and engagement with both supporters and critics. The temptation to respond defensively to criticism or ignore negative feedback should be resisted. Public acknowledgment of problems and clear communication about remediation builds more trust than pretending everything is perfect.

即使平台混亂、所有權頻繁更迭,Twitter/X 仍是加密圈溝通的主戰場。專案團隊必須維持一致語調,定期更新,積極與支持者及批評者對話。遇到批評時,不宜本能性地辯解或乾脆視而不見。坦承問題、清楚溝通解決方案,遠比假裝一切完美更能贏得信任。

Nansen, CoinGecko, and LunarCrush provide analytics on community health indicators. On-chain metrics like holder distribution, transaction patterns, and wallet behaviors reveal whether community is concentrated among few large holders or widely distributed. Social metrics including sentiment analysis, engagement rates, and follower growth distinguish authentic communities from bot-inflated numbers. Projects should monitor these indicators and use them to guide community strategy rather than treating community building as unmeasurable art.

Nansen、CoinGecko 及 LunarCrush 提供社群健康指標分析。鏈上數據如持幣分布、交易模式、錢包行為,可判斷社群是集中於少數大戶還是分布廣大。社群指標如情感分析、互動率、追蹤者成長,也能區分真實社群與機器人灌水。項目方應關注這些數據,據以調整社群策略,而不是把社群經營當成無法衡量的藝術。

Arbitrum exemplifies sustainable community building. The project spent years developing technology and engaging developers before token launch. The March 2023 airdrop rewarded actual protocol usage over nine months across multiple criteria, filtering for genuine users. Post-launch governance actively involves community in protocol decisions. The result is a community that remained engaged through bear market conditions because members identified with the protocol rather than just the token.

Arbitrum 是永續社群經營的典範。項目方在發幣前投入多年深耕技術、凝聚開發者。2023年3月空投是根據九個月協議實際使用狀況與多項指標遴選真用戶。上線後的治理也積極讓社群參與協議決策。因此,即使在熊市,社群成員仍持續投入,因為他們認同的是協議本身,不單是代幣。

Contrast this with countless projects that launched with massive social media followings, conducted hyped airdrops, then watched communities evaporate as token prices declined. The pattern repeats: initial spike, rapid exodus, ghost town. The underlying cause is the same: community was never real, just a collection of mercenaries attracted by extraction opportunity rather than genuine belief.

這與無數專案形成對比 ── 它們發行時有極高社群人數、話題空投,隨後價格下跌、社群蒸發,一再重演:先暴衝、再出走、最後淪為死城。原因如出一轍:這些社群從來不真實,只是一群見獵心喜的傭兵,圖利而非共識。

Community building cannot be outsourced. Marketing agencies can execute tactics, but authentic communities coalesce around founders and core contributors who demonstrate commitment, competence, and genuine care for participant experience. There is no shortcut or substitute for the human connection that transforms users into believers.

社群建設無法外包。行銷公司只能執行戰術,真正的社群卻是圍繞有承諾、有能力、真心關懷參與者的創辦人與核心貢獻者聚合而成。人與人之間的連結,才是將使用者變成信仰者的唯一途徑,沒有捷徑也沒有替代方案。

From a practical marketing standpoint, as outlined in a comprehensive token launch playbook: "Most crypto startups have a core product and a token - do not confuse the two. Your product likely fixes a problem, adds value to the user, and would probably be used without a token." The key is building genuine product-market fit first, then using the token to amplify growth rather than substitute for weak fundamentals.

從實務行銷角度來看,正如一份完整發幣手冊[所指出]:"多數加密新創有核心產品與代幣兩項資產——請勿混為一談。你的產品多半能解決問題、創造使用者價值,即使沒有代幣也會有用戶。" 關鍵在於先打造真的產品市場契合,再以代幣推升成長,而非用代幣掩飾根基薄弱。

Technical Readiness: Audits, Infrastructure, and Stress Tests

技術準備:合約審計、基礎設施與壓力測試

Token launches are fundamentally technical events that require robust infrastructure, thoroughly audited code, and proven ability to handle real-world usage. Yet many projects treat technical preparation as secondary to marketing and fundraising, resulting in preventable failures that destroy community trust and token value simultaneously.

