比特幣 網絡於 2028 年 3 月的下一次減半,將在加密史上最成熟的機構投資環境下展開——目前逾 10% 的比特幣流通量由企業及 ETF 掌控,相較 2020 年減半時不到 1%。

這種從散戶主導轉向機構控制的根本改變,結合過往週期所沒有的完整法規和技術架構,預示 2028 年減半將更像是「供給衝擊放大器」,而非單純的投機催化劑。歷史上減半事件曾帶來 93 倍至 7 倍的價格效應,但 2028 年的環境已變:ETF 保管金庫現有 140 萬枚比特幣,企業金庫另有 85.5 萬枚,形成本質性需求,可望使比特幣即使漲幅較以往溫和,價格仍能穩步提升。

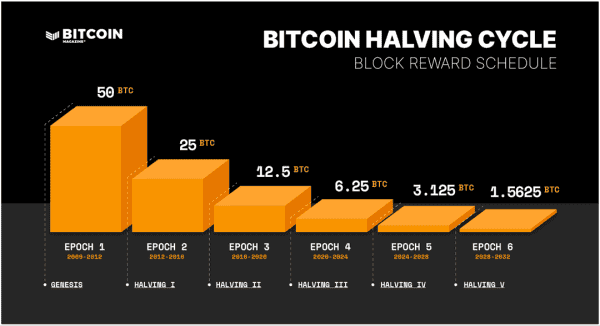

數學機制本質不變:區塊獎勵將從每區塊 3.125 枚減半至 1.5625 枚,每日新產出從 450 枚降至 225 枚,屆時剩餘約 127.5 萬枚尚未開採。但經濟環境徹底革新。光是 BlackRock 的比特幣 ETF 管理資產規模高達 710 億美元,MicroStrategy 則持有逾 58.2 萬顆,市值超過 620 億美元。

機構資本的進駐,為比特幣提供了過往未見的價格支撐與長線需求壓力,供給減少將與結構性需求同步作用,有機會拉長週期、墊高底部。

推動比特幣數位黃金論的稀缺數學

比特幣的貨幣政策精確無比,遠勝人類過往任何資產。至 2025 年 8 月,已開採 1972.5 萬枚,占全網 2100 萬枚硬上限的 94%。剩下僅約 127.5 萬枚,將以挖礦方式緩慢釋出,直至 2140 年最後一枚「聰」進入流通。由於減半機制的幾何進程,2020 年前已開採超過 87%,而剩下 13% 則需花費逾百年時間。

每經 210,000 個區塊(約四年),協議自動將區塊獎勵減半,無需人為干預。歷年為:2009 - 2012 年每區塊 50 枚,2012 - 2016 剩 25 枚,之後到 2020 年為 12.5 枚,2020 - 2024 年 6.25 枚,至今為 3.125 枚,2028 年 3 月減半後僅剩 1.5625 枚。

此減半機制造就了極高的「存量對流量比」(stock-to-flow),目前已超越白銀趨近黃金。該比率衡量現有庫存與年新增供給,比特幣現值約 58,預計 2028 減半後將升至 116 左右。黃金約 70,產業金屬多處於 1-5,彰顯比特幣在價值儲存領域的稀缺性。

能源結構也同步升級。現代 ASIC 礦機減半後每開採一枚比特幣耗電約 854,404 度(千瓦時),是減半前的近兩倍。算力亦已升至 898.86 EH/s,說明即使獎勵降低,市場力量仍能維持網絡安全。難度每 2,016 區塊自動調整,確保區塊間隔平均 10 分鐘,穩定產出。

用戶普遍理解約有 3-4 百萬枚比特幣永久丟失(遺失私鑰、硬體損壞或錢包無法取回),實際流通數可能僅 1,600 萬至 1,700 萬,這使得稀缺效應遠超協議本身設計,因這些永久凍結的比特幣,產生無法逆轉的通縮壓力,任何央行或政府都無法透過增發或查封收回。

機構入場,重塑減半遊戲規則

從散戶主導到機構主導,是比特幣自誕生以來最關鍵的結構變革。2020 年減半時,機構參與微乎其微;今天,BlackRock 的 IBIT ETF 單一產品就掌握逾 710 億美元的比特幣,整體 ETF 持有 140 萬枚,約占總流通量 6.8%。企業金庫再加 85.5 萬枚,使機構總持有超過流通量 10%。

MicroStrategy 在企業應用方面領先,握有 58.2 萬枚,總值逾 620 億,採取財庫定期投入策略,引領數十家上市企業將部分資本配置比特幣。該公司目標在 2027 年前累積 840 億美元,現已執行約三分之一。Marathon Digital、Bitcoin Standard Treasury 等大型企業及 GameStop 也積極投入,GameStop 更通過「Project Rocket」計劃增資 15 億美元購比特幣。

機構累積對 2028 減半供需格局產生深遠影響。交易所儲備已降至 250 萬枚,創 2019 年以來新低;2024 年 11 月以來,機構從交易所提幣 42.5 萬枚,同期上市公司累積買入 35 萬枚,顯示機構買盤直接減少流通供給。

傳統金融代表如高盛,把比特幣 ETF 持倉猛增 88%,成為 BlackRock IBIT 最大單一股東,掌握 14 億美元資產。JPMorgan 也持有近 10 億美元 ETF,並對旗下 Chase 卡用戶推出加密貨幣服務。摩根士丹利、嘉信理財、PNC 銀行公開規劃比特幣整合,State Street 則打造機構級託管系統。

ETF 生態系的成熟,回應了機構對監管透明、流動性與效率的需求。2025 年 7 月發行的「實物申購/贖回」機制,加強 ETF 運作效率並降低追蹤誤差。2025 年 8 月比特幣和以太 ETF 週均成交高達 400 億美元,展現可與傳統資產類別匹敵的流動性。這助機構輕鬆參與比特幣多頭行情,無需直接持幣面對操作與監管風險。

企業金庫分配動力也與 ETF 投資不同。例如 MicroStrategy 視比特幣為優於現金和債券的財庫儲備,作為長期儲值而非短線交易。這種「鑽石手」持有者,在市場波動時減少拋售壓力,價格下跌時更能提供支撐。

礦業產業如何隨減半週期蛻變

比特幣挖礦經歷四次減半,從宅家業餘走向產業規格。每輪減半都考驗技術與資金調整,以維持利潤。全網算力增長量化此過程:從 2009 年近乎零到如今高達 898.86 EH/s,超越全球多數國家的計算能力。即使區塊獎勵由 50 枚減到現今的 3.125 枚,但因價格上漲和技術飛躍,使產業持續壯大。

如今主要礦企皆為上市公司,營運規模史無前例。Marathon Digital 在多個數據中心維持 29.9 EH/s 算力,計劃年底擴增至 50 EH/s。Core Scientific 自挖 19.1-20.1 EH/s,並拓展到 AI 與高效能運算託管。Riot、CleanSpark、TeraWulf 等大廠合計掌控全球不少算力,每次減半後產業愈趨集中,效率較低的礦工陸續淘汰。

礦池分佈反映地理及技術變遷。Foundry USA 以 33.49% 全球算力領先,代表北美地區崛起。AntPool 雖受中國監管影響仍有 18.24%。目前美國已占全球 40% 算力,遠超過早期週期時的微不足道比例,中國主導地位則由過往 75% 銳減。

技術進步對維持礦工利潤至關重要。現代 ASIC 礦機每 TH 只需 24-26 焦耳,初代設備動輒數百焦耳。最新機型目標 2025 年實現每 TH 5 焦耳,能效將提升三倍。 efficiency improvement that could offset halving impact on marginal mining operations. This efficiency race drives constant capital investment in newer equipment, with older miners becoming unprofitable as rewards decline.

提升效率可以抵消減半對邊際挖礦作業的衝擊。這場效率競賽促使不斷將資本投入更新的設備,隨著挖礦獎勵下降,舊型礦機逐漸變得無利可圖。

Energy consumption patterns have shifted toward renewable sources as mining operations seek cost advantages and regulatory compliance. Cambridge University data indicates Bitcoin mining now uses - 43% renewable energy - , including hydro, wind, solar, and nuclear power. Mining companies increasingly co-locate with renewable energy projects, providing demand for stranded energy resources that would otherwise go unutilized. Texas leads this trend, with mining operations balancing wind and solar intermittency while participating in grid stabilization services.

隨著挖礦業者追求成本優勢及符合法規要求,用電模式正逐漸轉向再生能源。根據劍橋大學資料,比特幣挖礦目前有 - 43% 來自再生能源 - ,包括水力、風力、太陽能及核能。越來越多礦業公司與綠能專案共址設廠,消耗原本無法有效運用的剩餘能源。德州在這一趨勢中居於領先地位,當地礦業利用風能與太陽能的波動性,並參與電網穩定化服務。

The economic reality facing miners heading into 2028 involves doubled production costs due to halving effects. Current mining operations become profitable at electricity costs below - $0.06 per kilowatt-hour - for older equipment, while next-generation miners extend profitability thresholds to higher energy costs. Post-halving, these thresholds effectively double, forcing industry consolidation among the most efficient operators with access to cheapest electricity sources.

礦工面對2028年時的經濟現實,是減半效應帶來產生成本加倍。以現有舊型礦機而言,當電價低於 - $0.06/kWh - 時尚能獲利,而次世代礦機則能將獲利門檻提升至更高的電力成本。於減半之後,這些門檻實質上會加倍,促使產業向效率最高且能取得最便宜電力資源的業者整併。

Mining revenue increasingly depends on transaction fees as block rewards diminish over successive halvings. Currently, transaction fees represent a small fraction of total mining revenue, but fee markets become increasingly important for long-term network security. During network congestion periods, daily fees can exceed $3 million, compared to historical averages below $1 million. The development of fee markets becomes critical for maintaining mining incentives beyond 2140 when block rewards reach zero.

