以太坊價格在 2025 年大幅上漲,近期突破約 4,600 美元,創下自 2021 年 12 月以來的新高。這波強勁漲勢讓全球第二大加密貨幣再次成為焦點,也引發一個重要疑問:以太坊如今是否正在引領新一輪山寨幣季?隨著機構資金湧入 ETH 基金,散戶市場活動亦見增溫,加密貨幣交易者與分析師普遍樂觀,但是否真正進入山寨幣大牛市,抑或僅止於以太坊本身的行情,市場意見分歧。本文將說明以太坊近期表現亮眼背後的證據與市場情境,解析其在整體加密市場週期的定位,以及這一走勢可能對其他山寨幣及以太坊 Layer-2 生態系帶來的影響。

「山寨幣季」指的是比特幣以外的加密貨幣(基本上除了 BTC 以外的所有幣)大幅上漲並於一段期間表現優於比特幣的時期。此階段資金通常從比特幣流向風險更高的幣種,價格普遍飆升,且投資人追逐暴利,市場氣氛極為狂熱。在歷史上,山寨幣季常常在比特幣經過一輪大漲並價格趨穩後出現,交易者對其他標的尋求更大收益。

當前,隨著比特幣突破十萬美元歷史新高後略有回落,山寨幣迎來亮相條件。最大山寨幣以太坊展現強勁多頭訊號——從鏈上活動空前活躍到機構湧入高度關注——暗示其可能成為下一輪山寨幣行情的主導者。但問題在於,整體山寨幣市場是否真的全面啟動,還是我們正目睹一波聚焦 ETH 本身的「以太坊季節」?此外,若真的由以太坊帶領行情,這會對整個加密生態(尤其是基於以太坊之 Layer-2 網路)造成何種漣漪效應?

本文將聚焦於 2025 年市場現狀,同時回顧過往週期經驗,解析驅動以太坊上漲的核心因素(如 ETF 資金流入與企業採用)、以太坊網路發展狀況,以及 ETH 作為去中心化金融「支柱」的新敘事。亦會觀察山寨幣季早期跡象:比特幣市值佔比開始下滑,一些老牌山寨幣突然活躍——這些都是資金輪動的典型信號。不過,也需要提醒風險,包括以太坊創辦人 Vitalik Buterin 警告機構過度槓桿操作的潛在隱憂,以及當前市場亢奮可能伴隨的回調。最後,隨著 ETH 成功愈發與 Layer-2 擴容方案密切相關,將深入探討「以太坊季節」對如 Arbitrum、Optimism 及 Base 等 Layer-2 網路的意義——這些方案正承擔愈來愈多的鏈上交易。

以太坊 2025 年強勢回歸:重返歷史新高領域

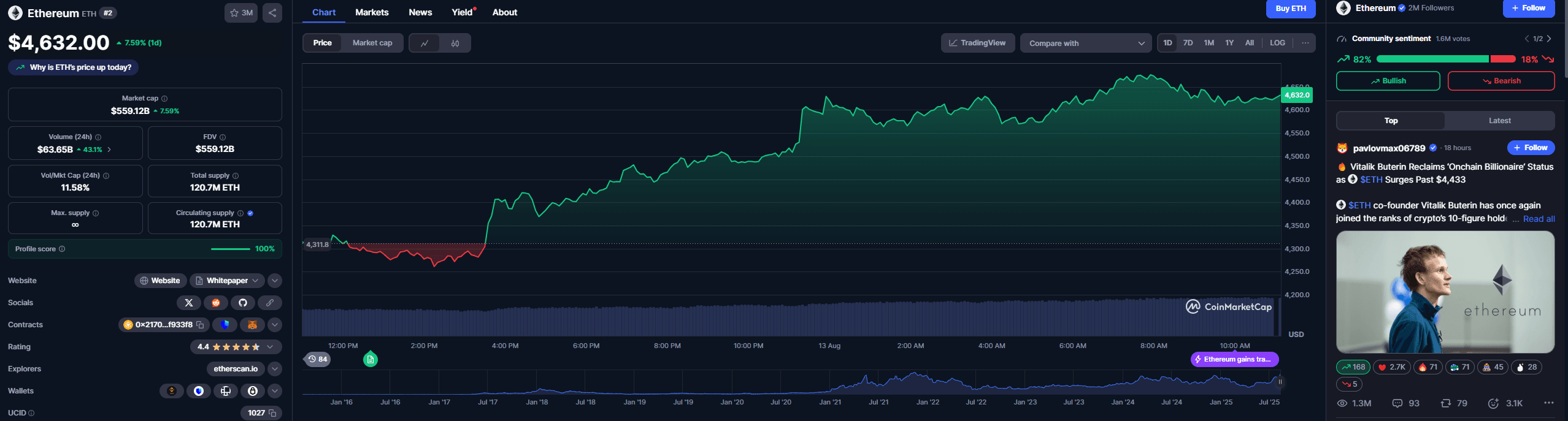

經歷 2022–2023 年熊市後,以太坊於過去一年強勁反彈。2025 年 8 月初,ETH 首度四年來重新站上 4,000 美元,並數日內迅速突破 4,200、4,500 美元。至 8 月中旬更一度觸及約 4,600 美元,距 2021 年 11 月創下的 4,800 美元歷史高點僅差數個百分點。做為對比,在上一輪熊市,ETH 一度跌破 1,000 美元,這波漲幅已超過四倍。強力升勢伴隨著大量空單回補:隨著價格攀升,做空 ETH 的交易者被迫平倉,加速推升價格。僅 48 小時內,超過 2 億美元 ETH 空單在交易所被清算,為本輪漲勢再添動能。有分析師戲稱「ETH 空軍全軍覆沒」,快速的價格變化打了不少悲觀交易者一個措手不及。這種連鎖清算效應,不僅凸顯多頭行情強勁,也反映市場信心正在轉向以太坊。

多項量化指標顯示以太坊進入新一輪牛市階段。交易量隨價格飆漲:8 月 8 日 ETH 首度突破 4,000 美元時,各大交易所日成交量幾乎是日均值的三倍。如此高的交易量顯示散戶及機構對 ETH 恢復興趣,且是真正的資金進場。更值得注意的是,區塊鏈鏈上數據顯示以太坊網路使用量創歷史新高,證明本輪上漲並非單純投機,而有實質用戶需求。2025 年 7 月,以太坊鏈上總交易筆數達 4,667 萬,刷新歷史紀錄。換句話說,即使和 2021 年底牛市高峰相比,如今以太坊網路交易活動更多。以美元計,2025 年 7 月 ETH 鏈上交易量達 2,380 億美元,月增 70%。不論是去中心化交易、穩定幣移轉還是智能合約互動,以太坊上結算的價值空前龐大,折射出生態發展興旺。

更關鍵的是,這波活動暴增尚未引發過去牛市那種無法承受的高額手續費。7 月至 8 月初,以太坊平均手續費維持在 0~4 美元間,僅極端壅塞時短暫上升至 6–8 美元。相比 2021 年那波牛市,當時高峰期常見單筆交易手續費動輒兩位數、甚至三位數美元。當前低手續費顯示,以太坊擴容升級與 Layer-2 解方已有效紓緩擁堵(後續章節將詳述)。實際上,以太坊鏈上出塊平均僅使用約 50% gas,上鏈空間相對充裕,這代表協議優化明顯,且鏈外擴容發揮成效,有利網路進一步成長並避免短期高成本壓力。

市場對以太坊未來抱持信心的另一重要指標,是 ETH 被鎖倉的比例持續攀高。自 2022 年「合併」後,越來越多持有者將 ETH 質押於網路,以確保安全並賺取收益。截至 2025 年 8 月,超過 30% ETH 總供應量已質押於存款合約,總數已逾 1.2 億枚,現價計逾 1,500 億美元。質押將這部分 ETH 暫時鎖定,減少市場流通,進一步加劇供給壓力並助漲行情。同時,交易所 ETH 持倉量持續下滑,目前僅剩 1,530 萬枚,創2016年以來最低,等於現存八枚 ETH 就有一枚被質押,熱錢包內餘額則降到九年新低。這說明許多投資者選擇長期持有,不論是參與質押或暫無拋售打算,降低拋壓亦讓市場供給更緊俏,有助於價格上揚。有 Cointelegraph 分析師指出,鏈上活躍增加、交易所供給下滑與質押熱潮,都是 ETH 多頭指標。

以太坊發動的市場正產生積極的「正向反饋迴路」——ETH 價格攀升,部分投資人帳面資產暴增後,藉由「財富效應」輪動進軍其他標的,推動山寨幣上漲。我們已看到部分中型代幣如萊特幣、Solana、Chainlink 等同步錄得雙位數成長。但在分析山寨幣行情前,首先要聚焦以太坊本身為何此刻強漲。這次行情並非無的放矢,背後有基礎因素與總體政策環境改變支撐。下個章節將檢視驅動力——從 ETF 資金流、到大型投資人敘事轉換——如何讓以太坊成為 2025 年最受矚目的主流加密資產。

是什麼推動以太坊大漲?機構資金湧入、新敘事等利多共振

多項利多因素在 2025 年共同推升以太坊,標誌其主流接受度與應用價值不斷提升。首先最重要的是,以太坊近來成為機構投資焦點。2025 年 8 月,美國上市的 ETH ETF(交易所交易基金)單日資金流入破紀錄,顯示大型資金積極佈局 ETH。僅 2025 年 8 月 11 日當天,以太 ETF 净流入達 10.1 億美元,寫下單日新高。作為對照,比特幣 ETF 當日僅吸引 1.78 億美元淨流入,ETH 基金單日流入是 BTC 基金的五倍。當中,貝萊德(BlackRock)旗下 iShares Ethereum Trust 單日吸收約 6.4 億美元資金,富達(Fidelity)的以太坊基金則錄得 2.77 億美元流入。總計目前美國以太坊 ETF 管理資產規模已逾 250 億美元,約佔 ETH 市值 4.8%,距離首度上市不到一年時間。如此規模的資金進場,為 ETH 帶來前所未有的主流關注度與增量需求。 explosive interest from institutions in an Ethereum investment vehicle would have been unthinkable a few years ago, when Bitcoin was the only crypto considered palatable for Wall Street.

從前幾年來看,機構對以太坊投資工具的爆炸性興趣幾乎是難以想像的,當時比特幣是唯一被華爾街視為可接受的加密貨幣。

This sudden institutional pivot toward Ethereum has been driven by a changing narrative. For years, Bitcoin was king in the eyes of traditional finance, lauded as “digital gold” – a simple, compelling analogy that helped institutions get comfortable with BTC as a store of value. Altcoins, by contrast, were often viewed with skepticism. But Ethereum has increasingly differentiated itself with a coherent value proposition that big investors are starting to appreciate. If Bitcoin is digital gold, Ethereum is being touted as “the backbone of future financial markets,” thanks to its role in decentralized finance (DeFi), smart contracts, and tokenized assets. This phrasing comes straight from Bloomberg ETF analyst Nate Geraci, who observed that many in traditional finance previously underestimated Ether simply because they didn’t understand it, but that is now changing. Ethereum’s blockchain is where a huge chunk of crypto economic activity happens – from lending and borrowing to trading and issuing new tokens – so owning ETH is increasingly seen as owning a crucial piece of the infrastructure for the “digital economy”. In essence, ETH produces yield (via staking), powers transactions in a vibrant network of dApps, and even burns fees (reducing supply) with each transaction. These features make it more akin to a productive asset or a form of “digital oil” that fuels Web3 platforms, rather than just a speculative token. Such narratives have given traditional investors a new bullish thesis for Ethereum on top of Bitcoin’s store-of-value appeal.

