全球銀行體系每日流動超過五兆美元,這些交易通過數十年前建構的網路進行,當時仍需電傳機與紙本確認。

SWIFT 訊息系統於 1973 年上線,至今依舊支撐著絕大多數的國際資金流動。匯款須穿越多個代理銀行,交易僅以訊息的方式於不同專屬資料庫間反覆流轉,每個環節都需數小時或數日來處理。對帳以批次方式進行,結算更需等到上班時間。即使全球金融運作極為複雜精密,底層基礎設施依然來自於網際網路尚未成形的年代。

然而在這些舊有架構下,某些本質性的轉變正悄然發生。它不是來自炫目的公有鏈或熱門的加密貨幣,而是在全球最大型銀行內部,步步為營地推動。花旗集團執行長 Jane Fraser 與摩根大通執行長 Jamie Dimon 都已將代幣化存款與區塊鏈基礎建設作為機構跨境支付和資金業務現代化的核心戰略。這些並非實驗性質的側翼專案,而是金融機構間資金移動方式的全面重建。

花旗於 2023 年 9 月推出 Token Services 平台,讓企業客戶的存款可以轉為數位代幣,即時進行跨境支付、全年無休。摩根大通則於 2025 年 6 月上線 JPMD 存款代幣,在 Coinbase 的 Base 區塊鏈上運行,讓機構客戶享有24小時結算和計息功能。德意志銀行則於 2025 年 5 月加入 Partior 的區塊鏈結算平台,成為歐元和美元結算銀行,進一步擴大亞洲大型金融機構聯網。

這些詞彙聽起來很技術性、甚至平淡:「代幣化存款」、「分散式帳本技術」、「原子結算」。但它們對全球金融體系的運作核心產生了深遠影響。這不是單純將代幣化存款與穩定幣比較,也不是銀行試圖與加密貨幣產業競爭,而是國際金融系統“水電管線”的根本重建,以可編程貨幣和共享帳本,一次一筆交易地推動。

這場轉型已經展開,且是由真實的資金經由真實系統流動。摩根大通的區塊鏈平台自 2020 年以來,處理的交易總額超過 1.5 兆美元,日均交易金額突破 20 億美元。花旗集團支付業務每日於 90 多國處理高達 5 兆美元,且積極將區塊鏈能力整合進其龐大基礎建設。

與加密貨幣市場的公開風波不同,這場革命是經由企業合作、監管核可以及與現有系統的謹慎整合推進。對比之下,去中心化金融(DeFi)協議標榜從外部顛覆銀行,而代幣化存款則是銀行利用區塊鏈技術,於受監管之授權環境內自我重建,服務於機構級規模。

Jane Fraser 將花旗的區塊鏈堆疊描述為流動性管理的「殺手級應用」,這也凸顯這波轉型的戰略急迫性。在企業財務長要求即時資訊與全時掌控、供應鏈 24 小時全球運作、資本市場追求即刻結算的今日,傳統銀行基礎設施已顯老態。代幣化存款不僅是漸進式改善,而是根本性架構升級:全年無休、可編程自動化、原子結算、透明對帳。

問題不在於這場變革會不會到來——大型銀行早已投入上億美元和上千小時開發工時。真正問題是這套新型架構對更廣泛金融體系究竟意義為何、監管如何調適、還存在哪些瓶頸,最終,SWIFT 時代的代理銀行制度會否如電傳機一樣邁向淘汰。

本文將深入剖析這場轉型,不只做表面比較,更探討代幣化存款的技術、營運、監管以及戰略層面。唯有了解正在構建的是什麼,以及其背後的重要性,我們才能窺見 21 世紀金融架構,正悄然於今日市場底層成形。

什麼是真正的代幣化存款?

在探索代幣化存款如何轉變銀行基礎建設前,需先明確了解其本質及與類似工具的區別,即便老練市場參與者也可能混淆,因此厘清內容非常重要。

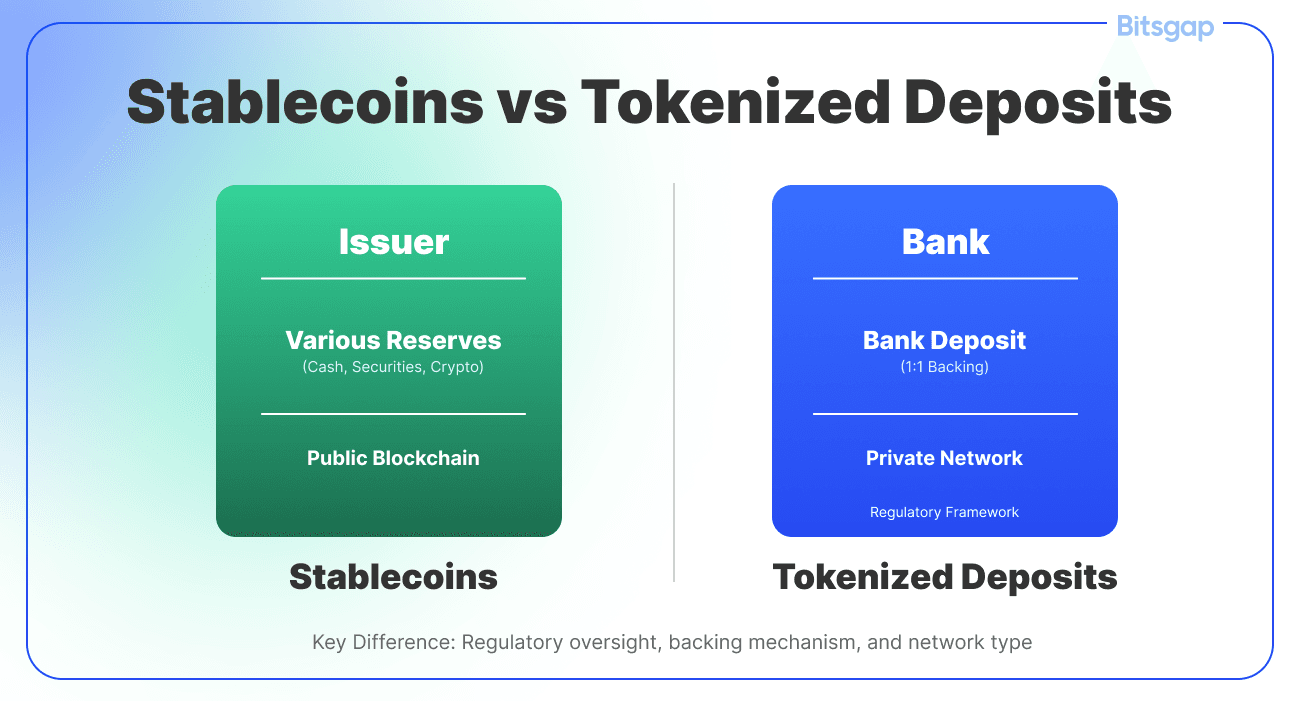

代幣化存款,是以數位方式在分散式帳本或區塊鏈上記錄的商業銀行負債。企業用戶持有代幣化存款時,相當於擁有對受監管銀行的債權,就如持有傳統銀行存款帳戶。關鍵差異不在於法律關係或負債性質,而在於存款的表現方式、移轉及可編程性。

可以這麼理解:傳統銀行存款存在各銀行專屬資料庫,當資金在不同銀行移轉時,必須透過 SWIFT 這類網路發送指令協調帳戶更新,讓多方獨立維護自家帳本,產生對帳困難與結算延遲。反觀代幣化存款,以數位代幣形式存在多家授權機構可同時存取的共享帳本。代幣本身即為該負債的最終紀錄,移轉只需於共享帳本上調整,不用訊息傳遞於多個系統間。

與穩定幣的區別極為關鍵,但也最易讓人誤解。穩定幣通常由非銀行機構(如 Circle、Paxos)發行,錨定美元,儲備資產為短期國債及現金,分離於發行方營運資產之外。它們可於公有鏈或私鏈流通,點對點轉帳不須經銀行中介。儲備資產則多於特殊目的載體或信託架構下保管,以便發行方倒閉時保障持有人權益。

代幣化存款運作不同。它直接由受監管商業銀行發行,屬於銀行資產負債表中的真實存款負債,因此本質上就是銀行貨幣,而非另類資產類別。用戶持有摩根大通代幣化存款,即直接擁有對摩根大通銀行 N.A. 的債權,並受 FDIC 保險與傳統存款人保障。每單位 JPMD 完全由等值法幣存款做全額支持,確保鏈上帳戶與帳外存款一一對應。

這些區別對監管、風控與功能性意義重大。代幣化存款完全受現行銀行法規範,不需全新類別,僅是存款這一既有工具的技術升級。發行銀行本就持有銀行牌照,接受嚴格審監、資本與流動性管控、定期受主管機關查核,監管明確可循。

中央銀行數位貨幣(CBDC)則屬另一範疇。CBDC 屬中央銀行負債,處於貨幣體系金字塔頂端。零售 CBDC 理論上讓全民直接在聯準會或歐洲央行持有帳戶,徹底重塑銀行體系,將商業銀行從支付服務中排除。批發 CBDC 僅於金融機構間用作結算工具,猶如今日的央行準備金,但具備不同技術屬性。

紐約聯邦準備銀行與大型銀行探討的「受監管負債網路」(Regulated Liability Network),則設想同一分散式帳本同時支持批發型 CBDC 與商業銀行存款代幣,顯示貨幣體系既須要央行貨幣做最終結算,也需商業銀行貨幣支持信用擴張與客戶關係。

電子貨幣代幣(E-money tokens),受歐盟電子貨幣指令與最新的 MiCA 法規監管,位於相近領域。電子貨幣屬於預付儲值,由專業電子貨幣機構發行,不是全面銀行。其監管要求與存款銀行不同,商業模式也多以支付為主,而非綜合性金融關係。

代幣化存款帳本結構因應業者不同但具共通特徵。多數主要銀行計畫採用「授權區塊鏈」或分散式帳本技術,僅限獲核可的節點參與交易驗證和帳本維運。花旗 Token Services 採私有以太坊鏈,摩根大通雖選用 Coinbase 推出的公有以太坊鏈(Base),卻以授權門檻限制存取權。

此種授權架構同時達成・・・ participate in the network, supporting know-your-customer and anti-money-laundering compliance. It allows banks to maintain control over governance, operational procedures, and technical standards. It enables higher transaction throughput than public blockchains typically achieve. And it provides the operational finality and reversibility mechanisms that regulated financial systems require when dealing with errors, fraud, or legal orders.

參與網路,支援認識你的客戶(KYC)和反洗錢(AML)合規性。這讓銀行得以維持對治理、營運程序和技術標準的控制。它帶來比公有區塊鏈更高的交易處理量。此外,也提供受監管金融體系在面對錯誤、詐騙或法律命令時所需的運作終局性及可回復機制。

From the client's perspective, tokenized deposits can operate almost invisibly. Citi designed its Token Services so clients don't need to set up separate wallets or hold tokens in accounts they must manage independently. The tokenization happens at the infrastructure layer, enabling new capabilities without forcing clients to adopt entirely new operational models. A corporate treasurer can instruct a payment through familiar interfaces, and the underlying technology handles the blockchain transactions transparently.

從客戶的角度來看,代幣化存款的運作幾乎可以做到無感。花旗銀行設計其代幣服務時,就是讓客戶毋須額外設立錢包或在必須獨立管理的帳戶持有代幣。代幣化是在基礎設施層實現,讓新功能無縫整合,而無需強迫客戶採用全然不同的營運模式。財務長可以透過既有熟悉的界面指示付款,底層技術則會透明地處理區塊鏈交易。

This design philosophy reflects a pragmatic recognition: large corporations and institutional clients care about functionality, not technology for its own sake. They want faster settlement, better liquidity management, programmable automation, and transparent reconciliation. Whether those benefits arrive through distributed ledgers, traditional databases, or some hybrid matters less than whether the system is reliable, cost-effective, and compatible with their existing operations.

這種設計理念反映出切合實際的認知:大型企業與機構客戶關注的是功能性,而不是純粹為了科技本身。他們追求更快的結算、更好的流動性管理、可程式化自動化,以及透明的對帳。不管這些好處是經由分散式帳本、傳統資料庫或某種混合方案實現,是否可靠、具成本效益並符合現有營運需求才是關鍵。

The ownership structure reinforces the banking paradigm. Traditional banks maintain custody of the underlying fiat deposits represented by tokens. The tokens themselves are bearer instruments in a technical sense, meaning possession of the cryptographic keys controls the tokens. However, the tokens only exist on permissioned ledgers where all participants are known and authorized. You cannot simply send a tokenized deposit to an anonymous wallet on a public blockchain. The tokens move only within controlled environments between identified counterparties.

這種所有權架構加強了傳統銀行體系的模式。傳統銀行負責保管由代幣代表的基礎法幣存款。技術上,這些代幣本質上是持有人工具,也就是說擁有加密金鑰就能控制代幣。然而,這些代幣只存在於經授權的帳本上,所有參與者皆為已知並獲得授權。你無法將代幣化存款隨意發送到公有區塊鏈上的匿名錢包。代幣僅於受控制的環境中、在已辨識身分的對手間流轉。

This closed-loop architecture addresses one of the fundamental tensions in digital money design: the conflict between programmability and regulatory compliance. Stablecoins on public blockchains can move anywhere, to anyone, at any time. This creates obvious compliance challenges. Tokenized deposits trade some of that permissionless flexibility for regulatory clarity and institutional compatibility. They are programmable money for the regulated financial system rather than for the open internet.