發幣本質上是高度技術性的事件,需要穩健的基礎設施、徹底審計過的程式碼,以及應對實際負載的能力。然而許多專案卻把技術準備置於行銷或募資之後,導致本可避免的失敗,最終摧毀社群信任與代幣價值。

Smart contract audits represent the baseline requirement, not optional luxury. Industry experts consistently emphasize that security must be baked in from the start. As noted in comprehensive token development guidance: "In 2025, rug pulls, exploits, and contract bugs still plague the industry. A single flaw can destroy user trust and investor confidence. This is why conducting a third-party smart contract audit is no longer optional - it's mandatory for any serious token launch." Reputable firms - CertiK, Trail of Bits, OpenZeppelin, ConsenSys Diligence - employ experienced security researchers who systematically analyze code for vulnerabilities including reentrancy attacks, integer overflows, access control failures, and logic errors. A single undiscovered vulnerability can enable exploits that drain protocol treasuries or manipulate token supplies.

智能合約審計是最低標準,絕非錦上添花。業界專家一再強調,安全必須從一開始就徹底落實。如[一份完整開發指引所述]:"到了2025年,地毯式詐騙、漏洞利用、合約 Bug 仍充斥業界。一個小缺陷就足以毀掉用戶信任與投資信心。這是為什麼第三方智能合約審計已不是選配,而是每個嚴謹發幣專案的強制要求。" CertiK、Trail of Bits、OpenZeppelin、ConsenSys Diligence 等知名公司聘有資深資安研究員,會系統性檢查重入攻擊、整數溢位、權限漏洞及邏輯錯誤等重大風險。一個未被發現的漏洞,足以被駭客用來洗劫協議金庫或操控供應量。

The Nomad Bridge hack in August 2022 illustrates audit limitations. Despite passing audit, a critical vulnerability allowed attackers to withdraw $190 million. The Wormhole bridge lost $320 million in February 2022 after exploiters discovered flaws in signature verification. Mango Markets suffered a $110 million exploit in October 2022 through oracle manipulation that audit did not anticipate. These incidents demonstrate that audit does not guarantee security, but lack of audit virtually guarantees eventual compromise.

2022年8月的 Nomad Bridge 攻擊就是審計侷限的明證。即使通過審計,還是有致命漏洞讓駭客盜走1.9億美元。Wormhole 橋則在2022年2月因簽章驗證機制被攻破,損失3.2億美元。Mango Markets 在2022年10月遭預言機操控,虧損1.1億美元,也是審計沒有預料到的問題。這些案例說明,審計無法保證安全,但沒做審計,最終一定出事。

Multiple audits from independent firms provide more confidence than single assessments. Different auditors bring different perspectives and methodologies. Code that satisfies one firm's review may contain vulnerabilities that another identifies. The cost - typically $50,000 to $200,000 per audit depending on code complexity - represents essential infrastructure investment rather than optional expense.

多由獨立機構重複審計遠比單一審計更可靠。不同審計團隊有不同觀點與方法,一家沒發現的缺陷,另一家可能查出。單次審計費用(視程式碼複雜度)約在5萬到20萬美元區間,是基礎建設的必要投資,不是可有可無的支出。

Bug bounty programs complement formal audits by crowdsourcing security review to broader researcher communities. Programs on platforms like Immunefi or HackerOne offer rewards for vulnerability discovery, creating economic incentive for ethical disclosure rather than exploitation. Successful programs offer meaningful bounties - major vulnerabilities should command six-figure rewards - to compete with black market exploitation rewards that can reach millions.

漏洞懸賞能用群眾外包補足正式審計,廣邀全球研究人員發現問題,像 Immunefi 或 HackerOne 等平台都能協助舉辦。提供高額賞金(重大漏洞應達六位數美元),才能吸引研究者揭露,而不是賣給黑市。這類計畫能有效防止漏洞被用來利用。

Infrastructure testing often receives insufficient attention despite being critical to launch success. RPC node capacity must handle expected transaction loads with margin for spikes. A successful token launch generates far more activity than typical usage - claim transactions, trading activity, and curious users all converge simultaneously. Insufficient infrastructure causes timeouts, failed transactions, and frustrated users.