這股機構轉向以太坊的突變,正是由於敘事的演變。在傳統金融界多年來,比特幣一直是王者,被讚譽為「數位黃金」──這個簡單且具說服力的比喻,有助於機構習慣於將BTC視為儲值工具。相比之下,山寨幣則經常被以懷疑眼光看待。但以太坊如今越來越能以明確一致的價值主張,讓大型投資人開始欣賞它。如果說比特幣是數位黃金,那麼以太坊則被吹捧為「未來金融市場的支柱」,這歸功於其在去中心化金融(DeFi)、智能合約與資產代幣化領域的角色。這種說法直接來自彭博ETF分析師Nate Geraci,他觀察到,許多傳統金融人士過去低估ETH,僅僅因為他們不了解它,但現在這一切正在改變。以太坊區塊鏈承載著大部分加密經濟活動──從借貸、交易到發行新代幣──因此,擁有ETH越來越被視作是持有「數位經濟」關鍵基礎建設的象徵。本質上,ETH能產生收益(通過質押)、驅動活躍的dApp網路交易,甚至每筆交易都會銷毀手續費(減少供給)。這些特性讓它更像是能帶來收益的資產,或是一種為Web3平台提供動力的「數位石油」,而不僅僅只是一枚投機代幣。這些新敘事讓傳統投資人對以太坊有了超越比特幣儲值訴求的新多頭論點。

The data backs up this narrative shift. Consider the trend of corporate treasury adoption of Ether. A few years ago, a handful of companies (like MicroStrategy or Tesla) made headlines for holding Bitcoin in their treasuries. Now, we are seeing companies begin to hold Ethereum as a strategic asset. By August 2025, public companies and fund treasuries collectively hold over $11 billion worth of ETH on their balance sheets. This figure swelled from around $9 billion to $13 billion just in the recent rally, as the price increase boosted the value of their holdings. More firms are embracing ETH “not just as a speculative play, but as a strategic financial tool,” explains Jamie Elkaleh, an executive at Bitget Wallet. Companies see that by holding and staking Ethereum, they can earn passive yield (currently staking yields are on the order of ~5% annually) while also participating in the burgeoning DeFi economy. This is a stark contrast to holding, say, cash (which yields little) or even Bitcoin (which has no native yield unless lent out). In Elkaleh’s words, Ethereum’s appeal to corporates lies in its “foundational utility” – treasuries can put ETH to work and simultaneously help secure the network by staking. It’s a mutually reinforcing dynamic, and one that further cements Ethereum’s image as the “digital oil” lubricating the gears of new financial infrastructure.

數據支持這個敘事的轉變。以企業金庫採用ETH的趨勢為例,幾年前,只有少數公司(如MicroStrategy或Tesla)因持有比特幣而成為焦點。現在,我們看到公司開始將以太坊作為策略性資產納入持有。截至2025年8月,上市公司與基金金庫合計在資產負債表上持有超過110億美元的ETH。這個數字僅在最近一次行情中,就從約90億美元增長至130億美元,因價格上漲提升了持有價值。越來越多企業將ETH視為「不僅僅是投機標的,而是策略性的金融工具」,Bitget Wallet高管Jamie Elkaleh如此說明。公司認為,持有並質押以太坊,不僅每年能獲得約5%的被動收益,同時也參與了蓬勃發展的DeFi經濟。這與持有現金(幾乎沒有收益)或比特幣(除非借出,否則沒有原生收益)形成鮮明對比。Elkaleh表示,以太坊對企業的吸引力在於它的「基礎效用」──金庫可以讓ETH發揮作用,同時透過質押協助保證網路安全。這是一種相互強化的動態,也進一步鞏固了以太坊作為「數位石油」的形象,為新金融基礎設施提供潤滑。

Another tailwind for Ethereum has been the evolving regulatory and macroeconomic environment in 2025, which has generally been more favorable to crypto than the storms of previous years. In the U.S., a major overhang was resolved when the Securities and Exchange Commission (SEC) effectively ended its lawsuit against Ripple (XRP) in mid-2025 and conceded ground on what constitutes a security in crypto. The conclusion of that high-profile case was interpreted as a broader green light for altcoins, Ethereum included, since Ether had also faced past questions about its regulatory status. In addition, U.S. regulators provided clarity that certain staking services and liquid staking tokens are not securities, easing fears that Ethereum’s move to proof-of-stake could invite regulatory crackdowns. This “regulatory clarity” around Ethereum’s core activities has boosted confidence among institutions and retail participants alike. Globally, countries like Canada and several in Europe already have Ethereum ETF products and friendly stances, adding to the legitimacy of ETH as an investable asset.

以太坊另一項順風吹拂,是2025年演變中的監管與宏觀經濟環境,這比過去幾年的風暴更加有利於加密產業。在美國,當證券交易委員會(SEC)於2025年中實質上「結束了對瑞波(XRP)的訴訟」,並在加密資產定義為證券問題上讓步時,長期懸而未決的問題終有解方。這起重磅案件的結論被解讀為給予包括以太坊在內山寨幣的「更廣泛綠燈」,畢竟ETH過去也曾面臨監管地位上的質疑。此外,美國監管方明確表示,某些質押服務及流動質押代幣並非證券,降低了以太坊轉向權益證明(PoS)可能引來監管打擊的擔憂。圍繞以太坊核心活動的這種「監管明朗」,大大提升機構及散戶參與者的信心。在全球,包括加拿大和多個歐洲國家已推出以太坊ETF相關產品與友善政策,進一步強化ETH作為投資標的資產的正當性。

The macro backdrop cannot be ignored either. After a period of rising interest rates in 2022–23 that hurt risk assets, the pendulum is swinging back. By mid-2025, there is a strong expectation that the U.S. Federal Reserve will begin cutting interest rates, potentially as soon as the fall. Futures markets put the probability of a September 2025 rate cut at over 80%. This prospect of easier monetary policy has been a boon for equities and crypto alike, as lower rates typically drive investors toward higher-yielding or growth-oriented assets (since bonds and cash become less attractive). Ethereum, with its combination of growth narrative and yield from staking, stands to benefit in a “lower for longer” rate environment. Indeed, news of softening inflation and imminent rate cuts coincided with Ether’s push past $4,300 in August. Simultaneously, geopolitical and policy developments such as the U.S. Congress advancing pro-crypto legislation (e.g., a bill to regulate stablecoins, known as the GENIUS Act) have improved sentiment. Sean Dawson, head of research at Derive, noted that “favorable U.S. government policy and well-timed institutional engagement has resulted in blood rushing back into the crypto market.” All these forces – macro tailwinds, regulatory clarity, and institutional narrative shifts – have aligned to create a kind of perfect storm for Ethereum specifically.

宏觀經濟背景同樣不容忽視。經過2022–23年一段加息導致風險資產受挫的時期後,現在局勢出現扭轉。到2025年中,美國聯準會有望進入降息週期,最早甚至可能在秋季啟動。期貨市場賦予2025年9月降息的可能性超過80%。貨幣政策放鬆的前景對股票與加密市場都是利多,因為低利率通常推動投資人追求更高收益或成長導向資產(由於債券與現金變得沒那麼吸引人)。以太坊結合成長敘事與質押收益,在「長期低利」環境中將更具優勢。事實上,通膨緩和及降息臨近的消息,就與ETH在8月突破$4,300同步發生。與此同時,美國國會推進如GENIUS法案等支持加密政策(針對穩定幣監管),也提振市場情緒。Derive研究主管Sean Dawson指出:「有利的美國政府政策和時機恰好的機構參與,讓資金迅速回流加密市場。」這些力量——宏觀順風、監管明朗和機構敘事轉變——共同為以太坊創造了一場難得的「完美風暴」。

On the retail side, Ethereum is also seeing renewed interest, albeit in a more measured way than the meme-fueled crazes of the past. There has been a steady uptick in the number of active Ethereum addresses (over 680,000 daily actives recently, a multi-year high), suggesting new and returning users are engaging with the network. Retail crypto investors are also increasingly aware of Ethereum’s central role in DeFi and NFTs, and many view owning ETH as a gateway to participate in those ecosystems. The psychological element is key: as Ethereum approaches their previous all-time high, retail traders have grown more bullish in online chatter – terms like “buying” and “bullish” started vastly outnumbering “selling” and “bearish” in social media posts once ETH crossed $4k. This uptick in retail optimism can itself become a self-fulfilling driver in the short term (through FOMO buying), though it’s something to watch cautiously as excessive euphoria can herald corrections. Market intelligence firm Santiment pointed out that the surge in bullish sentiment in early August was notable and cautioned that overconfidence sometimes leads to short-lived pauses even during uptrends.

從散戶面向來看,以太坊近期也出現了再度升溫的興趣,雖然比以往meme驅動的狂熱要來得理性得多。以太坊活躍錢包數穩步增加(最近日活躍超過68萬地址,創多年新高),顯示新用戶和回流者正在參與網路。散戶加密投資人也日益認識到以太坊在DeFi和NFT中的重要地位,很多人將持有ETH視為進入這些生態系統的門票。心理層面至關重要:隨著ETH接近歷史新高,散戶交易者在網路上的多頭熱情明顯升溫──當ETH突破4000美元,社群媒體「買進」和「看多」的用語明顯大於「賣出」、「看空」。這種散戶樂觀情緒短期內往往能推動(FOMO買盤),但同時也需要警惕,因過度狂熱往往預示後續修正。市調機構Santiment指出,8月初看多情緒的飆升頗為醒目,同時提醒說「過度自信有時即便在多頭行情中也會帶來短暫修正」。

In summary, Ethereum’s surge is underpinned by strong fundamentals and shifting perceptions. Big investors are buying in via record-breaking ETF flows, embracing Ethereum as a core holding alongside Bitcoin. Companies are putting ETH on their balance sheets and staking it, adding a long-term demand base. The network itself is smashing usage records in transactions and volume, reflecting real adoption. And external conditions – from Fed policy to regulatory wins – have created a more hospitable climate for a rally. All of these set the stage for Ethereum to potentially lead the crypto market’s next phase. But does this translate into a full-blown altcoin season? To answer that, we need to step back and examine how an “altcoin season” is defined, and whether the current market structure supports the idea that we’re entering one.