隨著區塊獎勵經歷多次減半而遞減,礦工收入日益仰賴交易手續費。當前手續費僅占總挖礦收入一小部分,但手續費市場將對維護長期網絡安全愈發重要。在網路壅塞時,單日手續費收入曾超過300萬美元,對比歷史均值僅約100萬美元。發展手續費市場,將成為2140年區塊獎勵歸零後,維持挖礦誘因的關鍵。

Geographic distribution continues evolving due to regulatory changes and energy economics. While China's mining ban forced massive relocations, countries like Kazakhstan, Russia, and Canada have attracted significant mining investment. The United States benefits from diverse energy markets, favorable regulations in states like Texas and Wyoming, and established financial infrastructure supporting publicly traded mining companies. This geographic diversification reduces regulatory risks while improving network decentralization.

隨著法規變化與能源經濟學影響,挖礦地理分布也持續演變。中國挖礦禁令使得大量礦場外移,哈薩克、俄羅斯與加拿大因此成為挖礦投資熱點。美國則受惠於多元能源市場、德州與懷俄明等州的有利法規,以及支持上市挖礦企業的金融基礎設施。這種地理多元化,降低了法規風險並提升了網路去中心化程度。

Historical halving impacts reveal evolving market patterns

Bitcoin's four completed halvings provide quantitative evidence for how supply reductions affect price discovery, though each cycle occurred within different market contexts that influenced magnitude and timing of price responses. The mathematical progression shows diminishing returns as Bitcoin matures, but also longer cycle durations and higher absolute price levels that maintain mining profitability despite reduced percentage gains.

比特幣已發生四次減半,為供給減少對價格發現產生何種影響,提供了定量依據。雖然每個週期的市場背景皆不同,導致價格反應的幅度與時間點也有所差異,但數學規律顯示隨著比特幣邁向成熟,報酬率呈現遞減現象,同時週期拉長且絕對價格上升,讓挖礦即使利潤百分比降低,獲利能力仍可維持。

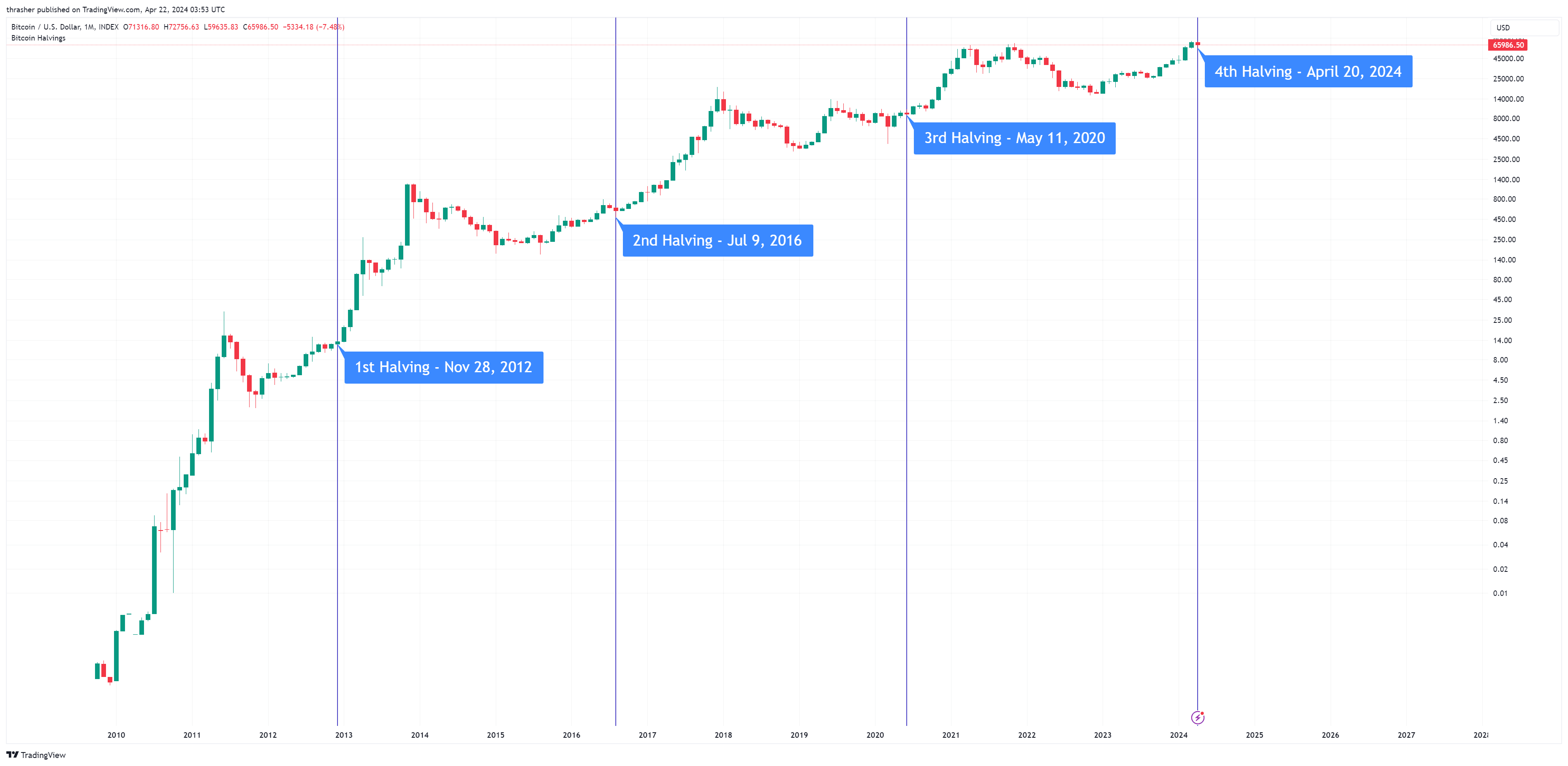

The November 28, 2012 halving established the foundational pattern when mining rewards dropped from 50 to 25 bitcoins per block. Bitcoin traded at - $12.35 on halving day - and reached - $1,147 within twelve months - , representing a staggering 9,188% gain. This inaugural halving cycle occurred during Bitcoin's experimental phase with minimal institutional awareness, limited exchange infrastructure, and CPU-based mining operations. The network's hash rate barely exceeded 25 terahashes per second, while daily trading volumes remained below $10 million.

2012年11月28日首次減半確立了基本走勢,當時每區塊獎勵由50枚降至25枚比特幣。減半當天價格為 - $12.35 - ,十二個月內來到 - $1,147 - ,大漲9,188%。這個首輪週期發生在比特幣的實驗期,機構參與幾乎為零、交易所基礎設施受限,且以CPU為主進行挖礦。全網算力僅略高於每秒25太哈希,日均交易量低於1,000萬美元。

The July 9, 2016 halving reduced rewards from 25 to 12.5 bitcoins per block amid growing institutional interest and professional mining operations. Bitcoin's halving day price of - $650.63 - preceded an initial 40% decline before the sustained bull market drove prices to - $19,987 by December 2017 - , a 2,972% gain over seventeen months. This cycle featured the emergence of cryptocurrency derivatives, regulated exchanges, and ASIC mining equipment that dramatically increased network security to 1.5 exahashes per second.

2016年7月9日第二次減半,區塊獎勵降至12.5枚,當時機構關注升高、挖礦步入專業化。減半日價格為 - $650.63 - ,隨後先跌40%,再展開多頭走勢,至2017年12月來到 - $19,987 - ,十七個月內暴漲2,972%。這一輪特色是加密衍生品問世、受監管交易所興起,以及ASIC礦機大幅提升網路安全,算力暴增至每秒1.5艾哈希。

The May 11, 2020 halving coincided with COVID-19 pandemic uncertainty and early institutional adoption signals. MicroStrategy and Tesla's corporate treasury allocations during this cycle marked the beginning of institutional acceptance. Bitcoin's halving day price of - $8,821 - eventually reached - $69,040 by November 2021 - , representing a 683% gain over eighteen months. The concurrent DeFi boom and NFT speculation created additional demand for Bitcoin as a foundational cryptocurrency, while network hash rate expanded to 120 exahashes per second.

2020年5月11日第三次減半發生於COVID-19疫情不確定時期,並有機構買盤初現,例如MicroStrategy與特斯拉陸續配置比特幣作為公司資產。減半價格 - $8,821 - ,十八個月後漲至 - $69,040 - ,報酬683%。當時DeFi熱潮與NFT炒作拉抬比特幣基礎性需求,網路總算力增長至每秒120艾哈希。

The April 20, 2024 halving broke historical patterns by occurring after Bitcoin had already achieved new all-time highs in March 2024. The - $73,135 pre-halving peak - represented the first time Bitcoin reached record prices before a halving event, driven by ETF launches that generated over $9 billion in institutional inflows. Bitcoin traded at - $64,968 on halving day - before declining 16% in subsequent weeks, suggesting traditional "sell-the-news" dynamics as the event became widely anticipated.

2024年4月20日第四次減半打破以往慣例,因為在減半前比特幣已於2024年3月創下新高。 - $73,135 減半前高點 - 乃首次於減半前觸頂,主因ETF推出吸引超過90億美元機構資金流入。減半日價格 - $64,968 - ,數週後下跌16%,顯示「利多出盡」賣壓現象,因該事件已被廣泛預期。

Academic analysis reveals consistent statistical patterns across halvings despite different market contexts. Regression analysis demonstrates 95% confidence intervals for outperformance beginning 100+ days post-halving, with optimal timing windows occurring 400-720 days after each event. The average performance 500 days post-halving across the first three cycles exceeded 1,800% gains, though with decreasing magnitude as Bitcoin's market capitalization expanded.