這種封閉回路的架構針對數位貨幣設計上的一項基本矛盾:可編程性與合規的衝突。公有區塊鏈上的穩定幣可以隨時轉移給任何人、到任何地方,這無疑產生合規挑戰。代幣化存款則犧牲部分這樣的無許可靈活性,換取合規明晰與體制相容。他們是為受監管金融體系打造的可程式化貨幣,而非開放網路上的數位貨幣。

The regulatory classification flows naturally from this structure. Under the GENIUS Act passed by the U.S. Senate in 2025, deposit tokens issued by regulated banks are explicitly recognized as distinct from stablecoins issued by nonbank entities. Banks issuing deposit tokens operate under their existing banking charters and supervision. They need no separate "stablecoin license" because they are not issuing stablecoins; they are simply using new technology to represent traditional deposit liabilities.

監管分類自然由這種架構衍生。在2025年美國參議院通過的GENIUS法案中,受監管銀行發行的存款代幣獲明確列為有別於非銀行實體發行的穩定幣。銀行發行存款代幣時仍受現有銀行執照與監理架構規範,無需另行取得「穩定幣執照」,因為他們並非發行穩定幣,而是利用新技術來代表傳統存款負債。

Understanding what tokenized deposits are and are not provides the foundation for assessing their impact. They are not a new form of money but a new technology for representing existing money. They are not crypto assets seeking regulatory approval but regulated banking products using blockchain technology. They are not alternatives to the banking system but tools for upgrading it. This distinction shapes everything that follows: how tokenized deposits function, how they are regulated, what advantages they provide, and what challenges they face.

了解代幣化存款是什麼、不是什麼,是評估其影響的基礎。他們不是一種全新的貨幣,而是現有貨幣的全新表徵方式。他們不是尋求監管核准的加密資產,而是運用區塊鏈技術的受監管銀行產品。他們不是銀行體系的替代品,而是升級銀行體系的工具。這一區別將牽動後續一切,包括代幣化存款如何運作、如何監管、能提供哪些優勢及可能面臨哪些挑戰。

From SWIFT to Smart Contracts: How Money Movement Is Changing

從 SWIFT 到智慧合約:金流運作模式如何轉變

The transformation from legacy payment rails to blockchain-based settlement represents more than a technology upgrade. It fundamentally reimagines how financial institutions coordinate, how transactions achieve finality, and how global liquidity flows.

從傳統支付管道轉型為區塊鏈基礎結算,不僅僅是技術升級。這一變革徹底重新構思了金融機構如何協同、交易如何達到終局,以及全球流動性如何流通。

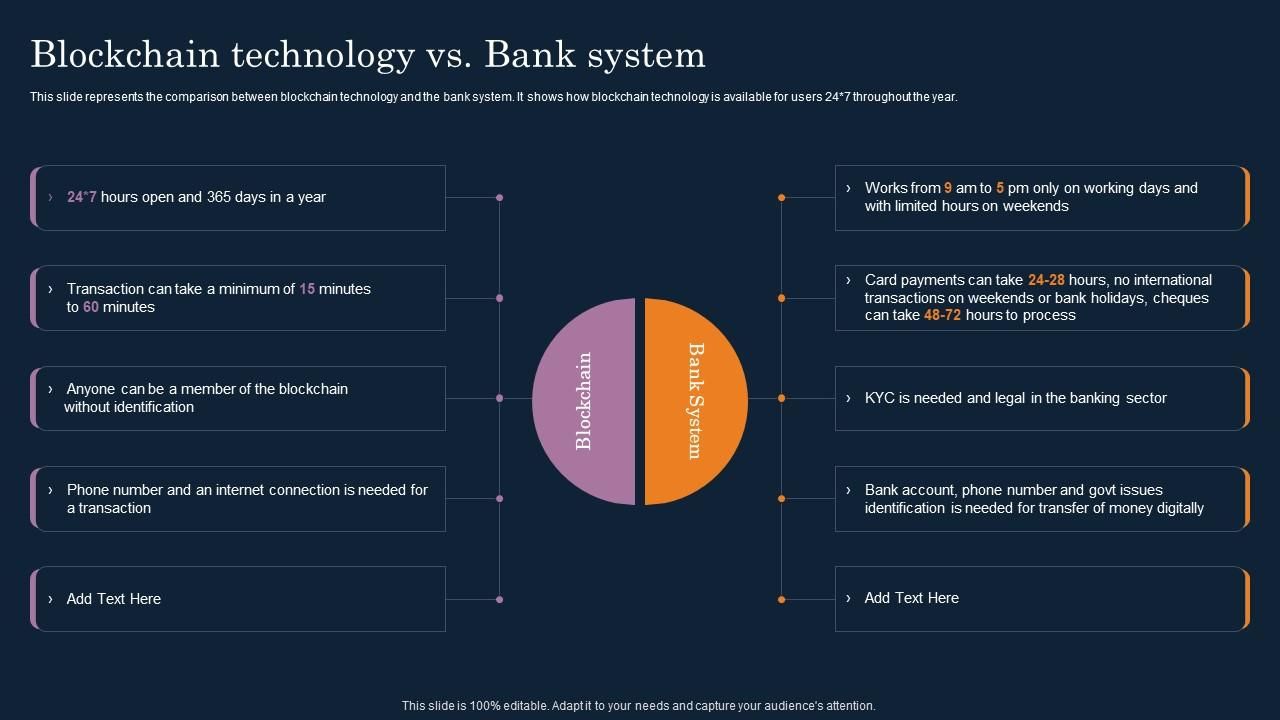

To understand the magnitude of this change, we must first examine what is being replaced. The SWIFT network, formally the Society for Worldwide Interbank Financial Telecommunication, does not actually move money. It moves messages about money. When a corporation in New York instructs its bank to pay a supplier in Frankfurt, that instruction becomes a SWIFT message transmitted from the sending bank to the receiving bank, possibly passing through intermediary correspondent banks along the way.

要理解這一轉變的意義,我們必須先檢視現有體系。SWIFT 網路(國際金融電訊協會)實際上並不移轉資金,而是傳遞有關資金的訊息。當位於紐約的公司指示其銀行支付給法蘭克福的供應商時,這項指示會成為 SWIFT 訊息,由發送銀行經過多家中介往來銀行,傳遞至接收銀行。

Each institution in this chain maintains its own ledger. The SWIFT message instructs them to update those ledgers, debiting one account and crediting another. But the actual movement of funds between banks happens through separate settlement mechanisms: correspondent banking relationships where banks maintain accounts with each other, or through central bank settlement systems like Fedwire in the United States or TARGET2 in Europe.

鏈條上的每個機構都維護自己的帳本。SWIFT 訊息只指示他們更新各自帳本,扣除本行某帳戶、加記另一方帳戶。但銀行間實際資金流動則是透過另一套結算機制完成:包括銀行之間的往來帳戶結算,或是美國 Fedwire、歐洲 TARGET2 等央行系統。

This architecture introduces multiple friction points. Messages travel separately from settlement. Different institutions update different databases, creating reconciliation requirements. Transactions queue in batches processed during business hours. Cross-border payments may traverse multiple correspondent banks, each adding time, cost, and operational risk. Foreign exchange conversion happens through separate trades that must be coordinated with the underlying payment. Throughout the process, money sits in nostro and vostro accounts, trapped as pre-funded liquidity that cannot be used for other purposes.

這種架構產生多層摩擦。訊息傳遞與實際結算是分開進行。不同機構更新不同資料庫,造成對帳需求。交易在營業時段分批處理。跨國匯款可能經過多家往來銀行,每一環節都增加時間、成本及營運風險。外匯兌換需另行進行,還需與支付交易同步處理。整個過程中,資金滯留於 nostro 與 vostro 帳戶,成為無法靈活運用的預備流動性。

The result is a system characterized by latency, opacity, and inefficiency. A traditional cross-border payment might take days to settle, passing through multiple intermediaries in a hub-and-spoke model that adds time and costs at each step. Senders and recipients see limited information about transaction status. Banks tie up enormous amounts of capital in correspondent account balances. Errors require manual intervention to unwind transactions already recorded across multiple separate systems.

這導致體系呈現高延遲、不透明和效率低落等現象。一筆傳統跨境付款可能得花上數天結算,期間需經中介轉手、步步增添時間和成本。交易雙方對於狀態的資訊有限。銀行需動用大量資本預存在往來帳戶。產生錯誤時,必須動用人工干預來撤銷那些已在不同獨立系統留有紀錄的交易。

None of this would matter if global commerce operated on a nine-to-five schedule in a single time zone with occasional cross-border transactions. But modern business runs continuously across all time zones with supply chains spanning multiple countries and currencies. The disconnect between how commerce operates and how payment systems function creates enormous friction.

如果全球商業還能只在單一時區、朝九晚五、偶而才有跨國交易,那這一切摩擦都不受影響。但現代商業活動二十四小時橫跨全球、多國與多種貨幣,實際運作與支付體系之落差帶來巨大阻力。

Tokenized deposit systems address these limitations through several key innovations, all enabled by the shared ledger architecture. First and most fundamentally, they combine messaging and settlement into a single atomic operation. When a tokenized deposit transfers from one party to another on a shared ledger, both the instruction and the settlement happen simultaneously. There is no separate message instructing a separate settlement. The transfer of the token is the settlement.

代幣化存款系統透過共用帳本架構帶來多項創新,解決上述限制。最根本的是,訊息傳遞與結算合而為一,形成原子操作。當代幣化存款於共用帳本上從一方轉給另一方時,指示與結算同步進行。不存在分開傳訊與分開結算的流程;代幣移轉本身即是結算。

This atomic settlement property eliminates many failure modes inherent in message-based systems. You cannot have a situation where the message is received but settlement fails, or where settlement occurs differently than the message instructed. Either the entire transaction succeeds or the entire transaction fails. The shared ledger provides a single source of truth that all parties can see simultaneously.

這種原子性結算特質,杜絕基於訊息系統下固有的失敗情境。不存在訊息到達但結算失敗,或結算結果與訊息內容不符的狀況。要嘛整筆交易成功,要嘛全盤作廢。共用帳本成為所有參與者隨時能查證的唯一事實來源。

Citi's Token Services enables institutional clients to complete cross-border payments instantly, around the clock, transforming processes that traditionally took days into transactions completed in minutes. The speed improvement is dramatic but understates the deeper change. More important than speed alone is the combination of speed with finality and transparency. Parties know immediately that settlement has occurred and can see proof on the shared ledger.

花旗銀行的代幣服務讓機構客戶可全天候即時完成跨境付款,把以往需耗時數天的流程,壓縮為幾分鐘即可完成。速度上的提升雖然驚人,但真正的重大意義是速度、終極結算與透明度的結合。交易雙方可以即時確認結算已完成,並可在共用帳本上驗證。

JPMorgan's Kinexys Digital Payments system, formerly JPM Coin, provides similar capabilities, processing roughly two billion dollars in daily transactions with near-instant settlement available 24/7. The system supports multiple currencies and integrates with JPMorgan's foreign exchange services to enable on-chain FX settlement. This means a corporate client can instruct a payment in one currency to a counterparty receiving a different currency, and the entire transaction including FX conversion settles atomically on the blockchain.

摩根大通的 Kinexys 數位支付系統(前稱 JPM Coin)同樣具備這類功能,每日處理約二十億美元交易,並可 24/7 提供近乎即時的結算。該系統支援多種貨幣,並整合摩根大通外匯服務,實現鏈上外匯結算。這代表企業客戶可以用一種貨幣付款,對方以另一種貨幣收款,整筆交易(包括匯兌)皆可在區塊鏈上以原子操作結清。

The operational implications are profound. Consider a multinational corporation managing cash across dozens of subsidiaries in different countries. Under traditional correspondent banking, moving funds between subsidiaries requires navigating multiple payment rails with different operating hours, settlement times, and fees. Liquidity gets trapped in transit and in buffers maintained to ensure subsidiaries can meet local obligations.

其營運意義深遠。以一間橫跨數十國子公司的跨國企業為例,若採傳統往來銀行體系,資金在子公司間轉移,須面臨不同行時、不同管道、各異費用及結算時程。流動性容易被卡在在途資金與為當地法規設置的安全緩衝之中。

With tokenized deposits on a shared ledger, the same corporation can move funds between subsidiaries continuously and instantly. Clients can now pay disbursements to counterparties without the need for prefunding, optimizing liquidity management and reducing transaction costs. A treasury department can maintain a more centralized liquidity pool and deploy funds precisely where and when needed rather than maintaining expensive buffers in each location.

有了共用帳本的代幣化存款,該企業即可隨時將資金即時劃撥至各子公司。客戶支付給對手方再也不必預存資金,進一步優化流動性管理並降低交易成本。財務部還可維持集中式流動資金池,資金部署更加精確、即時,而不用在每地都保留昂貴的備用資金。

The network effects matter enormously here. JPMorgan processes transactions reaching multiple billions of dollars on some days after introducing programmability to the network. Citi's payments business handles five trillion dollars daily across more than 90 countries, including 11 million instant transactions. As more counterparties join these tokenized networks, the utility increases dramatically. A closed-loop system connecting only a single bank's clients provides limited benefit. A network connecting hundreds of institutions and thousands of corporate clients fundamentally changes liquidity dynamics.

網路效益在此極為顯著。例如摩根大通自導入可程式化功能以來,部分天數的交易規模達數十億美元。花旗的支付業務涵蓋全球 90 多國、每日處理 5 兆美元,當中即時交易超過 1,100 萬筆。隨著越來越多對手方參與代幣化網路,網路效用水漲船高。僅封閉在某單一銀行客戶的系統作用有限,連接上百家機構、數千企業客戶的網路,則能徹底改變流動性生態。

Partior's blockchain-based settlement platform exemplifies this network approach, providing real-time atomic clearing and settlement for participating banks using tokenized commercial bank and central bank liabilities. The platform supports Singapore dollars, U.S.