總結來說,以太坊的這波上漲,背後建立在強勁的基本面與敘事翻轉。大型投資人透過創新高的ETF資金流入積極布局,把ETH當成與比特幣並列的核心部位。企業將ETH納入資產負債表並參與質押,為長線需求注入新動能。網路本身在交易量與使用率屢創紀錄,顯示真實用戶採用。外部條件——從聯準會政策到監管利多——也為漲勢營造了更佳環境。這一切鋪墊也許能讓以太坊帶領市場邁向新階段。但,這是否就等於全面性的山寨幣季(Altseason)來臨?要回答這個問題,還得回頭檢視「山寨幣季」的定義,與目前市場結構是否符合該現象。

Altcoin Season 101: Understanding the Cycle and Historical Parallels

「山寨幣季」(altcoin season, 或簡稱altseason)雖然是行內俚語,但它描述的是一種非常真實的市場現象。定義上,山寨幣季即指山寨幣價格集體表現優於比特幣的時期(一般以數週到數月計)。在這些階段,多數山寨幣價格大漲,漲幅往往數倍於過往,而比特幣則維持盤整或成長速度較慢。通俗來說,如果你的加密資產組合中,小幣種大幅超越BTC,你很可能正處於山寨幣季。這些時期通常伴隨市場高波動與全域瘋狂交易。新項目一夕暴漲,甚至許多早已被遺忘的老幣也能因投機尋寶熱潮死灰復燃。最關鍵的是,山寨幣季多屬牛市末段的「短暫高潮時刻」──通常發生在整體加密牛市的後段,一旦投機過度燃燒便很快降溫。

歷史上,山寨幣季經常與比特幣主導率下降同步發生。比特幣主導率指其市值佔整體加密資產的比例。當主導率急劇下滑,意味著所有山寨幣(集合)的價值正在比比特幣更快成長。我們可以參考兩個主要歷史案例:2017年末至2018年初,以及2021年春季的山寨幣熱潮。

-

2017–2018山寨幣季:比特幣於2017年底大漲,當年12月衝至2萬美元下方頂峰,當時比特幣市值佔整體加密市場約85%。然而,隨著2018年伊始,比特幣主導率迅速跌落──從2017年底的86%一路滑落至2018年1月的約38%。這場主導率崩塌來自上百種山寨幣價格爆炸式增長,即便此時比特幣己經脫離高點回落。導火索在於首次代幣發行(ICO)狂潮──也就是新代幣募資──使得大量資金湧入以太坊(購買ICO代幣需要ETH)同時流向這些全新的代幣。在那段期間,以太坊價格從10美元不到...year prior)、許多較小的山寨幣如瑞波幣(XRP)、Cardano 及其他也出現了指數級的漲幅。有那麼一段時間,似乎每個幣都能一飛沖天,導致比特幣相形之下竟然顯得「有點無聊」。這一波山寨幣季節在 2018 年初戛然而止,原因是對 ICO 的監管擔憂以及整體市場的疲勞,造成市場急遽下跌——許多山寨幣在接下來的熊市中蒸發了大部分價值。

-

2021 年山寨幣季節:快轉到 2020–2021 年,加密貨幣市場再次展現牛市行情,比特幣再次領跑,並於 2021 年 4 月創下當時新高(約 64,000 美元)。但在比特幣初步衝高之後,市場關注焦點逐漸轉向山寨幣。到 2021 年 5 月,比特幣的市佔率從年初的約 70% 滑落到年中的約 40%。這段期間,迷因幣如狗狗幣(Dogecoin)和柴犬幣(Shiba Inu)擁有驚人漲幅(狗狗幣在短短幾個月內暴漲超過 10,000%,受社群媒體與名人效應推動)。同時,NFT(非同質化代幣)在以太坊等鏈上爆炸成長,帶動了 NFT 與遊戲平台相關的代幣。這一輪山寨幣季節較為多元,不再只是單一 ICO 熱潮,而是涵蓋迷因幣、DeFi 代幣、NFT 相關代幣、智能合約平台代幣等多線齊發。2021 年 4 月 16 日,知名的“Altcoin Season Index”達到 98 分(滿分 100),極度顯示過去 90 天內山寨幣遠超比特幣。簡單來說,如果你在 2021 年初持有前 50 名的山寨幣,這段期間大多賺得比只持有比特幣還多。正如 2018 年一般,這波山寨幣狂潮之後也逐漸降溫;比特幣在 2021 年底第二波衝高刷新新高,許多山寨輪流見頂後進入 2022 年的回落週期。

從上述案例可以歸納出一個模式:山寨幣季節往往緊隨比特幣暴衝之後,在比特幣漲勢趨緩時啟動。持有大量 BTC 獲利的投資人會將部分資金轉進山寨幣,因這些幣種短線上潛力更大。這種資金輪動常被描述為 「BTC 先漲 -> ETH 接力 -> 中小市值山寨幣再漲。」 一般會從以太坊開始(做為最大、流動性最好的山寨幣),然後再擴散至規模更小、風險更高的幣種。一個重要前提是比特幣至少需穩定;如果比特幣暴跌,山寨幣通常跌得更慘,無法形成山寨幣季節。反之,若比特幣強勢或維持盤整,市場就有信心和空間投入山寨幣。

在這樣的理解下,當前時機如何?2025 年,比特幣於上半年迎來巨大漲幅,突破此前 69,000 美元高點,一度衝上 100,000 到 120,000 美元。事實上,有報導指出比特幣於 2025 年 7 月在部分交易所創下接近 119,000 美元歷史新高。在如此歷史級爆發後,比特幣動能稍微降溫,近來在 110,000 到 120,000 美元之間震盪,而非無止盡上攻。正如過往,我們開始看到資金轉向以太坊與部分山寨幣。比特幣市佔率於本輪高點時多年來首度超過 60%,如今開始下降。7 月初,比特幣市佔率約 64%;到 2025 年 8 月初,已跌到約 59%。這可能看起來變化不大,但在數兆美元市值中,5 個百分點代表數百億美元的資金流向山寨幣。市場觀察家十分關注市佔率破位。技術分析師甚至指出,比特幣市佔率於 2025 年中跌破多年上升趨勢線,可能是重大山寨幣週期啟動的強烈信號。

此外,以太坊最近與比特幣的相對表現也相當醒目。在一個月期間(6 月底至 8 月初),ETH 漲幅約 54%,比特幣僅約 10%。以太坊如此明顯領先,通常是山寨幣季節初期的重要徵兆。由 BlockchainCenter 維護的山寨幣季節指數,在這段期間一路由極低的“比特幣季”值升至 30-40 分(滿分 100),顯示市場開始傾向山寨幣,但截至 8 月初尚未進入全面山寨季。至 8 月中,此指數約在 50 初(膠著狀態),代表大約一半主流幣種在過去 90 天的表現超越比特幣。與此同時,短期的 Altcoin Month Index 在 30 天期間則明確高於 75 分,亮出「現在就是山寨月份!」的訊號。簡單說,在過去一個月,資金明顯轉往山寨幣,儘管長線格局還沒徹底反轉。

我們也見到典型的質性山寨幣季節前兆。其中之一是“沉睡”或“老牌”山寨幣同步暴漲,這通常意味著比特幣資金已大規模流向全體山寨。2025 年 7 月中就出現這現象:比特幣創新高且停滯後,一批資深山寨幣同步大漲。XRP(瑞波幣),因為多年的 SEC 訴訟而處於陰影,終於解決大部分法律不確定性後,火速衝上七年來首度新高,約 3.65 美元。受 XRP 帶動,其他“元老級”幣如以太坊經典(ETC)、萊特幣(LTC)、比特幣現金(BCH)等,在 7 月也出現雙位數日漲幅。這些老牌幣通常不動如山,除非市場動力出現重大切換。它們的突然回升,被專家視為“更大山寨幣季節潛在早期信號”。創投公司 Maelstrom 的投資長 Akshat Vaidya 7 月告訴 Decrypt,“老牌幣暴衝是山寨幣行情初期信號”,但他強調要等到真正的山寨季,還需看更新、更小的代幣是否全面加入。他觀察,比特幣市佔率開始自高點回落,而*“以太坊等山寨幣的資金輪動明顯展現動能集結”。* 他認為這和歷史週期相符:比特幣創高後,接下來幾個月常有山寨盛宴——換言之,加密貨幣史不斷重演。

這與我們觀察到的情形一致:以太坊領先衝鋒,其次是 XRP、LTC 等大幣,並有機會帶動剩餘山寨市場。值得注意的是,並非所有山寨幣都已起漲。許多中小型或新興專案代幣在 7 月仍較安靜,大家焦點仍在以太坊和主要大幣。部分分析師認為,這表示山寨行情屬於早期階段,尚未進入全面瘋狂。“還沒全面啟動,” 正如 Vaidya 所說。一般而言,更投機性的代幣(如小型 DeFi 代幣、新興 Layer-1、迷因幣等)往往要等大幣起完後,等交易者進一步追逐風險時才會上場;如條件繼續有利,市場可能朝這方向演化。

總結來說,當前的市場指標與專家觀點均顯示,由以太坊領軍的新一波山寨幣季節或已浮現。比特幣市佔明顯自高檔回落——目前落在五成末,這一區過往就是山寨發力期。以太坊近期明顯優於比特幣,資金輪動現象已成形。正如一位加密作家 8 月 13 日所說,「現在我們看到的不是‘Altseason’,而是‘以太坊季’。」 這也帶來一個有趣的細節:我們可能正處於「以太坊季」的特殊時刻。讓我們來深入探討這究竟意味什麼,又與傳統的山寨幣季有何不同。

以太坊季 vs 山寨幣季:ETH 獨自成派?

分析師們開始以「以太坊季」(Ethereum season)一詞來描述這種情況:以太坊不僅擊敗比特幣,也優於大多數山寨幣——成為資金輪動的最大贏家。在「以太坊季」,市場注意力和漲幅幾乎集中於 ETH;而其他規模較小的山寨幣(不含以太坊)則表現落後,或僅溫和上漲。這一觀念自 2025 年中廣受討論,因為當時大家注意到以太坊狂飆的同時,很多其他山寨幣實際上相對 ETH 是下跌的。加密分析師 Benjamin Cowen 指出:自 2025 年 4 月以來,若以 ETH 為單位,扣掉比特幣與以太坊本身那一籃山寨幣表現,平均蒸發了大約 50%。換句話說,如果你持有的是不含 ETH 的其他山寨指數,這幾個月以 ETH 計,平均都值下跌一半——這是非常慘烈的落後。Cowen 的結論是:這還不是全面山寨季,現在只是屬於以太坊的舞台。「山寨幣會有屬於它們的時刻——但目前市場的焦點,是 ETH 能否先突破 5,000 美元,」 CaptainAltcoin 的一份報告如此總結,并呼應 Cowen 看法。只要以太坊的市佔(總山寨市值中 ETH 佔比)在攀升,基本上就是以太坊主導階段。

事實上,以太坊在市值和影響力排名上持續攀升。ETH 現時約佔整個加密市場 20%(而比特幣約 55–60%);以太坊市值甚至比接下來好幾個最大山寨幣加總還高。因此,有人認為以太坊早就不再是傳統意義上的“山寨幣”,而是和比特幣並列市場兩大支柱。有些交易者甚至單獨看待 ETH。線上的迷因 「不是山寨季,是 #EthereumSeason」 正不斷流傳。circulated as ETH/BTC ratio ticks up. That ratio – which measures how many BTC one ETH is worth – is a key barometer. It has been rising off its lows, indicating Ethereum gaining on Bitcoin. As of August, ETH is around 0.038 BTC (3.8% of a Bitcoin). While that’s still below the peaks (Ethereum was ~8% of Bitcoin’s value at times in 2017 and 2021), the ratio has improved in Ethereum’s favor in recent weeks, reversing a prior trend of BTC outperformance earlier in the year.

