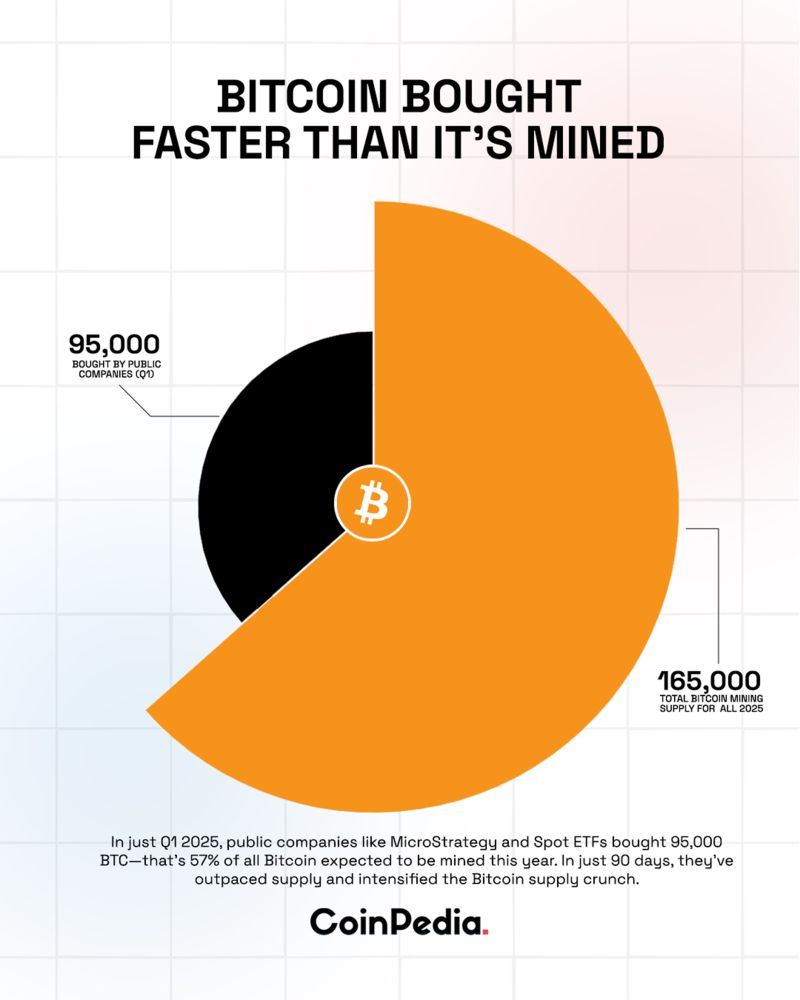

比特幣自2025年以來的強勁上漲,成為今年金融界最具標誌性的故事之一。世界最大加密貨幣在10月初突破12萬6千美元,靠著一波機構資金湧入,由新批准的比特幣現貨ETF提供管道而推升。這些ETF於2024年1月在美國證監會歷史性批准下推出,徹底改變了傳統投資者接觸比特幣的途徑。數月以來,機構買方需求幾乎無窮無盡,現貨比特幣ETF吸收的比特幣遠超礦工產出。

然而,在強勁行情之下,一個關鍵轉變已然浮現。Capriole Investments 的分析指出,首次在七個月內,ETF 與企業金庫購買的比特幣需求低於新開採比特幣的速度。2025年11月3日的這一發展,可能標誌著比特幣市場結構的拐點。代表機構整體購買的藍線,如今已跌破日挖礦發行的紅線。

其影響遠超市場技術層面。當機構需求長期超過新供應時,比特幣稀缺敘事激化,有力支撐價格上行。若反過來,則帶來不確定性。當最能消化每日發行額的機構退場時,市場將追問誰能填補需求空白,以及未來成交價格。

此動態關鍵在於,比特幣價值主張極度依賴其設計上的稀缺。與央行可隨意印製的法幣不同,比特幣總量上限為2100萬枚,並按照預定減半機制每四年降低新發行量。2024年4月減半之後,日均發行量降為約450 BTC。當最具實力買方的需求無法追上這一減量供應時,這代表推高比特幣至新高的多頭論述潛藏弱點。

若仔細檢視機構需求結構,狀況更顯複雜。現貨比特幣ETF只是整體需求的一部分。數位資產金庫公司,亦即將比特幣納入資產負債表作為戰略儲備的企業,成為另一大需求來源。但此渠道同樣出現壓力。資產淨值溢價大幅縮水,許多金庫公司股價跌至其比特幣持有價之下。

比特幣近期價格動向也反映這種情緒轉變。在10月初觸及12萬6千美元歷史高點後,比特幣進入整理區間,截至10月底約10萬9千美元。此時市場還經歷過一場槓桿多單大規模清算,近10億美元多單被平倉。盤整期間仍能維持支撐,顯示基本面尚存,但市場仍須面對機構賣壓或冷卻時能否撐住的考驗。

解析這次供需交叉,須細看多方因素相互作用。供給面包含日常產出、礦工行為、運營經濟及區塊鏈網絡維運成本等。需求端則涵蓋現貨ETF的資金流、企業財務策略、法規動態與宏觀經濟環境對風險偏好的影響。各環節互有牽動,任何細微變動亦可帶來市場大幅波動。

本文全面剖析比特幣當前供需格局,說明ETF如何由淨買家轉為淨賣家、企業金庫需求疲弱的根源,以及這些轉折對比特幣市場結構與價格趨勢的意義。分析過程結合學術供需模型、鏈上數據、監管文件與市場即時觀察,據實評估比特幣現階段的市場地位。

比特幣經濟模型的供給端

比特幣的供給機制,是其最具代表性、最富經濟含義的特質之一。與傳統金融商品供給易受企業策略、央行政策或市場狀態影響不同,比特幣發行遵循固定、不可變的協議機制,內建於其協議之中。這項基礎特性塑造了比特幣市場全貌,也是理解當前供需失衡的關鍵。

新比特幣產生依賴於「挖礦」過程——高效能電腦競速破解加密難題。當礦工成功解題時,可將新交易區塊寫入區塊鏈,並獲得新產出的比特幣作為獎勵。2009年比特幣誕生時區塊獎勵為50 BTC,其協議設計為約每四年(或每210,000區塊)獎勵減半,形構通縮機制。

第四次比特幣減半於2024年4月19日發生,區塊獎勵由6.25 BTC降至3.125 BTC。此舉極大改變了比特幣供給格局。減半前以每10分鐘一區塊計,大致每日新增約900枚比特幣;減半後日新增降至約450枚。以2025年10月價格(約11萬美元)計,每日市場新增供應約5,000萬美元,減半前為1億美元左右。

學界亦發展出分析比特幣固定供應與需求互動的模型。2025年Rudd與Porter於《風險與金融管理期刊》發表,提出專為比特幣設計的供需均衡模型。他們將比特幣完全無彈性的供給曲線,與具有固定替代彈性的需求函數結合,並以2024年減半後真實數據做校準。模擬顯示,只要機構需求稍增,在流動供給有限情況下,便能推動價格顯著升值。

比特幣的減半安排未來仍將持續,至約2140年21,000,000枚全數挖出。目前約1,970萬枚比特幣已產出,為總數約94%。這高比例代表未來減半對總流通量影響遞減,但卻會劇烈改變每日新增供給。