學術分析顯示,儘管市場環境不同,減半週期後的統計型態具高度一致性。回歸分析呈現減半一百多天後,價格優於大盤表現的信心水準達95%,而最佳投資時窗介於400至720天之間。前三個減半週期,於減半後500天平均上漲逾1,800%,但隨市值擴大,漲幅遞減。

Mathematical models based on historical data predict the next cycle peak around November 2025, approximately 19 months after the 2024 halving. These models anticipate the following trough in November 2026, 31 months post-halving, based on extending historical cycle patterns. However, the unprecedented pre-halving all-time high and institutional demand structure suggest traditional timing models may require recalibration for current market conditions.

基於歷史資料的數學模型預測,下次牛市高點大約落在2025年11月,也就是2024年減半後大約19個月。根據延伸的週期規律,下一次低點則預估在2026年11月,約為減半後31個月。然而,此次出現史無前例的減半前新高與機構需求變化,意味傳統週期推算模型可能需因應現況調校。

The evolution from 93x gains in 2012 to 7x gains in 2020 demonstrates Bitcoin's maturation trajectory while absolute price increases remain substantial. Even diminished percentage returns translate to significant dollar appreciation as Bitcoin's price base expands. A theoretical 3x gain from $70,000 pre-2028 halving levels would reach $210,000, representing hundreds of billions in market capitalization increase despite modest percentage terms relative to early cycles.

從2012年漲幅93倍到2020年僅7倍,顯示比特幣不斷成熟。然而,隨著基期墊高,雖然%增幅下滑,絕對價格成長依然可觀。例如2028年前若自$70,000翻三倍至$210,000,市值仍可增加數千億美元,即使增幅遠不及早期週期。

Market microstructure has transformed across halving cycles as institutional participation increased. The 2012 cycle featured retail-dominated trading with high individual volatility. The 2016 cycle included early institutional players alongside sophisticated retail traders. The 2020 cycle mixed retail enthusiasm with emerging corporate adoption. The 2024 cycle demonstrated institutional flows dominating through ETF demand structure, creating different volatility patterns and recovery timelines compared to retail-driven historical cycles.

市場微觀結構隨減半週期與機構參與而劇變。2012年以散戶主導,波動大。2016年有早期機構與資深散戶共存。2020年散戶熱情融入企業採用。2024年則由ETF資金主導市場,波動型態與回升節奏與過去散戶驅動的週期明顯不同。

Corporate treasuries and ETFs reshape demand dynamics

The structural transformation of Bitcoin demand from speculative trading to strategic allocation fundamentally alters traditional halving economics. Unlike retail investors who often trade based on sentiment and technical analysis, institutional holders typically maintain positions through extended periods, creating sustained demand pressure that previous cycles lacked. This "strong hands" ownership pattern becomes increasingly significant as institutional allocation percentages continue expanding.

比特幣需求由投機轉向策略配置,徹底改變傳統減半經濟學。不同於傾向依市場情緒與技術分析短線操作的散戶,機構持有者多半長期持有,帶來過往週期所缺乏的穩定需求壓力。此種「強手」型持有模式,隨著機構配置比重不斷上升,其影響力將愈發重要。

BlackRock's IBIT ETF exemplifies institutional demand mechanics with - $71 billion in assets under management - and record-breaking inflows reaching - $6.35 billion in May 2025 alone - . The fund's success demonstrates institutional appetite for Bitcoin exposure through regulated financial products rather than direct cryptocurrency ownership. IBIT's - $4.2 billion single-day trading volume - in April 2025 exceeded many individual stock trading volumes, indicating Bitcoin's integration into traditional portfolio management strategies.

貝萊德IBIT ETF展現機構需求動能, - 管理資產達$710億 - ,2025年5月單月流入高達 - $63.5億 - ,屢創紀錄。該基金成績說明,機構尋求受監管的金融商品來持有比特幣,勝過直接持幣。2025年4月,IBIT單日交易量高達 - $42億 - ,超越不少單一股票,顯示比特幣已納入傳統資產配置策略。

The competitive dynamic between ETFs and corporate treasury adoption reveals different institutional approaches to Bitcoin investment. While ETFs provide diversified exposure for institutional investors managing multiple asset classes, corporate treasury allocation represents strategic decisions by individual companies to hold Bitcoin as a primary reserve asset. The second quarter of 2025 data shows - corporate treasuries acquired 131,000 bitcoins - compared to - 111,000 bitcoins added by ETFs - , marking the third consecutive quarter where direct corporate buying exceeded ETF accumulation.

ETF與企業金庫配置競爭,體現機構投資比特幣的不同做法。ETF讓多元資產管理者獲取風險敞口,企業金庫則屬於單一公司將比特幣作為儲備資產的策略決策。2025年第二季, - 企業共購入131,000枚比特幣 - ,ETF僅 - 增持111,000枚 - ,已連續三季企業直接買入量超越ETF增持。

MicroStrategy's treasury strategy serves as a template for corporate Bitcoin adoption, with the company holding - 582,000 bitcoins - valued at over $62 billion. The company's aggressive acquisition program targets $84 billion in total Bitcoin purchases by 2027, representing one of the largest corporate asset allocation strategies in history. MicroStrategy's approach involves using debt and equity offerings specifically to fund Bitcoin purchases, creating a direct pipeline from capital markets to Bitcoin demand.

MicroStrategy的金庫策略堪稱企業採用比特幣的典範,目前持有 - 582,000枚比特幣 - ,總值超過620億美元。公司積極收購,目標2027年前購買規模達840億美元,成為史上企業資產配置最大案之一。其作法是透過債務及股票發行,專款專用購買比特幣,直接搭建資本市場與比特幣需求的橋樑。

The withdrawal of - 425,000 bitcoins from exchanges - since November 2024 demonstrates how institutional accumulation directly impacts liquid supply. This phenomenon creates artificial scarcity beyond the protocol's halving mechanism, as long-term holders remove coins from trading circulation. Exchange reserves at - 2.5 million bitcoins - represent five-year lows, indicating that available supply for trading has declined even as total bitcoins in circulation continue growing through mining.

自2024年11月以來, - 已有425,000枚比特幣自交易所撤出 - ,顯示機構積累已直接影響市場流動供給。這種現象不僅有協議層面的減半稀缺,更有長期持有者將幣退出流通所產生的人為稀缺。交易所持幣僅 - 250萬枚 - ,創下五年新低,說明即便比特幣數量隨挖礦持續增長,可供交易的即時供給卻正在萎縮。

Goldman Sachs's evolution exemplifies traditional finance's Bitcoin integration path. The investment bank increased its Bitcoin ETF holdings by - 88% to $1.4 billion - , becoming BlackRock's largest IBIT shareholder while expanding cryptocurrency services for institutional clients. 這種從懷疑態度到大規模配置的發展,反映了自2020年減半周期開始、並於2024年ETF獲批後加速的華爾街廣泛接受趨勢。

因應機構採用的監管框架自過去幾次減半以來已大幅成熟。美國證券交易委員會於2024年1月批准現貨比特幣ETF,移除了先前限制機構參與的監管障礙。隨後於2025年7月批准以現貨實物認購與贖回機制,提升了ETF效率並降低了讓大型投資者憂慮的追蹤誤差。這些監管進步創造了營運基礎建設,有利於支撐2028年減半周期期間的機構持續需求。

銀行業整合透過傳統金融服務加速機構採用。摩根大通與Coinbase合作,使Chase信用卡可用於加密貨幣充值,而PNC銀行則透過銀行帳戶直接提供加密貨幣交易服務。摩根士丹利考慮向數千名經紀人推薦比特幣ETF,這有可能讓數百萬零售投資人透過傳統財富管理管道接觸比特幣。

從以交易為主到以持有為主的需求模式轉變,預示2028年減半前後比特幣價位將呈現不同的表現。過去的周期中,以散戶交易者獲利了結為主,帶來快速暴漲與大幅修正。機構持有者通常會在波動期間繼續持有部位,著重於長期價值增長,而不是短線價差。這種行為差異可能延長牛市時間,同時減緩先前減半周期那種高峰至低谷的劇烈波動。

採礦經濟透過產業轉型進化

比特幣挖礦已從去中心化的個人活動,演變為集中化工業營運,這對於網絡安全、地緣分布、與經濟永續性在2028年都具有深遠影響。數學現實是:雖然每四年挖礦獎勵減半,但營運成本持續上升,迫使礦商在技術創新及運營效率方面不斷提升,以維持利潤空間。

目前全網算力約 - 898.86 exahashes per second - ,運算力超過多數國家總和,透過工作量證明機制保障比特幣網絡安全。即使經歷三次減半,算力依然增長,顯示比特幣價格上升與技術進步抵消了獎勵減少的壓力。然而,2028年減半獎勵將從每區塊3.125降至1.5625顆比特幣,對邊際礦工來說,等於生產成本加倍,這將嚴峻考驗現有模式。

現代ASIC礦機效率已提升到 - 24-26 joules per terahash - ,比早期設備提升千倍。像比特大陸(Bitmain)、MicroBT、嘉楠(Canaan)等公司不斷推進半導體設計,力求在減半不斷侵蝕獲利的形勢下保持競爭優勢。下一代礦機預計2025年可達 - 5 joules per terahash - ,帶來3倍效率提升,雖然技術進步速度已遜於比特幣早期的指數增長。

上市礦商現已主導全球算力分布,替代了早期靠個人在前幾次減半時維護網絡的格局。Marathon Digital的 - 29.9 exahashes per second - 營運能力,需跨多個數據中心,總用電已超越小型城市。Core Scientific營運 - 19.1-20.1 exahashes per second - ,並多元布局AI與高效能運算託管,以提升設施利用率及提高非比特幣挖礦收益。

中國禁礦後的地緣重分配,展現出監管政策能夠迅速重塑網絡安全分布。2021年中國礦工一度控制全球超75%算力,政策限制後數月內資本轉移到哈薩克、俄羅斯、加拿大和美國。美國目前承載超過 - 40% global hash rate - ,受惠於多元能源市場、德州及懷俄明等州的友善監管和成熟金融基礎建設,支撐上市礦商發展。