Partior 的區塊鏈結算平台正是此種網路模式的典範,為參與銀行提供即時原子性清算和結算,並使其能以代幣化商業銀行和央行負債進行交易。該平台支援新加坡元、美元等多種貨幣。dollars, and euros through founding correspondent banks including DBS, JPMorgan, and Standard Chartered. Deutsche Bank completed its first euro-denominated cross-border payment on Partior in collaboration with DBS, executing the transaction across different financial market infrastructures and demonstrating how blockchain can complement existing systems.

美元與歐元交易,是透過包含星展銀行、摩根大通與渣打銀行等創始代理行協助完成的。德意志銀行與星展銀行合作,於Partior平台上完成了首筆以歐元計價的跨境支付,該交易橫跨不同的金融市場基礎設施,展現出區塊鏈技術如何補足現有系統。

The Partior model is instructive because it shows how tokenized deposits can create shared infrastructure while preserving banks' individual client relationships and regulatory compliance obligations. Financial institutions connect to Partior to make instant interbank cross-border payments 24/7, resolving longstanding inefficiencies including settlement delays, high costs, and limited transaction transparency. Nium became the first fintech to join the Partior network, giving its clients access to 24/7 instant payments without requiring another API integration, demonstrating how the network can extend beyond traditional banks to encompass the broader financial ecosystem.

Partior模式具有啟示性,因為它展現了如何透過代幣化存款建立共用基礎建設,同時保持銀行各自與客戶的關係及合規義務。金融機構可接入Partior平台,進行全年無休、即時的跨行跨境支付,一舉解決以往存在的結算延遲、高成本與交易透明度有限等長期問題。Nium成為首家加入Partior網路的金融科技公司,使客戶可不需再整合其他API下,直接享有全年無休的即時付款,顯現出此網路可擴展至傳統銀行以外,涵蓋更廣泛的金融生態系。

Smart contracts add another dimension by enabling programmable settlement logic. In traditional systems, conditional payments require manual processes or complex escrow arrangements. Smart contracts allow parties to encode business logic directly into the payment instruction. A payment can be programmed to execute automatically when specified conditions are met: delivery confirmation, regulatory approval, or completion of a related transaction.

智慧合約透過讓結算邏輯可編程,為系統增添了新維度。在傳統系統中,附條件付款往往需手動處理或複雜的託管安排。智慧合約則允許各方直接將商業邏輯寫入付款指令。付款可預設:只要達成特定條件,例如交貨確認、獲監管核准或相關交易完成,即自動執行。

Citi's Token Services can optimize trade finance by replacing letters of credit and bank guarantees with smart contracts that automatically release payments once set conditions are met. In pilot testing, international shipping company Maersk transferred tokenized deposits to instantly pay service providers, compacting process times from days to minutes.

花旗的Token Services可用智慧合約取代信用狀與銀行保函,條件一旦達成即自動付款,大幅優化貿易融資流程。於試點測試中,國際航運公司馬士基以代幣化存款瞬間支付服務商,將原本需耗時數天的流程壓縮至數分鐘。

The trade finance use case illustrates the power of combining atomicity with programmability. Traditional trade finance involves complex coordination between multiple parties: importer, exporter, banks in different countries, shipping companies, customs authorities, and insurance providers. Documents must be verified, goods must be inspected, title must transfer, and payment must release, all according to carefully sequenced conditions. The coordination happens through a combination of legal agreements, physical documents, and manual verification.

貿易融資案例展現原子性與可編程性的結合威力。傳統貿易融資往往需進行複雜的多方協調,包括進出口商、跨國銀行、航運公司、海關及保險公司。文件需審核、貨物需驗收、權利需移轉、款項需釋出,並都必須依照嚴密安排的流程順序進行協調,其過程仰賴法律合約、實體文件與人工驗證。

Smart contracts can encode much of this logic and execute it automatically when conditions are verified. The verification itself can happen through oracle services that feed external data onto the blockchain, or through tokenization of the underlying assets and documents. When the bill of lading is tokenized and transferred, confirming receipt of goods, the smart contract can automatically release payment. Settlement happens atomically: the buyer receives the tokenized bill of lading representing ownership of the goods, and the seller receives payment, simultaneously and irreversibly.

許多這類邏輯皆可透過智慧合約編碼,並於條件達成時自動執行。驗證可靠預言機(oracle)服務將外部資料寫入區塊鏈,或運用基礎資產及文件的代幣化技術完成。當提單被代幣化並移轉、確認已收貨品後,智慧合約即可自動釋放款項。結算以原子性方式完成:買方同時收到象徵貨物所有權的提單代幣,賣方同時收到款項,兩者同步且不可逆。

This atomic delivery-versus-payment capability extends beyond trade finance. JPMorgan's Kinexys Digital Assets platform launched a Tokenized Collateral Network application enabling the transfer of tokenized ownership interests in money market fund shares as collateral for the first time on blockchain. The system supports frictionless transfer of collateral ownership without the complexity of moving assets through traditional means. The platform has already enabled more than 300 billion dollars in intraday repo transactions by providing short-term borrowing in fixed income through the exchange of cash for tokenized collateral.

這種原子化的「貨款兩訖」能力也應用至貿易融資以外。摩根大通Kinexys Digital Assets平台上線了代幣化擔保品網路(Tokenized Collateral Network),首次實現貨幣市場基金份額代幣化所有權於區塊鏈上移轉作為擔保品。該系統讓擔保品所有權可流暢移轉,免去傳統實體資產交割的繁複。迄今該平台已支援逾三千億美元當日回購(repo)交易,透過現金與代幣化擔保品交換,提供固定收益型短期融資。

The repo market provides a compelling example of how atomic settlement reduces risk. In traditional repo transactions, there is a brief window where one party has transferred securities but not yet received cash, or vice versa. This creates settlement risk that participants must manage through margins, collateral agreements, and credit limits. Atomic settlement on a shared ledger eliminates this risk entirely. Securities and cash transfer simultaneously in an indivisible transaction. Either both sides complete or neither does.

回購市場正好體現原子型結算如何降低風險。在傳統回購交易時,一方證券轉移但尚未收到現金、或反之,於此空窗產生結算風險,需靠保證金、擔保協議與信用額度控管。共享帳本上的原子結算徹底消除此風險,證券與現金以不可分割、同時且不可逆的單一交易完成-要嘛雙方都成交,要嘛皆作廢。

Foreign exchange settlement benefits similarly. Standard Chartered completed euro-denominated cross-border transactions between Hong Kong and Singapore using Partior's global unified ledger infrastructure, becoming the first euro settlement bank to use the platform. FX settlement risk, where a bank might pay out one currency before receiving the other, represents one of the largest intraday risk exposures in financial markets. Payment-versus-payment settlement on blockchain networks can eliminate this risk.

外匯結算也有類似效益。渣打銀行利用Partior的全球統一帳本基礎設施,在香港和新加坡間完成歐元計價跨境交易,成為首家使用該平台的歐元結算銀行。外匯結算風險,即銀行支付一種貨幣前未收到另一種貨幣,是傳統金融市場最大當日風險來源之一。區塊鏈上「付款對付款」(payment-versus-payment)模式可消除此風險。

Partior is developing payment-versus-payment capabilities for FX settlement, which offers significant promise in reducing settlement risk especially for non-mainstream currencies. Other planned features include intraday FX swaps, cross-currency repos, and programmable enterprise liquidity management, all building on the atomic settlement foundation.

Partior正開發FX結算「付款對付款」功能,對降低特別是非主流貨幣的結算風險具巨大潛力。其他規劃功能還有當日外匯互換、跨幣種回購、及可程式化的企業流動性管理,所有這些皆建基於原子性結算架構。

The technical implementation varies across platforms but shares common patterns. Transactions are submitted to the network, validated according to predefined rules, executed atomically, and recorded on the shared ledger. The validation can check balances, verify signatures, ensure compliance with payment limits or regulatory requirements, and confirm that smart contract conditions are met. The ledger update happens only if all validations pass, ensuring transaction integrity.

不同平台的技術實作雖異,但皆有共通結構:交易送交網路、依預定規則驗證、原子化執行、登錄於共享帳本。驗證程序可檢查餘額、驗署、確保符合付款上限或法規,並確認智慧合約條件達標。只有所有驗證全數通過,帳本才會更新,保障交易完整性。

Throughput, latency, and finality present important technical considerations. Public blockchains like Ethereum mainnet currently process 15-30 transactions per second with block times of 12-13 seconds, insufficient for global payment systems handling millions of transactions daily. JPMorgan chose Base for JPMD deployment partly because it offers sub-second, sub-cent transactions, dramatically better performance than Ethereum mainnet. Layer 2 scaling solutions and permissioned blockchains can achieve much higher throughput, with some systems processing thousands of transactions per second.

吞吐量、延遲與確定性是重要技術考量。以以太坊主網為例,目前每秒僅能處理15-30筆交易,區塊時間12-13秒,遠不足應付每日數百萬筆交易的全球支付系統。摩根大通選擇Base部署JPMD,部分原因即其能實現亞秒級、亞美分級的交易效能,遠勝於以太坊主網。第二層擴容方案(Layer 2)或許可權區塊鏈則能達數千TPS。

Finality, the point at which a transaction becomes irreversible, varies across blockchain designs. Some systems provide probabilistic finality where the chance of reversal decreases exponentially as more blocks build on top of a transaction. Others provide deterministic finality where transactions are final as soon as they are confirmed. For institutional payments, deterministic finality is strongly preferred because participants need certainty that settlement is complete and cannot be unwound except through deliberate counterparty action.

「確定性」指交易不可逆的確定時點,依區塊鏈架構而異。部分系統具「機率性確定」,即累積越多區塊反轉機率越低;其他設計則為「決定性確定」,經確認即不可逆。對機構型支付而言,決定性確定性更受青睞,因為參與者須確認結算已完成且除了合意對手方作業外絕不可逆。

Security represents another critical dimension. Blockchain systems must protect against both external attacks and internal malfeasance. External attacks might target the network infrastructure, cryptographic keys, or smart contract code. Internal malfeasance could involve node operators, bank employees, or compromised client credentials. Permissioned networks can implement stronger access controls and identity verification than public blockchains, reducing certain attack vectors while introducing different governance challenges around who controls the network and under what rules.

安全性也是關鍵環節。區塊鏈系統需兼顧外部攻擊與內部不當行為。外部攻擊可能針對網路基礎設施、密鑰或智慧合約原始碼;內部風險則涵蓋節點營運者、銀行職員或用戶憑證被盜。許可權鏈可加強存取控制與身分驗證,減少部分攻擊途徑,但同時帶來另類治理挑戰:誰掌控網路,規則由誰訂定。

The comparison with public blockchain infrastructure highlights different design philosophies optimized for different use cases. Blockchain eliminates the need for multiple intermediaries by creating direct payment corridors, with transactions often completed in minutes rather than days. Public blockchains prioritize permissionless access, censorship resistance, and decentralized control. Permissioned networks prioritize transaction throughput, regulatory compliance, and operational governance. Neither is inherently superior; they serve different purposes for different users.

與公鏈基礎設施的比較,凸顯出各自對應不同需求的設計哲學。區塊鏈直連支付渠道,省去層層中介,交易往往幾分鐘完成而非數天。公鏈以開放存取、抗審查與去中心化為核心;私有或許可鏈則注重高頻交易、合規與治理。兩者無本質優劣,僅適合不同情境與需求。

For institutional financial services, the permissioned approach currently dominates because it better aligns with regulatory requirements, risk management practices, and business models based on trusted relationships rather than trustless protocols. Public blockchains succeed where openness and censorship resistance provide fundamental value, as in cryptocurrency markets or certain decentralized finance applications. The question is not which is better in absolute terms but which better fits specific use cases and constraints.

對機構型金融服務,目前以許可鏈為主,因其更容易符合法規、風險控管,且模式本就以信賴為基礎而非無信任協議。公鏈則在「開放」及「不受審查」至關重要的領域(如加密貨幣市場、某些DeFi應用場景)發揮價值。問題不在孰優孰劣,而是場景與限制誰更適用。

As tokenized deposit infrastructure matures, hybrid models may emerge that bridge permissioned and public networks. A corporation might maintain tokenized deposits on a bank's permissioned blockchain for most treasury operations but interact with public DeFi protocols through controlled gateways for specific purposes. Interoperability between networks, discussed in later sections, will determine how fluid such interactions can become.

隨著代幣化存款基礎設施趨向成熟,結合私有與公有區塊鏈的混合模式或將興起。例如,一家企業大多數資金操作都在銀行的許可鏈上執行,但為某些需求也能經受控閘道介接到公有DeFi協議。各網路間的互通性(稍後章節介紹)將決定這種跨網互動的流暢性。

The trajectory is clear even if the endpoint remains uncertain: money movement is shifting from message-based correspondent banking toward direct settlement on shared ledgers. SWIFT will not disappear overnight, and traditional correspondent banking relationships will persist for many purposes. But the gravitational center of global payments infrastructure is migrating toward tokenized deposits on blockchains that combine instant settlement with programmable logic and 24/7 availability. This represents not just faster legacy systems but a fundamentally different architecture for how financial institutions coordinate and how money moves through the global economy.