但供給不僅來自新產出。既有持有者行為也深刻影響流通供給。長期持幣者不願在現價出售實際等於減少流通量,儘管這些幣依然存在鏈上。區塊鏈數據顯示,約75%比特幣供給已連續半年未流動,顯現出許多大戶更視比特幣為戰略資產而非交易品。

礦工自身亦受經濟壓力影響新供給釋放。2024年4月減半讓礦工區塊獎勵瞬降一半,迫使產業加速調整以求生存。礦商主要採兩大策略因應:一是升級硬體提升效能,二是轉型布局AI與高效能運算業務等多元收入。

礦業負債規模大增以維持競爭力。根據VanEck分析,2024第二季至2025第二季,比特幣礦商總債務由21億美元激增至127億美元,單年增幅近5倍。龐大負債支應礦機更替與基礎建設投入,並為多元收入做鋪墊。

主要礦商發行了數十億美元的債券及可轉換... notes. TeraWulf 宣布 $3.2 十億美元資優先擔保票據發行,這是上市挖礦公司有史以來最大規模。IREN 完成了 10 億美元可轉換公司債發行,而 Bitfarms 則提出了 3 億美元可轉換票據。季度模式顯示了這波借貸的規模:$4.6 十億美元在 2024 年第四季,隨著減半後 2025 年初降至 2 億美元,第二季反彈至 15 億美元,而僅 2025 年第三季就約為 60 億美元。

這些債務帶來巨額成本。TeraWulf 最近發行的票據 利率為 7.75%,每年約需支付 2.5 億美元利息,幾乎是其 2024 年 1.4 億美元營收的兩倍。這種財務結構使礦工在獲利壓力下,必須積極創造收入,不管是透過比特幣挖礦還是其他業務。當比特幣價格不足以維持盈餘礦業運作時,負債過高的礦工可能被迫出售持有的比特幣,進一步增加供給,在市場不利時點帶來賣壓。

VanEck 的分析師 Nathan Frankovitz 和 Matthew Sigel 將這一挑戰形容為"融化的冰塊問題":礦工每拖一天升級設備,其全球算力佔比就會下降,直接造成每日比特幣收入減少。這樣的競爭態勢迫使企業必須持續投入資本支出,即使區塊獎勵一再減半,舉債循環依舊持續。

因此,比特幣的供給面比單純的發行時間表複雜許多。協議確保新幣產出可預期,但礦工和長期持有者的行為,讓實際可於現貨市場購得的比特幣量變數增加。新幣產出固定、礦業獲利受壓、以及長期持有者意志強烈聯合起來,將供給大幅收緊,特別是在機構需求強勁時更是明顯。當前市場的關鍵問題即是這股需求能否持續。

機構資金流動與比特幣 ETF

現貨比特幣 ETF 於 2024 年 1 月推出,徹底改變了機構資金進入比特幣市場的方式。過往若機構要配置比特幣,往往得克服諸多實務障礙:比方取得加密資產專業託管服務、設立安全流程、面對不確定的法規規範,以及應對不了解數位資產的合規部門。現貨比特幣 ETF 消除了這些摩擦,讓機構可直接透過標準券商帳戶用熟悉、受監管的 ETF 商品獲得比特幣曝險。

美國證券交易委員會於 2024 年 1 月 11 日核准了十一檔現貨比特幣 ETF,成為加密市場重大里程碑。這些商品以實體持幣給投資人提供直接的比特幣現貨價格曝險,不同於早期期貨型 ETF 易產生溢價虧損及追蹤誤差。產品線囊括金融巨頭如 BlackRock、Fidelity、Grayscale、Bitwise、ARK Invest 等,各自爭取機構與散戶配置。

初期需求極為火爆。2024 年 2 月間,現貨比特幣 ETF 平均每日淨流入 2.08 億美元,大幅超過當時每日新挖出約 5,400 萬美元的比特幣。ETF 需求與新幣供給之間的失衡,迅速推動價格飆漲,從 2024 年初約 45,000 美元,一路漲至 2025 年 10 月高點超過 126,000 美元。

BlackRock 的 IBIT 脫穎而出,吸引了自 2025 年初至今 $281 億美元淨流入,遠超其他競品總和。其成功原因在於強大的經銷網絡、品牌及費率競爭力。至 2025 年底,IBIT 賬上持有超過 80.5 萬顆比特幣,市價約 870 億美元,成為全球持幣量最高的比特幣機構之一。

供需動態在 2025 年 5 月達到極致。該月,比特幣 ETF 共買進 26,700 枚 BTC,但礦工同期僅生產 7,200 枚。ETF 買盤與新產出的 3.7 比 1 比例,史無前例。有些週期內,ETF 甚至一週買進 18,644 枚 BTC,遠超當前 450 枚/日產出六倍。

針對比特幣 ETF 價格發現的學術研究已證實這些商品如今主導比特幣價格形成。2025 年發表於《Computational Economics》的研究分析了從 ETF 啟動到 2024 年 10 月的高頻交易數據,運用「信息領導力佔比」指標,發現交易量最高的三檔 ETF ——即 IBIT、FBTC 及 GBTC——在約 85% 的時間內主導了價格發現流程,遠勝於現貨市場。這意味機構資金流已經成為比特幣短期價格的主導因素,原先的加密貨幣現貨交易所角色已被取代。

ETF 運作機制加劇其市場影響力。當出現正流入時,核准參與者需於現貨市場購買比特幣來創建 ETF 新單位,直接推高需求;反之,贖回時則需賣出比特幣以返還現金,形成即時的資金與現貨價格互動機制,讓機構情緒直接反映在市場價格。

然而,2024 年大部分與 2025 年初表現強勁的流入走勢,到夏末開始出現逆轉。至 8 月中旬,機構需求顯現疲態,ETF 與加密資產金庫綜合需求下降,與日常新挖產量接近甚至低於,且此趨勢至 10 月加速惡化。

10 月初看似一片樂觀。現貨比特幣 ETF 在截至 2025 年 10 月 4 日的一週內流入 $35.5 億美元,推升比特幣衝破 126,000 美元創歷史新高。幣圈一片歡騰,社群沸騰,紛紛預言大眾採納與新目標價似乎已是「Uptober」行情必然。不過,這種樂觀情緒轉瞬即逝。

到 2025 年 10 月 20 日,氣氛急轉直下。比特幣 ETF 總計出現 4,047 萬美元流出,僅 BlackRock IBIT 即見 1 億 65 萬美元被贖回,賣壓快速增強。10 月 30 日,比特幣 ETF 錄得 4.88 億美元單日淨流出,十二檔基金無一錄得正流入——一致性的拋售是一大警訊。

分週來看,機構資金退潮格外明顯。至 2025 年 10 月 31 日當週,現貨比特幣 ETF 累計淨流出 6 億美元。自 10 月 11 日起,流出加總已達16.7 億美元,僅數週就徹底逆轉先前的紀錄流入。

即便仍是最大比特幣 ETF,BlackRock IBIT 也遭遇自 8 月 4 日以來最大單日贖回,10 月 30 日單日就流出 2.91 億美元。ARK & 21Shares 的 ARKB 流出 6,562 萬美元,Bitwise 的 BITB 贖回 5,515 萬美元。就連自信託轉成 ETF 以來持續流失資金的 Grayscale 產品,也沒得到其他競品的流入抵消。