能源取得已成礦業競爭關鍵,礦工需尋找最低電價以維持利潤。劍橋大學資料顯示 - 43% 可再生能源使用率 - ,包括水電、風能、太陽能及核能。德州積極發展綠能挖礦,礦場能平衡風、光間歇性,於高峰時段提供電網穩定服務。業者也愈來愈常與再生能源基地共址,將無法外送的剩餘電力變現,而非輸送至傳統用電區域。

挖礦盈虧門檻主要受用電成本影響,目前舊型礦機須低於每度電$0.06才能維持競爭力。2028年減半後,門檻將實質翻倍,迫使產業整合,只有最有效率與最廉價電力者才能存活。每次減半後,這種整合都會加速,低效礦工被淘汰,市場只剩具備永續競爭力的業者。

隨著區塊獎勵逐步接近零,交易手續費收入對長期挖礦可持續性愈發重要。當前每日手續費高峰時期約 - $3 million - ,顯著高於過去不足$1百萬的水準,反映手續費市場逐漸興盛。然而與區塊獎勵相比,手續費仍僅佔小比重,2140年之後獎勵歸零,網絡安全資金來源長期值得關注。

礦池分布顯示算力進一步集中至少數大型業者。Foundry USA掌控全球 - 33.49% 算力 - ,服務美國本土專業礦商。AntPool即使面對中國礦業監管,依然維持 - 18.24% - 市佔。雖然主要礦池集中度提升引發去中心化疑慮,但礦工如發現惡意行為可隨時轉投其他礦池,形成持續良性競爭的經濟誘因。

雙用途礦場基礎建設發展成新趨勢,設施橫跨加密貨幣挖礦及AI訓練、高效能運算等新興應用,提升設施利用率。當比特幣挖礦暫時無利可圖時,仍可透過其他運算任務取得收入,提升抗景氣循環能力。

環保法規愈益影響礦業營運,愈來愈多國家要求減碳、或採用綠電。歐盟建議取消加密礦業稅收優惠,數個司法管轄地區則對化石燃料礦業採直接禁止。這些政策趨勢讓使用可再生或碳中和能源的礦商獲得更多競爭優勢,能源成本考量之外的環保門檻隨之抬高。

價格預測模型和分析師預期高度一致:將有大幅度升值

量化模型、機構分析和學術研究趨於一致預期比特幣將於2028年減半周期內大幅升值,儘管對升幅速度與規模仍有分歧。傳統金融機構、加密研究公司及大學模型普遍看好上行趨勢,但對具體估值路徑及方法持不同看法。

ARK Invest提出最積極的機構估值, - 悲觀情境約$300,000 - ,- 基本情境約$710,000 - ,- 樂觀情境2030年可達$1,500,000 - 。其多元模型涵蓋ETF機構採用率、新興市場需求、國家級儲備潛力及Metcalfe’s Law網絡效應,來解釋指數型成長。該模型假設ETF到2033年將佔比特幣總供給15%,須持續大規模機構加倉才能維持目前走勢。

傳統投行則採更保守且仍看漲的評估,聚焦生產成本與價值儲存競爭模型。高盛認為 - 若比特幣占據20%全球價值儲存市場,價格可達$100,000 - ,直接與黃金的傳統避險地位競爭。摩根大通產生成本模型則指出減半後價格應維持在 - $53,000 - 以上,雖然該行預期先有修正才會迎來持續升值。

儘管2022年脫鉤受批評,存量/流速(Stock-to-flow)模型仍以稀缺性為指標預測大幅升值。現有供應/流通比約為58,預計2028年減半後會倍增到約116,參考過去走勢,對應價位將 - 超過$130,000 - 。雖然該模型在2022年熊市時失效,支持者認為機構採納與監管明朗化已創造不同市場動態,有望恢復過去稀缺性與價格的聯動邏輯。

Metcalfe’s Law 應用於Bitcoin 的估值顯示,隨著網絡規模擴大,具有指數級增長的潛力。Fidelity 的模型預測,根據用戶採用曲線與網絡價值關係,到 2038-2040 年,比特幣每枚可達到 $10 億美元的水準,且中期目標在 2030 年前後接近 $100 萬美元。這些模型假設比特幣的用戶基礎與實用性將持續擴展,從純粹投機用途朝向功能性貨幣與價值儲存的實際應用。

學術研究對比特幣長遠估值潛力提供了立場不一的觀點。美國聯準會分析指出,比特幣與傳統總體經濟因素脫鉤,質疑標準資產定價模型是否適用於加密貨幣市場。不過,網絡外部性研究則顯示,隨著使用者採用與交易量增加,價值將同步上升,若比特幣獲得更廣泛的數位貨幣地位,則長期走勢偏向樂觀。

風險情境分析顯示,儘管主流預期偏向樂觀,核心預測值本身仍存在重大不確定性。若出現監管打壓、科技失效、市場飽和、利率上升導致會產生收益的資產更具吸引力,或挖礦中心化等問題,都可能使幣價增值受阻。相反地,若有國家儲備比特幣、加速機構採用、貨幣貶值驅動替代資產需求,及第二層解決方案成功發展,價格甚至可能超越激進的目標。

蒙地卡羅模擬利用機率模型嘗試量化預測不確定性。ARK Invest 的分析顯示,一年期預測中有 77% 機率正報酬,95% 信賴區間介於 $30,000 到 $448,000,顯示即使主流看漲,不確定性仍極高。這些寬廣的預測範圍真實反映了採用率、監管反應與宏觀經濟狀況對比特幣走勢的不確定性。

生產成本模型聚焦於挖礦經濟學來建立價格下限,表示比特幣價格長期而言通常約略對應邊際生產成本。2028 年減半後,區塊獎勵再減半,生產成本實質倍增,或支持較高永續價格水準。但這些模型假設挖礦持續有利可圖,亦未考慮可能的效率提升會壓低成本。

以傳統商品作對比分析,可提供進一步估值架構。比特幣類黃金的庫存流通比(stock-to-flow ratio)接近金價,意味著藉由更優的可攜性、可分割性與可驗證性,有機會實現與黃金持平甚至溢價。若比特幣能從黃金 13 兆美元市值中擷取顯著市佔,單一比特幣僅由市場替代效應即可漲至數十萬美元。

大多數具公信力分析師的共識,在 2028 減半週期內預期比特幣將大幅升值,保守估計價格區間為 $100,000-$200,000,激進模型則預測 $400,000-$600,000。範圍之廣,主要反映機構採用率、監管反應、技術發展與總體經濟狀況等重大不確定性,這些變數最終將決定下一輪減半週期中比特幣的價格走勢。

監管環境轉型帶來史無前例的機構支持

比特幣周邊的監管景觀自前幾次減半週期以來,已徹底轉型,從原本的敵意與懷疑,演化為結構化接納,為機構投資人提供法律明確性與可操作框架,進而支持大規模採用。這場監管進化,讓 2028 減半會處於截然不同的環境,遠非過去那些在監管不確定與稽查執法環伺下發生的減半週期。

川普政府於 2025 年 1 月 23 日簽署的行政命令《加強美國在數位金融科技領域領導地位》,代表美國有史以來最全面支持加密貨幣的政策框架。該命令訂下讓美國成為「全球加密資本」的目標,同時推廣美元支撐的穩定幣、創設戰略性比特幣儲備與數位資產庫存。這與前一屆政府著重執法的政策路線完全相反,為機構投資人提供佈局所需的監管確定性。

在主席 Paul Atkins 的領導下,SEC 的政策走向從 Gary Gensler 激烈對抗的取締,轉為重視創新、釐清加密企業發展路徑的監管框架。由專員 Hester Peirce 領導的加密特別小組制定涵蓋證券分類、量身打造的公開揭露規範以及務實的註冊途徑等綜合性規章。此種共創式手法與以往靠執法行動維持不確定性的減半週期,有極大對比。

SAB 121 監管解禁,移除了銀行提供加密託管業務所面臨的主要阻礙與財報壓力。這項監管變革讓傳統金融機構得以直接提供比特幣託管和交易服務,創造超越專業加密服務供應商的機構參與。美國主要銀行如 JPMorgan、Goldman Sachs 及 Morgan Stanley 均宣布在這一監管明朗化後擴大加密貨幣業務布局。

2024 年 1 月比特幣 ETF 核准,為機構接受度帶來關鍵突破,建立能滿足退休基金、捐贈基金及資產管理人受信義務要求的監管投資工具。2025 年 7 月,ETF 現貨申購及贖回機制獲批,更進一步提升 ETF 運作效率並降低引發專業投資人擔憂的追蹤誤差。這些監管通過促成了超過 $5000 億比特幣 ETF 資產管理規模(AUM)的營運基礎設施。

各州政府也透過立法支持加密貨幣儲備和支付,加速比特幣法案進程。新罕布什爾州配置 5% 州儲備於比特幣,亞利桑那州啟動比特幣儲備計畫。這類州級採用創造監管先例與政治動能,助力推動更廣泛的政府認可,並有潛力影響聯邦政策發展與國際監管協調。

透過 G20 與金融行動特別工作組(FATF)標準的國際監管協同,形成加密貨幣跨境遵循的全球架構。2025 年起,48 國落實的「加密資產共同申報機制(CARF)」促成加密交易資訊的自動交換,稅務機關得以全面取得數據,同時為跨多司法管轄區的機構投資人創造監管確定性。

歐盟加密資產市場(MiCA)規範於 2024 年 12 月 30 日全面實施,為整個歐盟提供涵蓋加密資產服務商與穩定幣的綜合監管架構。歐盟區內的通行權一體化,讓合規加密服務能跨境經營,帶來效率與市場可及性,全面推動歐洲機構採用。