即使最終型態未明,趨勢已十分清晰:資金流動正從過去以訊息為主的代理行網絡,轉向在共享帳本上直接清算。SWIFT不會一夕消失,傳統代理銀行架構仍有其必要。但全球支付基礎設施的重心,正逐步轉向結合即時結算、可編程邏輯與全年無休服務的區塊鏈代幣化存款系統。這不僅是傳統系統提速,更是金融機構協作模式與資金流動架構的根本性轉變。

The 24/7 Bank: Why Always-On Finance Changes Everything

24/7銀行:為何「永遠在線」的金融會改變一切

The transition from batch processing to continuous real-time operation represents one of the most significant operational transformations in modern banking. Yet this shift remains underappreciated, perhaps because the implications extend far beyond technology into

由批次處理轉向持續即時運作,是現代銀行營運模式最重大變革之一。然而這項轉變卻往往被低估,或許原因在於其影響不只是技術層面——更涵蓋……組織文化、風險管理與商業模式。

傳統銀行以工作日為基礎運作,並設有明確的交易截止時間。於截止時間後收到的款項,必須等到下一個處理週期才能結算。跨境交易必須應對多個時區和當地的營業時間。證券交割通常於T+2或T+1進行,在交易執行與最終結算之間產生時間差。負責全球營運的財務部門為確保各地子公司在本地營業時間內有充足資金,需維持資金緩衝,即使這意味著一地的資本需在夜間或週末閒置,而其他地區卻可能面臨短缺。

在交易需要人工介入、電腦連續運作成本過高、全球商業節奏緩慢的時代,這種批次處理模式是合理的。然而,這些限制如今皆不再相關。企業供應鏈全年無休,全球金融市場其實無時無刻不在運作,隨時都在世界某處有交易市場開放。跨國企業需要在業務需求發生時隨時轉移資金,而不是受限於銀行的處理時間表。

代幣化存款能實現真正的24/7銀行業務,因為共享帳本基礎設施全年無休並可即時結算交易,不受日曆與時鐘限制。Partior的24/7區塊鏈網路與本地貨幣實時支付系統和RTGS系統互補且能互通,彌補這些系統未能連續運作的不足。紐約的財務長週日下午即可即時、最終將資金匯至新加坡子公司,該交易無須等待週一早上處理,亦無須等待相關時區代理銀行開業。

這種運營模式在企業財資管理上引發多重層面的變革。首先,也是最明顯的,是流動性管理大幅提升效率。若沒有24/7能力,企業必須在各地維持流動性緩衝,以應對資金無法在非營業時段調撥的狀況。有了全年無休的可用性,財資可以集中資金池,按實際需求精準調配資金到所需地點與時點。

以一家橫跨亞洲、歐洲和美洲的全球製造商為例。若無即時全球支付,財務長可能需分散維持共一億美元流動性於各地區,以確保能支付薪資、供應商款項和應付突發狀況。有了24/7即時轉帳,則可能僅需七千萬美元,維持較小的中央資金池及區域緩衝,遇實際需求時再調撥資金,而非事前為假設性需求預留成本高昂的資金緩衝。

釋放出來的三千萬美元流動性可更有效運用:償還債務、投資營運,或投入更高收益的工具。長期下來,成千上萬家公司累積起來,僅靠減少閒置資本便已創造可觀價值。

利息最佳化是自然結果。在批次處理環境下,週五下午轉帳的資金可能要到週一才到帳,白白損失兩天的利息。即時結算下,資金可隨時賺取利息報酬,不會在轉帳途中浪費時間。對於管理數十億美元流動性的企業來說,即使微小的利息效率提升,累積也會相當可觀。

Jane Fraser指出,雖然銀行能提供24/7的代幣化貨幣,許多企業財務部門尚未準備好「隨時開機」的運作模式。這點突顯了一個關鍵:技術能力已超前於組織準備度。企業若在週六深夜收到即時款項,必須有系統能偵測、記錄並回應這些交易。財資管理系統、企業資源規劃軟體(ERP)、會計系統都需從批次轉為持續運作。

人的因素也同樣重要。傳統財資團隊在工作時間上班,正因為當時才有交易處理。全年無休的運營帶來了下班時段監控、例外處理和決策的新問題。企業是否要設立24/7財資運營中心?自動化系統能否處理大多數情境,由人員隨時待命監督?企業如何在提升效率與全天候人力成本之間取得平衡?

不同組織會根據規模、產業與運營模式,對此有不同解答。跨時區持續生產的全球製造商,或許會自然而然地將24/7財資運營納入現有模式。支付模式較可預期的專業服務公司,則可能選擇在工作時間進行批次處理,即便底層技術已支援持續結算。

風險管理影響層面不限於運營就緒與否。持續結算徹底改變信貸風險、市場風險與操作風險的性質,且這些變化細微但重要。日內信貸風險降低,因為結算是即時、持續發生,不需等至結束批次才結算。但全年無休的運作也開啟了新的錯誤與詐騙風險,可能馬上擴大、而非在批次對帳時才被發現。

智能合約自動化帶來機會也帶來風險。一方面,自動執行可減少人為錯誤,並確保商業邏輯一致性。另一方面,智能合約若編碼有誤,則可能導致系統性失敗並影響大量交易。2010年5月美股閃崩事件,由於自動交易演算法觸發,正說明自動化雖能消滅某些失效方式,同時卻也會產生或強化另外一些。

對帳與會計是另一個主要運營面向。在批次處理下,對帳依循交易批次完成的特定時點進行。會計系統按日或定期日誌登錄交易。Citi的代幣服務提供自動化對帳,減少當不同機構維護不同帳冊時的人工處理。共享分類帳成為所有方可見的單一事實來源,消除過去機構間需比對各自帳簿以找出和解差異的困擾。

但持續結算也代表持續會計。不再是以單日分錄記錄所有交易,而需隨時隨地即時入帳。企業資源規劃系統須與區塊鏈支付系統整合,隨時抓取交易資料並及時更新財務紀錄。這項技術整合雖屬可行,但需要大幅升級系統及重設流程。

24/7營運模式也影響銀行自家資產負債管理。傳統銀行根據既定交易流量規律計算日內流動性需求。全年無休的營運意味流動性需求也是持續不斷、沒有既有的自然休止可進行資金再平衡。不像傳統穩定幣,未來存款代幣可能納入存款保險及計息,代表銀行或會對代幣存款支付利息。計息的代幣存款將如傳統計息帳戶,以持續累積利息並即時可用,銀行產品間的界線更為模糊。

擔保品管理也有相似變革。JPMorgan的代幣化擔保品網絡,支援以貨幣市場基金份額的代幣權益作擔保品,讓雙方能隨時根據市場狀況或頭寸變化動態調整擔保,而無需等到特定結算時段。此一能力,對於擔保要求極易隨市價與倉位變動的回購和衍生品市場尤為重要。

以衍生品市場來說,持續結算和擔保品管理可顯著降低對手方風險。傳統做法是在特定時點補充初始及追加保證金,期間市場波動可能遠超保證金緩衝。若改為即時結算與計算保證金,這些風險窗口將被關閉,雖然同時也會增加操作複雜度。

文化及組織意涵亦不容忽視。傳統銀行的運作,歷來與作業時間與結算日曆同步。交易員、財資主管、營運組、風險經理的工作作息,皆環繞開盤收市、付款截止與結算週期安排。進入全年無休模式將打亂這些節奏,迫使組織重新思考工作型態、職責分配及監督方式。

部分機構會充滿熱忱地擁抱這場變革,將更佳的流動性管理和客戶服務視為競爭優勢。也有機構會被迫被市場、客戶需求拉著前進,但苦於舊系統和慣性。領先者多半是本就跨時區、多地營運的全球銀行,已經有持續營運文化;較小的地區銀行則可能較長時間維持傳統運營模式。

客戶教育同樣是一大挑戰。企業財資主管熟悉批次處理和工作日流程,是因為他們已經——operated within those constraints for decades. Explaining the benefits of 24/7 settlement, demonstrating how to use new capabilities, and helping clients redesign their own treasury processes to take full advantage all require sustained effort. Fraser's comment about corporate readiness for always-on operations likely reflects this educational and change management challenge as much as technological concerns.

在這些限制下運作已經數十年了。說明全天候(24/7)結算的好處、展示如何利用新功能,並協助客戶重新設計自己的資金管理流程以盡最大優勢,這一切都需要持續不斷的努力。Fraser 所提到企業是否已做好隨時在線運作(always-on)的準備,很可能反映出教育和變革管理方面的挑戰,甚至多於技術層面的考量。

The regulatory implications deserve attention as well. Banking regulations developed when institutions operated during business hours with defined settlement cycles. How do reserve requirements, capital buffers, liquidity coverage ratios, and stress test scenarios adapt to continuous operations? Should regulators expect different operational risk profiles from 24/7 banks? These questions lack definitive answers but will shape how continuous settlement integrates with prudential regulation.

監管層面的影響同樣值得關注。銀行法規是在金融機構以營業時間運作、並有明確結算週期的時代訂立的。存款準備金要求、資本緩衝、流動性覆蓋率以及壓力測試場景,應如何調整以適應連續運作?監管單位是否應對全天候銀行的營運風險有不同的預期?這些問題目前尚無定論,但它們將會影響持續結算如何與審慎監管融合。

Looking forward, the always-on bank represents not merely a faster version of existing banking but a qualitatively different operational model. The implications extend from technology infrastructure through accounting systems, risk management frameworks, organizational structures, client relationships, and regulatory expectations. Early adopters will discover which changes create competitive advantage and which introduce new challenges. Followers will learn from pioneers' experience but risk falling behind as client expectations shift toward continuous service and instant settlement.

展望未來,隨時在線的銀行並不僅僅是現有銀行業的加速版,而是一個本質上截然不同的營運模式。其影響涵蓋技術基礎設施、會計系統、風險管理架構、組織結構、客戶關係及監管期望。早期採用者將發現哪些改變能帶來競爭優勢、哪些則會帶來新挑戰。後進者雖可借鏡先行者經驗,但隨著客戶預期轉向連續服務與即時結算,落後風險大增。

The transformation is irreversible not because the technology compels it but because client needs demand it. Once corporate treasurers experience instant cross-border settlement and continuous liquidity management, they will not willingly return to batch processing and business-hour constraints. The 24/7 bank becomes the new baseline expectation, forcing the entire industry to adapt or risk losing clients to more agile competitors.

這場轉型之所以無法逆轉,並非因為技術所逼,而是因為客戶需求使然。當企業財務長體驗過即時跨境結算與連續的流動性管理後,他們不會心甘情願回到批次處理與營業時間的限制。全天候銀行成為新的標準期待,迫使整個產業必須適應,否則就有被更敏捷的競爭者奪走客戶的風險。

Technical Infrastructure and Interoperability

技術基礎架構與互通性

The promise of tokenized deposits depends fundamentally on the technical infrastructure supporting them: the blockchain architectures, smart contract platforms, interoperability layers, and APIs that enable institutions to deploy programmable money at scale. Understanding this infrastructure reveals both the capabilities currently available and the challenges that remain.

代幣化存款的實現,根本上依賴於其所依附的技術基礎:包括區塊鏈架構、智慧合約平台、互通層和 API,這些要素讓金融機構能大規模部署可編程貨幣。了解這些基礎設施,能看出目前可用的功能以及尚待克服的挑戰。

Most major tokenized deposit implementations use permissioned distributed ledger technology, though specific choices vary. Citi's Token Services operates on a private, Ethereum-based blockchain, giving the bank full control over network participation and governance while benefiting from Ethereum's mature tooling and development ecosystem. JPMorgan deployed JPMD on Base, Coinbase's public Ethereum layer-2 blockchain, but implemented permissioned access controls so only authorized institutional clients can use the tokens.

多數主流的代幣化存款實作,都是建立在有權限的分散式帳本技術上,不過各家選擇不盡相同。花旗銀行的 Token Services 運作在以太坊(Ethereum)私有鏈上,銀行可完全掌握網路參與與治理,同時享有以太坊成熟的開發工具與生態系。摩根大通則將 JPMD 部署在 Coinbase 所運營的公開以太坊 Layer-2 區塊鏈 Base 上,但加入權限限制,僅授權的機構型客戶能使用這些代幣。

The Ethereum Virtual Machine has become something of a standard for smart contract execution even in permissioned environments. Developers familiar with Solidity, the dominant smart contract programming language, can deploy code to Ethereum-based permissioned chains with minimal adaptation. This talent availability and tooling maturity gave Ethereum-derived architectures significant advantages despite the platform's well-known limitations around transaction throughput and fees on public mainnet.

以太坊虛擬機(EVM)即使在有權限環境下,也已成為智慧合約執行的某種標準。熟悉 Solidity(主流智慧合約程式語言)的開發者,僅需極少調整即可部署程式碼到以太坊為基礎的私有鏈。這種人才供給與工具成熟度,賦予以太坊衍生架構明顯優勢,儘管該平台在公鏈主網上的交易吞吐量及手續費等限制是眾所周知的。

Other enterprise blockchain platforms like Hyperledger Fabric, Corda, and Quorum offer alternative architectures optimized for permissioned use cases. Hyperledger Fabric uses a modular architecture where components for identity management, consensus, and ledger storage can be customized for specific needs. Corda focuses on financial services use cases with built-in support for complex financial agreements and privacy-preserving data sharing. Quorum, developed by JPMorgan and later spun out, extends Ethereum with enterprise features including transaction privacy and permissioned networks.