短短數週從巨額流入到持續流出的轉折,反映機構情緒能以極快速度逆轉。有多項因素導致這番變化。美聯儲政策不確定性亦是一大主因,因主席 Jerome Powell 在 10 月議決後對 12 月降息表達遲疑。隨之而來的Here’s the translated content in zh-Hant-TW, following your instructions to skip markdown links:

利率預期的重新定價,使得各類資產的風險胃納下降。

宏觀經濟疑慮已不僅止於貨幣政策層面。CryptoQuant 的分析師指出,美國投資人對加密貨幣的需求急劇下降,現貨比特幣 ETF 七日平均流出創下自四月以來最弱。CME 期貨基差降至多年新低,顯示近期交易活動由機構與散戶投資人獲利了結主導,而非有新的資金進場。

然而,最具指標性的發展或許出現在 2025 年 11 月 3 日,當日 ETF 與企業金庫的機構需求,七個月來首次低於每日挖礦產出的供給。這一指標由 Capriole Investments 負責人 Charles Edwards 所追蹤,他將現貨 ETF 流量與企業金庫的數位資產活動綜合,作為機構吸收力道的衡量標準。象徵綜合機構需求的藍線,自三月以來一度持續高於比特幣每日產出的紅線,卻在此時首次跌破,暗示市場結構出現了根本轉變。

Edwards 對此表達憂慮,表示「這是過去幾個月,使我仍然維持比特幣多頭的核心指標,雖然其他資產表現都優於比特幣。」這蘊含明確訊號:當過去吸收超出挖礦產出的機構買盤,成為淨中立或賣方時,比特幣失去了一項推升行情的關鍵支撐。

市場當前面臨的問題是,這是否僅僅是比特幣衝高後的暫時再平衡,還是機構資金對持有加密貨幣的興趣出現結構性變化。答案很可能將決定比特幣在 2025 年剩餘期間乃至 2026 年的走勢。

當需求落後於供給:市場影響的概念化

理解當機構需求低於新增供給時的狀況,需要將比特幣市場看作一個動態均衡體系,價格由可得供給量與競爭出價之互動所產生。有別於傳統商品可因價格訊號而調節產出,比特幣的供給日程完全固定且無法變動,使得「需求」成為短期價格唯一可變的因素。

當前狀況構成這樣一個場景:每天約有 450 枚比特幣透過挖礦獎勵進入市場,在現行情況下對等約五千萬美元新增供給。當 ETF 與企業金庫等機構買家持續吸收超過此數量時,就會造成必須由現有持有人釋出庫存來彌補的供給缺口。願意在現價賣出的持有人,需與機構買盤競爭,這會推升價格,形成更高出價吸引賣家的動力。

反之,當需求短缺於新增供給時,則產生了不同的市場動能。每日獲得 450 枚比特幣的礦工必須做出選擇:持有等待價格上漲,還是為了營運成本、償還債務而出脫。鑒於礦業公司目前承受著重大壓力──產業負債超過 127 億美元,且多家負擔利息已高於總收入──拋售壓力依然沉重。若機構未能消化這些每日產出,礦工則必須尋找其他買家,且可能得以更低價格賣出。

供給需求模型的學術框架,為這些動態提供了洞察。Rudd 與 Porter 的模型顯示,比特幣供給曲線完全缺乏彈性,因此當需求轉折時容易引發極端波動。他們以 2024 年 4 月減半為基礎的分析指出,「機構及主權積累能力,能顯著改變價格趨勢,隨著需求提升,比特幣有限流動性的影響被放大。」

此模型的內涵也可反推:機構積極吸收能迅速拉高幣價,因為壓縮了市場即時可交易供給;相反,機構冷淡或賣壓上升時,則通過增加流通量削弱支撐。當需求長期短缺於新增發行時,剩餘供給必須經過以下幾個途徑進行消化:價格下跌吸引抄底買盤,零售和中小投資人進場接手,或是暫時轉移至交易所持有,等待下一輪買家入場。

鏈上數據呈現了比特幣持有者群體的分布。存放於交易所、隨時可拋售的比特幣儲備,近年降至多年低點,愈來愈多比特幣進入長期存放。這種流動供給的結構性減少,先前放大了 ETF 機構買盤對市場的影響;同理,若交易所儲備持續限制,機構若恢復賣出甚至僅止步於買盤中立,其效果亦會被誇大。

當機構需求減弱時,不同市場參與者行為成為關鍵。散戶通常較機構更受價格波動影響,雖然能進行動態買入,但資金規模有限,未必能補足機構流出。長期持有者──「HODLer」──一般在熊市買進持有,但其需求池終究有限。衍生品市場上的槓桿交易者能帶來短期動能,但只會擴大波動,而非穩定市場。

過往供需失衡時的經驗,為當前提供的參考有限。2024 年 1 月 ETF 推出前,並無可比擬的機構需求管道。比特幣主要透過現貨交易所的全球散戶、礦工,以及對沖基金與企業金庫等早期機構參與者形成價格。ETF 及其認購-贖回機制,代表一種行為尚未完全經歷壓力測試的全新結構性需求來源。

其他資產類別由 ETF 成為主導因子的歷史例子,結果好壞參半。股票市場中,ETF 資金流轉向時,個股波動可能被動加劇,因被動投資壓倒主動投資。黃金等大宗商品市場,ETF 雖重要但非主導,ETF 淨流出往往對價格不利,但實體需求(如珠寶、工業、央行等)仍能一定程度支撐。

比特幣與這些類比有本質不同:它沒有可撐腰的工業需求,無現金流可供估值,作為支付媒介的實際應用有限。比特幣的價值主張主要在於稀缺性、網絡安全,以及作為去相關資產或「數位黃金」的地位──這些都需持有人持續信仰與需求維繫。

當原先用大額資金認證比特幣價值的機構,突然反向操作時,就是對敘事的根本挑戰。這個每日約 450 枚比特幣(折合五千萬美金)之供需缺口,相較於兩兆美元的市值似乎很小,但它正是市場定價的「邊際流動」。如同規模以兆計的石油市場,實際報價大波動常來自每日的百萬桶供需失衡;比特幣每日流向由機構買轉為賣時,價格也會隨之劇烈擺動。

這些影響會在推動價格、波動性與流動性等多層面展現:過去帶動行情的機構買盤轉為賣壓時,漲勢動能轉弱。巨型機構買家退場會讓價格波動擴大、流動性變差,買賣差價擴大、單筆大單沖擊價格更明顯,甚至形成惡性循環:賣壓觸發更多停損、槓桿單遭強平。這種動態往往會持續,直到價格降至有價值投資者願意承接為止。

然而,機構需求與價格之間並非機械式的絕對關聯。比特幣曾多次展現驚人韌性,在歷次大跌後長時間整理並再創新高。市場目前必須判斷,這一波需求疲弱僅僅是…institutional adoption or signals a more fundamental reassessment of Bitcoin's role in professional portfolios. The answer will likely determine whether Bitcoin's latest rally represents a sustainable advance or an exhaustion peak.