中央銀行數位貨幣(CBDC)發展也因競爭動態反而間接支撐比特幣需求。雖然全球超過 137 國(占全球 GDP 98%)研究 CBDC,相關研究顯示政府數位貨幣與比特幣報酬具有正相關。川普政府禁止美國版 CBDC、同時推動美元穩定幣的政策,為比特幣作為非政府數位資產提供明確定位。

稅務規範革新讓機構投資人獲得必要的操作確定性以利策略性佈局。自 2025 年起的 1099-DA 表單將全面申報加密交易明細,2026 年起的成本基礎追蹤要求則提高整體帳務清晰度,解除以往機構採用路上的稅務疑慮。

環境監管日益影響挖礦運營,透過碳排限制與可再生能源要求,各地政府方針大相逕庭。歐盟建議取消加密礦工稅賦優惠,美國部分州如德州則反向提供可再生能源挖礦獎勵。這種分歧帶來不同區域競爭優勢,同時也可能在重視環保的地區壓縮挖礦空間。

銀行融入大幅提速,在監管明確下,傳統金融機構得以開展加密貨幣業務。JPMorgan 攜手 Coinbase 開放 Chase 信用卡加密資產補足,PNC 銀行直接於帳戶內提供加密交易服務,Morgan Stanley 也考慮納入比特幣 ETF 推薦,顯示監管明確度正推動傳統金融與加密市場鏈結。

與過去減半週期的對比,凸顯監管進化對機構採用的重要性。2012 年減半時監管全無、僅 Mt. Gox 一家主要交易所且缺乏任何監督。2016 年初建監管,但執法不確定性依舊。2020 年減半監管日趨明朗,但機構基礎設施尚未齊備。至於 2028 年減半,將發生在comprehensive regulatory frameworks supporting institutional participation at unprecedented scale.

全面性的監管框架支援機構級參與達到前所未有的規模。

Technical network developments expand bitcoin's utility beyond digital gold

比特幣的技術網絡發展讓其效用超越僅作為數位黃金

Bitcoin's technical infrastructure has evolved substantially through Layer 2 solutions, protocol improvements, and scaling developments that expand the network's utility beyond simple value storage, creating additional demand drivers that could amplify the 2028 halving's economic impact. These technical developments address historical limitations around transaction throughput, programmability, and user experience while maintaining Bitcoin's base layer security and decentralization properties.

比特幣的技術基礎架構已經透過第二層擴充方案、協議改進,以及擴展性發展大幅進化,讓網絡的應用超越單純的價值儲存,創造出額外的需求動能,有可能強化 2028 年減半的經濟影響力。這些技術進展針對歷史上的交易吞吐量、可程式化能力和用戶體驗等限制進行改善,同時維持比特幣基礎層的安全性與去中心化特性。

The Lightning Network represents the most significant Layer 2 scaling solution, with - $145 million in total value locked - across - 16,400 nodes - and - 75,700 payment channels - as of 2025. Lightning enables instant Bitcoin transactions with average costs of - 0.0016 satoshis ($0.000000443) - , dramatically reducing fees compared to base layer transactions that can exceed $10 during network congestion. This payment infrastructure creates utility for Bitcoin as medium of exchange rather than purely store of value, potentially expanding demand beyond speculative and treasury allocation use cases.

閃電網絡是最具代表性的第二層擴容方案,截至 2025 年,總鎖倉價值達 1.45 億美元、節點數量逾 16,400 個、支付通道超過 75,700 條。閃電網絡實現了即時比特幣交易,平均費用僅 0.0016 個聰($0.000000443),在網絡擁塞時遠低於基礎層超過 10 美元的手續費。這套支付基礎設施賦予比特幣作為交換媒介的效用,而不僅僅是價值儲存,有機會讓需求擴展到投機與企業資產配置以外的應用場景。

Lightning Network adoption accelerates through merchant integration, remittance services, and micropayment applications that leverage Bitcoin's programmable money characteristics. Major payment processors including Strike, Cash App, and various international remittance services utilize Lightning for cross-border transfers that bypass traditional correspondent banking systems. These use cases create sustained demand for Bitcoin liquidity while demonstrating practical applications that extend beyond speculative investment.

閃電網絡的普及加速,透過商家整合、匯款服務及微支付應用,發揮比特幣可程式化貨幣的特性。像是 Strike、Cash App 及眾多國際匯款服務等主流支付平台,利用閃電網絡跨境轉帳,繞過傳統國際聯行系統。這些使用案例除了展現超越投機投資的實際應用,也創造了對比特幣流動性的長期需求。

Rootstock (RSK) provides smart contract functionality with Ethereum compatibility while maintaining Bitcoin's security through merge-mining. This sidechain enables decentralized finance applications, tokenization projects, and programmable Bitcoin functionality that competing blockchains have dominated. RSK's development creates potential for Bitcoin to capture value from decentralized finance markets without compromising the base layer's conservative development approach.

Rootstock(RSK)提供了兼容以太坊的智能合約功能,並透過合併挖礦維持比特幣的安全性。這條側鏈讓去中心化金融應用、資產代幣化專案與可程式化比特幣的功能得以在比特幣鏈上實現,使其有機會競爭並分食原本屬於其他區塊鏈的去中心化金融市場價值,同時不犧牲基礎層穩健的開發路線。

Stacks represents another major Layer 2 development enabling smart contracts and decentralized applications on Bitcoin through its unique consensus mechanism that settles transactions to Bitcoin's base layer. Stacks' programming language Clarity provides formal verification capabilities that enhance security compared to other smart contract platforms, while Bitcoin anchoring ensures transaction finality through proof-of-work consensus.

Stacks 是另一項重要的第二層技術發展,以其獨特的共識機制實現將交易結算到比特幣基礎層之上,使得比特幣能支援智能合約與去中心化應用(DApps)。Stacks 的專屬語言 Clarity 提供形式化驗證能力,增強安全性,而比特幣錨定則用工作量證明確保交易最終性。

Liquid Network operates as a federated sidechain providing faster settlement times and enhanced privacy features for institutional Bitcoin transactions. The network facilitates high-volume trading and custody operations through major exchanges and financial institutions, creating infrastructure that supports institutional adoption while reducing base layer congestion from large-value transfers.

Liquid Network 作為聯邦側鏈,為機構級比特幣交易提供更快的結算速度與更強的隱私功能。該網絡促進大型交易所及金融機構之間的高頻交易與託管操作,建立起有利於機構採用的基礎設施,同時減少大額轉帳對基礎層造成的擁塞。

State channel implementations beyond Lightning Network provide additional scaling solutions for specific use cases including gaming, micropayments, and streaming applications. These technical developments create programmable Bitcoin functionality without compromising base layer security, enabling new applications that generate sustained demand for Bitcoin liquidity.

除了閃電網絡之外,狀態通道的應用也為遊戲、微支付及串流等特定場景提供額外的擴容方案。這些技術進展使比特幣擁有可程式化功能,並在不損及基礎層安全性的前提下,推動新型應用,持續帶來對比特幣流動性的需求。

Bitcoin Improvement Proposal (BIP) process continues advancing protocol development through community consensus, with - 389 BIPs - in Bitcoin's history addressing consensus-critical changes, protocol improvements, and process enhancements. Recent BIPs focus on privacy improvements, scaling optimizations, and developer tooling that enhance Bitcoin's technical capabilities while maintaining backward compatibility and decentralization properties.

比特幣改進提案(BIP)機制持續通過社群共識推進協議發展,截至目前為止,已有 389 份 BIP 涉及協議性關鍵更動、改進及流程優化。近期的 BIP 著重於隱私強化、擴容優化和開發工具,提升比特幣技術能力,並同時確保向下相容與去中心化特性。

Taproot activation in 2021 provided the foundation for enhanced privacy and programmability that Layer 2 solutions continue building upon. Taproot's script efficiency improvements reduce transaction costs and enable more complex smart contract functionality while maintaining privacy through output indistinguishability. These base layer improvements support Layer 2 development and expand Bitcoin's technical capabilities.

2021 年的 Taproot 升級為隱私性和可程式化功能打下基礎,進一步為第二層解決方案開發鋪路。Taproot 優化了腳本效率,降低交易成本,並實現更複雜的智能合約同時保護隱私(因輸出難以區分)。這些基礎層提升支援了第二層發展,也擴展了比特幣的技術潛力。

Mining infrastructure developments include stranded energy monetization, renewable energy integration, and dual-use facilities that optimize computational resources across cryptocurrency mining and artificial intelligence workloads. These infrastructure improvements enhance mining economics while addressing environmental concerns that could influence regulatory responses and institutional adoption decisions.

礦業基礎設施的創新發展包含閒置能源貨幣化、再生能源整合,以及可同時支援加密貨幣挖礦與人工智慧運算的雙重用途設施。這些基礎建設提升礦業經濟效益,同時回應環保議題,影響相關監管回應及機構採用決策。

The development of Bitcoin-native financial services creates additional demand for Bitcoin beyond speculative trading and treasury allocation. Lending protocols, derivatives platforms, and custody services built on Bitcoin infrastructure enable sophisticated financial applications while maintaining Bitcoin's security properties. These services create yield generation opportunities that compete with traditional fixed-income investments.

比特幣原生金融服務的發展,開拓了除投機交易與企業資產配置之外的需求。基於比特幣基礎設施的借貸協議、衍生品平台和託管服務,讓複雜的金融應用得以實現,同時保有比特幣的安全特質。這些服務創造了收益生成機會,得以與傳統固定收益投資競爭。

Privacy enhancements through Lightning Network, coin mixing services, and protocol developments address institutional concerns about transaction visibility and regulatory compliance. Enhanced privacy features enable Bitcoin usage in applications requiring confidential transactions while maintaining regulatory transparency through selective disclosure mechanisms.