其他企業級區塊鏈平台如 Hyperledger Fabric、Corda 與 Quorum,則為有權限的應用場景提供了不同的最佳化架構。Hyperledger Fabric 採用模組化架構,身份管理、共識、帳本儲存等組件均可針對需求客製化。Corda 則聚焦在金融服務,內建複雜金融合約與保護隱私的資料分享功能。Quorum 由摩根大通開發、後來獨立出來,在以太坊基礎上加強了企業功能,如交易隱私與有權限網路等。

The choice between platforms involves tradeoffs across multiple dimensions. Ethereum-based systems benefit from extensive developer communities, mature tooling, and interoperability with Ethereum-native applications. Purpose-built enterprise platforms like Hyperledger and Corda offer better privacy controls, higher transaction throughput, and financial-services-specific features but less extensive ecosystems. Public blockchain deployment with permissioned layers, as JPMorgan chose for JPMD, combines aspects of both: leveraging public infrastructure and tooling while maintaining control over access and usage.

在平台選擇上,會牽涉多面向的取捨。以以太坊為基礎的系統受惠於廣大的開發社群、成熟的工具,以及與以太坊原生應用的互通性。像 Hyperledger、Corda 這類為企業而生的平台,則提供更佳的隱私控管、更高的交易吞吐量及專為金融服務打造的功能,但生態系規模較小。摩根大通選擇在公有鏈上以權限層部署 JPMD,則兼顧兩者優勢,既可利用公共基礎設施與工具,又能掌控存取與使用權。

Consensus mechanisms vary as well. Public blockchains like Ethereum use proof-of-stake or proof-of-work to achieve decentralized consensus among untrusted validators. Permissioned networks can use simpler and faster consensus algorithms like practical Byzantine fault tolerance variants or Raft because all validators are known and authorized. The consensus choice affects transaction finality, throughput, and resilience but matters less to end users who simply want reliable settlement.

共識機制也有所不同。像以太坊這類的公有鏈,採用權益證明(Proof-of-Stake)或工作量證明(Proof-of-Work)來讓陌生的驗證者間建立去中心化共識。有權限的網路則可用更簡單而快速的共識演算法,如實用拜占庭容錯(PBFT)或 Raft,因為所有驗證者的身份皆已知且獲授權。共識機制的選擇會影響交易最終性、吞吐量與韌性,但對於只關心可靠結算的終端用戶而言影響不大。

Smart contract capabilities enable the programmable aspects of tokenized deposits. Contracts can encode conditional logic: execute payment only if certain conditions are met, split payments among multiple recipients according to defined formulas, or trigger secondary transactions automatically when primary transactions complete. The power comes from combining these capabilities: a trade finance smart contract might verify delivery confirmation through an oracle service, automatically execute payment from buyer to seller, trigger a secondary payment from seller to shipping company, and update trade documentation, all atomically and automatically.

智慧合約功能賦予代幣化存款可編程的特性。合約可寫入條件邏輯:只有在特定條件成立時才執行付款、依照公式自動分派付款給多個對象,或在主要交易完成時自動觸發次級交易。其威力來自於這些功能的組合,例如:貿易融資的智慧合約可透過預言機服務確認交貨、從買家自動付款給賣家、再自動支付運費給貨運公司,並同步更新貿易文件,以上流程皆可自動且原子性地完成。

Security in smart contract development remains challenging. Code vulnerabilities can create exploits that drain funds or disrupt operations. Even well-audited contracts sometimes contain subtle flaws discovered only after deployment. Financial institutions deploying tokenized deposits must invest heavily in code audits, formal verification where practical, and operational safeguards including circuit breakers that can halt activity if anomalies are detected.

智慧合約開發的安全性依舊極具挑戰。程式碼漏洞可能被利用,造成資金被盜或業務中斷。即便經過嚴格審核的合約,有時也會在實際部署後才發現隱蔽的缺陷。金融機構在部署代幣化存款時,必須投入大量資源於程式碼審核、(於可行範圍內)進行形式驗證,並建立運營防護措施,如可在異常時緊急斷路的機制。

Interoperability represents perhaps the greatest technical challenge facing tokenized deposit infrastructure. Each bank's implementation exists on a separate blockchain or private ledger. If you had a separate Citi Coin and a Wells Fargo Coin, there's a good chance they'd use different technologies, creating interoperability challenges for using distributed ledger technology for interbank payments. Transactions within a single institution's blockchain settle efficiently, but moving value between different institutions' systems requires bridges or intermediary layers.

互通性也許是代幣化存款基礎設施面臨的最大技術挑戰。每家銀行的實作,各自有不同的區塊鏈或私有帳本。假設你擁有不同的花旗幣與富國幣,它們很可能採用不同技術,導致分散式帳本在跨行支付時的互通障礙。同一機構內帳本上的交易結算效率高,但跨機構則需靠橋接或中介層移轉價值。

Several approaches to cross-chain interoperability have emerged. Atomic swaps enable direct exchange of tokens between blockchains using cryptographic techniques that ensure either both sides complete or neither does. Wrapped tokens involve locking tokens on one blockchain and minting equivalent tokens on another, with a custodian managing the locked collateral. Cross-chain messaging protocols like Chainlink's Cross-Chain Interoperability Protocol enable blockchains to exchange data and instructions, allowing smart contracts on one chain to trigger actions on another.

目前已出現數種跨鏈互通方案。原子互換(atomic swaps)可利用加密技術直接於鏈與鏈間交換代幣,保證雙方要嘛都交易成功、要嘛都不成交。包裹代幣(wrapped tokens)是在一條區塊鏈上鎖定代幣,於另一鏈上鑄造等值代幣,存託人負責管理鎖定的抵押品。像 Chainlink 的跨鏈互通協議這類的跨鏈訊息協定,則允許不同鏈之間交換資料與指令,可讓一條鏈上的智慧合約觸發另一條鏈上的行動。

Circle's Cross-Chain Transfer Protocol represents another interoperability approach, enabling native USDC to move between supported blockchains without wrapped tokens. While designed for Circle's stablecoin rather than bank-issued tokenized deposits, the protocol demonstrates technical patterns that could apply more broadly. Users burn USDC on the source chain and mint equivalent USDC on the destination chain, with Circle's infrastructure ensuring atomicity and finality.

Circle 的跨鏈轉帳協議是另一種互通路徑,允許原生 USDC 在受支援的區塊鏈間直接移轉,而無需包裹代幣。儘管該協議主要設計給 Circle 的穩定幣(非銀行發行的代幣化存款),但所體現的技術模式具備廣泛應用潛力。用戶會在發送鏈「銷毀」USDC,然後於目標鏈鑄造等值 USDC,由 Circle 基礎設施確保操作的原子性及最終性。

Partior's approach differs by creating a shared settlement layer that multiple banks use rather than connecting separate bank blockchains. Partior's unified ledger enables real-time atomic clearing and settlement, providing instant liquidity and transparency by using programmable shared infrastructure rather than sequential processing in legacy payment systems. Banks participating in Partior can settle with each other directly on the shared ledger rather than exchanging tokens between separate systems.

Partior 方案的路徑不同,其打造的是多家銀行共同使用的共享結算層,而非聯結各自獨立的銀行區塊鏈。Partior 的統一帳本支援原子性實時清算與結算,利用可編程共享基礎架構提升流動性及透明度,不走傳統順序處理路徑。參與的銀行得以直接於共享帳本互相結算,而非跨系統交換代幣。

The network effects of these different interoperability models vary significantly. Atomic swaps work peer-to-peer but require both parties to be online simultaneously and become complex for multi-party transactions. Wrapped token approaches centralize risk with the custodian managing locked collateral. Cross-chain messaging protocols create dependencies on oracle services and message relay infrastructure. Shared settlement layers like Partior require participants to agree on common governance and technical standards.

這些不同互通模式所產生的網路效應差異很大。原子互換屬於點對點,需要雙方同時在線,若是多方交易則更複雜。包裹代幣將風險集中於管理抵押品的託管方。跨鏈訊息協定則依賴預言機服務和中繼訊息基礎設施。像 Partior 這樣的共享結算層,則要求參與者在治理與技術標準上達成共識。

For institutional use cases, trust-based interoperability solutions may prove more practical than fully trustless bridges. Banks already maintain correspondent banking relationships backed by legal agreements and credit lines. Extending these relationships to include interoperability between tokenized deposit systems adds technical capabilities without fundamentally changing the trust model. A bank might agree to accept another bank's tokenized deposits at par with minimal friction because existing agreements and capital relationships already support that trust.

對於機構應用場景而言,基於信任的互通方案可能比完全去信任的橋接設計更實際。銀行間早已有代理銀行關係,這些關係有法律協議與信貸作後盾。只需將互通層納入代幣化存款系統,即能提升技術能力,且不用根本改變原有信任架構。一家銀行或許能因現有協議與資本關係信任,而零摩擦接受另一家銀行的代幣化存款並按面額處理。

API layers provide another critical infrastructure component, enabling existing banking systems to interact with blockchain-based tokenized deposit infrastructure. Citi designed its Token Services for seamless integration with clients' existing systems, avoiding the need for clients to adopt entirely new platforms or interfaces. Clients can instruct payments through familiar banking channels, with the bank's systems translating those instructions into blockchain transactions behind the scenes.

API 層為另一項關鍵基礎建設,能讓既有銀行系統與區塊鏈型代幣化存款基礎設施互通。花旗銀行設計其 Token Services 時,就是為了能與客戶現有系統無縫整合,讓客戶無需學習全新的平台或介面。客戶仍可透過熟悉的銀行通道指示付款,由銀行系統將指令在後台自動轉為區塊鏈交易。

This API approach reflects pragmatic recognition that

這種 API 策略反映了一種務實的認知,即wholesale replacement of existing corporate treasury systems is unrealistic. Large corporations run complex ERP environments, custom treasury management platforms, and payment processing systems representing decades of investment and configuration. Successful tokenized deposit adoption requires working with this installed base rather than demanding replacement.

替換現有企業財務管理系統(corporate treasury systems)進行全面升級並不切實際。大型企業營運著複雜的ERP環境、客製化的財資管理平台及支付處理系統,這些系統代表了數十年的投資與配置。成功推動代幣化存款的採用,需與現有系統基礎協同整合,而非一味要求全數替換。

Latency in tokenized deposit systems generally falls far below traditional correspondent banking but varies by implementation. Partior carried out end-to-end settlements involving both U.S. and Singapore dollars in under two minutes, dramatically faster than traditional cross-border settlement but still longer than the near-instant settlement possible in single-blockchain environments. The difference reflects interoperability overhead and validation requirements when transactions cross institutional boundaries.

代幣化存款系統的延遲通常遠低於傳統代理銀行,但具體效能仍因不同實作而異。Partior平台曾以不到兩分鐘的時間完成美元及新加坡元的端到端結算, 大幅領先傳統跨境結算時間, 但仍稍慢於單一區塊鏈環境下可實現的近乎即時結算。這主要反映了交易橫跨不同機構時,互通運作的額外負擔與驗證需求。

For many institutional use cases, settlement in minutes rather than seconds makes little practical difference. The critical threshold is same-day settlement with sufficient speed that transactions can complete within operational timeframes. Instant settlement provides obvious benefits for time-sensitive situations, but the jump from multi-day to sub-hour settlement captures most of the practical value for treasury management applications.

對多數機構應用場景而言,結算時間從數秒提升至數分鐘,其實在實務上影響有限。最關鍵的門檻在於能實現「同日結算」,並確保交易能於營運時段內完成。即時結算在時間極為敏感的情境下當然有其顯著優勢,然而將多日結算縮短至一小時內,已經涵蓋了大部分財資管理應用的實際價值。

Throughput represents another important dimension. Base blockchain offers sub-second, sub-cent transactions, providing the performance required for high-volume payment applications. Permissioned enterprise blockchains can achieve even higher throughput because they optimize for that goal without the decentralization constraints of public blockchains. The relevant question is whether throughput meets or exceeds the transaction volumes the institution expects to handle, not whether the blockchain matches payment card network speeds of thousands of transactions per second.

「處理量」是另一關鍵面向。底層區塊鏈可支援小於一秒、低於一美分的交易速度與手續費,滿足高頻支付應用的性能需求。權限制的企業級區塊鏈甚至能實現更高的吞吐量,因其優化目標不受公鏈去中心化限制。真正要問的是:這樣的處理量能否支撐或超越機構預期的業務需求,而不必拘泥於是否能達到支付卡網路那種每秒數千筆交易的水準。

Privacy-preserving technologies address concerns about transaction visibility on shared ledgers. Institutions may hesitate to use shared blockchains where all participants can potentially see all transactions, even if identities are pseudonymous. Zero-knowledge proofs enable proving transaction validity without revealing transaction details. Ring signatures and mixing protocols obscure transaction graphs. Confidential transactions hide amounts while enabling validation that inputs equal outputs.

隱私保護技術專門解決共享帳本上交易可見性的疑慮。即使參與者身分化名,部分機構仍會對所有人可見之區塊鏈存有遲疑。零知識證明可以在不揭露細節前提下證明交易有效性;環簽名與混合協議則能混淆交易路徑;保密交易(Confidential transactions)可隱藏金額,同時確保收付方金額平衡驗證通過。

JPMorgan published a whitepaper demonstrating a proof-of-concept exploring on-chain privacy, identity, and composability, recognizing these as major themes for continued blockchain evolution in institutional contexts. Enhanced privacy measures are crucial for enabling broader adoption without compromising commercial confidentiality or exposing competitive information.