機構採納,或是正在對比特幣在專業投資組合中的角色進行更根本性的重新評估。這個問題的答案,很可能會決定比特幣最近一波漲勢是具有持續性的上升,還是即將耗盡的高峰。

Corporate Treasuries and the Digital Asset Treasury Model Under Stress

企業金庫與數位資產金庫模型的壓力考驗

The corporate treasury trend, pioneered by MicroStrategy (now rebranded as Strategy) in 2020 under CEO Michael Saylor's leadership, introduced a novel capital allocation strategy: converting corporate cash reserves into Bitcoin holdings. The approach rested on a straightforward thesis - Bitcoin's fixed supply and disinflationary monetary policy would preserve purchasing power better than cash, which loses value to inflation and opportunity cost. By 2025, this model had expanded dramatically, with over 250 organizations, including public companies, private firms, ETFs, and pension funds, holding Bitcoin on their balance sheets.

由 MicroStrategy(現已更名為 Strategy)執行長 Michael Saylor 於 2020 年率先推動的企業金庫模式,帶來了一種創新的資本分配策略:將企業現金儲備轉換為比特幣持有。這個做法背後的邏輯很簡單——比特幣供給固定且具去通膨的貨幣政策,相比於因通膨與機會成本而持續貶值的現金,更能保住購買力。到了 2025 年,這個模式已大幅擴張,包括超過250家上市公司、未上市公司、ETF 和退休基金,皆已將比特幣納入資產負債表。

The digital asset treasury model operates through a self-reinforcing mechanism during bull markets. Companies issue equity or debt at valuations above their net asset value (NAV) - the per-share value of their Bitcoin holdings - then use proceeds to purchase more Bitcoin. This increases their Bitcoin-per-share metric, theoretically justifying the premium valuation and enabling further capital raises. When Bitcoin's price appreciates, these companies' stock prices often rise faster than Bitcoin itself, creating a leveraged exposure that attracts momentum investors.

這種數位資產金庫模型在牛市期間,形成自我強化的良性循環。企業以高於其淨資產價值(即單位股份背後的比特幣價值)發行新股或債券,並將籌得資金用來購買更多比特幣。這提升了每股比特幣持有量,理論上也支撐了溢價估值,使企業可進一步融資。當比特幣價格上漲時,金庫企業的股價經常漲得比比特幣本身還快,形同槓桿,吸引動能投資人跟進。

Strategy exemplifies this approach at scale. By mid-2025, the company held over half a million BTC, more than half of all Bitcoin held by public companies. Strategy's stock traded at a significant premium to its Bitcoin NAV, typically 1.7 to 2.0 times the underlying asset value, signaling sustained investor confidence in the company's capital allocation strategy and its ability to grow Bitcoin-per-share through disciplined fundraising.

Strategy在這方面成為大規模的典範。到 2025 年中,該公司已持有超過50萬顆比特幣,超過所有上市公司所持比特幣的一半。Strategy 股票常以1.7到2.0倍於其比特幣NAV的顯著溢價交易,顯示投資人對其資本分配策略及持續增加每股比特幣的能力充滿信心。

The model spawned imitators. Companies like Marathon Digital, Riot Platforms, Bitfarms, Cipher Mining, Hut 8, and others transformed from pure-play mining operations into hybrid enterprises holding substantial Bitcoin treasuries. International players joined the trend, with Japan's Metaplanet emerging as a prominent example. The company transformed from an unprofitable hotel business into the fourth-largest Bitcoin treasury firm, accumulating significant holdings through a combination of debt financing, asset sales, and creative financial engineering.

這個模式催生了大量模仿者,Marathon Digital、Riot Platforms、Bitfarms、Cipher Mining、Hut 8 等企業,從單純的挖礦事業轉型為持有大量比特幣金庫的混合型公司。國外業者亦加入此潮流,日本的 Metaplanet 就是一個鮮明案例——該公司從虧損旅館事業轉型成為全球第四大比特幣金庫公司,透過債務融資、資產出售和創新的金融工程,快速累積比特幣持有量。

By late 2024 and into 2025, approximately 188 treasury companies had accumulated substantial Bitcoin positions, many with minimal business models beyond Bitcoin accumulation. These entities effectively operated as publicly traded Bitcoin proxies, offering investors leveraged exposure to cryptocurrency price movements through traditional equity markets. During Bitcoin's ascent, this structure worked brilliantly, generating impressive returns for early participants.

到了2024年底至2025年,約188家金庫公司已累積大量比特幣持倉,許多企業除持有比特幣外,幾乎沒有其他營運模式。這些公司實際上作為比特幣的上市代理,讓投資人透過傳統股票市場,用槓桿參與加密貨幣價格波動。比特幣走升階段,這種結構十分奏效,為早期參與者創造了可觀報酬。

However, the model contains inherent fragilities that surface during periods of price weakness or market skepticism. The central risk involves a scenario researchers describe as the "death spiral" - a cascading failure triggered when a company's stock price falls too close to or below its Bitcoin NAV. When this happens, the multiple of NAV (mNAV) that justified further capital raises compresses or disappears entirely. Without the ability to issue equity at premiums to NAV, companies lose their primary mechanism for acquiring more Bitcoin without diluting existing shareholders.

然而,這個模式本身具有脆弱性,在價格走弱或市場質疑時就會暴露。當公司股價過度貼近甚至跌破其比特幣NAV時,便可能發生所謂「死亡螺旋」——這是一種連鎖失敗。屆時,本可作為融資依據的mNAV(市價對NAV倍數)壓縮甚至消失,公司無法以溢價發行新股,自然無法以不稀釋舊股東的方式增持比特幣。

A Breed VC report outlined seven phases of decline for Bitcoin treasury companies. The sequence begins with a drop in Bitcoin's price that reduces the company's NAV premium. As market capitalization contracts relative to Bitcoin holdings, access to capital tightens. Without equity buyers or willing lenders, companies cannot expand holdings or refinance existing Bitcoin-backed debt. If loans mature or margin calls trigger, forced liquidations follow, depressing Bitcoin's price further and dragging other treasury companies closer to their own spirals.

一份 Breed VC 報告指出比特幣金庫公司的衰退有七個階段。首先是比特幣價格下跌,使公司NAV溢價收斂。當企業市值相對於比特幣持有量收縮,籌資能力也隨之削弱。若無人願意認購新股、也無法取得新貸款,公司既無法擴張持倉,也無法將既有比特幣做抵押的債務再融資。如果貸款到期或觸發追繳保證金,只能被迫平倉,進一步壓低比特幣價格,把其他金庫公司拖向自己的死亡螺旋。

By October 2025, signs of this stress had become apparent. Net asset value premiums collapsed across the digital asset treasury sector. According to a 10x Research analysis, "The age of financial magic is ending for Bitcoin treasury companies. They conjured billions in paper wealth by issuing shares far above their real Bitcoin value - until the illusion vanished." Retail investors who paid two to seven times the actual Bitcoin value when buying treasury company shares during periods of hype saw those premiums evaporate, leaving many shareholders underwater while companies converted inflated capital into real Bitcoin holdings.