基礎設施測試往往被忽略,但卻攸關發幣成敗。RPC 節點必須能負荷預期交易量,甚至留有應急空間。成功發幣時,兌領、交易、圍觀者都會同時湧入,遠遠超過日常流量。基礎設施若不夠力,定會出現逾時、中斷、用戶無法交易等狀況。

Load testing simulates heavy usage before real users arrive. Synthetic tests generate thousands of simultaneous transactions to identify bottlenecks, measure response times under stress, and verify that systems degrade gracefully rather than catastrophically when capacity limits are exceeded. Teams should test at multiples of expected launch day activity because real-world usage invariably exceeds projections.

上線前的壓力測試是不可或缺的。必須用模擬流量產生數千並行交易,辨識瓶頸、測量壓力下反應時間,以及確認系統在超載時是優雅退場而非全線崩潰。團隊必須以高於預期發行日數倍的指標來測試,因為實際用量往往遠超預估。

Token bridge security deserves particular attention for projects deploying across multiple chains. Bridges represent persistent attack surfaces that require continuous monitoring and security updates. Each bridge integration introduces dependencies on external systems whose security the project cannot fully control. Teams should carefully evaluate which chains genuinely benefit their use case versus which represent speculative expansion that increases attack surface without corresponding value.

跨鏈專案更要重視橋接器的安全。橋接器是持續的攻擊目標,必須時刻監控、定期更新。每接入一條新鏈,就多一分對外部系統(其安全狀態專案方難以主控)的依賴。團隊需謹慎評估哪些鏈是真正有利應用場景,哪些只是投機式擴張,只會擴大攻擊面而無實質效益。

Integration testing with exchanges and market makers prevents launch day chaos. Does token contract format match exchange expectations? Do transfer mechanics work correctly? Are decimal places handled consistently? These mundane details cause real problems when discovered during live trading rather than test environments. Coordination calls between technical teams several weeks before launch identify and resolve compatibility issues.

與交易所、造市商做集成測試同樣不可少。合約格式是否符合集成方標準?轉帳規則有無問題?小數點處理一致嗎?這些看似瑣碎的細節,若是在上線時才遇到,往往釀成重大災難。最好的做法,是提前數週讓技術團隊協調測試並修正相容性問題。

Frontend user experience receives less attention than backend infrastructure but determines user success rates. If claiming tokens requires multiple transaction confirmations, each step represents dropout opportunity. If error messages provide no actionable guidance, users give up rather than troubleshoot. If gas estimation fails, users either overpay or have transactions fail. Polished user experience - clear instructions, helpful error messages, transaction status tracking - dramatically improves launch success.

前端使用體驗常被忽略,卻是用戶體驗的關鍵。若領幣流程要多次確認,每一步都可能流失用戶。錯誤訊息若沒有明確指示,使用者只會直接放棄,不會主動排查。Gas 預估出錯,用戶不是多花錢就是交易失敗。流暢的使用者體驗——明確說明、友善提示、即時狀態追蹤——會大幅提升上線成果。

Monitoring and incident response capabilities must be in place before launch. When problems occur - and they will - how does the team detect issues, coordinate response, communicate with users, and deploy fixes? A documented incident response plan, pre-established communication channels, and assigned roles prevent chaos when seconds matter. The difference between quickly resolving a problem and letting it spiral often determines whether the project maintains credibility.

監控與事件應變能力必須於發佈前就全部到位。問題一定會發生——團隊該如何偵測、協調解決、回報用戶和部署修正?一份明確的應變計畫、預先設置的溝通渠道、分配好的人員職責,能在分秒必爭時防止混亂。能否速戰速決,不讓災情惡化,常常左右項目能否保住信譽。

Rollback mechanisms require consideration despite philosophical resistance from decentralization advocates. If critical vulnerability is discovered hours after launch, can contracts be paused? Can migrations to corrected contracts occur without starting over? The tension between immutability principles and practical ability to respond to discoveries has no perfect resolution, but having options beats discovering during crisis that no remediation path exists.