摩根大通(JPMorgan)曾發表白皮書,展示一個針對鏈上隱私、身分、以及可組合性(composability)的概念驗證,並認知這些都是區塊鏈能否在機構層廣泛發展的重大主題。強化的隱私防護措施,是實現更廣泛採用、同時免於商業機密外洩及避免競合資訊暴露之關鍵。

The governance of blockchain infrastructure matters enormously for institutional adoption. Who controls the network? Who can join as a node operator or validator? How are technical upgrades decided and implemented? What happens when disputes arise or transactions need reversal due to errors or fraud? Public blockchains answer these questions through decentralized governance, albeit often with challenges around coordination and plutocratic voting power. Permissioned networks must establish explicit governance frameworks.

區塊鏈基礎設施的治理模式,對於機構採納極為重要。誰控制這個網路?誰能成為節點營運者或驗證者?技術升級的決策與執行由誰主導?若發生糾紛、錯帳或詐欺須逆轉交易,該如何處理?公有鏈這類問題靠去中心化治理解決,但經常受制於協調困難及投票權過於集中的挑戰。權限制網路則必須建立明確的治理架構。

Partior is backed by a consortium of global banks including DBS, JPMorgan, Standard Chartered, and Deutsche Bank, creating a multi-party governance model where major participants collectively control the network's evolution. This approach balances the need for coordination and standards with the desire to avoid single-institution control that could introduce conflicts of interest.

Partior由DBS、摩根大通、渣打銀行及德意志銀行等全球性銀行聯盟共同支持,採集體治理模式,使主要參與者共同主導網路發展。此種設計可兼顧協調與標準訂定需求,又能防止單一機構主控所帶來的利益衝突風險。

Network resilience and business continuity require careful consideration. Blockchain networks must continue operating even if individual nodes fail, network partitions occur, or deliberate attacks target infrastructure. Permissioned networks with a limited number of known validators can achieve strong resilience through redundancy and geographic distribution. The tradeoff is that network operation depends on the validators remaining operational and properly motivated to maintain service.

網路韌性與營運持續性也需審慎規劃。即便出現節點故障、網路隔離,或遇惡意攻擊,區塊鏈仍須維持運作。權限型網路因驗證者數量有限且可辨識,得以透過備援及地理分散提升韌性。其權衡點在於網路高度依賴這些驗證者正常運行,且須有足夠動機持續維護服務。

Operational reversibility presents a particular challenge. Traditional payment systems allow transactions to be reversed or recalled in certain circumstances: errors, fraud, or legal orders. Blockchain systems designed for immutability resist reversal by architecture. Financial institutions need mechanisms to handle exceptional situations while preserving the finality that makes blockchain settlement attractive. Solutions typically involve permissioned capabilities allowing authorized parties to mint new tokens offsetting erroneous transfers rather than literally reversing blockchain transactions.

交易可逆性是一大挑戰。傳統支付系統允許在特定情況下進行交易撤回或逆轉,如錯帳、詐欺或司法命令等。區塊鏈因強調不可竄改,天生難以逆轉交易。金融機構必須取得處理極端狀況的機制,同時保留區塊鏈不可撤銷結算所帶來的好處。常見作法是授權特定方發行新代幣來對消錯誤轉帳,而非直接逆轉原有鏈上紀錄。

The technical infrastructure for tokenized deposits continues evolving rapidly. Current implementations provide sufficient capabilities for initial deployment and pilot programs, but scaling to full production across diverse use cases will require ongoing development. Standards for interoperability, identity management, privacy preservation, and cross-chain settlement remain works in progress. The industry must balance the benefits of customization for specific needs against the imperative of compatibility and standardization enabling network effects.

代幣化存款相關的技術基礎設施仍在快速演進。目前的實作已足以支援早期部署及試點計畫,但要擴展至全面正式營運、涵蓋多元應用場景,仍需持續開發。互通、身分管理、隱私保護、跨鏈結算等標準尚在持續制定中。業界需在滿足特定需求的客製化與推動兼容性、標準化以產生網路效應之間取得平衡。

Ultimately, the technical infrastructure matters insofar as it enables the functional capabilities institutions and their clients require: fast settlement, programmable logic, continuous availability, transparent reconciliation, and interoperability across institutions and networks. The specific blockchain platforms, consensus mechanisms, and interoperability protocols are means to these ends rather than ends in themselves. As the technology matures and standards emerge, the infrastructure should become increasingly invisible to end users who simply experience superior payment and liquidity management capabilities without needing to understand the underlying blockchain mechanics.

最終,技術基礎設施的重要性在於能否實現機構及其客戶所需:快速結算、可程式邏輯、持續可用、透明對帳及夠跨機構/跨網路互通。至於採用哪種區塊鏈平台、共識演算法、互通協議,這些都只是達成功能的手段而非目的。隨技術成熟、標準落地,基礎設施應將逐漸對終端用戶「隱形」,用戶僅需享受更佳支付與流動性管理體驗,而無需瞭解底層區塊鏈細節。

Compliance and Regulation: Built for the Regulated World

One of the most significant advantages tokenized deposits hold over many cryptocurrency alternatives is how naturally they fit within existing regulatory frameworks. While crypto markets often struggle with regulatory uncertainty, tokenized deposits emerged from regulated banks operating under established supervision, making compliance integration a design feature rather than an afterthought.

代幣化存款相較許多加密貨幣的重大優勢之一,在於它自然而然地能納入現有監管框架。加密貨幣市場常因監管不明朗備受掣肘,然而代幣化存款則源自受嚴格監管銀行體系,在既有監理下運作,使合規整合成為設計本身的一部分,而非事後補救。

Traditional banking regulation divides oversight across multiple dimensions: prudential regulation ensuring banks remain safe and sound, conduct regulation governing how banks treat customers, and functional regulation covering specific activities like payments or securities services. Banks issuing tokenized deposits already operate under comprehensive supervision across all these dimensions. The blockchain technology introduces new operational characteristics but does not fundamentally alter the legal nature of the deposit or the regulatory obligations surrounding it.

傳統銀行監管分為多個層面:審慎性監理以確保銀行穩健經營、行為監理規範銀行對待客戶之方式、功能監理則針對支付、證券服務等特定業務設下規範。發行代幣化存款的銀行,早已涵蓋在上述所有監理範疇內。區塊鏈帶來新的運作特性,卻未根本改變存款的法律性質或其所受監理義務。

In the United States, banks issuing tokenized deposits operate under the supervision of their primary federal regulator: the Office of the Comptroller of the Currency for national banks, the Federal Reserve for state member banks and bank holding companies, or the Federal Deposit Insurance Corporation for state non-member banks. These regulators examine banks regularly, assess capital adequacy, review risk management practices, and enforce compliance with banking laws. Tokenized deposits simply represent another product offering subject to this existing supervision.

在美國,發行代幣化存款的銀行由其主要聯邦監管單位監督:全國性銀行屬於貨幣監理署(OCC)、州會員銀行及銀行控股公司則由聯邦儲備系統(Federal Reserve)監管、州非會員銀行則受聯邦存款保險公司(FDIC)監理。這些單位定期稽查、審核資本適足性、檢視風險管理,並強制執行銀行相關法規。代幣化存款在現有監理下,僅屬於銀行所提供的另一種產品。

The Office of the Comptroller of the Currency clarified its position on bank crypto activities through interpretive letters beginning in 2020, confirming that national banks may provide custody services for crypto assets, use stablecoins for payment activities, and operate nodes on blockchain networks. The GENIUS Act, passed by the Senate in June 2025 and signed into law in July 2025, established a federal regulatory framework for payment stablecoins while explicitly recognizing deposit tokens issued by regulated banks as distinct from stablecoins issued by nonbank entities.

美國貨幣監理署自2020年起透過釋義信函,明確表示全國性銀行可為加密資產提供託管服務、利用穩定幣進行支付及營運區塊鏈節點。2025年6月,美國參議院通過Genius法案,並於同年7月生效,該法建立了支付型穩定幣的聯邦監管體系,明確區隔受監管銀行發行之存款代幣與非銀行機構發行之穩定幣。

The GENIUS Act requires payment stablecoin issuers to hold at least one dollar of permitted reserves for every stablecoin issued, with permitted reserves limited to coins, currency, insured deposits, short-dated Treasury bills, repos backed by Treasury bills, government money market funds, and central bank reserves. Issuers must submit periodic reports of outstanding stablecoins and reserve composition, certified by executives and examined by registered public accounting firms, with those having more than 50 billion dollars in outstanding stablecoins required to provide audited annual financial statements.

Genius法案要求支付型穩定幣發行方,必須為每一枚穩定幣持有至少一美元等值的合格準備金,且準備金僅限現金、貨幣、受保存款、短天期國庫券、國庫券擔保回購、政府貨幣市場基金及央行存款等。發行機構需定期申報未償還穩定幣及其準備金組成,由高層主管認證,並接受註冊會計師事務所審查。未償還穩定幣超過500億美元者,須提供經審計的年度財報。

The GENIUS Act explicitly states that payment stablecoins issued by permitted issuers are not securities under federal securities laws or commodities under the Commodity Exchange Act, removing them from SEC and CFTC jurisdiction. For banks issuing tokenized deposits, this classification provides clarity: deposit tokens are bank products supervised by banking regulators, not novel crypto assets requiring new regulatory approaches.

Genius法案同時明訂,合格發行機構所發行的支付型穩定幣,不屬於聯邦證券法下之「證券」,也非商品交易法下之「商品」,因此不受SEC與CFTC管轄。此一分類對於發行代幣化存款的銀行而言,相當明確:存款代幣屬於銀行產品,由銀行監理單位監管,而非另類加密資產,不須嶄新的監理模式。

All stablecoin issuers under the GENIUS Act must comply with the Bank Secrecy Act, implementing anti-money-laundering and counter-terrorist-financing measures. Banks already maintain robust BSA compliance programs as a core regulatory requirement, giving them infrastructure advantage over nonbank stablecoin issuers building compliance capabilities from scratch.

所有受Genius法案規範的穩定幣發行者,均須遵守銀行保密法(BSA),實施反洗錢及防制資恐措施。銀行本來就已建置完整的BSA合規體系,這讓銀行在合規基礎設施上,較新興的非銀行穩定幣發行者具備顯著優勢。

The know-your-customer requirements embedded in banking regulation align naturally with permissioned blockchain architectures. Distributed ledger systems used for tokenized deposits maintain know-your-customer, anti-money-laundering, and

銀行法規對「認識你的客戶(KYC)」的要求,自然與權限制區塊鏈相得益彰。代幣化存款所運用的分散式帳本系統,均保留KYC、反洗錢以及...counter-terrorist-financing checks as integrated components of the infrastructure. When a transaction initiates, the system validates that all parties are properly identified and authorized before allowing execution. This contrasts sharply with public cryptocurrency systems where pseudonymous addresses can receive funds without identity verification, creating ongoing regulatory friction.

在基礎設施中,反恐融資檢查作為整合性元件運作。當交易啟動時,系統會驗證所有參與方是否已正確身分識別且具備授權,才允許執行。這與公用型加密貨幣系統形成鮮明對比,後者允許具匿名性的地址在未經身分驗證下接收資金,持續引發合規上的摩擦。

Transaction monitoring and suspicious activity reporting become more straightforward on shared ledgers where all participants can see relevant transactions. Rather than piecing together activity across multiple correspondent banks and jurisdictions, a tokenized deposit network provides transparent transaction history visible to relevant authorities. Banks can implement automated monitoring tools examining blockchain data continuously, flagging unusual patterns for investigation.

在所有參與者皆可見相關交易的共享帳本上,交易監控及可疑活動通報變得更加直接明瞭。與其要穿梭於多家代理銀行及跨法域拼湊資料,代幣化存款網路則能提供對相關主管機關透明可見的交易歷史。銀行可部署自動化監控工具,持續檢查區塊鏈數據,標記異常模式以供調查。

The GENIUS Act requires stablecoin issuers to possess technical capability to seize, freeze, or burn payment stablecoins when legally required and to comply with lawful orders. Permissioned blockchain architectures can implement such controls through administrative smart contracts allowing authorized parties to lock or transfer tokens in response to legal process. This capability is essential for law enforcement and sanctions enforcement but challenging to implement in truly decentralized systems.

GENIUS法案要求穩定幣發行人具備在法律要求時,查封、凍結或銷毀支付型穩定幣的技術能力,並必須配合法律命令。許可型區塊鏈架構可透過管理智能合約來實現此類控管,允許授權方在接獲法定程序時鎖定或移轉代幣。這項能力對於執法與制裁執行至關重要,但在真正去中心化系統下很難實現。

Sanctions compliance illustrates both the advantages and challenges of tokenized deposits. Office of Foreign Assets Control regulations prohibit transactions with sanctioned entities, and banks must screen all payments against sanctions lists. The GENIUS Act explicitly subjects stablecoin issuers to Bank Secrecy Act obligations including sanctions compliance, requiring sanctions list verification. Tokenized deposit systems can implement automated sanctions screening before transaction execution, blocking prohibited transfers before they settle rather than identifying violations after the fact.

制裁合規展現出代幣化存款的優點與挑戰。美國海外資產管制辦公室(OFAC)規定禁止與受制裁實體進行交易,銀行必須將所有付款與制裁清單比對。GENIUS法案更明確規定穩定幣發行人需遵循《銀行保密法》,包括必須實現制裁合規並進行清單驗證。代幣化存款系統可在交易執行前自動篩查制裁狀況,於未結算前即阻擋被禁止的轉帳,而非事後才發現違規。

However, the programmability of tokenized deposits creates potential compliance challenges. If a smart contract automatically executes payments based on conditions without human review, how do banks ensure each automated payment complies with sanctions requirements? The answer requires embedding compliance checks within smart contract logic or limiting automation to low-risk scenarios with sufficient human oversight. This tension between automation efficiency and compliance assurance will require ongoing attention as smart contract sophistication increases.