到 2025 年十月,這種壓力跡象已十分明顯。整個數位資產金庫業的NAV 溢價全面崩潰。根據10x Research 分析,「比特幣金庫公司金融魔法的時代即將終結。它們靠股價遠高於實際比特幣價值發行新股,創造出數十億紙上財富——但幻象最終破滅。」熱潮時期以兩倍到七倍實際 NAV 買入的散戶股東,看到溢價灰飛煙滅,許多人陷入套牢,公司則將虛高資本兌換成實際比特幣持有。

Metaplanet's experience illustrates the boom-bust dynamic. The company effectively transformed a market capitalization of $8 billion, supported by just $1 billion in Bitcoin holdings, into a $3.1 billion market cap backed by $3.3 billion in Bitcoin. The compression from an 8x premium to trading near or below NAV represented wealth destruction for equity holders even as the company accumulated more Bitcoin. Strategy experienced a similar pattern, with its NAV premium compressing significantly from November 2024 peaks, resulting in a slowdown of Bitcoin purchases.

Metaplanet 的經驗充分體現這種盛衰循環。公司曾以80億美元的市值,背後僅有10億美元比特幣持倉,後來市值壓縮到31億美元,卻有33億美元比特幣支撐。從8倍溢價到貼近甚至低於NAV交易,代表股東財富劇烈蒸發,即使公司實際比特幣持有增加。Strategy 也歷經一樣狀況,NAV溢價自2024年11月高點大幅壓縮,導致比特幣購買速度明顯放緩。

The debt burden these companies accumulated amplifies downside risks. By 2025, Bitcoin treasury companies had collectively raised approximately $3.35 billion in preferred equity and $9.48 billion in debt, according to Keyrock Research. This creates a wall of maturities concentrated in 2027 and 2028, along with ongoing interest and dividend payments through 2031. Companies' ability to service these obligations depends heavily on Bitcoin maintaining price levels that support their business models.

這些公司積累的債務進一步放大下行風險。根據 Keyrock Research,至2025年比特幣金庫公司共發行約33.5億美元優先股與94.8億美元負債。這形成2027、2028年債務集中到期壓力,以及直到2031年間持續的利息、股息支出。它們償付這些義務的能力,極度仰賴比特幣價格能否維持支撐營運的區間。

Cash flow from underlying core businesses varies dramatically across the treasury company cohort. Strategy generates software licensing revenue that provides some cash flow cushion. Mining companies like Marathon and Riot produce Bitcoin directly, though at costs that fluctuate with hashrate difficulty and energy prices. Some treasury companies lack meaningful operating businesses entirely, relying exclusively on capital markets access to sustain operations and acquire more Bitcoin.

這些金庫公司本業現金流強弱不一。Strategy 有軟體授權金可支撐現金流、Marathon 與 Riot 等礦商則直接生產比特幣,但成本會隨算力難度及能源價格起伏。有些公司甚至完全沒有具體營運,只能依賴資本市場籌資維持營運與增購比特幣。

The weakening demand from digital asset treasuries compounds the broader institutional demand shortfall. When these companies actively accumulated Bitcoin, they provided consistent buying pressure that helped absorb mining output alongside ETF flows. As NAV premiums collapsed and capital markets access tightened, treasury companies' Bitcoin acquisition pace slowed or stopped entirely, removing another significant demand channel from the market.

數位資產金庫需求減弱,加劇整體機構需求低迷的壓力。當這些公司積極買入時,除了 ETF 流量外,還能一併吸收挖礦新供給,形成穩定買盤來源。而隨著NAV溢價崩跌、資本市場籌資困難,金庫公司的比特幣增持速度趨緩甚至停滯,市場又少了一個重要需求管道。

The structural issues extend beyond individual company health to broader market implications. If overleveraged treasury companies face forced liquidations to meet debt obligations or margin calls, they add to selling pressure precisely when Bitcoin least needs additional supply. The interconnected nature of these companies' fortunes means that weakness in one can cascade through the sector, as declining Bitcoin prices compress all NAVs simultaneously, limiting everyone's capital-raising ability.

這些結構性問題,不僅限於單一公司的經營壓力,更影響市場整體。如果高槓桿金庫公司因還債或保證金追繳而被迫平倉,會在比特幣最不需要賣壓時,加重拋售壓力。這些公司命運互相連動,一家出現問題,市場下跌將壓縮所有公司的NAV,進一步限縮各自的募資能力。

Fortunately, most treasury companies in 2025 still rely primarily on equity financing rather than extreme leverage, limiting contagion risk if some entities fail. Strategy's approach of balancing equity issuance with convertible debt, maintaining conservative loan-to-value ratios, and actively managing its capital structure provides a template for sustainable Bitcoin treasury operations. However, the sector's growth attracted less disciplined operators whose capital structures may prove unsustainable if Bitcoin consolidates or corrects from recent highs.

所幸,2025 年多數金庫公司仍以發行新股為主,並未極端槓桿化,某些玩家出現問題時,傳染風險也較可控。Strategy 平衡新股發行與可轉債,維持保守的貸款成數,且積極管理資本結構,為比特幣金庫可長可久的經營提供典範。不過,該領域成長也吸引不少缺乏紀律的經營者,他們的資本結構若遇比特幣盤整或回檔恐不堪考驗。

The 10x Research analysis suggests that the NAV reset, while painful for equity holders, creates a cleaner foundation for the next market phase. Companies now trading at or below NAV offer pure Bitcoin exposure with optionality on future operational improvements. The shakeout "separated the real operators from marketing machines," suggesting that survivors will be better capitalized and capable of generating consistent returns. Whether this optimistic view proves correct depends partly on whether Bitcoin's price can stabilize and resume its upward trajectory, restoring the conditions that made the treasury model viable in the first place.

據10x Research 分析,這波NAV重置雖讓股東受傷,卻為下一波市場行情打下更紮實的基礎。如今以NAV或低於NAV交易的公司,能為投資人提供純粹比特幣曝險,加上日後經營改善的潛在加分。這次淘汰賽「讓真正的經營者得以存活,把市場包裝者淘汰出局」,存活者資本結構更健全,長期穩定獲利的可能性更大。這種樂觀解讀是否能成真,部分要看比特幣價格能否穩定、重新上揚,重現金庫模式最初可行的市場條件。

Contrasting Periods: When ETFs Absorbed Supply Faster Than Mining

對比期:當ETF吸納速度超越開採產量

The period from late 2024 through mid-2025 represented Bitcoin's golden age of institutional demand dominance. During these months, the combination of spot

2024 年底到 2025 年中,是比特幣機構需求主導的黃金時代。在這幾個月——ETF flows and corporate treasury accumulation consistently exceeded daily mining output, often by substantial margins. This dynamic created what supply-demand frameworks describe as a supply shock - a structural imbalance where available supply fails to meet demand, forcing prices higher to attract sellers from existing holders.

ETF流與企業庫藏資產的累積,一直穩定且大幅超過每日挖礦產量。這樣的動態產生了供需理論中所謂的「供應衝擊」——也就是現有供應無法滿足需求,導致價格必須提高,以吸引既有持有者願意出售。

May 2025 exemplified this pattern at its extreme. As documented earlier, Bitcoin ETFs purchased 26,700 BTC while miners produced only 7,200 BTC during that month. This 3.7-to-1 ratio meant institutions absorbed nearly four times the new supply entering circulation. Some weekly periods showed even starker imbalances, with ETFs buying 18,644 BTC in a single week when daily production averaged 450 BTC. At these rates, institutional buyers absorbed the equivalent of more than 40 days of mining output in just seven days.