透過閃電網絡、混幣服務以及協議層的改進,加強了比特幣的隱私性,回應機構對交易透明度與合規的關切。進階隱私功能讓比特幣能被運用於需要保密交易的應用,同時透過選擇性揭露機制維持監管上的透明度。

Cross-chain interoperability solutions enable Bitcoin integration with other blockchain networks through wrapped Bitcoin tokens, atomic swaps, and bridge protocols. These technical developments expand Bitcoin's utility across decentralized finance ecosystems while maintaining native Bitcoin ownership and security properties.

跨鏈互通方案讓比特幣可以透過包裝比特幣(WBTC)、原子交換與橋接協議整合進其他區塊鏈網絡。這些技術發展拓展了比特幣在去中心化金融生態系的效用,同時維持原生比特幣的所有權與安全特性。

Technical infrastructure maturation creates sustained demand drivers beyond speculative investment that could amplify the 2028 halving's economic impact. As Bitcoin evolves from digital gold to programmable money through Layer 2 solutions, the network captures value from payments, decentralized finance, and various applications that generate consistent demand for Bitcoin liquidity. This utility expansion creates additional upward pressure on Bitcoin prices that compounds with supply reduction effects from the halving mechanism.

技術基礎設施的成熟帶來了超越投機投資的持續性需求動力,有可能放大 2028 年減半帶來的經濟影響。隨著比特幣透過第二層方案從數位黃金進化成可程式化貨幣,網絡得以從支付、去中心化金融及其他穩定帶來流動性需求的多元應用中進一步捕獲價值。這種應用面的擴展,使比特幣價格產生額外的上行壓力,並與供給減半效應疊加。

Comparison with traditional commodities reveals bitcoin's unique economic properties

與傳統商品相比揭示比特幣獨特的經濟屬性

Bitcoin's monetary and economic characteristics diverge substantially from traditional commodities, creating unique supply-demand dynamics that may amplify halving effects beyond historical commodity market behavior. While gold and other precious metals provide useful comparison frameworks, Bitcoin's digital nature, programmatic scarcity, and network effects generate economic properties without precedent in traditional commodity markets.

比特幣在貨幣與經濟特性上與傳統商品截然不同,造就出獨特的供需動態,可能讓減半效應遠超過歷來商品市場的反應。儘管黃金和其他貴金屬提供了有參考價值的對照架構,比特幣的數位本質、程式化稀缺性和網絡效應,讓其具備傳統商品市場前所未見的經濟特質。

Gold maintains a stock-to-flow ratio near 70 through approximately 3,000 tonnes of annual production against existing above-ground stocks of roughly 200,000 tonnes. Bitcoin's current stock-to-flow ratio of 58 approaches gold's scarcity level and will exceed it after the 2028 halving when the ratio reaches approximately 116. However, Bitcoin's supply schedule operates through algorithmic certainty rather than geological discovery and mining economics that influence gold production, creating fundamentally different supply dynamics.

黃金每年約生產 3,000 噸,地表流通存量約 20 萬噸,stock-to-flow 比率約為 70。比特幣目前的存量流量比為 58,已趨近於黃金,並將在 2028 年減半後提升至約 116,進一步超越黃金稀缺度。然而,比特幣的供給由演算法確定,並非受限於地質探勘與開採經濟性,這使兩者的供給動力有根本性的不同。

Unlike gold mining that responds to price incentives through increased exploration and production capacity, Bitcoin mining cannot increase supply above the predetermined issuance schedule regardless of price levels or mining investment. This supply inelasticity means Bitcoin price appreciation cannot trigger supply responses that moderate price increases, as occurs with traditional commodities during bull markets. The mathematical certainty of Bitcoin's supply schedule creates scarcity economics without precedent in commodity markets.

與黃金礦業可因價格誘因提升勘探與擴產不同,比特幣礦工無論價格多高、投入再多資本,都無法讓供給超越預定發行速度。這種供給僵固性意味著比特幣價格上漲時,無法像傳統商品在多頭市場那樣誘發供給增加以緩解漲幅。比特幣供給機制的數學確定性,締造了商品市場前所未見的稀缺經濟學。

Industrial commodities like copper, oil, and agricultural products typically maintain stock-to-flow ratios between 1 and 5, reflecting their consumption in manufacturing and energy production. These commodities experience supply-demand balancing through production adjustments and substitute goods that moderate price extremes. Bitcoin's lack of industrial consumption or substitute goods creates demand dynamics driven purely by monetary and speculative factors rather than productive economic applications.

工業型商品如銅、石油、農產品,其 stock-to-flow 比率通常介於 1 到 5 之間,反映其廣泛被消耗於製造與能源產業。這些商品靠著產能調節與替代品使供需達到平衡,避免價格波動過大。而比特幣沒有工業用途或替代商品,其需求動能純粹由貨幣屬性與投機因素推動,而非生產性經濟應用。

Silver provides interesting comparison as both industrial metal and monetary asset, with a stock-to-flow ratio around 25 that Bitcoin has already exceeded. Silver's dual demand from industrial applications and investment creates different price dynamics compared to pure store-of-value assets like Bitcoin. However, silver's supply responds to mining economics and recycling that can moderate price appreciation, while Bitcoin's fixed supply schedule prevents supply-side responses to demand increases.

白銀同時兼具工業金屬與貨幣資產特性,stock-to-flow 比率約 25,已被比特幣超越。白銀產生於工業需求與投資雙線驅動,價格動態也迥於像比特幣這種單純儲值資產。不過,白銀的供給會受礦業經濟性及回收調節影響,產量得以回應需求(從而抑制漲幅);而比特幣由於螺絲釘般固定的供給,則不存在這種供給面的調節機制。

Traditional commodity trading involves physical storage, transportation, quality verification, and delivery mechanisms that create operational costs and market frictions. Bitcoin's digital nature eliminates these physical constraints while enabling instant global transfer, divisibility to eight decimal places, and perfect authenticity verification through cryptographic signatures. These superior monetary properties create competitive advantages over physical commodities for store-of-value applications.

傳統商品交易涉及實體存儲、運輸、品質驗證與交割等流程,造就高昂的營運成本及市場摩擦。比特幣作為數位資產,排除了這些物理限制,實現全球即時轉帳、精細到八位小數的可分割性,並以密碼學簽章實現百分之百真偽驗證。這些優越貨幣屬性賦予其在儲值應用上相較於實體商品的顯著競爭優勢。

Network effects distinguish Bitcoin from traditional commodities through Metcalfe's Law relationships where network value increases proportionally to the square of user adoption. Gold and other commodities lack network effects, with their value determined purely by supply-demand balancing rather than network expansion. Bitcoin's network effects create potential for exponential value appreciation

網絡效應讓比特幣明顯區隔於傳統商品—根據梅特卡夫定律,網絡價值與用戶數的平方成正比。黃金與其他大宗商品並無網絡效應,其價值僅由供需平衡決定,而非用戶網絡的擴展。比特幣的網絡效應創造出價值呈指數級增長的潛力as adoption increases, contrasting with linear supply-demand relationships governing traditional commodities.

隨著比特幣的採用程度提升,其市場行為與傳統商品所受到線性供需關係的影響大為不同。

Storage and custody differences create operational advantages for Bitcoin compared to physical commodities. Gold storage requires secure vaults, insurance, transportation, and verification systems that generate ongoing costs and operational risks. Bitcoin storage requires secure key management but eliminates physical infrastructure costs while enabling global accessibility through internet connectivity. These operational advantages reduce barriers to Bitcoin ownership and accumulation.

儲存及託管上的差異,使比特幣相較於實體商品具備營運上的優勢。黃金的儲存需要安全金庫、保險、運輸及驗證系統,以保障資產安全,但這些都會產生持續的成本與營運風險。比特幣的保管僅須妥善管理密鑰,即可免去實體設施的支出,並且經由網際網路即可全球存取。這些營運優勢降低了比特幣持有與累積的門檻。

Divisibility and transferability provide Bitcoin with monetary properties that exceed traditional commodities. Gold's physical properties limit divisibility and complicate small-value transactions, while Bitcoin enables micro-transactions and precise value transfer without physical constraints. These properties support Bitcoin's utility as medium of exchange in addition to store-of-value applications, creating broader demand patterns than pure commodity investments.

可分割性與可轉移性使比特幣擁有超越傳統商品的貨幣特性。因為黃金的物理特性,其分割程度有限,且小額交易相當複雜;相較下,比特幣能夠精確地進行微小額支付與價值轉移,無受實體限制。這些特性不僅有助於比特幣作為價值儲存手段、也拓展了作為交換媒介的實用性,使其需求遠較純粹商品投資為廣。

Market structure differences affect price discovery mechanisms between Bitcoin and traditional commodities. Commodity markets feature established futures markets, spot trading, and industrial hedging that create sophisticated price discovery mechanisms. Bitcoin markets remain relatively nascent but increasingly sophisticated through ETF development, derivatives markets, and institutional participation that improve price efficiency and reduce volatility.

市場結構上的差異,導致比特幣與傳統商品在價格發現機制上也有所不同。商品市場具有完善的期貨交易、現貨市場及產業避險,形成成熟的價格發現系統。比特幣市場雖仍屬新興,但隨著 ETF 產品、衍生性市場發展及機構資金的參與,價格效率逐步提升,波動性也同步下降。

Regulatory frameworks governing Bitcoin differ substantially from traditional commodity regulations developed over decades of market evolution. Commodity markets operate under comprehensive regulatory oversight addressing market manipulation, position limits, and delivery requirements. Bitcoin regulation continues evolving but increasingly resembles securities regulation rather than commodity frameworks, creating different market dynamics and investor protection mechanisms.