即使去中心化派會反對,Roll back(回滾)機制還是值得事先設計。若發現致命漏洞,合約能暫停運作嗎?能否無需全部重啟地遷移至修正版?不變性的哲學與危機應對的現實本就衝突,但事前備有選項,總比臨陣發現無解要好太多。

Third-party dependencies should be catalogued and monitored. Does the token contract depend on oracles? What happens if those oracles malfunction? Does frontend rely on specific RPC providers? What if they experience downtime? Identifying single points of failure and establishing backup providers creates resilience.

第三方依賴必須完整清點範圍並持續監控。合約有依賴預言機嗎?出問題怎麼辦?前端是否只仰賴單一 RPC 服務商?如果癱瘓怎麼辦?識別單一潛在失效點、建立備援方案才有韌性。

Technical preparation cannot be rushed. Teams should allocate months for 技術準備絕不能趕鴨子上架。團隊必須預留數月……security review, infrastructure building, testing, and bug fixing. Compressed timelines lead to shortcuts that create vulnerabilities. The market will not reward teams for launching on arbitrary deadlines if launches are plagued by technical failures. Better to delay launch than to execute poorly and damage reputation permanently.

安全性審查、基礎設施建置、測試與修復漏洞。壓縮時程通常會導致取巧,進而產生潛在的安全風險。如果發佈時出現技術故障,市場不會因為團隊趕上隨意設定的死線而給予獎勵。與其倉促上線導致執行不良並永久損害聲譽,不如延後發佈。

Timeline and Coordination: How to Sequence the Launch

Token launches require coordinating across technical, legal, marketing, and partnership workstreams with precise timing. The typical pre-launch timeline spans three to six months, though complex projects may require longer preparation. Understanding critical path dependencies and sequencing decisions prevents costly delays or rushed execution.

代幣發行需要跨技術、法務、行銷及合作夥伴等多個工作流程進行精確協調。標準的發佈前時程通常為三至六個月,但複雜項目可能需要更長的準備時間。了解關鍵路徑依賴及流程排序,能避免代價高昂的延遲或倉促上線。

As emphasized in a16z crypto's operational guidelines: "The first thing to know when launching a token is that it takes time and teamwork. The process involves several types of stakeholders - protocol developers, third party custodians, staking providers, investors, employees, and others - all of whom must be on the same page when preparing for the creation and custody of a new digital asset."

正如 a16z crypto 的操作指引中所強調的:「發行代幣首先要了解這是一個需要花時間與團隊合作的工程。此過程牽涉多種類型的利害關係人—協議開發者、第三方託管人、質押服務商、投資者、員工等等—在新數位資產的創建及託管準備期間,大家都必須步調一致。」

The timeline begins at T-minus six months with tokenomics finalization and legal structure establishment. Teams must complete token design, model supply and demand dynamics under various scenarios, and incorporate entities in appropriate jurisdictions. Legal structure determines tax treatment, regulatory obligations, and ability to engage with service providers. These foundational decisions constrain all subsequent choices, so rushing them creates problems that cannot be fixed later.

時程從發佈前六個月開始,包括代幣經濟最終化及法務架構建立。團隊需完成代幣設計、於各種場景下的供需動態建模,並於適當法域設立實體。法務架構決定稅務處理、法規責任及能否和服務供應商合作。這些基礎決策會影響所有後續選擇,倉促決策將產生後續無法修補的問題。

Smart contract development and initial security review occur in months four through six. Teams write token contracts, vesting contracts, governance mechanisms, and any protocol-specific functionality. First pass code audits identify major issues that require redesign rather than minor fixes. This phase requires close collaboration between developers and auditors to ensure that fixes do not introduce new vulnerabilities.

智能合約開發及初步安全審查會在發佈前四至六個月進行。團隊會撰寫代幣合約、歸屬合約、治理機制及任何協議專有功能。初步的程式碼稽核僅能找出重大問題,需要重新設計而非小修小改。此階段需開發者和稽核員密切合作,確保修正不會引入新漏洞。

Market maker and exchange discussions begin at T-minus three months. Professional market makers require months to evaluate opportunities, negotiate terms, and deploy infrastructure. Exchanges have listing pipelines with limited capacity and their own schedules. Starting these conversations early ensures availability and prevents finding that preferred partners have no capacity for the planned launch window.