2025年5月就是這種模式發揮到極致的例子。正如先前所記錄,當月比特幣ETF 購入了26,700顆BTC,而礦工僅產出7,200顆BTC,呈現3.7比1的比例,意味機構幾乎吸收了四倍於市場新增供給量。有些週期失衡更為嚴重,ETF甚至在某一週單週購入18,644顆BTC,當時每日產量平均僅為450顆BTC。依此推算,機構買家在短短七天內吸收超過40天的產出。

The macroeconomic context supported this aggressive accumulation. Bitcoin reached $97,700 in early May, posting approximately 4% gains before pulling back to around $94,000. The relatively mild correction following such rapid appreciation, combined with continued institutional buying, signaled robust underlying demand. Each dip found buyers willing to absorb available supply, creating a rising floor under prices that emboldened further institutional allocation.

宏觀經濟背景支持了這種激進的累積行為。比特幣在5月初突破$97,700,短線上漲約4%,其後僅回落至約$94,000。在快速上漲後的修正幅度十分溫和,再加上機構持續買入,顯示出背後有強勁的基本需求。每次價格回落,都有買家承接市場拋售,形成不斷墊高的價格底部,進一步激勵機構配置。

BlackRock's IBIT demonstrated particular strength during this period, posting 17 consecutive days without capital outflows, a remarkable streak indicating sustained institutional conviction. The fund raised nearly $2.5 billion over just five days, showcasing the velocity of capital flowing into Bitcoin through ETF wrappers. By this point, spot Bitcoin ETFs collectively surpassed $110 billion in assets under management, representing a substantial portion of Bitcoin's accessible supply locked into these vehicles.

貝萊德的IBIT在這段期間展現了特別強勢,連續17天零資金流出,凸顯機構信心的持續性。該基金僅在五天之內就吸引了近25億美元資金,展現資本大量湧入ETF包裝比特幣的速度。此時,現貨比特幣ETF的管理資產總額已超過1,100億美元,等同於比特幣可用供應量中,相當可觀的部分被鎖定在這些產品內。

The concentrated nature of this demand intensified its market impact. With BlackRock's IBIT alone absorbing such massive flows, single-day purchase requirements could exceed multiple days of mining output. Authorized participants creating new ETF shares had to source real Bitcoin from spot markets, often executing large block trades that removed coins from exchange inventories. This mechanical buying pressure operated independently of traditional supply-demand signals, as ETF flows reflected allocation decisions made days or weeks prior rather than real-time price-sensitive trading.

這種需求的集中性讓其市場影響力更為強烈。僅貝萊德IBIT一檔產品,其單日購買需求就常常超過數天的挖礦產量。授權參與人為創造ETF新份額,必須從現貨市場購買真實的比特幣,通常以大宗交易方式從交易所庫存中移除流通幣。這種機械式買盤獨立於傳統供需信號,因為ETF流入反映的是數天或數週前的配置決策,而非即時、對價格敏感的交易行為。

Analysis from 2025 shows that institutional demand surpassed new supply by 5.6 times over extended periods. Institutions accumulated 545,579 BTC while miners produced only 97,082 BTC during comparable timeframes. This sharp imbalance fundamentally altered Bitcoin's market structure, transforming the cryptocurrency from an asset primarily traded on fragmented spot exchanges to one increasingly influenced by institutional flows through regulated U.S. ETF channels.

2025年的分析顯示,在較長的時段內,機構需求超越新產出5.6倍。具體來說,機構累積了545,579顆BTC,而礦工同期僅生產97,082顆BTC。如此劇烈的不平衡,徹底改變了比特幣的市場結構,使其由原本碎片化現貨交易所間運作的資產,漸漸轉變為受美國受監管ETF資金流所主導。

The supply shortage manifested in observable market behaviors. Exchange balances - representing Bitcoin held on trading platforms and theoretically available for sale - declined to six-year lows. Long-term holders refused to sell at prevailing prices, anticipating further appreciation driven by continued institutional accumulation. The combination of reduced exchange inventories and aggressive ETF buying created conditions where even modest additional demand moved prices significantly.

供應短缺反映在可觀察到的市場行為上。交易所錢包餘額——即比特幣在交易平台上的存量,也就是理論上可拋售的部位——降到六年新低。長期持有者拒絕在現價出售,預期機構持續累積將推升價格。交易所庫存減少與ETF積極買盤並存,即使增量需求不大也能帶動明顯的行情上漲。

This dynamic validated the bullish thesis that had driven Bitcoin from the low $40,000s at the start of 2024 to eventual peaks above $126,000 in October 2025. The rally's fundamental underpinning rested on quantifiable supply-demand imbalances rather than speculative fervor or leverage buildup. When institutions consistently absorbed multiples of new supply, price appreciation became almost mechanical, with each successive wave of buying forcing prices to levels that would attract sufficient selling from existing holders.

這種結構性的動力,驗證了支撐比特幣從2024年初4萬多美元低點一路漲至2025年10月超過$126,000高峰的多頭論點。這波行情的基本支柱是可量化的供需失衡,而非單純投機熱潮或槓桿堆積。當機構一再將新增供應數倍於消化,價格幾乎變得自動上升,每一波買盤都推動行情來到足以刺激既有持有者釋出籌碼的價位。

The April 2024 halving amplified these effects. By cutting daily issuance from 900 to 450 BTC, the halving reduced new supply by 50% while institutional demand continued growing. Pre-halving, ETFs absorbed roughly 3 times daily mining output. Post-halving, with production cut in half, the same institutional buying represented 6 times or more of new supply. This mathematical reality created powerful upward pressure that persisted for months.

2024年4月的減半效應進一步放大這一現象。減半將每日發行量由900顆縮減至450顆,令新供給瞬間縮減一半,機構需求則持續增長。減半前,ETF大約吸收3倍於每日挖礦產出;減半後,產量腰斬,類似的買盤代表著6倍甚至更多的新增供給。這種算術上的現實,製造了強勁且持續數月的上漲壓力。

Academic modeling suggests these supply shocks can trigger hyperbolic price trajectories under certain conditions. When liquid supply drops below approximately 2 million BTC while institutional demand remains strong, relatively modest daily purchases can drive exponential price appreciation. The Rudd and Porter framework demonstrates that institutional accumulation rates of 1,000-4,000 BTC per day, easily achievable given observed ETF flows, could lead to six- or seven-figure Bitcoin prices over multi-year horizons if sustained.

學術模型指出,在某些條件下,這類供應衝擊會引發拋物線式的價格走勢。當流動性供給降到約200萬顆BTC以下,而機構需求仍然旺盛時,即便日成交新增買盤規模不大,也能快速推動價格呈指數型上升。Rudd與Porter等人的模型顯示,若機構每日吸納1,000至4,000顆BTC(現實中由ETF流入可輕易達到),長期而言足以推動比特幣價格衝上六七位數美元。

The contrast between this earlier period of institutional demand dominance and the current environment where demand lags supply illustrates Bitcoin's sensitivity to marginal flow changes. Despite Bitcoin's approximately $2 trillion market capitalization, daily flows measured in tens of millions of dollars drive short-term price action. When institutions flip from absorbing 3-5 times daily production to absorbing less than daily production, the impact manifests quickly in price momentum and volatility.