然而,代幣化存款的可程式化特性也帶來潛在的合規挑戰。若智能合約於無人審查下自動執行付款,銀行該如何確保每筆自動付款均符合制裁要求?答案是在智能合約邏輯內嵌入合規檢查,或者將自動化限制於風險較低且有人參與監控的場景。自動化效率與合規保證間的這種拉鋸,將隨著智能合約技術日益複雜而需持續關注。

The European Union's regulatory approach has evolved rapidly, with MiCA providing comprehensive framework for crypto assets. MiCA's provisions covering asset-referenced tokens and e-money tokens took effect on June 30, 2024, imposing strict reserve requirements, whitepaper disclosures, and authorization processes for stablecoin issuers. Crypto Asset Service Providers must begin applying for licenses starting January 2025, with an 18-month grandfathering period allowing existing providers to continue while transitioning to full compliance.

歐盟的法規架構快速演進,MiCA法案為加密資產提供了完整框架。MiCA針對資產參照型代幣與電子貨幣代幣的規範於2024年6月30日生效,對穩定幣發行人施加嚴格的準備金要求、白皮書資訊揭露及發行授權程序。自2025年1月起,加密資產服務提供商須開始申請許可證,並有18個月過渡期,讓現有服務商在轉型全盤合規前得以繼續運作。

MiCA divides stablecoins into e-money tokens backed by single fiat currencies and asset-referenced tokens backed by multiple assets. E-money tokens face requirements similar to electronic money under existing EU e-money directives, requiring issuers to be licensed in the EU, maintain fully backed reserves, and publish detailed disclosures. Issuers must maintain at least 30 percent of reserves in highly liquid assets, with all reserves held in EU financial institutions.

MiCA將穩定幣區分為單一法幣支持的電子貨幣代幣與多重資產支持的資產參照型代幣。電子貨幣代幣需遵循現行歐盟電子貨幣指令相似的要求,發行人在歐盟需取得執照,維持全額準備金支持,並公開詳細資訊。發行人還必須至少將30%準備金放在高流動性資產,且所有準備金須存放於歐盟金融機構。

Both GENIUS Act and MiCA require regulated stablecoin issuers to hold reserves in conservative one-for-one ratios against all stablecoins in circulation, with deposits held in bankruptcy-protected structures. Both frameworks entitle holders to redemption at par and impose obligations on exchanges and service providers handling stablecoins. The convergence between U.S. and EU approaches, despite different starting points and political contexts, reflects shared policy goals around consumer protection, financial stability, and regulated money.

GENIUS法案與MiCA皆要求受監管的穩定幣發行人,對流通之所有穩定幣以審慎且一對一比例持有準備金,並存放於具破產保護的結構內。兩者均保障持有人可按面額贖回,同時對涉足穩定幣的交易所與服務商施加義務。美歐兩地雖出發點與政治背景不同,但在消費者保護、金融穩定及規管貨幣等政策目標上已呈現趨同。

For banks issuing tokenized deposits in multiple jurisdictions, the proliferation of regulations creates compliance complexity but not fundamental uncertainty. Banks operate across borders routinely, managing compliance with different regulatory regimes as part of normal operations. The key advantage is that tokenized deposits generally fit within existing banking regulation rather than requiring entirely new frameworks.

對於在多個司法管轄區發行代幣化存款的銀行而言,法規擴張增加了合規複雜度,但並未產生根本性不確定性。銀行本就習慣跨境經營,並將遵守各地法規作為例行營運的一部分。其關鍵優勢在於,代幣化存款大多可納入現有銀行監理框架,而無須制定全新結構。

Asia-Pacific jurisdictions have taken varied approaches. Singapore's Monetary Authority of Singapore backed Partior's development and praised it as "a global watershed moment for digital currencies, marking a move from pilots and experimentations towards commercialization and live adoption". Singapore has established itself as a supportive jurisdiction for financial innovation while maintaining strong regulatory oversight, creating an attractive environment for blockchain-based financial services.

亞太地區各國迥異。新加坡金融管理局(MAS)支持Partior專案發展並稱其為「數位貨幣全球分水嶺,象徵從測試到商業化及落地應用的重要里程碑」。新加坡在維持嚴格監理的同時,成功塑造金融創新支持者形象,為區塊鏈金融服務創造優勢環境。

Hong Kong similarly positioned itself as a digital asset hub, though maintaining careful regulatory controls. Hong Kong's Stablecoin Ordinance, passed in May 2025, requires all stablecoin issuers backed by the Hong Kong dollar to obtain licenses from the Hong Kong Monetary Authority, maintain high-quality liquid reserve assets equal to par value of stablecoins in circulation, and submit to strict requirements including AML/CFT compliance and regular audits.

香港亦定位為數位資產樞紐,同時維持嚴謹管理。2025年5月通過的《穩定幣條例》要求所有以港元為擔保的穩定幣發行人,必須向香港金融管理局申領牌照,並以高品質流動資產按流通量面值備足準備金,同時接受嚴格要求,包括反洗錢/打擊資恐合規及定期審計。

Japan's regulatory approach emphasizes consumer protection and financial stability, with the Financial Services Agency maintaining stringent oversight of crypto activities. Tokenized deposits issued by licensed banks would fall under existing banking regulation, though specific guidance continues developing as the technology matures.

日本專注於消費者保護與金融穩定,由金融廳對加密活動實施嚴密監督。受執照銀行發行的代幣化存款屬於現行銀行法規框架下,隨技術逐步成熟,具體指引亦在持續制定中。

The regulatory landscape remains dynamic, with frameworks continuing to evolve as regulators observe market developments and industry practices. However, the fundamental regulatory advantage of tokenized deposits is already clear: they work within established legal and regulatory structures rather than challenging them. Comptroller of the Currency Jonathan Gould stated that the GENIUS Act "will transform the financial services industry" and that "the OCC is prepared to work swiftly to implement this landmark legislation", indicating regulatory receptiveness to facilitating tokenized deposit adoption.

監理格局亦非常動態,政策框架會隨監管機關觀察市場發展及產業實務而演進。不過,代幣化存款的基本監管優勢已非常明顯:其運作於既有法規結構之下,而非衝擊傳統體系。美國貨幣監理署署長Jonathan Gould表示GENIUS法案「將徹底改變金融服務業」,並指出「OCC已準備迅速推動該里程碑法案的落實」,顯示監管機構已為推動代幣化存款採納做好準備。

The on-chain transparency of blockchain systems provides regulators with new oversight tools. Rather than requesting reports or conducting examinations based on samples, regulators could potentially observe all transactions on permissioned networks in real time. This surveillance capability raises privacy concerns but offers unprecedented regulatory visibility into financial activity. The balance between transparency for oversight and confidentiality for commercial operations will require ongoing negotiation as blockchain adoption expands.

區塊鏈系統的鏈上透明度賦予監理者全新監督工具。監理機關將能夠在許可網路上即時觀察所有交易,而無須再仰賴報表或抽樣檢查。此種監監能力雖引發隱私疑慮,但賦予對金融活動史無前例的可見度。如何在監督透明與商業機密間取得平衡,隨區塊鏈應用擴大勢必成為持續協商焦點。

One significant area requiring continued regulatory development involves the treatment of smart contracts within banking law. When a smart contract automatically executes a payment based on programmed conditions, who bears liability if the outcome differs from what parties intended? How should courts interpret smart contract code when disputes arise? Should banks be held to the same standards for smart contract execution as for manual transaction processing? These questions lack definitive answers, and different jurisdictions may develop different precedents.

另一個亟需監理發展的重大領域是如何將智能合約納入銀行法律規範。當智能合約依編程條件自動執行付款時,若結果與當事人預期不符,責任究竟歸屬何方?法院遇到爭議時,該如何解讀智能合約原始碼?銀行於執行智能合約時,標準是否應與人工處理交易相同?這些問題尚無明確結論,各地法域亦可能發展出不同先例。

Cross-border regulatory harmonization would significantly benefit tokenized deposit development, but achieving such harmonization has proven elusive even in traditional banking. The Basel Committee on Banking Supervision coordinates international banking regulation but allows substantial national discretion. The Financial Stability Board published recommendations on global stablecoin arrangements including cross-border collaboration, transparent disclosures, and compliance with AML/CFT measures, providing high-level principles but leaving implementation details to national authorities.

跨境監管協調將大幅促進代幣化存款發展,但協調一致即使在傳統銀行業都極為困難。巴塞爾銀行監理委員會負責協調國際銀行法規,但允許成員國高度自主。金融穩定委員會則針對全球穩定幣安排提出建議,包括跨境協作、資訊透明及遵守AML/CFT,僅提供高層原則,實際細節則交由各國落實。

For tokenized deposits to realize their full potential for global liquidity management, regulatory frameworks must enable cross-border flows while preserving national policy autonomy and preventing regulatory arbitrage. This tension between integration and sovereignty characterizes international financial regulation generally and will shape tokenized deposit regulation specifically.

如要充分發揮代幣化存款於全球流動性管理的潛力,監管框架必須支持跨境流動,同時維護國內政策自主及防止監管套利。這種整合與主權間的張力,不僅是國際金融法規一貫特色,也將深刻影響代幣化存款之規管發展。

Data localization requirements illustrate the challenge. Some jurisdictions require financial data to be stored within their borders, complicating global blockchain networks that inherently distribute data across multiple nodes potentially in multiple countries. Technical solutions like partitioned ledgers or encryption can address some concerns, but regulatory acceptance varies.

資料在地化要求充分展現監管挑戰。有些國家規定金融數據必須存放於本國境內,這對天生分布於多國多節點的全球區塊鏈網路造成難題。分割帳本或加密等技術可部分因應,但各國監管接受度不一。

The Digital Operational Resilience Act in the EU represents another regulatory development affecting tokenized deposits. DORA mandates incident reporting, risk management systems, and strong cybersecurity measures for financial entities including crypto asset service providers. Banks deploying tokenized deposits must ensure their blockchain infrastructure meets operational resilience standards, including the ability to continue operations during outages, recover from failures, and respond to cyber attacks.

歐盟的《數位營運韌性法案》(DORA)則是另一項影響代幣化存款的監理發展。DORA要求包括加密資產服務供應商在內的金融機構,必須進行事件通報、建立風險管理系統及採取高強度資安措施。銀行若部署代幣化存款,需確保其區塊鏈基礎設施達到營運韌性標準,包括當掉線時仍能維持運作、從故障中恢復、並可應對網路攻擊。

Looking forward, the regulatory environment for tokenized deposits will likely remain broadly favorable given that banks operate under established supervision and that tokenized deposits simply represent technological evolution rather than regulatory revolution. Specific rules will continue developing as regulators gain experience with blockchain-based banking and as industry practices mature. The fundamental compatibility between tokenized deposits and existing regulatory frameworks means regulatory development will refine approaches rather than

展望未來,代幣化存款的監理環境預期將持續友善,因為銀行本就受既有監理,且代幣化存款僅是技術演進、非規範革命。隨監管機關累積區塊鏈銀行實務經驗產業慣例日益成熟,細部規則仍會繼續完善。代幣化存款與現行監管體系的本質相容性,意味著監管發展將是調整細節、而非大幅重構。determine whether tokenized deposits are permissible at all.

這種監管整合相較於監管較少的加密貨幣替代品,代表了一項重大優勢。雖然監管明確有時看似限制創新,但同時也讓機構級採用成為可能、並可大規模推展。企業財務主管、金融機構和大規模用戶在部署新技術到關鍵營運時,都需要監管確定性。代幣化存款可以提供這種確定性,而真正去中心化的加密貨幣則做不到,因此它們比起建立於傳統金融外平行系統,更有可能徹底改造主流金融基礎建設。

The Real Competition: Stablecoins, CBDCs, and Tokenized Deposits

當前的數位貨幣格局包含多種重疊分類:由商業銀行發行的代幣化存款、由非銀行實體發行的穩定幣、由貨幣當局發行的央行數位貨幣,以及由特定機構發行的電子貨幣代幣。瞭解這些類型之間的差異及其對不同應用場景的相對優勢,有助於釐清哪種數位貨幣可在各種情境中勝出。

比較首先從發行方和權益性質談起。代幣化存款由持牌商業銀行發行,代表對該銀行的請求權,並由銀行資產負債表全額背書,受資本與流動性規範約束。穩定幣通常由非銀行實體發行,並由與發行機構經營資產分離的準備金支持,這些準備金通常存在特殊目的載體或信託架構中。央行數位貨幣則由中央銀行發行,代表對央行負債的直接請求權,使其在貨幣體系層級上與實體現金和銀行準備金並列最高。

相應地,資產支持與準備結構也有所不同。代幣化存款不需額外準備金,因其本質只是現有銀行存款的數位化,這些存款本身已由銀行資產組合和資本緩衝支持。銀行發行代幣化存款,並非創造新貨幣,而是將現有存款負債「代幣化」。根據例如GENIUS法案等規範,穩定幣發行方必須以全額準備支持,允許的準備資產包含現金、受保存款、國庫券、附買回、貨幣市場基金與央行準備金。央行數位貨幣則以央行資產負債表為後盾,其主要組成為國債、外匯準備,有時也包含黃金。

監管處遇則反映上述結構差異。根據GENIUS法案,發行存款代幣的銀行適用其現行銀行執照與監理規範,而非銀行穩定幣發行方則需取得聯邦或州級認證支付型穩定幣發行人資格。聯邦與州監管機關必須針對穩定幣發行方制定專屬資本、流動性及風險管理規定,但條文則豁免其遵循傳統銀行資本標準。央行數位貨幣將受央行法定職權與監督,具體監管依CBDC設計而異。