與做市商與交易所的洽談應在發佈前三個月展開。專業做市商通常需數個月來評估機會、協商條件並架設基礎設施。交易所的上架流程有容量限制及排程。及早開始接洽,可確保資源到位,避免優先合作對象到了預定時程反而沒有配合空檔。

Final audits, legal opinion letters, and compliance documentation consume T-minus two months. After code changes are complete, formal audits issue final reports. Legal teams prepare opinion letters on regulatory classification, draft white papers or prospectuses meeting local requirements, and confirm that all compliance obligations are satisfied. This bureaucratic phase feels slow but attempting shortcuts invites regulatory attention.

最終審計、法務意見書、合規文件需在發佈前兩個月內完成。程式碼變更結束後正式稽核會出具最終報告。法務團隊會撰寫監管分類意見書、草擬符合當地法律要求的白皮書或說明書,並確認已滿足所有合規義務。這一行政階段雖然進展緩慢,但若圖取捷徑往往反而招致監管審查。

T-minus one month focuses on marketing acceleration and community mobilization. Announcement schedules are finalized, content calendars are populated, press relationships are activated, and community calls increase frequency. The goal is generating maximum attention at launch while providing sufficient information that participants make informed decisions rather than speculating blindly.

發佈前一個月需加速行銷及動員社群。公告行程最終確定、宣傳日曆填滿、媒體關係啟動並增加社群聚會頻率。目標是在發佈時達到最大關注,同時提供足夠資訊,讓參與者能明智決定,而非盲目投機。

The final week before launch requires military precision. All systems undergo final testing. Exchange integrations are verified. Market makers confirm readiness. Legal teams provide clearance. Communication plans are rehearsed. Backup procedures are validated. War rooms are established with representatives from every function standing by to address issues.

發佈前最後一週必須像軍事行動般精密。所有系統要進行最終測試、確認交易所整合無誤、做市商確認可隨時上線、法務團隊給予最後放行。溝通計劃需演練、備援程序要檢查無遺。成立臨時作戰中心,由每個專職代表進駐,以隨時應對突發狀況。

Launch day itself is both climax and anticlimax. If preparation was thorough, the actual launch is mechanical execution of tested procedures. Teams monitor systems, track performance metrics, communicate updates, and respond to inevitable surprises. If preparation was inadequate, launch day is chaos - systems fail, partners are not ready, community is confused, and price action reflects the disorder.

發佈日本身既是高峰也是反高潮。若準備充足,發佈僅是照程序表執行已測過的步驟。團隊會監控系統、追蹤績效指標、即時通報進度並應對難免發生的意外。準備不足時,發佈日就是混亂—系統故障、合作夥伴措手不及、社群困惑、價格波動反映四處失序。

Post-launch, the first 24 to 72 hours are critical. Initial trading establishes price discovery, community reactions determine sentiment trajectory, and technical performance either validates preparation or exposes gaps. Teams should be fully available for this period rather than treating launch as endpoint.

發佈後首24到72小時至關重要。初步交易決定價格發現,社群反應影響後續市場情緒,而技術表現則驗證準備成果或者揭露漏洞。團隊在這段時間必須全員待命,不能把發佈當作結束點。

Cross-functional coordination cannot be overemphasized. Developers, lawyers, marketers, and business development teams often operate in silos with inadequate communication. Token launches require these functions to operate in lockstep with shared timelines, mutual dependencies, and constant information flow. Weekly cross-functional meetings in the final quarter before launch ensure alignment and surface issues before they become crises.

跨部門協作極其重要。開發人員、律師、行銷和業務發展團隊常是各自為政,溝通不暢。代幣發佈要求這些功能組精確同步,時程共享、相互依賴並保持資訊即時流通。在最後一季每週召開跨部門會議,能確保共識及及早處理問題,避免事態惡化。

Buffer time should be built into timelines. Audits take longer than vendors promise. Legal opinions require multiple revision rounds. Exchange integrations reveal compatibility issues requiring code changes. Marketing assets require unexpected revisions. Building slack into schedules prevents cascading delays when individual workstreams slip.