這段機構需求主導期與當今需求低於供給的市場情境形成強烈對比,突顯比特幣對資金流向邊際變化的敏感性。即使比特幣市值約為2兆美元,每日僅數千萬美元的資金流向仍能主導短線行情。一旦機構由吸收3到5倍於每日產出,轉為連當日產出都吸收不完,價格動能與波動便會迅速反應。

The sharp reversal from record inflows in early October to sustained outflows by month's end exemplifies this volatility. Bitcoin peaked above $126,000 on the strength of those early October inflows, only to consolidate in the $105,000-$110,000 range as outflows persisted through month's end. The $20,000+ decline from peak to trough occurred over just a few weeks, demonstrating how quickly sentiment can shift when the marginal buyer - in this case, institutional ETF allocators - steps away from the market.

10月初創紀錄資金流入轉為月底持續流出,就是這種波動性的最佳寫照。比特幣在10月初資金灌入助推下突破$126,000,但隨著本月流出生效,價格迅速回落至$105,000至$110,000區間盤整。短短數週內出現2萬多美元的波幅,突顯只要邊際買家——這裡指的就是ETF機構分配者——選擇離場,市場情緒變化之迅速。

The question facing investors now is whether institutional demand will resume levels that exceed supply, restoring the favorable dynamics that powered Bitcoin's rally, or whether the current demand weakness persists or worsens, forcing a more substantial repricing. Historical precedent offers limited guidance, as spot Bitcoin ETFs represent a structural innovation whose behavior through complete market cycles remains unknown. The answer will likely emerge through the daily flow data that has become the most closely watched real-time indicator of Bitcoin's institutional adoption trajectory.

投資人現在面臨的問題,是機構需求是否會回升到超越供給、重啟支撐比特幣大漲的有利動態,還是目前需求疲軟將持續甚至惡化,迫使市場進行更大幅度的再定價。歷史經驗能提供的參考相當有限,因為現貨比特幣ETF本身就是結構創新,其在完整市場週期中的表現尚未可知。答案或許只會在每日交易流量數據中漸漸揭露,而那也是目前最受矚目的比特幣機構採納即時指標。

Macro, Regulatory, and Sentiment Factors Driving Demand Changes

驅動需求變動的總體經濟、監管及市場情緒因素

The dramatic shift in institutional Bitcoin demand through late 2025 reflects a convergence of macroeconomic headwinds, regulatory uncertainties, and evolving market sentiment. Understanding these factors provides context for why previously aggressive institutional buyers suddenly retreated, allowing demand to fall below new supply for the first time in months.

2025年下半年機構比特幣需求劇烈轉變,其本質反映出總體經濟逆風、監管不確定性與市場情緒持續變化的交織。理解這些因素,有助於解釋為何此前積極的機構買家忽然退縮,結果是數月來首次出現需求低於新增供給的局面。

Monetary policy represents the primary macroeconomic force shaping institutional risk appetite. The Federal Reserve's cautious stance on further rate cuts introduced uncertainty precisely as Bitcoin approached its all-time highs. Following the central bank's October 2025 rate reduction, Chair Jerome Powell cast doubt on a December move, noting that another cut was "far from guaranteed." This statement triggered repricing across risk assets, with investors recalibrating expectations for the pace of monetary easing.

貨幣政策無疑是主導機構風險偏好的主要總體經濟力量。美國聯準會對進一步降息的審慎態度,正值比特幣挑戰歷史新高時,為市場增添不確定性。2025年10月央行宣布降息後,主席鮑爾對12月再降息表示懷疑,強調未來降息「毫無保證」。這番言論引發風險資產再評價,投資人同步重新調整對寬鬆節奏的預期。

Bitcoin's correlation with broader risk assets intensified through 2024 and 2025. Analysis shows Bitcoin's correlation with the S&P 500 reached 0.77 by 2024, up from 0.3 in 2020, transforming Bitcoin from an uncorrelated alternative asset into a high-beta extension of equity market risk appetite. When equity markets face pressure, as occurred following disappointing tech earnings in late October 2025, Bitcoin absorbs proportional or amplified selling pressure. The cryptocurrency's inverse correlation with the U.S. Dollar Index reached -0.72 by 2024, meaning dollar strength, often associated with risk-off positioning, coincides with Bitcoin weakness.

2024至2025年間,比特幣與主流風險資產的相關性進一步升高。分析指出,比特幣與S&P 500指數的相關係數至2024年已升至0.77,遠高於2020年的0.3,使比特幣由原本的非相關資產,變成股市風險偏好的高貝塔延伸。當股市受壓,例如2025年10月底科技企業財報表現不佳後,比特幣也承受類似甚至更猛烈的賣壓。同時,比特幣對美國美元指數的負相關係數也達到-0.72,意即美元走強——通常意味避險偏好提升——也同步壓抑比特幣表現。

Interest rate expectations directly influence institutional capital allocation decisions. When Treasury yields rise on expectations of sustained higher rates, the opportunity cost of holding non-yielding assets like Bitcoin increases. Institutional allocators face pressure to justify Bitcoin positions when risk-free rates offer attractive returns without the volatility inherent in cryptocurrency markets. The repricing of rate expectations following Powell's October comments contributed to the institutional selling that manifested in Bitcoin ETF outflows.

利率預期直接影響機構資本配置的決策。當公債殖利率因高利率常態化的預期而走高,持有像比特幣這樣無孳息資產的機會成本迅速上升。當無風險利率已能取得誘人報酬,而無須承擔加密貨幣那種高波動,機構分配人必須額外說服自己持續持有比特幣。鮑爾十月談話使市場利率預期重新定價,這一變化直接導致比特幣ETF發生明顯資金流出。

Broader macroeconomic anxiety amplified these dynamics. Persistent inflation, elevated interest rates, and uncertainty around Fed policy created an environment of heightened caution

更廣泛的總經焦慮也加劇了這些動態。持續的通膨、高企的利率,以及聯準會政策的不確定性共同營造出比以往更為謹慎的市場氛圍。among institutional investors. The specter of a potential U.S. government shutdown in late October added to political uncertainty, prompting risk reduction across portfolios. Crypto-specific concerns, including periodic exchange security incidents and regulatory enforcement actions, maintained elevated risk premiums for cryptocurrency exposure.

在機構投資人之間,美國政府可能於十月底關門的陰影,加深了政治不確定性,促使投資組合普遍降低風險。針對加密貨幣的特殊疑慮,包括交易所偶發的安全事件及監管執法行動,使持有加密貨幣的風險溢價維持在高檔。

The regulatory landscape presents a complex picture of progress mixed with ongoing uncertainty. The January 2024 approval of spot Bitcoin ETFs represented a watershed regulatory endorsement, validating Bitcoin's legitimacy as an investable asset class for institutional participants. However, questions about broader cryptocurrency regulation, particularly regarding the classification and treatment of other digital assets, continue creating uncertainty.

監管環境呈現出進展與持續不確定性交織的複雜局面。2024年1月現貨比特幣ETF獲批可說是監管上的關鍵里程碑,確認了比特幣作為機構投資人可投資資產類別的合法地位。然而,對於更廣泛加密貨幣監管的相關問題,特別是其他數位資產的歸類與處理,仍舊帶來不確定性。

The Trump administration's stance on cryptocurrency regulation generated initial optimism but uncertain execution. While campaign rhetoric suggested a more favorable regulatory environment for digital assets, specific policy implementations remained ambiguous through late 2025. The Securities and Exchange Commission's leadership transition, with Paul S. Atkins confirmed as Chairman in April 2025, raised expectations of accelerated approvals for additional cryptocurrency products and greater regulatory clarity. However, translating pro-crypto sentiment into concrete policy changes proved slower than markets anticipated.