隨著 ETH/BTC 比率上升,這一比率——即一枚 ETH 能兌換多少 BTC——成為關鍵的指標。這個比率自低點回升,顯示以太坊相對於比特幣正逐步增強。截止八月,ETH 約為 0.038 BTC(相當於比特幣的 3.8%)。雖然這還低於過往的高點(2017 年與 2021 年以太坊曾達到比特幣價值的約 8%),不過最近幾週該比率已經顯著有利於以太坊,逆轉了上半年 BTC 表現優於 ETH 的趨勢。

One consequence of an Ethereum-centric rally is that investor capital tends to flow into Ethereum-related projects more than into external alt themes. We’re seeing that play out: tokens and projects directly tied to Ethereum’s ecosystem (like Layer-2 network tokens, decentralized exchange tokens, liquid staking derivatives, etc.) have garnered interest. For example, the native tokens of Layer-2 networks Arbitrum (ARB) and Optimism (OP) have bounced from their bear-market lows as Ethereum usage grows, though so far their price gains have been modest compared to ETH’s run. Another example is Coinbase’s new Layer-2, Base, which doesn’t have a token but has attracted a flood of capital into applications built on it (like the recent social app Friend.tech that went viral). Base’s total value locked (TVL) reportedly rocketed by 9,000% in a matter of weeks, reaching about $4.5 billion, as users rushed to deploy assets on this Ethereum-aligned network. Such staggering growth underscores that much of the excitement is concentrated within the Ethereum universe – the “Ethereum-led ecosystem,” as one report calls it.

以太坊帶動的行情有一個結果:投資者資金往往更多流向以太坊本身及相關專案,而不是外部的其他山寨幣主題。我們已經看到這一現象:直接與以太坊生態綁定的代幣和專案(如 Layer-2 網路代幣、去中心化交易所代幣、流動質押衍生品等)受到關注。例如,Layer-2 網路 Arbitrum(ARB)與 Optimism(OP)的原生代幣,因以太坊用量增加而自熊市低點反彈,雖然目前漲幅仍相較於 ETH 較為溫和。另一個例子是 Coinbase 推出的新 Layer-2「Base」,雖然沒有發幣,但憑藉在其上建構的應用(如近期爆紅的社交 app Friend.tech),吸引大量資本湧入。據報導,Base 的鎖倉總額(TVL)在數週內暴增 9,000%,達到約 45 億美元,用戶爭相在這個與以太坊高度綁定的網路部署資產。如此驚人的成長凸顯了大部分熱度集中在以太坊體系內——正如某報告所稱的「以太坊主導生態系」。

During this Ethereum season, smaller altcoins measured against ETH have struggled. Cowen notes that many alt/ETH pairs have been bleeding, meaning if you held alt X instead of ETH, you’d have less ETH now than a few months ago. This dynamic could persist until Ethereum decisively breaks its all-time high and perhaps exhausts some of its momentum. Historically, what often happens is: Ethereum leads the initial phase of the alt rally, sometimes even nearly keeping pace with Bitcoin’s gains, and then once Ethereum itself hits a plateau (for instance, if ETH reaches a big psychological price like $5,000 and then consolidates), the next phase begins where capital rotates to smaller alts en masse. A similar pattern was observed in previous cycles: Ethereum would pump hard, then when it cooled, the truly manic altseason kicked off (with things like the DeFi summer in 2020 or the meme coin craze in 2021). We could be heading for a repeat. As Cowen mentioned, traders should watch the ETH/BTC trend – “as long as ETH/BTC keeps climbing, altcoins measured against BTC will likely rise too. However, ALT/ETH pairs will continue to bleed for another week or two before we get any meaningful relief bounce.” In other words, first ETH outperforms everything (Ethereum season), then eventually the smaller alts start outperforming ETH in the later stage of a full altcoin season.

在這一波以太坊行情(Ethereum season)期間,相較於 ETH 的小型山寨幣表現普遍吃力。Cowen 指出,許多山寨/ETH 交易對下跌,意味若你用山寨 X 取代 ETH,現在持有的 ETH 會比幾個月前還少。這一現象可能持續到以太坊 decisively 突破歷史新高、並消化一定動能為止。歷史上常見的模式是:以太坊先領漲主導山寨行情初期,有時甚至能跟比特幣的漲幅幾乎同步,等到 ETH 自身漲到一個平台(例如突破心理大關 $5,000 並進入盤整期),下一階段才會資金大量輪動到小型山寨幣。在過往循環中也有類似情況:以太坊衝一波,待其降溫後,真正瘋狂的 altseason(如 2020 DeFi 夏天、2021 meme 幣狂潮)才開始。我們也許正朝這一劇本前進。正如 Cowen 強調,交易者應該持續觀察 ETH/BTC 走勢——*「只要 ETH/BTC 持續上行,山寨幣相對於 BTC 也有望上漲。但 ALT/ETH 對應組合還會再 bleed 一兩週,之後才可能出現較像樣的反彈。」*換句話說,第一階段是 ETH 獨領風騷(以太坊季),最後才會進入小型 alts 表現優於 ETH 的完整 altseason 後半場。

Some market analysts have even sketched out a potential roadmap for this rotation. Crypto commentator Miles Deutscher described a three-stage cycle that could play out over months: Stage 1: An ETH-led mini altcoin season (we’re arguably in this now) where Ether rallies strongly and large-cap alts perk up. Stage 2: A rotation back into Bitcoin – he speculates that at some point Bitcoin may regain dominance and make another push (possibly toward $120k–$140k) while many altcoins lag behind. Stage 3: Finally, a “blow-off” altcoin rally where capital floods back into Ethereum and then into smaller tokens, marking the cycle’s speculative peak. Under this scenario, the true broad altseason might still be ahead, after a potential interim Bitcoin run. Whether or not things unfold exactly in that sequence, the key takeaway is that Ethereum’s strength is a necessary ingredient for a broader altcoin season, but it might not immediately translate into across-the-board altcoin gains until a bit later. For now, Ethereum is in the driver’s seat.

部分市場分析師甚至為這種輪動提出了可能的路線圖。加密評論員 Miles Deutscher 描述了一個可能持續數月的三階段循環:第一階段,由 ETH 領漲的小型山寨行情季(目前我們大概就處於這一階段),以太坊大幅拉升,巨頭山寨也跟著上行。第二階段,資金再度回流至比特幣——他推測某個時間點比特幣將重奪主導地位,又會有一波衝刺(甚至可能奔向 $12 萬~$14 萬),而大多數山寨幣則相對落後。第三階段,則是一波*「終極瘋漲」*的山寨幣行情,資金回流以太坊再湧向小型代幣,宣告本輪投機高峰。在這種情景下,廣義的 altseason 可能還沒來臨,還需經過比特幣的階段性行情。儘管未來是否真的如此發展仍有變數,重點在於以太坊的強勢是開啟更廣泛山寨行情的必備條件,但這種力量未必馬上讓整體山寨幣同漲。就目前來看,以太坊才是主角。

It’s also worth considering how sentiment and risk appetite differ in an Ethereum-led phase versus a typical alt free-for-all. When Ethereum is the focus, it suggests the market mood is bullish but still somewhat measured – investors are putting money into what is arguably a “safer” big-cap crypto with fundamental support. Ethereum has institutional buyers, real usage, and comparatively lower risk than tiny altcoins. An “Ethereum season” implies confidence in crypto’s medium-term outlook, but not blind speculation on every token. Once we transition to a full altseason, usually the psychology shifts to a more euphoric, risk-blind chase of any coin that’s moving (we saw that with dog-themed coins in 2021, etc.). There are early signs of increasing speculative appetite – for example, mentions of obscure altcoin tickers popping up more on forums, and some relatively new projects (like Sui or Sei, which are new layer-1 chains) popping 20-30% in a day. But overall, the market in August 2025 still seems to be placing its biggest bets on Ethereum and a handful of top players. As one trader on X (Twitter) put it, “We’re seeing early signals of an altcoin season... It could very well be that history repeats, with a post-BTC all-time high altseason. But you’ll have to wait for a true altseason to see newer coins pump”.

值得注意的是,以太坊帶頭的階段與典型全面山寨交投熱潮下,市場情緒與風險偏好其實有所不同。以太坊成為焦點時,說明市場雖然偏多但相對理性——投資人選擇有基本面支撐、機構買盤、大規模應用、風險相對較低的大型主流幣。這種「以太坊季」意味著投資人對中期前景有信心,但還沒到盲目追投每一枚幣的情緒。轉入完整版 altseason 後,市場心理才會變得極度亢奮、不計風險地追逐一切上漲幣種(如 2021 年狗狗幣題材)。目前投機偏好已有初步升溫——例如有些冷門幣 ticker 在論壇被頻繁提起,還有一些較新(如 Sui 或 Sei 屬於新 layer-1)的項目一天內上漲 20-30%。但整體來看,2025 年 8 月的市場仍將最大籌碼押注於以太坊及少數頭部項目。如同一位 X(Twitter)上的交易者所說:「我們已經看到 altseason 的早期訊號……歷史可能會重演,等 BTC 創新高之後就會有真正的 altseason。但你得再等等,等到真的 altseason 來臨,才會看到新幣噴發。」

For the average crypto participant, the implications are clear: Ethereum is currently providing leadership and relative stability, and many are eyeing ETH’s milestones (like the all-time high near $4.8k, and the big $5,000 level) as the next pivotal moments. If Ethereum decisively breaks into price discovery above its old peak, it could trigger a wave of FOMO (fear of missing out) and a shift into “full risk-on mode” across crypto. Until then, it remains “Ethereum season.” As Petar Jovanović wrote on August 13, the market’s eyes are on ETH hitting $5K, and “for now, this is still very much Ethereum season. Altcoins will have their time – but [first] the market’s eyes are on ETH...”.

對多數加密市場參與者而言,意義非常明確:目前是以太坊帶頭、提供相對穩定的行情,許多人都將 ETH 的關鍵里程碑(如歷史高點 $4.8k 及大關 $5,000)作為下一步關鍵觀察重心。若 ETH 強勢突破歷史高點進入新一波價格發現,將可能引爆 FOMO(錯失恐懼症)及全市場*「全面風險開啟」。在這之前,還是「以太坊季」。正如 Petar Jovanović 8 月 13 日所說,目前市場注目 ETH 衝擊 $5K,「現在確實完全屬於以太坊季。山寨遲早有機會——但目前,全市場眼光都在 ETH 身上...」*

Speaking of Ethereum-centric growth, one area tightly interwoven with Ethereum’s success is the Layer-2 scaling sector. Ethereum’s rally and heavy usage directly impact Layer-2 networks that help carry its load. Let’s examine how an Ethereum-led altcoin season (or “Ethereum season”) might play out for those Layer-2 solutions and what changes we’re seeing in network usage patterns.

談到以太坊驅動的增長,有一個與其成敗密不可分的領域:Layer-2 擴容解決方案。ETH 漲勢及高用量會直接帶動承擔其負載的 Layer-2 網絡。我們來探討一下,以太坊主導的 altcoin season(以太坊季)如何影響這些 Layer-2 解決方案,以及我們正在看到的網路使用行為變化。

Layer-2 Networks in an Ethereum Boom: Scaling Up for the “Season”

One of the most significant developments since the last crypto cycle is the rise of Ethereum Layer-2 networks – secondary blockchains or rollups that extend Ethereum’s capacity by processing transactions off the main chain (Layer 1) and then settling results back to it. In 2021, high traffic on Ethereum meant sky-high fees and a poor experience for many users. By contrast, here in 2025, Ethereum’s bull run is occurring in tandem with unprecedented Layer-2 adoption, fundamentally changing how a new altcoin season could unfold. In short, if “Ethereum season” comes true and usage explodes, Layer-2 networks are poised to absorb much of that activity, keeping the system more scalable and efficient than in past booms.