時程中應預留緩衝時間。審計通常比供應商承諾的還要久、法律意見需多次修正、交易所整合會暴露需改程式的相容性問題、行銷素材也常要臨時重製。加大鬆動量,才能在個別流程延宕時避免連鎖延期。

The temptation to rush should be resisted. Market conditions may seem perfect, competitors may be launching, or impatient investors may pressure for speed. But premature launch with incomplete preparation damages projects far more than short delays. Markets forget delays quickly. Markets never forget disastrous launches.

必須抗拒草率上線的誘惑。即使市場看似絕佳、競爭對手將發佈或投資人催促加速,沒準備好就強推上線只會帶來長遠災難。市場很快會遺忘延遲,但絕不會忘記失敗的發佈。

Common Mistakes to Avoid

Analyzing token launch failures across the 2024-2025 cycle reveals recurring patterns that teams should actively avoid. These mistakes are neither subtle nor novel, yet they persist with depressing regularity.

分析 2024-2025 這一輪代幣發佈失敗案例,會發現若干反覆出現的錯誤,團隊需積極避免。這些錯誤既不罕見也不新奇,卻令人沮喪地不斷重演。

Unrealistic valuations top the list. Teams that raise at $1 billion fully diluted valuations despite minimal users, negligible revenue, and speculative roadmaps burden their tokens with mountains of overhead. Early investors who purchased at $10 million valuations naturally sell when public markets offer exits at $500 million. The resulting selling pressure overwhelms genuine demand, causing price spirals that destroy confidence. Conservative valuations that leave room for growth serve projects far better than headlines about massive raises.

不切實際的估值排在首位。有些團隊即便用戶極少、營收微薄、願景高度投機,卻仍以高達10億美元的完全稀釋估值募資。早期在1000萬美元估值入場的投資人,自然會在市值5000萬時出脫。由此產生的拋壓遠超實際需求,引發價格雪崩、信心盡失。保守估值、預留成長空間比轟動頭條的大額募資對項目更有利。

Insufficient liquidity provision creates fragile markets where single transactions cause violent price swings. Teams that launch with thin order books discover that excited community members cannot buy tokens without pushing prices to unsustainable levels, while small profit-takers crash prices precipitously. Adequate liquidity - through market-making arrangements, protocol-owned liquidity, or treasury-seeded pools - enables price discovery without chaos.

流動性不足會形成脆弱市場,單一交易就能引發劇烈價格波動。僅靠薄弱掛單上線,會發現熱情社群根本買不到幣,不然就是一買價格衝天,小額獲利者再輕鬆砸盤將價打回原型。透過做市、協議所有流動性、或金庫注資池,為價格發現提供充足流動性,才能避免這種混亂。

Community overhype without substance generates expectations that reality cannot match. Marketing that promises revolutionary technology, transformative economics, or exponential growth creates disappointment when delivery is merely incremental progress. Better to underpromise and overdeliver than to set expectations that guarantee disillusionment.

社群過度炒作但缺乏實質內容,將導致現實遠低於期待。若行銷強調「革命性技術」、「顛覆性經濟」或「指數型增長」,結果只是微幅進展,勢必令支持者大失所望。不如求穩低調,把成果做出來反勝於設定必然幻滅的高預期。

Token unlock cliffs create predictable dump events that sophisticated traders exploit while retail holders suffer losses. Projects that release 50 percent of supply in single unlocks watch prices crater as recipients race to exit. Linear vesting over extended periods distributes pressure evenly. Coordinating unlocks with protocol milestones ties supply increases to demand catalysts.

一次大量解鎖(unlock cliff)會出現明顯的拋售潮,被老手交易者利用,散戶則慘遭割韭菜。若項目一次釋放一半供應量,看著價格直墜,因為大家爭先恐後拋售。採用長時間線性歸屬,平均釋放壓力,並將解鎖時點與協議重大里程碑搭配,讓供給釋放與需求增長相互呼應。

Insider dumps destroy trust permanently. When team members or early investors sell significant positions immediately after lock-up expiry, community interprets this as lack of confidence. Even if sales are planned treasury management, the optics are devastating. Teams should communicate sale intentions proactively, structure disposals gradually, and demonstrate continued commitment through remaining holdings.