比特幣所受的監管體系,與經過數十年市場演進而建立的傳統商品法規有明顯區別。傳統商品市場受全面監管,管控市場操縱、倉位限制、交割要求等。比特幣法規則持續演變,並愈發接近證券監管模式,而非單純的商品規範,進而導致不同的市場動態與投資人保護機制。

The absence of productive yield distinguishes Bitcoin from income-generating assets but aligns with gold and other non-yielding stores of value. However, Bitcoin's potential for yield generation through lending, staking derivatives, and Layer 2 applications creates opportunities for return enhancement without compromising base asset ownership, contrasting with physical commodities that lack similar yield opportunities.

比特幣不具生產性收益,這使其有別於帶來收入的資產,但卻與黃金及其他非收益型價值儲存資產一致。然而,比特幣可藉由借貸、質押衍生品及第二層應用產生收益,使投資人有額外的獲利機會,且不影響底層資產擁有權,這與無法產生類似收益的實體商品截然不同。

Correlation patterns between Bitcoin and traditional commodities reveal changing relationships as Bitcoin matures. Early Bitcoin development showed minimal correlation with commodity markets, but institutional adoption has increased correlation with risk assets while maintaining negative correlation with the U.S. dollar. These correlation patterns suggest Bitcoin increasingly functions as risk asset rather than commodity hedge, though this relationship may evolve as institutional adoption progresses.

比特幣與傳統商品間的相關性隨著其成熟度提升而有所變化。早期比特幣幾乎與商品市場無關聯,但機構資金進場後,其與風險資產的相關性提升,對美元則維持負相關。這意味著比特幣愈來愈傾向於風險資產的定位,而非商品避險工具,儘管這樣的關係仍可能隨機構採用率改變持續演化。

The unique combination of programmatic scarcity, network effects, superior monetary properties, and institutional adoption creates economic dynamics for Bitcoin that differ fundamentally from traditional commodities. While commodity frameworks provide useful analytical tools, Bitcoin's digital nature and network characteristics generate unprecedented economic behavior that may amplify halving effects beyond historical commodity market patterns.

比特幣獨特結合了程式化稀缺、網路效應、優越的貨幣屬性,以及機構採用,所形成的經濟動態,與傳統商品有根本區別。雖然商品分析框架有其參考價值,但比特幣的數位本質和網路特徵,使其經濟表現前所未有,甚至可能讓減半效應超越以往商品市場的歷史模式。

Current 2025 market conditions set stage for unprecedented halving dynamics

2025 年市場現況為前所未有的減半動態鋪路

The Bitcoin market environment heading into the 2028 halving presents unprecedented institutional adoption, regulatory clarity, and technical infrastructure that fundamentally differs from conditions surrounding previous halving events. These structural changes suggest the 2028 halving will operate within mature financial markets rather than speculative cryptocurrency ecosystems that characterized earlier cycles, potentially creating different risk-reward profiles and volatility patterns.

邁向 2028 年減半,比特幣市場處於前所未有的機構採用、法規明朗化及技術基礎建設狀態,與過往減半時期的環境大異其趣。這些結構性變化意味著 2028 減半將發生於成熟金融市場裡,而不是過去以投機為主的加密貨幣生態,預料將帶來截然不同的風險報酬組合及波動模式。

Institutional ownership concentration has reached levels that create structural demand and supply dynamics unlike previous halving cycles. With - over 10% of Bitcoin supply controlled by institutions - through ETFs and corporate treasuries, the market features significant "strong hands" ownership that historically maintains positions through volatility periods. This ownership concentration reduces liquid trading supply while providing price support during market corrections, creating conditions where supply reduction from halving meets already constrained available supply.

機構持有比特幣的集中度已達高點,形成與以往減半週期截然不同的供需結構。透過 ETF 與企業金庫,機構掌握超過 10% 的比特幣供應,這些「強手」通常在市場波動期間堅守持倉。所有權集中降低了流動供給,同時也在市場修正時提供價格支撐,使減半帶來的供給萎縮更加受到現有供應緊張的影響。

Bitcoin's correlation with traditional financial markets has evolved from near-zero relationships during early halvings to current correlations of - 0.58 with the Russell 1000 - and - 0.53 with financial stocks - . This integration with traditional markets means Bitcoin price movements increasingly reflect broader economic conditions, institutional portfolio allocation decisions, and macroeconomic factors rather than purely cryptocurrency-specific developments. These correlation patterns suggest the 2028 halving will occur within broader financial market context rather than isolated cryptocurrency speculation.

與傳統金融市場的關聯度,也由過去幾乎為零,提升至目前與羅素 1000 指數有 0.58、與金融類股有 0.53 的相關性。這代表比特幣的價格走勢越來越受整體經濟狀況、機構資產配置及總體經濟條件影響,而不再只是加密市場本身。因此, 2028 減半預計會在更廣泛的金融市場背景下發生,而不再只是孤立的加密貨幣投機週期。

The emergence of Bitcoin as a treasury asset for public companies creates sustained demand that operates independently of speculative trading cycles. MicroStrategy's - 582,000 bitcoin holdings - and aggressive acquisition program targeting - $84 billion in total purchases by 2027 - represents strategic allocation decisions based on long-term value storage rather than short-term trading. This corporate treasury trend creates predictable demand that could provide price floors during market volatility.

比特幣作為上市公司金庫資產的興起,帶來獨立於投機週期之外的長期穩定需求。以 MicroStrategy 持有 582,000 枚比特幣,以及預計到 2027 年總計投入 840 億美元的大型購買計畫為例,這些決策乃基於長期價值儲存的策略分配,而非短線交易。這波企業金庫趨勢創造可預期的需求,有望在市場波動時為價格提供下檔保護。

Current trading volumes averaging - $38.9 billion daily - demonstrate institutional-grade liquidity that supports large-value transactions without significant price impact. However, exchange reserves at - 2.5 million bitcoins - representing five-year lows indicate that available trading supply has declined even as institutional participation has increased. This combination of high liquidity and reduced available supply creates market conditions where incremental demand could generate substantial price impacts.

目前單日均交易量達到 389 億美元,展現出機構等級的流動性,可支撐大額交易且不致引發劇烈波動。但同時,交易所儲備僅剩 250 萬枚比特幣,創下五年來新低,顯示雖然機構參與度提升,但可流通供應反而減少。這種高度流動性加上供應短缺的局面,使得額外需求上升時可能導致資產價格顯著波動。

The regulatory environment provides institutional investors with legal clarity and operational frameworks that enable strategic Bitcoin allocation decisions. SEC approval of Bitcoin ETFs, banking integration through traditional financial institutions, and comprehensive regulatory frameworks remove barriers that previously limited institutional participation. This regulatory clarity enables pension funds, endowments, and other fiduciary investors to consider Bitcoin allocation without previous legal uncertainties.

法規環境的進步,為機構投資人帶來法律明析及操作標準,有助於策略性地配置比特幣。美國證管會(SEC)批准比特幣 ETF、傳統金融機構的銀行整合,以及完善的監管架構,皆清除了過去限制機構介入的障礙。這種法律明確性讓退休基金、捐贈基金及其他受託人投資人,能在無法律疑慮下考慮配置比特幣。

Interest rate environment and monetary policy create macroeconomic conditions that could influence Bitcoin demand through the 2028 halving cycle. Federal Reserve policy decisions, inflation expectations, and currency debasement concerns affect institutional asset allocation decisions between Bitcoin, bonds, equities, and alternative investments. Bitcoin's negative correlation with the U.S. dollar creates potential hedging demand during currency weakness periods.

利率環境與貨幣政策也將於 2028 減半週期內塑造影響比特幣需求的總體經濟條件。聯準會的政策決議、通膨預期與貨幣貶值疑慮,會牽動機構在比特幣、債券、股票及另類投資間的資產配置。比特幣對美元的負相關,也使其在美元走弱時有潛在避險需求。

Geopolitical developments including nation-state Bitcoin adoption, central bank digital currency competition, and international monetary system evolution create additional demand drivers beyond traditional investment allocation. Countries like El Salvador's Bitcoin legal tender adoption and proposed U.S. Strategic Bitcoin Reserve create government demand that operates independently of market speculation, potentially providing sustained price support through halving cycles.

地緣政治進展 — 包括國家層級採用比特幣、央行數位貨幣(CBDC)競爭,以及國際貨幣體系的演變 — 也帶來超越傳統投資配置的新需求來源。如薩爾瓦多推動比特幣法償,以及美國提議戰略比特幣儲備,這些政府需求不受市場投機週期影響,有望為減半期間帶來長期穩定的價格支撐。

Technical infrastructure maturation through Layer 2 solutions, payment systems, and financial services creates utility demand for Bitcoin beyond speculative investment and treasury allocation. Lightning Network growth, decentralized finance integration, and merchant acceptance create sustained demand for Bitcoin liquidity that compounds with investment demand to create upward price pressure.

技術基礎建設的成熟,包括第二層方案、支付系統及金融服務,帶動比特幣超越投機投資及金庫用途的實際需求。閃電網路成長、去中心化金融整合、商家支付接受度提升,都持續帶來比特幣的流動性實需,加上投資需求將形成疊加的上漲壓力。

Market microstructure evolution toward institutional-grade trading infrastructure supports large-value transactions and sophisticated trading strategies that improve price discovery and reduce manipulation risks. Professional market makers, algorithmic trading systems, and derivatives markets create trading environments that resemble traditional asset markets rather than early cryptocurrency exchanges with limited liquidity and operational risks.

市場微觀結構的演化,轉向機構級交易基礎設施,促進大額交易並支援複雜交易策略,有助於價格發現並降低操控風險。專業造市商、演算法交易系統及衍生性商品市場,為比特幣交易建立起類似傳統資產市場的環境,遠勝早期流動性有限、營運風險高的加密貨幣交易所。

The unprecedented combination of institutional ownership, regulatory clarity, technical infrastructure, and macroeconomic conditions creates market conditions for the 2028 halving that differ fundamentally from previous cycles. These structural changes suggest potential for sustained price appreciation with reduced volatility compared to retail-driven historical cycles, though absolute price movements may remain substantial due to Bitcoin's expanding market capitalization and institutional demand patterns.