自上個加密牛市以來,最重大發展之一就是以太坊 Layer-2 網路的崛起——這些二層鏈或 rollup 方案將交易於主鏈(Layer 1)之外處理,然後再回寫到主鏈結算,藉此擴展以太坊的容量。2021 年以太坊網路淤塞,導致手續費飆升、用戶體驗惡劣。相比之下,2025 年這波以太坊多頭卻與前所未有的 L2 採用率同步進行,根本上改變新一輪 altseason 的展開方式。簡言之,若這次「以太坊季」真如預期爆發,Layer-2 網路將吸收大量交易流量,使系統延展性與效率遠優於過去的牛市高峰。

The numbers are revealing: as of mid-2025, it’s estimated that over 85% of all Ethereum ecosystem transactions now occur on Layer-2s rather than the Layer-1 chain. In other words, the vast majority of individual user transactions (like token swaps, NFT trades, game interactions, etc.) are happening on networks like Arbitrum, Optimism, Base, zkSync, and others that piggyback on Ethereum’s security. Meanwhile, Ethereum L1 continues to do what it does best – act as the settlement and security layer for big value transfers. It still processes about 85% of all the value moved (since large transfers, whales moving funds, and final settlements often occur on L1). Ethereum L1 also holds the lion’s share of assets: around 90% of all stablecoin value and over 80% of tokenized real-world assets in crypto are on Ethereum mainnet. So Ethereum is evolving into a two-tier system: Layer-1 as the high-value backbone, and Layer-2 as the high-volume workhorse for everyday transactions.

數據也說明了一切:截至 2025 年中,估計以太坊生態系統 85% 以上的所有交易都發生在 Layer-2,而不是主網 Layer-1。換言之,絕大多數用戶的日常交易(例如代幣兌換、NFT 買賣、鏈遊互動等)都在 Arbitrum、Optimism、Base、zkSync 等這些依附以太坊安全性的網路上完成。與此同時,以太坊主網(L1)仍專注於高價值的結算與安全職能,繼續處理約 85% 的總價值流動(主要因大額轉帳、巨鯨資金調度與最終結算多仍發生在 L1)。主網也持有大部分資產——全體穩定幣價值約九成、超過八成的鏈上 RWA 代幣都在以太坊主網。所以以太坊逐漸演化成雙層結構:Layer-1 負責高價值骨幹,Layer-2 撐起日常高頻交易。

This shift has been supercharged by recent technical upgrades. In late 2024, Ethereum implemented the “Dencun” hard fork (which includes the EIP-4844 upgrade, also nicknamed Proto-Danksharding). Dencun introduced so-called “blobs” of data that Layer-2 rollups can use to post transactions to Ethereum at very low cost. The result was a drastic reduction in the cost for L2s to write data to L1 – essentially cutting their operating costs by an order of magnitude. One report noted that after Dencun, data settlement costs became “near-zero” for L2s, allowing some like Coinbase’s Base network to operate with over 98% profit margins on its transaction fees. With such low costs, L2s can keep user fees extremely cheap (often just pennies per transaction) and still be sustainable businesses. This has made Layer-2s far more attractive to users, driving a virtuous cycle of adoption. For example, on decentralized exchanges (DEXs), the number of trades on L2 more than doubled year-over-year by May 2025, and that month Base even surpassed Ethereum L1 in total DEX trading volume – a remarkable milestone. It shows that users, when given the option, will happily trade on a faster, cheaper L2 venue while relying on Ethereum’s security assurances in the background.

這種轉變大幅受到近期技術升級的推動。2024 年底,以太坊實施「Dencun」硬分叉(包括 EIP-4844 升級,即 Proto-Danksharding)。Dencun 引入了「blobs」數據結構,讓 Layer-2 rollup 能以極低成本將交易資料寫回以太坊主鏈。結果,L2 寫入主網的成本呈數量級下滑,一份報告甚至指出,Dencun 之後,L2 資料結算成本近乎於零,使 Coinbase 旗下的 Base 等網路能以高達 98% 以上的交易費用毛利率運作。低成本讓 L2 能將用戶手續費壓至極低(一筆交易僅需幾美分),同時維持可持續的商業模式。這讓 Layer-2 對用戶吸引力大幅提升,形成良性循環。例如,在去中心化交易所(DEX)領域,2025 年 5 月 L2 上的交易筆數年增一倍以上,Base 當月甚至首次超越以太坊主網成為 DEX 總交易量最大的平台,意義深遠。這顯示,只要有更快更便宜的選項,絕大多數用戶樂於在 L2 交投,同時信賴以太坊背後的安全性。

So, if Ethereum usage surges further in an altcoin season, Layer-2 networks are ready to carry the extra load. We’re already seeing them step up. Base, the newcomer L2 incubated by Coinbase, has made headlines with its explosive growth. Within just a few months of launch, Base reportedly saw a 9,000% increase in total value locked, reaching about $4.5B TVL, thanks in part to popular new dApps launching there. Base has also become the dominant L2 by some measures: by May 2025 it was accounting

因此,如果以太坊的使用量在這輪山寨行情中再爆發,Layer-2 網路已經整裝待發,準備承載更大負載。我們已經看到它們開始接手這一重任。由 Coinbase 孵化的新晉 L2「Base」以爆炸性增長成為焦點。據悉,Base 上線短短數月,鎖倉總額激增 9,000%,突破約 45 億美元,部分歸功於在其上推出的熱門新 dApp。Base 也逐漸成為某些指標下的主導 Layer-2:截至 2025 年 5 月,該網路已佔...for over 80% of all L2 transaction fees and generating nearly $6 million in monthly revenue (suggesting very high usage). Some of that activity is driven by hype cycles (like Base’s ecosystem had a frenzy of meme coin trading and a new social app), but importantly, it demonstrates the scalability of Ethereum’s broader network. At one point, Base alone handled more transactions than the entire Ethereum mainnet, and combined, L2s routinely process many times the throughput of L1. Despite that, Ethereum L1 itself has not buckled – its block utilization is around 50%, fees are moderate, and it’s serving its role as final settlement.

跳過 markdown 連結的翻譯。

超過 80% 的所有 L2 交易手續費都是由其產生,並且每月創造近 600 萬美元的收入(顯示出非常高的使用率)。這當中有部分活動來自炒作循環(例如 Base 生態發生過迷因幣交易熱潮和新社交應用程式),但更重要的是,這證明了以太坊整體網絡的可擴展性。有一度,僅僅 Base 就處理的交易量超過整個以太坊主網,而整體來看,L2 通常可以實現 L1 多倍的吞吐量。即便如此,以太坊本身依然穩健——區塊利用率只有約 50%,手續費屬於中等水準,並且持續發揮最終結算層的作用。

What does this mean for a potential altcoin season led by Ethereum? It means the next altcoin frenzy might look and feel different for participants. In 2017, if you tried to buy a hot ICO token, you probably did it on Ethereum L1 and paid high gas fees (or the network lagged). In 2021, trading DeFi tokens or minting NFTs on Ethereum became prohibitively expensive at peak times, pricing out smaller users. In 2025, Layer-2s offer an outlet to handle a surge of transactions without congesting Ethereum mainnet. If millions of new users rush into crypto chasing altcoin gains, they can be onboarded via L2s where they’ll experience low fees and fast confirmations, all while ultimately being secured by Ethereum. This is likely to encourage even more activity, as the usual brake on altcoin manias – e.g. $50 or $100 transaction fees on Ethereum making small trades uneconomical – is far less of an issue now. So an altcoin season in the Layer-2 era could potentially be more intense and involve even higher transaction counts than previous ones, since the capacity is so much greater. It also means that the benefits will accrue back to Ethereum: every trade on Arbitrum or Base still ultimately uses ETH (for paying L2 fees, which eventually consume ETH on L1) and showcases Ethereum’s platform effect.

這對於一場可能由以太坊領頭的山寨幣季節意味著什麼?這表示下一波的山寨幣熱潮,對參與者來說體驗可能會大不相同。2017 年時,若你想買熱門的 ICO 代幣,大概得在以太坊 L1 上進行,並且支付高昂的 Gas 費(或網路延遲);2021 年,在高峰時刻於以太坊上交易 DeFi 代幣或鑄造 NFT,成本高得離譜,讓許多小額用戶被排除在外。到了 2025 年,Layer-2 成為應對交易激增的出口,卻不會塞爆以太坊主網。若有數百萬新用戶湧入加密市場追逐山寨幣收益,他們可以直接從 L2 上車,享受低手續費和快速確認,同時最終還是受到以太坊安全性的保障。這極可能激發更多活動,因為以往山寨幣熱潮遇到最大阻力——如以太坊 $50 或 $100 一筆的手續費讓小額交易變得不划算——現在這問題已大幅減輕。因此,Layer-2 時代的山寨幣季節有可能更加猛烈,交易筆數甚至遠超以往,因為容量大得多。此外,這些紅利最終會回饋到以太坊本身:在 Arbitrum 或 Base 做的每一筆交易,最終仍需用 ETH 支付(L2 手續費最後消耗 L1 的 ETH),同時展現以太坊的平台效應。

Layer-2 tokens and ecosystems might themselves become part of the altcoin season story. Many L2 networks launched tokens (Arbitrum’s ARB, Optimism’s OP, etc.) and those could rally if speculation turns their way. So far, the performance of L2 tokens has been somewhat underwhelming – for instance, ARB trades below its initial airdrop price as of August, even though Arbitrum is one of the top rollups by usage. Some traders attribute this to the fact that these tokens are mainly governance tokens (not required for using the network, aside from maybe paying fees in some cases), so their value isn’t directly tied to usage. However, in a euphoric market, fundamentals often take a backseat to narrative. If Ethereum is soaring and people are looking for the “next Ethereum,” they might bid up L2-related projects or DeFi protocols running on L2s, expecting them to catch up. Already, we saw hints of this: when Ethereum’s price blasted past $4,200, optimism spread to smaller-caps and one report noted “smaller-cap altcoins follow ETH’s bullish trajectory”. It cited that Ethereum’s rally was “triggering broader market participation”, implying traders were starting to branch out beyond just ETH.

Layer-2 代幣和生態體系本身可能也會成為這次山寨幣季節的主角之一。很多 L2 網絡已經發行代幣(如 Arbitrum 的 ARB、Optimism 的 OP 等),若市場情緒轉向,這些代幣有望迎來一波行情。迄今為止,L2 代幣表現尚稱平平——比如 ARB 到 8 月都跌破最初空投的價格,儘管 Arbitrum 是使用者數一數二的 rollup。有些交易者認為,這些代幣主要是治理代幣(除部分手續費,並非必要用於網絡操作),因此價值不直接和使用綁定。不過,市場狂歡時,基本面常常輸給敘事熱潮。如果以太坊飆漲,人們尋找「下一個以太坊」時,就可能熱炒 L2 相關項目或在 L2 上運行的 DeFi 協議,期待他們補漲。事實上我們早已見到這種苗頭:每當以太坊突破 $4,200,大盤樂觀氛圍很快蔓延到小型幣種,有報導指出 「小市值山寨幣跟隨 ETH 上漲」。報告還稱,以太坊的上漲 「帶動更廣泛的市場參與」,暗示交易者開始不只盯著 ETH 了。

Moreover, specific success stories on L2s can create mini-seasons of their own. For example, if a certain DeFi application on a Layer-2 becomes the hot thing (much like how Compound or Uniswap kick-started DeFi Summer on Ethereum in 2020), it could drive a lot of new users and capital to that L2. We’ve already seen early examples: the friend.tech social token platform launched on Base in August 2023 brought a surge of transactions and fees to Base. In the current climate, any viral dApp on an L2 can direct attention (and token value) to that layer. This adds another dimension to altcoin season: not only do we consider which coin, but also on which chain the activity is happening. Right now, Ethereum and its Layer-2s form a kind of interconnected megasystem, and collectively they dominate many sectors (DeFi TVL, NFT trading, on-chain stablecoins, etc.). As noted earlier, Ethereum hosts 58% of all tokenized assets across all chains – by far the largest share. So if we indeed get a roaring alt season, much of that could play out on Ethereum mainnet and L2s, reinforcing Ethereum’s position. It’s telling that even after all the growth of rival blockchains in recent years, Ethereum still anchors the majority of on-chain economic activity in categories like stablecoins and real-world asset tokens.