內部人員拋售將永久摧毀信任。若團隊成員或早期投資人一解鎖就大幅出貨,在社群眼中這就代表完全沒信心。即便只是預先規劃的金庫管理,觀感也是災難性。團隊應主動溝通售出意向、漸進式出清,並用持續持有展現承諾。

Overreliance on single exchanges or market makers creates fragility. Projects entirely dependent on Binance for liquidity discover that exchange technical issues, regulatory complications, or shifting priorities can eliminate trading infrastructure suddenly. Diversification across exchanges, venues, and service providers provides resilience.

過度依賴單一交易所或做市商的項目往往脆弱不堪。完全仰賴 Binance 提供流動性,若遇到交易所技術問題、監管疑慮,或資源分配改變,交易基礎設施就可能瞬間消失。多元布局於多家交易所、不同渠道與服務商才能確保韌性。

Poor communication during crisis situations compounds problems. When exploits occur, when markets crash, when roadmaps slip, transparency and rapid acknowledgment maintain trust better than silence or spin. Communities forgive mistakes but rarely forgive deception or negligence.

危機時刻若溝通失靈只會加劇問題。出現安全漏洞、行情崩潰、進度落後時,及時坦誠面對,比起沉默或敷衍自圓其說更能贏得社群信任。錯誤能被原諒,欺騙和疏忽則不然。

The failures carry common DNA: teams prioritized short-term metrics over long-term sustainability, valued marketing over fundamentals, rushed preparation to meet arbitrary deadlines, and failed to model downside scenarios honestly. Success requires inverting these tendencies - building genuine value, managing expectations conservatively, preparing thoroughly, and planning for adversity.

這些失敗有共通的 DNA:團隊著眼短期數字勝於長遠穩健、看重行銷勝於基本面、倉促準備只為趕死線、從未真實模型評估最壞情況。走向成功需反其道而行—追求真實價值、保守預期管理、充分準備、逆境預做規劃。

The Future of Token Launches: Professionalization and Transparency

The token launch landscape in 2025 looks dramatically different from 2021's speculative frenzy or even 2023's cautious recovery. Professionalization has accelerated, driven by regulatory frameworks, institutional participation, and hard lessons from previous cycles.

2025 年的代幣發佈生態已大異於 2021 年的投機狂潮,甚至不同於 2023 年的謹慎回暖。專業化速度加快,受到監管架構、機構參與及前幾輪週期慘痛教訓推動。

On-chain launch frameworks are emerging as alternatives to traditional launchpad models. CoinList OnChain, Base Launch, and similar platforms conduct token distributions entirely through smart contracts, eliminating central intermediaries while maintaining compliance and fairness mechanisms. These systems use verifiable on-chain credentials to establish participant eligibility, conduct price discovery through algorithmic auctions, and distribute tokens programmatically. The transparency is absolute - anyone can verify that distributions occurred as specified and that no preferential treatment occurred.

鏈上發佈框架逐漸取代傳統 launchpad 模型。CoinList OnChain、Base Launch 及類似平台,完全以智能合約自動化代幣分發,無需集中式中介,同時保持合規與公平。這些平台用鏈上認證驗證參與資格、使用演算法拍賣發現價格並自動分配代幣。透明度極高,所有分發皆可查證,無特權之虞。

Regulatory compliance is shifting from grudging necessity to

(內容到此為止,待補完續接)competitive advantage. Projects that operate transparently within legal frameworks increasingly access institutional capital unavailable to regulatory arbitrageurs. MiCA's implementation across the EU creates standardized rules that reduce uncertainty for compliant projects while increasing costs for those attempting to operate in gray areas. The U.S. regulatory environment, while less clear than Europe's, is also maturing with ongoing SEC enforcement and potential legislative clarity.

競爭優勢。在合法框架下透明運作的專案,越來越能獲得制度性資本,而這些資本是監管套利者無法取得的。MiCA 在歐盟的實施建立了一套標準規則,降低了合規專案的不確定性,同時提高了試圖在灰色地帶運作專案的成本。雖然美國的監管環境較歐洲不明確,但在 SEC 持續執法及潛在立法的推動下,也正逐漸成熟。

Data transparency and analytics are becoming prerequisites for serious consideration. Projects that publish real-time on-chain metrics, conduct independent tokenomics audits, and provide verifiable evidence of protocol usage earn trust that marketing cannot manufacture. Platforms like Dune Analytics, Nansen, and Token Terminal enable anyone to verify claims about users, revenue, and activity. In this environment, projects cannot fake success - numbers speak for themselves.