機構持有、法規明朗、技術健全與總體經濟條件的前所未有結合,為 2028 減半週期創造了與過往截然不同的市場環境。這些結構性革新顯示,比起以散戶為主的歷史減半週期,未來比特幣可能更具持續上漲動能且波動性降低,儘管絕對價格變化仍可能因市值及機構需求擴張而非常顯著。

Environmental, social, and governance (ESG) considerations increasingly influence institutional Bitcoin allocation decisions through renewable energy mining requirements, carbon accounting frameworks, and sustainability reporting standards. Mining industry evolution toward renewable energy sources and carbon-neutral operations addresses institutional concerns while creating operational advantages for mining companies with environmental compliance.

環境、社會與公司治理(ESG)考量,正透過可再生能源挖礦要求、碳會計規範與永續報告標準,日益影響機構分配比特幣的決策。隨著挖礦產業逐漸採用再生能源及邁向碳中和營運,不僅回應了機構端的環保疑慮,也為合規挖礦公司創造了營運優勢。

Derivatives market development provides institutional investors with sophisticated risk management tools including futures, options, and structured products that enable hedged Bitcoin exposure and yield generation strategies. These financial instruments create additional demand for underlying Bitcoin while providing institutions with familiar risk management frameworks from traditional asset classes.

衍生性商品市場的發展,為機構投資人提供期貨、選擇權及結構型產品等進階風險管理工具,使其能以避險方式接觸比特幣並制定收益策略。這些金融工具不但提升比特幣現貨需求,也讓傳統資產管理機構能以熟悉的風控架構進入此新興資產領域。

Long-term implications beyond the 2028 halving

2028 減半之外的長期影響

The 2028 Bitcoin halving represents a pivotal transition Here is the translation according to your requirements. Markdown links are skipped.

加密貨幣從實驗性技術演進為成熟的機構級資產類別,其發展已到關鍵節點,帶來的長期影響遠超過短期價格變動。機構採用、監管框架、技術基礎建設與全球貨幣不確定性的匯聚,構建出有利條件,可能讓比特幣在減半事件後的數十年間,於國際金融體系中確立其角色。

隨著比特幣的庫存流通比(Stock-to-Flow Ratio)超越黃金,並且各國央行面臨債務可持續性及貨幣貶值壓力,貨幣政策的影響變得愈發重要。比特幣固定供給機制,為機構投資者和國家提供了對抗貨幣膨脹的避險工具,傳統資產難以媲美。比特幣稀缺的數學確定性,相較於依賴開採經濟和地質限制的黃金及其他保值資產,賦予其競爭優勢。

隨著減半週期遞增,區塊獎勵接近歸零,比特幣從倚賴挖礦獎勵轉向以交易手續費維持的過渡也接近臨界點。2028年之後,1.5625枚比特幣的區塊獎勵將要求手續費市場大幅發展,才能通過經濟誘因維護網路安全。第二層解決方案及比特幣實用性的提升,或能創造足夠的交易量與手續費支撐礦工營運,然此轉型在所需規模下仍未經考驗。

國際貨幣體系整合,可能因主權國家採用比特幣及央行儲備多元化而加速。面臨貨幣不穩、制裁風險或高通膨壓力的國家,或將如薩爾瓦多將比特幣定為法定貨幣、以及美國所提的戰略比特幣儲備法案──進一步提升比特幣配置。政府需求不僅創造持續上行的價格壓力,也使比特幣成為黃金與外匯並列的地緣資產。

金融基礎建設的成熟,透過與傳統銀行的串接、託管方案及監管架構,使擁有數兆美元資產的退休基金、保險公司與主權財富基金等,能參與比特幣。這些機構投資者運作週期較長且資本量較大,或能創造跨越多次減半周期的持續需求。

科技演進方面,包含量子運算、密碼學進展及區塊鏈擴容,都會影響比特幣的長期價值及網路安全。雖量子計算威脅現有密碼演算法,比特幣開發社群已著手研擬抗量子方案。若能成功應對科技挑戰,將進一步強化比特幣的反脆弱特性與機構信心。

央行數位貨幣、替代加密貨幣及傳統金融創新推動的競爭格局,雖帶來比特幣在貨幣角色上的潛在挑戰,但比特幣去中心化架構、成熟紀錄以及網路效應,形成政府數位貨幣難以複製的競爭優勢。競爭亦可加速比特幣創新,同時驗證其核心價值主張。

環保永續要求持續影響機構比特幣配置之決策,透過ESG投資框架及法規標準體現。礦業產業朝可再生能源與碳中和運營的發展,能消除部分機構採用障礙,創造對環保合規礦工的營運優勢。成功的環境整合,能去除機構採納之阻礙,並支撐長期價格上漲。

世代財富轉移,作為重大長期需求驅動力,年輕熟悉加密貨幣的族群,將繼承傳統資產持有者的可觀財富。這樣的人口結構轉型可能加速比特幣普及,投資組合配置偏好將向數位資產傾斜,造就超越現有機構採用趨勢的持續需求。

比特幣2100萬枚最大供給的數學推進,意味著隨著剩餘比特幣逐漸歸零,市場上新幣釋出的每件減半事件,都會變得更加罕見。雖然每次減半帶來的絕對供應減少量下降,但百分比減幅維持不變,造就稀缺溢價可能延展跨數十年的價格上升。

關於數位稀缺、網路效應及可程式化貨幣的經濟理論持續演進,比特幣展現前所未有的貨幣屬性。學術研究、央行分析與機構框架,愈來愈重視比特幣的獨特性,並發展針對數位資產的分析工具與估價模型,區別於傳統商品體系。

人工智慧、區塊鏈和數位支付的交匯,或將為比特幣創造全新應用場景,超越現有的保值與支付功能。這些科技結合有望產生擴大網路效應的新需求動能,並圍繞可程式化貨幣及自動化金融系統,創造嶄新的經濟模式。

全球金融體系的韌性,因比特幣基於去中心化的架構,獨立於傳統銀行體系、政府貨幣政策及地緣衝突而大受益。在金融危機、銀行倒閉或國際衝突中,傳統系統受損時,這些系統性優勢更顯珍貴,可能持續推動對去中心化替代方案的需求。

結論:機構減半時代

2028年比特幣減半,將標誌著比特幣由實驗階段正式邁入機構時代,徹底改變過去以供給減少為核心的經濟動態。機構持有量首次突破總供應量的10%,橫跨多國與多層級的完備監管體系,和成熟的金融基礎建設匯集,令傳統減半效應一方面因流動性受限而增強,一方面又因市場參與專業化而被調節。

不似過往主要由散戶投機與技術採用主導的周期,2028年減半時,- 140萬枚比特幣儲存在ETF -,- 58.2萬枚成為MicroStrategy的財庫策略基石 -,傳統金融機構則將比特幣服務納入客戶體系。這種機構參與,帶來過往缺乏的持續需求動能與價格穩定機制,意謂著有可能迎來更長持續期的上升、波動度卻像成熟資產類別那樣減弱。

由3.125枚至1.5625枚挖礦獎勵的數學確定性減少,創造可預測的供給限制,並前所未有的結構性需求變化互動。當交易所庫存降至五年新低的250萬枚,機構持續累積,將資金從流動貨源抽離市場,2028減半供給衝擊將在已極為緊縮的市場條件下發酵,有可能放大傳統稀缺效應。

技術基礎建設的演進,從二層解決方案、支付系統到金融應用,讓比特幣用途超越投機或財庫,造就流動性需求與投資需求的疊加。閃電網路成長、智能合約能力與傳統金融整合,展現比特幣朝向可程式化貨幣邁進,創造多樣經濟應用價值,而不僅止於投機交易。

監管從執法不確定轉向架構化接受,為機構投資者提供必要的法律明確性和營運框架以便戰略配置。SEC批准比特幣ETF、銀行業合規授權與完善合規標準打通了先前阻礙機構參與的障礙,亦建立了支撐兆元資產級發展的基礎建設。

主流機構分析師的價格預測一致看好2028減半周期的上升潛力,保守估計落在10萬至20萬美元,激進模型則定於40萬至60萬美元。這些預測反映出真實的機構採用趨勢與供需經濟,而非投機情緒,顯示受基本面驅動的可持續升值潛力。

總體影響遠超短期價格層面,涵蓋比特幣國際貨幣體系角色、投組分配策略及金融科技創新。2028減半不僅是又一輪供給減少,亦證明比特幣從實驗性技術邁向與黃金、國債及傳統價值儲存工具直接競爭的既定貨幣資產。

最重要的是,這次減半將驗證,比特幣的機構化成熟是否能維持早期週期的網路效應與升值潛力,還是說市場效率與機構化會讓歷史循環趨於更傳統資產的表現。數學稀缺性、機構採用及regulatory integration creates conditions for Bitcoin's most significant economic experiment since its creation - demonstrating whether digital scarcity can maintain exponential growth characteristics within mature financial systems.

監管整合為比特幣自創立以來最重大的經濟實驗創造了條件——驗證數位稀缺性在成熟金融體系中能否維持指數型成長的特性。

This institutional halving era marks Bitcoin's graduation from cryptocurrency markets to traditional asset class inclusion, with implications for monetary policy, portfolio theory, and international finance that will extend far beyond the immediate supply reduction effects. The 2028 halving stands as the definitive test of Bitcoin's ability to maintain revolutionary growth characteristics while achieving evolutionary integration within established financial systems.

這個機構減半時代,標誌著比特幣從加密貨幣市場「畢業」進入傳統資產類別,對貨幣政策、投資組合理論,以及國際金融都產生了遠超供給減少直接效果的深遠影響。2028年的減半,將成為比特幣在維持革命性成長特質的同時,實現與現有金融體系進化式融合的終極考驗。