此外,L2 上的個別爆紅案例也可能帶動自己的小型熱潮。例如,如果某款 Layer-2 上的 DeFi 應用程式像當年 Compound 或 Uniswap 引爆 2020 年以太坊的 DeFi Summer 一樣走紅,那麼將有大量新用戶與資本湧向該 L2。我們已見過類似範例:friend.tech 社交代幣平台於 2023 年 8 月在 Base 啟動,帶來 Base 交易與手續費暴增。現今時代,任何在 L2 爆紅的 dApp 都能為那一層吸引關注(及帶來代幣價值)。這讓山寨幣季節多了全新視角:我們不僅得考慮哪一顆幣,還得看在哪一條鏈發生。當下,以太坊與其 Layer-2 形成一個相互聯繫的巨型系統,聯手主導多數領域(如 DeFi TVL、NFT 交易、鏈上穩定幣等)。如先前提到,以太坊掌握全鏈 58% 的代幣化資產——遠高於其他鏈。因此,若真有豪邁的山寨幣季節降臨,許多活動都會在以太坊主網及 L2 發生,加強以太坊地位。值得注意的是,儘管近年競鏈發展迅猛,以太坊在穩定幣和實體資產等關鍵領域仍穩坐最大鏈中心。

One potential challenge with L2s during a frenzy is bridging and liquidity fragmentation. Users have to move assets between Ethereum L1 and various L2s (and possibly other L1s). In a fast-moving market, bridges can become bottlenecks or points of risk (hacks, delays). However, infrastructure has improved here too, with many fast bridges and decentralized bridge protocols now in place to shuttle funds around quickly. If Ethereum fees do spike at the absolute peak of usage, some chaos could ensue with moving funds, but likely far less severe than in past cycles thanks to advance planning and multiple options (e.g., you can always trade on a different L2 instead of rushing back to L1).

L2 熱潮下的一個潛在挑戰是橋樑和流動性碎片化。用戶必須在以太坊主網與各 L2(甚至其他公鏈)間移動資產。在節奏極快的市場裡,跨鏈橋有機會變成瓶頸或隱含風險點(如駭客、延遲)。不過,這方面基礎設施也明顯進步,當前已出現許多快速橋與去中心化橋協議,能以高速在鏈間搬運資產。如果以太坊主網手續費在使用高峰時劇烈飆升,資金移轉過程或許會出現亂象,但由於有提前規劃與多元選擇(如可直接在其他 L2 交易,不需急著回到 L1),情況應該比前幾輪牛市會緩和許多。

In essence, Layer-2s ensure that an Ethereum-led altcoin season can be bigger and more accessible than ever. They allow the excitement to scale. For average users, this means you might experience the next altcoin boom through networks like Arbitrum or Base without even touching Ethereum mainnet directly – yet Ethereum will still be the underlying security blanket making it all possible. It also means the narrative of Ethereum being the “backbone of future finance” is validated in real time: while Bitcoin sits largely in wallets as digital gold, Ethereum’s network (with its L2 extensions) is bustling with activity, trade, and innovation even at peak times.

總結來說,Layer-2 確保了由以太坊主導的山寨幣季節可以比以往更大、更普及,讓熱潮有機會無限擴展。對一般用戶而言,這代表下波山寨幣繁榮也許可以直接透過 Arbitrum、Base 等 L2 網路參與,甚至連主網都不用碰,但底層的安全保障仍來自以太坊。此外,「以太坊是未來金融主幹」的敘事也在現實中得到驗證:比特幣大多安靜地當數位黃金躺在錢包中,而以太坊生態(包含 L2 擴展)即使在頂峰期仍然活躍、充滿交易與創新。

From an investment standpoint, one might conclude that if you believe an altcoin season is coming, betting on Ethereum and its ecosystem could be a relatively safer way to capture that upside. This is something even prominent analysts have suggested. Veteran trader Michaël van de Poppe commented that while Ethereum’s rapid rise to $4,200 was a “wild move” and chasing it at those highs carries risk, allocating capital to projects within the ETH ecosystem might deliver better percentage returns if momentum continues. His rationale is that smaller projects related to Ethereum (like certain L2 tokens or DeFi protocols) could see outsized gains once the rally broadens, potentially outpacing even ETH, but they are still tethered to Ethereum’s success. In other words, if you’re bullish on ETH, there are leveraged ways within its orbit to express that – though of course with higher risk.

從投資角度來看,如果你相信山寨幣季節即將來臨,部署資本在以太坊及其生態系統可能會是一種相對更安全的吃紅利途徑。這也是不少知名分析師曾提出的觀點。資深交易員 Michaël van de Poppe 指出,以太坊一路急升至 $4,200 是個「瘋狂的舉動」,如今追高風險極高,但如果熱度延續,把資本分配到 ETH 生態項目或許更有機會拿到更高百分比報酬。他的理由是,與以太坊相關的小型項目(如某些 L2 代幣或 DeFi 協議),一旦行情展開,有望跑贏 ETH 本身,但最終仍依賴以太坊成敗。換句話說,看好 ETH 的人,其實可以在其生態圈內用「槓桿」形式參與,只不過風險相對更高。

To summarize, Layer-2 networks stand as critical infrastructure and likely beneficiaries of an Ethereum-led market rally. If Ethereum truly leads a new altcoin season, expect L2 usage to set fresh records as users flock to cheaper platforms to trade and invest. Already, by mid-2025, L2s handle the majority of transactions (85%+) in the Ethereum ecosystem. That trend will only intensify if the pace of speculation picks up. The endgame envisioned by many Ethereum proponents – where the main chain is a secure settlement layer and most activity happens on L2s – is basically happening now. An altcoin season will test just how far this “modular” approach can go in accommodating a tidal wave of demand. All signs so far are encouraging: the network has headroom, fees are low, and upgrades like Dencun have done their job in supercharging capacity. For traders and developers, it’s an exciting prospect: a bull run without the same bottlenecks and pain points as last time.

總而言之,Layer-2 網絡堪稱關鍵基礎建設,也是以太坊主導行情下的最大受惠者之一。若以太坊真的領軍新一輪山寨幣季節,L2 用量勢必再創新高,因用戶會蜂擁至手續費更低的平台投資與交易。到了 2025 年中,L2 已承擔以太坊生態 85% 以上的交易,未來若投機節奏加快,這趨勢只會更加明顯。許多以太坊倡議者所描繪的終極畫面——主鏈作為安全結算層、大部分活動移轉至 L2——基本上正在發生。山寨幣季節將檢驗這種「模組化」架構能否承載海量需求。目前一切訊號皆相當正面:網路容量有餘裕,手續費低廉,Dencun 這類升級也顯著擴增產能。對於交易者與開發者而言,這意味著有望迎來一場比前幾輪牛市少了許多痛點與瓶頸的上漲行情。

Of course, no rally is without risks. It’s important to temper excitement with an understanding of what could go wrong or throw the market off course. In the final section, we’ll look at the key risks and uncertainties that could affect Ethereum’s trajectory and the broader altcoin season thesis.

當然,沒有任何一場行情是沒有風險的。我們應該冷靜看待這波熱潮,認清有哪些潛在問題可能導致行情破滅或脫軌。最後,我們將探討哪些關鍵風險與不確定性可能影響以太坊的走向,以及整個山寨幣季節的命運。

Risks and Challenges: Caution in the Midst of Euphoria

風險與挑戰:狂熱之中需謹慎

While the current outlook for Ethereum and altcoins is undeniably optimistic, it’s crucial to acknowledge that the crypto market remains highly volatile and laden with risks. History has shown that roaring rallies can reverse suddenly, and new challenges can emerge just when things seem most bullish. Here are some of the key risks and factors to watch as we evaluate whether Ethereum will successfully lead a sustained altcoin season:

雖然當下以太坊與山寨幣的前景無疑非常樂觀,但我們不可忘記,加密市場本質上波動劇烈且充滿風險。歷史告訴我們,猛烈的牛市可以在一夜間反轉,當一切看似最美好之際,新的挑戰也能突然殺到。以下是我們評估以太坊能否成功帶領長線山寨幣季節時,必須關注的一些主要風險與因素:

-

Overheating and Pullbacks: Rapid price appreciation often sows the seeds of its own correction. As Ethereum hovers near all-time highs, some traders are growing wary of a short-term pullback. Profit-taking by short-term holders is already on the rise according to on-chain data. We saw a glimpse of this when ETH briefly hit $4,600 – shortly after, there was a bout of selling as speculators locked in gains, causing minor dips. Market sentiment indicators also flash warnings; Santiment noted that bullish chatter spiked dramatically as ETH crossed $4k, which can signal overconfidence. In strong uptrends, pauses or corrections are healthy and expected. Even staunch bulls urge caution about “buying at such elevated levels” without a plan. We should remember that after Ethereum’s previous peak in 2021, it suffered multiple 20-30% corrections on the way up and much larger ones in the subsequent bear market. A sudden macro scare or a wave of deleveraging could easily cause ETH to retrace a chunk of its gains in the short run. Such a pullback, if it happened, might temporarily stall any budding altcoin season because a sharp ETH drop would likely shake the entire market.

-

過熱與回調:價格快速上漲,往往埋下自己修正的種子。當以太坊在歷史新高附近徘徊時,不少交易者已開始警惕短線回檔。根據鏈上數據,短線持有者獲利了結的情形明顯增加。當 ETH 一度衝上 $4,600 時,旋即出現一波拋售潮,投機者鎖定獲利引發小幅回落。市場情緒指標同樣亮起警訊:Santiment 指出,ETH 突破 $4,000 時看多言論暴增,這可能意味著過度自信。強勢上升趨勢中,暫停或修正屬於健康且正常現象。即使最堅定的多頭也提醒切勿「在高檔盲目追高」,應該有計畫地行動。回想 2021 年以太坊上波高點,途中就經歷數次 20-30% 的修正,熊市中跌幅更大。新一波宏觀風險或去槓桿浪潮,很可能讓 ETH 短期內回吐部分漲幅。若真出現這種回調,恐將暫時壓抑剛萌芽的山寨幣季節,因為 ETH 暴跌通常會動搖整體市場。

-

Institutional Overleverage: One of the new risk factors in this cycle, as highlighted by none other than Vitalik Buterin, is the possibility of institutions overextending themselves with Ethereum. The fervor around Ethereum ETFs and corporate treasury accumulation, while positive, can have a dark side if not

-

機構過度槓桿:這一輪行情中新出現的風險因素之一,正是 Vitalik Buterin 本人提到過的——機構可能在以太坊上過度槓桿。圍繞以太坊 ETF 和企業庫存累積的熱潮,雖然看起來正面,但如果未能...(內文未完)managed prudently. Vitalik cautioned in August that the trend of corporations buying up ETH for their treasuries and staking yields could turn into an “overleveraged game.” What did he mean by this? Essentially, if companies or funds are borrowing money to buy ETH (leveraging their positions) or if ETF providers are utilizing derivatives extensively to meet demand, it introduces the risk of a cascade. Imagine if ETH’s price fell sharply – those same institutional players might face margin calls or risk controls that force them to sell into a falling market. Jamie Elkaleh echoed this concern, warning that overleveraging by corporate treasuries could destabilize the ecosystem, especially if forced liquidations trigger cascading sell-offs. This scenario is somewhat analogous to past incidents in crypto (for instance, the leveraged unwinding of positions that contributed to 2021’s mid-cycle crash or even the 2022 collapse of players like Terra/Luna, albeit that was more DeFi-centric). While there is no immediate sign of crisis – corporate holdings are still a fraction of ETH supply – it is a risk factor that grows as more big players pile in. The saving grace is that many of these institutional holders claim to be long-term oriented. But sentiment can change quickly if, say, a major ETF sees outflows or a big fund decides to trim exposure.