數據透明度與分析已成為專案受重視的前提。願意公開鏈上即時數據、主動進行獨立代幣經濟審計,並能提供協議實際使用的可驗證證據之專案,能贏得非行銷所能創造的信任。像 Dune Analytics、Nansen、Token Terminal 這類平台,讓任何人都能驗證專案關於用戶、收入、活躍度的宣稱。在這樣的環境下,專案無法假造成功——數字會說話。

The rise of on-chain reputation systems creates accountability that previous cycles lacked. Team members whose projects fail or who engage in questionable practices carry that history across future ventures. Protocols that deliver on promises build reputations that transfer value to subsequent projects. These dynamics incentivize long-term thinking and responsible behavior while punishing short-term extraction.

鏈上聲譽系統的興起,建立了以往週期所缺乏的問責機制。專案失敗或從事可疑行為的團隊成員,他們的這段經歷會被帶到未來的創業路上。而能夠兌現承諾的協議,則建立起可延續到後續專案的優良聲譽。這些動態促使更長期、負責任的思維與行為,同時懲罰短期掠奪。

Token launches are converging toward a recognizable playbook: conservative tokenomics that prioritize sustainability over hype, comprehensive legal preparation that enables operation in major markets, multi-month community building that creates genuine believers rather than mercenary farmers, professional service providers that deliver infrastructure rather than smoke and mirrors, and transparent communication that earns trust through honesty rather than promising moons.

代幣發行正逐漸一致走向一套明顯的標準流程:採用保守並重視永續性的代幣經濟設計、完善法律準備以支持在主要市場運營、數月社群經營以建立真正的信仰者而非投機農夫、引入提供實質基礎建設的專業服務團隊,而不是空有噱頭、並以誠實透明溝通贏得信任,而非畫大餅。

The playbook does not guarantee success - market conditions, competitive dynamics, and execution quality still matter enormously. But following the playbook dramatically increases odds while ignoring it virtually guarantees problems.

這套流程並不能保證成功——市場情勢、競爭動態與執行力仍舊極為關鍵。但遵循這流程大幅提升成功機率,而忽視它則幾乎注定出問題。

Looking forward, the professionalization trend seems irreversible. The marginal token launch in 2026 will involve more legal review, more sophisticated tokenomics modeling, more rigorous technical preparation, and more professional service providers than its 2021 equivalent. This creates higher barriers to entry that filter low-effort projects while enabling better-prepared teams to stand out.

展望未來,專業化趨勢已難以逆轉。到了 2026 年,一場一般規模的代幣發行所需的法律審查、精密經濟模型、技術準備與專業服務,勢必遠超 2021 年同類發行。這提高了進入門檻,有效篩選出低投入專案,讓備戰充足的團隊脫穎而出。

The question facing founding teams is whether they treat token launches as speculative events or strategic operations. Those who understand the difference and prepare accordingly will benefit from institutional tailwinds, regulatory clarity, and market evolution that rewards substance over hype. Those who cling to previous cycle playbooks will struggle in an environment that no longer tolerates shortcuts.

創辦團隊眼下最大的抉擇,就是你是否將代幣發行視為投機事件還是策略性營運。明白其中差異並謹慎準備者,將受惠於機構資本、監管明朗與市場轉變,帶來重內涵、去噱頭的獎勵。仍抱守過往週期舊招者,終將難以在禁不起投機取巧的當下存活。

The next wave of successful tokens will come from disciplined teams that understand what must happen before the token drops, prepare meticulously across every dimension, coordinate seamlessly across functions, and execute launches that reflect genuine value rather than manufactured excitement. The market has matured. Have you?

下一波成功的代幣發佈,將來自自律而嚴謹的團隊——明瞭發幣前必須完成哪些準備,面面俱到,功能橫向配合、發行成果展現真正價值、而非人為操弄炒作。市場已經成熟,你準備好了嗎?