存取與發行模式也大不相同。代幣化存款僅提供給發行銀行的客戶,且多限於機構與企業客戶,而非零售用戶。穩定幣依發行方業務模式和監管約束可廣泛流通,有些穩定幣專攻機構市場、有些則力求零售普及化。央行數位貨幣可能呈現多種型態:零售型CBDC讓全民持有數位央行貨幣;批發型CBDC僅供金融機構間清算;或者采混合型分層存取。

可程式化程度取決於具體實作而非分類。無論是代幣化存款還是穩定幣,都可嵌入智能合約邏輯,但許可型的代幣化存款網路因與銀行基礎設施深度整合,可能提供更精進的可程式化功能。迄今多數CBDC設計以基本支付功能為主,較不強調進階可程式化,這更多是政策選擇而非技術上受限。

對許多機構用戶而言,核心區別在於對手方風險。代幣化存款承擔發行銀行的信用風險,但適用存款保險(有額度限制)、資本規範與監管監督。若超出保險額度,高額存款則需考量銀行信用等級與倒閉時的清算機制。穩定幣所涉風險則因結構而異。GENIUS法案規定穩定幣持有人在破產時對準備資產有第一順位請求權,具一定保障,但與銀行存款相比風險型態不同。CBDC則因央行可創造基礎貨幣來履約,理論上信用風險極低,惟若發生極端情境如貨幣危機、主權違約,甚至CBDC也可能受影響。

收益性方面亦有差異。GENIUS法案禁止合格支付型穩定幣發行方對持有人支付利息,令穩定幣成為無息資產。此限制旨在避免穩定幣直接與銀行存款爭奪資金。代幣化存款則可為計息或不計息產品,視銀行設計如同傳統存款一般。存款代幣理論上可支付利息,例如JPMorgan的JPMD就可對持有人付息,讓代幣化存款具穩定幣所不及的彈性。大多數零售型CBDC設計為無息貨幣替代品,而批發型CBDC則如同銀行準備金,可能支息。

互通性與網路效應亦是一大維度。流通於公有鏈的穩定幣可在錢包間自由流動並對接DeFi協議,於加密生態實現高度互通,但與傳統金融基礎設施整合有限。代幣化存款主要在銀行網路內運作,與現有金融體系高度整合,若需與公有鏈生態互動則須透過專用橋接或合作。CBDC理論上可依設計選擇是否與私人銀行系統或公用加密網路互通,但多數方案優先考慮與現有金融體系兼容。

擴展性則依系統架構而定。公有鏈穩定幣受限於鏈本身的處理能力與延遲,但L2解決方案及替代鏈已大幅提升效能。許可型區塊鏈的代幣化存款因驗證節點有限且專為效能優化,可達高吞吐量,無須兼顧去中心化。批發型CBDC可能採用類似的許可型架構,效能媲美代幣化存款。而零售型CBDC由於需服務全國人口、每日數十億筆交易,面臨更嚴峻的可擴展性挑戰。

隱私層面差異明顯。公有鏈穩定幣提供偽匿名隱私:交易全透明,但地址與身份未必直接關聯。有些重視隱私的穩定幣會採用零知識證明等技術加強保護。許可型網路上的代幣化存款對外界隱私更高,但發行銀行與監管單位則能查閱所有交易。CBDC則引發重大隱私疑慮,尤其零售型CBDC可能讓央行完全掌握公民消費資訊,帶來監控風險,因而在多數國家面臨政治阻力。

針對跨境支付,各類型各有強項。穩定幣經公有鏈可於全球即時流通,無需代理銀行,但法遵與AML/KYC管制在實務上限制其優勢。代幣化存款能於銀行網路內實現快速跨境清算,但需銀行間有合作或透過中介平台。CBDC則可藉央行間雙邊協議、多邊平台、或跨系統協議促進跨境支付,但多數仍停留於概念階段。

各類型在其強項應用場景中展現不同策略利基。穩定幣適合開放型加密生態,方便用戶在無特定銀行往來下自由交易,服務加密原生用戶、DeFi應用,以及在監管不確定下,強調公有鏈彈性的場景。代幣化存款則優於機構財務管理、企業支付,以及重視銀行關係、監管明確與與現有金融體系整合多於無許可存取的應用。CBDC適用於實現貨幣政策目標、強化支付基礎設施韌性、推動金融普惠,但因政治和技術挑戰,推動較為遲緩。

市場競爭並非你死我活。不同形式數位貨幣可共存,服務不同用戶與用例。一家大型企業可能會以代幣化存款進行資金管理與企業支付,使用穩定幣於特定區塊鏈應用,傳統現金與存款則用於…routine operations. An individual might use CBDCs for everyday payments, tokenized deposits through banking relationships for savings and investments, and stablecoins for crypto trading or cross-border remittances.

例行操作。一個人可能會將央行數位貨幣(CBDC)用於日常支付,透過銀行關係將資金存入代幣化存款以作為儲蓄和投資用途,並且使用穩定幣來進行加密貨幣交易或跨境匯款。

The more relevant question is which form will dominate mainstream institutional finance. Here tokenized deposits hold significant advantages: regulatory clarity, banking relationship integration, sophisticated functionality, and alignment with existing corporate treasury operations. A consortium of nine banks including Goldman Sachs and Citigroup is working to launch a G7-backed stablecoin, with the market potentially reaching 50 trillion dollars in payments by 2030, suggesting major banks see strategic importance in both tokenized deposits and bank-issued stablecoins.

更關鍵的問題是,哪一種形式將主導主流機構金融領域。在這方面,代幣化存款具有明顯優勢:法規明確、可與銀行關係整合、具備高度複雜的功能,並且能與現有的企業財資操作相結合。包括高盛(Goldman Sachs)和花旗集團(Citigroup)在內的九家銀行組成的聯盟,正致力於推出一款獲得G7支持的穩定幣,預計到2030年,該市場的支付規模可能達到50兆美元,這顯示主要銀行已將代幣化存款和銀行發行的穩定幣視為戰略重點。

Citi revised its stablecoin forecast in September 2025, predicting the market could reach 1.9 trillion dollars by 2030 in a base scenario or as much as 4 trillion dollars if adoption accelerates. These projections encompass both independent stablecoins and bank-issued variants, reflecting growing confidence that digital money will capture substantial share of payment volumes.

花旗集團於2025年9月修訂了其對穩定幣市場的預測,認為在基本情境下,到2030年市場規模可能達到1.9兆美元,若採用速度加快,甚至可能高達4兆美元。這些預測同時涵蓋了獨立發行的穩定幣與銀行發行的穩定幣,這反映出業界對數位貨幣能夠占據大量支付份額的信心日益增強。

The policy debate around CBDCs illustrates political sensitivities that do not affect tokenized deposits. Senator Ted Cruz sponsored legislation to block the Federal Reserve from introducing a retail CBDC, claiming it could be used to track American citizens. These concerns reflect deep-seated tensions around government power, financial privacy, and the role of central banks. Tokenized deposits avoid these political challenges because they preserve the existing two-tier banking system with commercial banks intermediating between central banks and customers.

圍繞CBDC的政策討論凸顯出一些並不會影響代幣化存款的政治敏感性。參議員克魯茲(Ted Cruz)曾提出立法阻止聯邦準備理事會發行零售型CBDC,聲稱這可能被用來追蹤美國公民的行為。這些擔憂反映了人們對政府權力、金融隱私、以及中央銀行角色的深層緊張關係。代幣化存款則避免了這些政治挑戰,因為它保留了現有的雙層銀行體系,讓商業銀行持續作為央行與客戶之間的中介。

The future monetary system will likely combine multiple forms of digital money with differentiated roles. Central bank money (reserves and potentially wholesale CBDCs) provides the settlement layer. Commercial bank money (traditional deposits and tokenized deposits) serves as the primary medium for most economic activity, leveraging banks' credit creation and customer relationship capabilities. Stablecoins and potentially retail CBDCs provide alternatives for specific use cases where traditional banking has limitations. E-money tokens serve niche markets particularly in payments where specialized providers can offer better service than general-purpose banks.

未來的貨幣體系很可能會結合多種數位貨幣形式,各自發揮不同的角色。中央銀行貨幣(準備金以及可能出現的批發型CBDC)將作為結算層。商業銀行貨幣(傳統存款和代幣化存款)則是大多數經濟活動的主要媒介,發揮銀行的信貸創造與客戶關係等優勢。穩定幣以及潛在的零售型CBDC則為傳統銀行難以覆蓋的特定應用場景提供替代方案。電子貨幣代幣則服務於特定利基市場,尤其是在某些支付領域,專業服務供應商可提供優於通用型銀行的服務。

This multi-layered ecosystem requires interoperability protocols enabling value transfer between different forms of digital money. The GENIUS Act directs the Federal Reserve, in collaboration with the Treasury, to create reciprocal arrangements with foreign jurisdictions having substantially similar stablecoin regulatory regimes to facilitate international transactions and interoperability. Similar frameworks will need to develop for interoperability between tokenized deposits, stablecoins, and potential CBDCs.

這個多層次生態系需要具備互通協議,才能讓不同型態的數位貨幣進行價值轉移。《GENIUS法案》要求美國聯準會與財政部合作,和具有大致相同穩定幣監管體系的外國司法管轄區建立互惠安排,以促進國際交易和互通性。未來還需要發展類似的框架,實現代幣化存款、穩定幣和未來可能推出的CBDC之間的互通。

The competitive landscape continues evolving as regulatory frameworks crystallize and market participants refine their strategies. Banks increasingly recognize that they must develop digital money capabilities or risk disintermediation by stablecoin issuers and technology companies. Banking experts note that banks of all sizes need a stablecoin strategy now, with a clear vision of how they will connect customers, partners, and developers into the next generation of money movement. This competitive pressure drives rapid development of tokenized deposit infrastructure and related capabilities.

隨著監管框架日益成型,市場參與者戰略也在調整,競爭態勢正持續演變。銀行越來越意識到,若不發展數位貨幣相關能力,將有被穩定幣發行商和科技公司邊緣化的風險。銀行專家指出,各種規模的銀行都需要即刻制定穩定幣策略,明確如何將客戶、合作夥伴和開發者對接至下一代資金流動平台。這股競爭壓力加速了代幣化存款基礎建設及相關能力的迅速發展。

Ultimately, tokenized deposits hold structural advantages for serving institutional finance: regulatory clarity, banking supervision, interest-bearing capability, sophisticated programmability, and natural integration with existing treasury operations. Stablecoins will continue serving crypto-native ecosystems and use cases where openness and permissionless access provide value. CBDCs, if implemented at scale, would reshape monetary systems but face formidable political and technical hurdles. The transformation of global finance will likely proceed through tokenized deposits upgrading the core infrastructure of commercial banking rather than through wholesale replacement of banks by stablecoins or central bank digital currencies.

最終,代幣化存款因具有法規明確、銀行監管、可計息、高度可編程,以及與現有財資操作自然整合等結構性優勢,將成為機構金融服務的關鍵利器。穩定幣則將繼續服務於原生加密生態系以及講究開放性和無需許可存取的特定應用場景。若CBDC能大規模落地,勢必將重塑貨幣體系,但目前仍面對嚴峻的政治和技術挑戰。全球金融的轉型或將主要經由代幣化存款升級商業銀行的核心基礎設施,而非完全以穩定幣或CBDC取代銀行體系。

The New Banking Stack

理解代幣化存款不僅需要檢視單一產品,更需要洞察其啟動的新技術與營運架構。這個新興的銀行技術堆疊(banking stack),代表著金融機構在網路上創造、轉移與最終結算價值的基本重構。

The foundation layer consists of the distributed ledgers themselves: permissioned blockchains or distributed ledger networks where tokenized deposits exist and transactions execute. This layer provides the shared data substrate that replaces separate bank databases and message-passing systems. Whether implemented on Ethereum-derived chains, purpose-built enterprise blockchains like Hyperledger, or hybrid architectures, the core function remains: maintaining a synchronized ledger of tokenized liabilities accessible to all authorized participants.

基礎層由分布式帳本本身組成:包括私有區塊鏈或分布式帳本網路,代幣化存款即存在於此並於此執行交易。這一層提供共享資料底層,替代了傳統各家銀行獨立資料庫與訊息傳遞系統。無論是建構於以太坊系區塊鏈、專為企業打造如Hyperledger的聯盟鏈,或其他混合架構,核心職責始終一致:維護一份同步化、可由所有授權參與者存取的代幣化債務帳本。

The token issuance layer sits above this foundation, comprising the systems and processes through which banks create tokenized deposits representing their liabilities. This layer bridges traditional banking systems and blockchain infrastructure. When a corporate client instructs the transfer of funds into tokenized form, the bank debits the traditional deposit account, mints equivalent tokenized deposits on the blockchain, and provides the client with access to those tokens. The reverse process redeems tokens, burning them on the blockchain and crediting traditional accounts.

在基礎層之上,是代幣發行層,涵蓋銀行創建代幣化存款、代表其負債的系統與流程。這一層承接傳統銀行系統與區塊鏈基礎設施。當企業客戶指示將資金轉為代幣化形式時,銀行會扣除傳統存款帳戶金額,在區塊鏈上鑄造等值的代幣化存款,並將該代幣分配給客戶。相反地,贖回流程則是在區塊鏈上銷毀代幣,並將金額返還至傳統帳戶。