謹慎管理。Vitalik 在八月警告,目前企業為了庫存買入 ETH 並進行質押獲取收益的趨勢,可能演變成一場*「過度槓桿的遊戲」。這句話是什麼意思?簡而言之,如果公司或基金為了買 ETH 而借錢(槓桿操作),或 ETF 發行商大量使用衍生性商品來滿足需求,就會帶來連鎖風險。想像一下,如果 ETH 價格暴跌,這些機構投資人可能會遇到追加保證金或風控機制,被迫在跌市賣出,形成惡性循環。Jamie Elkaleh 也同樣擔憂,警告企業財務部門如果過度槓桿,可能會動搖整個生態系,尤其是在強制平倉引發連環拋售時。這種情景在過去的加密貨幣事件中也曾發生(比如 2021 年周期中段因槓桿爆倉導致的崩盤,或者 2022 年 Terra/Luna 等玩家倒閉,儘管那件事較偏去中心化金融領域)。雖然現在還沒有立即的危機跡象——企業持有的 ETH 佔供給量其實還很少——但這是一個會隨大戶玩家湧入而提高的風險因素。好消息是,許多機構持有者聲稱他們是長期*持有者。但如果像某大型 ETF 發生資金淨流出、或大基金決定降低曝險,市場情緒也能瞬間反轉。

-

Regulatory and Legal Risks: The regulatory climate has improved, but it’s not without remaining hazards. In the U.S., the SEC has thus far only approved futures-based Ethereum ETFs, not a spot ETF. There is optimism that a spot Ether ETF could eventually get greenlit (especially given Grayscale’s recent legal win for a Bitcoin ETF), but no guarantees. If regulators were to push back or if some negative ruling emerged – for example, classifying certain Ethereum-based yield products as securities – it could chill institutional enthusiasm. Globally, regulations on crypto taxation, exchange licensing, or stablecoins could indirectly impact Ethereum usage. One specific area to watch is stablecoin regulation: Ethereum heavily relies on stablecoins like USDT and USDC as its liquidity engine in DeFi. The GENIUS Act progressing in Congress aims to regulate stablecoin issuance. If mishandled, new rules could affect stablecoin availability, which in turn would affect trading volumes on Ethereum. Additionally, Ethereum’s status as not a security is generally accepted in the U.S. now (the SEC’s focus has moved elsewhere), but were that ever to be challenged, it’d be a huge blow. European and Asian regulators are mostly positive on ETH, but one should keep an eye on any nation that might curtail crypto activity (for instance, if a major economy limited crypto trading, it reduces global liquidity).

-

法規與法律風險:監管環境雖已改善,但仍存在不少潛在風險。在美國,目前 SEC 僅批准了以期貨為基礎的以太坊 ETF,尚未通過現貨 ETF。儘管大家對現貨以太 ETF 最終獲批感到樂觀(特別是考慮到 Grayscale 最近在比特幣 ETF 官司的勝利),但沒有任何保證。如果監管機構態度轉向,或有不利於加密產業的裁決出現——例如將某些以太坊收益產品認定為證券——都可能澆熄機構熱情。國際上,不論是加密貨幣稅制、交易所執照、或穩定幣法規等都可能間接影響以太坊應用。特別要注意的是穩定幣規範:以太坊在 DeFi 裡高度依賴 USDT、USDC 等穩定幣作為流動性引擎。美國國會推行中的 GENIUS Act 旨在規管穩定幣發行。如果處理不當,新規則可能衝擊穩定幣供給,進而影響以太坊上的交易量。此外,雖然現在美國普遍認為以太坊不屬於證券(SEC 重心已不在 ETH),但萬一未來這一地位遭質疑,將是巨大打擊。歐亞地區監管大多對 ETH 持正面態度,但大家還是得注意是否有國家限制加密業務(例如某主要經濟體禁止加密交易,全球流動性就會減少)。

-

Macro Economic Shifts: The macroeconomic tailwinds that currently favor crypto could shift direction. Markets are pricing in interest rate cuts and a soft landing for the economy. However, if inflation were to unexpectedly roar back or if the Federal Reserve changes its stance to a more hawkish tone, risk assets like crypto could see renewed pressure. One cannot rule out macro surprises – e.g., an economic slowdown that’s sharper than anticipated or a credit event in traditional markets – that cause investors to reduce exposure to volatile assets. In such scenarios, Bitcoin tends to outperform altcoins (investors retreat to the relative safety of BTC or to cash), which would put a quick end to an altcoin season. So far in 2025, the macro signs are benign, but this is a variable largely outside crypto’s control.

-

宏觀經濟變化:目前有利加密貨幣的宏觀經濟順風可能會轉向。市場普遍預期降息與經濟軟著陸,但如果通膨意外回升、或聯準會政策轉鷹,風險性資產如加密貨幣可能重新承壓。另不可排除其他宏觀意外,例如經濟衰退超預期或傳統市場出現信用事件,致使投資人縮減高波動性資產部位。在這類情境下,比特幣往往優於山寨幣(投資人轉向 BTC 或現金避險),山寨季也容易戛然而止。2025 年目前宏觀環境氣氛尚穩,但這始終是加密圈難以控制的變數。

-

Security and Technical Hurdles: Ethereum’s core infrastructure has proven resilient through the Merge and subsequent upgrades, but rapid growth can sometimes reveal technical bottlenecks or vulnerabilities. One example is the risk associated with bridges connecting Layer-2s and other chains. In past years, bridge hacks have led to significant losses. If an altcoin season intensifies and more value flows through multi-chain bridges, they become juicy targets for attackers. A major hack or exploit (whether on a DeFi protocol or a cross-chain bridge) could momentarily spook the market and dent confidence in the ecosystem’s safety. Ethereum itself hasn’t had a catastrophic technical failure in a long time (the last major incident was the DAO hack and chain split in 2016, which gave birth to Ethereum Classic), and it’s battle-tested at this point. But one should always consider tail risks – for instance, what if a critical bug were found in a popular Layer-2’s code, forcing a pause or rollback? Such an event could freeze activity and impact prices. The Ethereum core developers are also planning future upgrades (like the Verge, Purge, etc. in the roadmap); while none seem likely to destabilize things, any complex software rollout carries risk.

-

安全與技術障礙:以太坊主體基礎設施已通過合併與多次升級的考驗,但快速增長下也可能暴露技術瓶頸或漏洞。例如跨 Layer-2 或跨鏈的橋(bridge)存在安全風險,過去幾年橋被駭事件屢見不鮮造成鉅額損失。若山寨季熱度高昂、更多資金流過多鏈橋,這些橋就會變成駭客的肥羊。一旦出現重大駭客行動或漏洞(無論是在 DeFi 協議還是跨鏈橋),都可能短暫嚇壞市場,侵蝕生態系安全信心。以太坊本身已許久未出現災難性技術事故(上次是 2016 年的 DAO 駭客與分鏈事件,誕生了以太坊經典,以後就屢經戰火驗證)。但還是要考慮極端尾部風險——比如某熱門 Layer-2 出現重大 bug,必須暫停甚至回滾?這類事件可能造成交易凍結並衝擊價格。以太坊核心開發團隊也在規劃更多未來升級(如 Verge、Purge 等),雖不大可能動搖系統,但任何大型軟體升級都有潛在風險。

-

Market Psychology and Timing: There’s a saying: “By the time everyone calls it altcoin season, it’s almost over.” Markets are forward-looking and often contrarian. If sentiment becomes unanimously convinced that altcoin season is here and will persist, that’s when one must be most cautious. We’ve started to see mainstream financial media pick up on Ethereum’s rally and altcoin chatter. A sudden flood of retail FOMO, while initially boosting prices, could create a blow-off top scenario. Already, some analysts are issuing lofty price targets – for example, Fundstrat’s Tom Lee recently predicted Ethereum could reach $16,000 by year-end 2025 if macro tailwinds hold and derivatives demand persists. Prediction markets give about a 74% probability that Ethereum will hit a new all-time high in 2025. These are optimistic odds. If everyone is positioned for more upside, the market can become fragile to any disappointment. It’s possible the altcoin season, if it fully materializes, might be short and intense, as these periods often are. Timing exits is notoriously hard – many retail investors got caught when the music stopped in previous cycles, holding bags of altcoins that plunged in value.

-

市場心理與時機掌握:有一句話說,「當大家都喊山寨季來了,其實快結束了。」市場本就前瞻、甚至逆向操作;當市場情緒一致認定山寨季來臨且會持續時,反而要最小心。主流財經媒體已開始關注以太坊與山寨幣熱潮。散戶一旦 FOMO 湧入,最初雖推升價格,卻也可能堆疊形成爆量見頂風險。目前部分分析師已開出高價預測,例如 Fundstrat 的 Tom Lee 最近預測:如果宏觀順風與衍生需求持續,以太坊 2025 年底可能達 $16,000。預測市場亦給出74% 概率 以太坊在 2025 創新高,這確實是十分樂觀的機率。當市場一致做多時,往往變得容易因失望而劇烈調整。山寨季即使真實上演,可能還是短暫且猛烈——正如過往週期一樣。高點落袋出場更是難之又難,許多散戶都曾在前幾輪週期音樂停擺時,被套在暴跌山寨幣上。

-

Competition from Other Altcoins and Blockchains: Another angle to consider is that while Ethereum is in focus now, crypto markets have many moving parts. It’s conceivable that another narrative could steal the spotlight from Ethereum if something big happens. For example, if a rival smart contract platform like Solana or Cardano suddenly delivers a breakthrough or an explosive rally (perhaps due to its own upgrade or a specific app going viral there), it could divert capital from Ethereum and muddle the idea of an Ethereum-led altseason. In 2021, we saw mini-seasons like the “Solana Summer” where SOL and its ecosystem boomed independently. Right now, Ethereum has the clear momentum and its L2s cover its scalability, but one shouldn’t dismiss the rest of the field. There are still Bitcoin-centric cycles (like if Bitcoin ETFs get approved, BTC could briefly suck the oxygen again), and specific sectors like AI tokens or metaverse coins could have their own runs not tightly correlated with Ethereum. An altcoin season implies broad participation, but it’s possible not all boats will rise evenly. If Ethereum becomes too dominant, ironically, that might limit the upside of smaller alts (as we discussed in Ethereum season).

-

其他山寨幣/鏈的競爭:另一個必須考慮的角度是——雖然現在市場焦點在以太坊,但加密市場有許多動態變數。完全有可能浮現另一個敘事搶走以太坊風頭。例如 Solana 或 Cardano 這類對手智能合約平台若突然有重大技術突破或瘋狂漲勢(可能來自於升級或熱門應用爆紅),就有機會吸走資本,讓山寨季主角不再單純是 ETH。2021 年曾有類似「Solana 夏天」這種獨立小牛市。眼下雖以太坊氣勢強勁、L2 為其擔綱擴展性,但不該輕忽其他陣營。比特幣為核心的輪動也未消失(例如若 BTC ETF 突然獲批,資金或短暫回流 BTC),而如 AI 幣或元宇宙幣板塊有時也能走出自身行情。正統的山寨季代表普遍參與,但也有可能不是所有項目都漲得整齊。如果以太坊過於強勢,反而會抑制一些較小山寨幣的上漲空間(如我們在 Ethereum season 討論過的)。

In light of these risks, prudent risk management is key even as optimism runs high. The fundamentals for Ethereum look stronger than ever and the ingredients for an altcoin season are largely in place, but external shocks or internal excesses could derail things. Traders and investors are advised to keep an eye on leverage in the system (funding rates, borrow levels), watch for any signs of trend reversals in BTC dominance or ETH momentum, and not overextend on illiquid alt positions that could become hard to exit in a downturn.

面對這些風險,即使市場樂觀聲浪高企,謹慎的風險管理仍是關鍵。以太坊的基本面比以往任何時候都強大,山寨季的諸多要素也已就緒,但外部衝擊或內部泡沫失控一樣可能讓行情偏離軌道。建議交易者與投資人密切觀察系統中的槓桿狀況(如資金費率、借貸部位)、留心 BTC 主導率或 ETH 動能的趨勢反轉訊號,並避免大幅押注流動性弱的山寨幣,以免行情反轉時難以脫身。

Jamie Elkaleh perhaps summed it up well: “All the ingredients for an Ethereum altcoin season are here, but there are no guarantees… risk management remains critical to preserve both value and decentralization.”. It’s a reminder that even as Ethereum becomes a “lightning rod for corporate capital” and retail enthusiasm, one must stay vigilant for potential downsides.

Jamie Elkaleh 的總結也許很貼切:*「以太坊山寨季的所有條件都齊備了,但一切都不能保證……風險管理仍是守護價值與去中心化的關鍵。」*這提醒我們,無論以太坊如何成為「企業資金的避雷針」和散戶熱潮標的,都不能掉以輕心任何潛在下行風險。

Final thoughts

Ethereum’s powerful resurgence in 2025 – marked by new price highs, booming network activity, and surging institutional interest – has positioned it as the prime contender to lead a new altcoin season. The evidence of a shifting regime in crypto markets is mounting: Bitcoin’s dominance has started to slip from its peak, capital is rotating into Ether, and even long-dormant altcoins are showing flickers of life as investors broaden their horizons. In many ways, what we are witnessing could be dubbed an “Ethereum season.” Ethereum has taken center stage with outsized gains and is currently outperforming most of the crypto field. Its breakout above key levels – climbing past $4,000, then $4,500 – has been the catalyst injecting confidence into the entire altcoin complex.

總結

2025 年以太坊強勢再起——不但創下新高,鏈上活動火熱,機構興趣激增——已成主導新一波山寨季的最有力競爭者。加密市場輪動的證據不斷湧現:比特幣主導率已經從頂部下滑、資金明顯輪入以太幣,甚至長期沉寂的老山寨幣也開始甦醒,投資人目光正不斷擴大。從多個角度來看,這波行情可說是「以太季」。以太坊近期表現遠勝大多數主流幣種,成為舞台正中央。它突破歷史關鍵價位——先是 $4,000 再上 $4,500——成為整個山寨行情信心的關鍵催化劑。

Yet, the full bloom of an altcoin season, classically defined, requires more than just a strong Ethereum. It requires sustained and broad-based altcoin outperformance versus Bitcoin, a trend that persists over multiple weeks or months. Are we there yet? Not quite, but we appear to be on the cusp. By all accounts, Ethereum’s recent rally is a vital clue and precursor. Jamie Elkaleh emphasized that Ethereum’s surge alongside a dip in BTC dominance toward the high-50% range “points to early capital rotation”, and on-chain signals like record transaction volume and growing Layer-2 usage “add weight to the shift.” Still, Elkaleh rightly notes a true altcoin season will hinge on sustained altcoin outperformance, a rising total altcoin market cap, and persistent new liquidity inflows (such as those driven by ETFs or other investment vehicles). In plainer terms, altcoins need to keep beating Bitcoin over an extended period, and fresh money – not just recycled

然而,要真正迎來傳統定義的全面山寨季,光靠以太坊強勢還不夠——還需要山寨幣對比特幣持續且廣泛超越,並且這一趨勢需維持數週甚至數月。我們到了嗎?還沒完全到,但彷彿已站在門檻上。從各項指標來看,以太坊的這波漲勢是一個重要的線索與前兆。Jamie Elkaleh 指出,以太與 BTC 主導率下滑至高 50% 區間*「顯示資金正在早期輪動」*,鏈上交易量創新高與二層用量激增也「加重了轉折訊號」。但 Elkaleh 也強調,真正的山寨季,還得看山寨幣持續領先、總市值攀升,以及新資金(如 ETF 或其他投資產品帶來的)持續湧入。簡單來說,山寨幣必須在一段長時間內反覆戰勝比特幣,並取得真正的「新進」資金——而非僅是市場內部流資——如此山寨季才算真正到來。profits – should be coming into the altcoin space.

此時此刻,許多關鍵要素已經就位。以太坊展現出卓越的基本面表現:使用率創下歷史新高,技術升級提升了網絡容量,而該資產如今也穩穩地進入機構投資者視野,ETF資金流入屢創紀錄。圍繞以太坊的敘事已經演變,突顯其在未來金融體系中的關鍵角色,讓這個投資故事與比特幣的「數位黃金」概念並駕齊驅。資金外溢至其他山寨幣已經開始,儘管步伐尚屬溫和。我們見證了XRP法律勝訴如何點燃了傳統山寨幣熱潮,也看到去中心化金融平台與Layer-2網絡在以太坊動能的帶動下蓬勃發展。如果以太坊能保持獨立於比特幣的上升軌跡——基本上開闢自己的領導地位——那麼它「鞏固超越其它山寨幣的地位」的機會將大為提升,也很可能帶動整個市場同步上行。

接下來會發生什麼事?有幾種情境是合理的。在多頭情境中,以太坊持續攀升,最終突破歷史高點,甚至有望明確站穩5,000美元大關。這樣的里程碑可能成為心理觸發點,引爆加密市場的「全部風險偏好」行為。散戶的FOMO(錯失恐懼症)情緒可能高漲,遲來的投資者或將蜂擁買入不僅僅是ETH,更涵蓋各種山寨幣,而經典的山寨季輪動模式(大市值、中市值、小市值輪翻熱漲)可能快速上演。在這種情境下,比特幣市佔率很可能進一步跌破50%,同時扣除BTC的山寨幣總市值大幅上升。以太坊ETF的存在,以及比特幣現貨ETF可能即將上市,這些都將為市場持續注入流動性,至少能讓行情維持一段時間。Layer-2網絡將在這種環境下蓬勃發展,吸納用戶與交易,助長自身成長,進而強化以太坊的價值,形成良性循環。

在較為中性的情境下,以太坊或許會帶動一波溫和的山寨幣上漲,但不至於大舉狂熱。可能出現ETH表現突出並創下新高,但整體山寨幣漲勢依然有選擇性——更偏重質優項目或擁有明確敘事的幣種(如以太坊生態代幣、AI主題代幣等),而非無差別狂拉全場。這將類似於「以太坊季」淡出為溫和的山寨季,但或許不會重現2017或2021年的極端狂潮。在這種情境下,比特幣表現依然穩健,市佔率處於中間區間。加密市場可能出現主導輪動(先BTC、再ETH、然後若干幣種),卻不會有那種傳統意義上的頂峰瘋狂,有些人甚至認為這對市場健康更有利,雖然對渴望百倍報酬的投機者來說略顯平淡。

當然,在空頭情境下,若遇到出乎意外的事件——無論是宏觀動盪還是加密業內問題——都可能迅速中斷山寨幣的反彈,以太坊漲勢會在壓力位(例如前高)受阻,如果比特幣也跟著回檔,整體市場勢頭就暫時降溫,山寨季延至未來。值得一提的是,像2019年那樣,比特幣的強勢行情,卻未能帶來真正的山寨季,反而BTC市佔率長期攀升。這是否可能重演?考慮到以太坊如今的強大地位與用戶基礎,重現機率較低,但加密市場從未有必然之事。

那麼針對Layer-2的角度——「如果以太坊季真的來臨,Layer-2會如何發展」?研究顯示,若以太坊進入高需求階段(價格和用戶活動雙增),Layer-2解決方案將承擔交易主力,讓成長更具可持續性。其實這點已經實現:以太坊使用率創新高時,L2已經處理了超過85%的交易,並壓低手續費。如果以太坊季加劇,我們預計Layer-2網絡將吸引更多用戶、資金和投資熱度(如創投、代幣投機等)。實際上,進入山寨幣的新玩家,很可能就是在Base或Arbitrum等網路上起步,甚至意識不到背後用的其實是以太坊的基礎設施——這也證明當前擴容體驗有多無縫。Layer-2熱潮也意味著,未來的山寨季會比以往更緊密地和以太坊生態綁定。最火紅的山寨幣,許多都將直接來自以太坊生態(L2代幣、DeFi代幣,或各類質押ETH衍生資產)。以太坊的漲潮,必然率先推動其港灣內的項目揚帆。

最終,以太坊作為下一個山寨季領頭羊的崛起,標誌著這個加密市值第二大資產的市場成熟。自2015年僅有願景的投機「山寨」至今,以太坊已發展為支撐整個加密經濟龐大領域的多元平台。它持續吸引大額資本與用戶的能力,證明市場的山寨行情可以由基本面驅動,而非僅靠炒作。當然,加密市場從不只是基本面——人性心理、宏觀環境與創新周期都會共同作用。交易者與愛好者都要保持資訊敏銳與操作靈活。請緊盯重點指標:比特幣市佔率(是否持續下滑?),ETH/BTC比值(以太幣是否繼續領漲?),DeFi和L2生態的鎖定總價值(健康增長還是泡沫過熱?),以及ETF核准或利率決策這類外部因素。

結論來說,面對「以太坊是否領銜新一輪山寨季?」這個問題,可以這樣總結:以太坊確實展現出近年來最有力的領頭候選資格。近期的突出表現及其底層結構條件(機構認同、鏈上優勢、擴容方案)與以往山寨季爆發前的情況高度相似。如果現有趨勢不變,我們或將迎來真正的「以太坊季」——不僅引領,甚至定義一個全新周期。如果以太坊成功,也很可能將帶領整個山寨幣市場一同步入更寬廣的多頭行情。

最後,提醒投資者以樂觀與謹慎並存的心態迎接這個激動人心的可能性。加密市場瞬息萬變,但就目前而言,明顯是以太坊處於主導地位。以太坊季或許即將到來,若歷史可以借鑑,山寨幣落後的時間應該不會長——但同時也要記住,季節會輪換,審慎的策略才能穿越最狂熱的漲勢。