川普政府在加密貨幣監管上的立場最初帶來樂觀情緒,但執行卻充滿不確定性。雖然競選言論曾暗示將為數位資產帶來更友善的監管環境,但直到2025年底,具體政策推動仍不明朗。隨著2025年4月Paul S. Atkins被確認為證券交易委員會(SEC)主席,市場對加密貨幣產品加速審批與監管明朗化期待升高。然而,將挺加密貨幣的立場轉化為具體政策的速度,比市場預期慢得多。

Institutional investors particularly value regulatory clarity, as compliance frameworks and capital requirements depend on definitive classification of assets and activities. The absence of comprehensive cryptocurrency legislation or clear agency guidance keeps many large allocators, particularly those subject to strict fiduciary standards, cautious about significant cryptocurrency exposure. Until major regulatory questions find resolution, a subset of potential institutional demand remains locked out despite the availability of regulated ETF access.

機構投資人極為重視監管明確性,因為合規架構及資本要求均取決於對資產及活動的明確分類。缺乏全面的加密貨幣立法或明確機關指引,使得許多大型配置者──特別是受嚴格受託責任約束者──在大幅投資加密貨幣時保持審慎。只要主要監管問題尚未解決,就算已經有受監管的ETF可用,部分潛在機構需求仍被排除在外。

Market structure considerations influenced institutional behavior during late 2025. The concentration of ETF assets in BlackRock's IBIT raised concerns about systemic risk. As one analysis noted, removing IBIT's influence, the remaining ETF sector would have seen net outflows of $1.2 billion through 2025. This concentration meant that any change in BlackRock's flows or client sentiment could disproportionately impact overall ETF demand. When IBIT experienced its largest single-day redemption since August on October 30, 2025, it signaled that even the most successful fund faced selling pressure.

市場結構的考量於2025年底影響了機構行為。ETF資產過度集中於貝萊德的IBIT,引發了系統性風險的疑慮。正如某份分析所指出,若排除IBIT的影響,其餘ETF行業到2025年將累計有12億美元淨流出。如此集中的狀況意味著,貝萊德資金流動或客戶信心的任何變化,都會對整體ETF需求產生不成比例的影響。當IBIT在2025年10月30日出現自八月以來最大單日贖回時,這表示即便是最成功的基金也面臨了賣壓。

Sentiment indicators reflected deteriorating market psychology. The Fear & Greed Index slid deeper into "fear" territory through late October, suggesting that trader confidence eroded even as prices remained elevated by historical standards. Social media discussion shifted from euphoria during the "Uptober" rally to anxiety and debate about market sustainability following the reversal to outflows. This sentiment shift often becomes self-reinforcing, as deteriorating confidence prompts selling that validates concerns and triggers additional selling.

市場情緒指標反映出市場心理惡化。恐懼與貪婪指數在十月底進一步滑向「恐懼」區間,顯示即使價格仍處在歷史高水位,交易者信心卻已流失。社群媒體討論自「Uptober」行情時期的狂喜,轉變為對市場持續性的焦慮與辯論,而這種情緒變化往往會自我強化──信心惡化催生賣壓,而賣壓的出現又印證了憂慮,進一步引發更多賣出。

Technical factors contributed to the demand shift. Bitcoin's rapid appreciation to $126,000 extended significantly above psychological resistance levels and moving averages that had contained prior rallies. When prices stretched too far too fast, profit-taking became rational behavior for institutions that had accumulated at much lower levels. The absence of sustained follow-through buying above $120,000 suggested exhaustion of near-term demand, prompting technically-oriented traders to reduce exposure or establish short positions.

技術面因素也助長了需求轉變。比特幣價格迅速攀升至12萬6千美元,大幅突破了心理壓力區及過去限制多頭行情的移動平均線。當價格漲幅過大過快,對於以往低價累積部位的機構來說,適時獲利了結成為合理行為。價格始終無法在12萬美元以上持續買盤,顯示短期需求疲乏,促使偏重技術分析的交易者減碼或甚至建立空頭部位。

The derivatives market structure provided additional insight into institutional positioning. CME Bitcoin futures basis - the premium of futures contracts over spot prices - dropped to multi-year lows through late October. This compression typically indicates that participants prefer selling futures rather than establishing long positions, suggesting skepticism about near-term appreciation. Low funding rates on perpetual futures contracts confirmed limited demand for leveraged long exposure, as speculators avoided paying carry costs to maintain bullish positions.

衍生品市場結構對機構部位提供了進一步線索。芝加哥商業交易所(CME)比特幣期貨溢價——即期貨合約價格相對現貨價的溢價幅度——在十月底跌至多年新低。這種收斂通常代表市場參與者傾向賣出期貨而非建立多單,說明對短期漲勢的懷疑情緒。永續合約資金費率偏低,證實槓桿多單的需求有限,投機者不願意為維持做多部位而支付持倉成本。

Institutional portfolio rebalancing may have contributed to outflows. Bitcoin's strong performance through 2024 and into 2025 increased its weight in portfolios that initially established small positions. When position sizes grow beyond target allocations, institutional investors face pressure to trim regardless of short-term price views, particularly approaching year-end when performance gets locked in. This mechanical selling from rebalancing can occur independently of fundamental views on Bitcoin's long-term prospects.

機構投資組合的再平衡可能也推動了資金流出。比特幣在2024到2025年的強勢表現,使得原本小比例投資比特幣的組合權重大幅上升。當部位超出既定配置目標時,機構投資人無論短線看法如何,往往都會面臨減碼壓力,特別在年底績效結算時更是如此。這種純屬再平衡的賣壓往往與比特幣長期前景的基本面看法無關。

The interplay of these factors - monetary policy uncertainty, regulatory ambiguity, deteriorating sentiment, and technical exhaustion - created conditions where institutional demand that previously dominated market flows shifted to selling or neutrality. The mathematical outcome manifested in the early November crossing point where institutional demand fell below daily mining supply. Whether this represents a temporary consolidation phase or a more concerning reversal of institutional adoption trends remains the central question for Bitcoin's near-term outlook.

在這些因素——貨幣政策不確定性、監管曖昧、情緒惡化與技術面疲乏——交互作用下,原本主導市場資金流向的機構需求轉向賣出或觀望。其數據化結果就是在11月初,機構需求首次低於每日比特幣新增供給。這究竟只是短暫的盤整,還是機構採納趨勢的逆轉,成為比特幣短線展望的核心問題。

Risks and Consequences for Bitcoin Price and Market Structure

比特幣價格及市場結構之風險與後果

The sustained period where institutional demand trails daily Bitcoin production introduces several interconnected risks for price stability and market structure. Understanding these risks requires examining potential scenarios ranging from benign consolidation to more concerning demand deterioration, along with their implications for different market participant groups.

當機構需求長期低於每日比特幣產出時,會為價格穩定性及市場結構帶來多重連鎖風險。認識這些風險,需要評估從單純盤整到更令人憂心的需求惡化等不同情境,以及這些情境對各類市場參與者的可能影響。

The most immediate risk involves continued downward price pressure if institutional selling persists or accelerates. Bitcoin's October peak above $126,000 established a local top that markets have so far failed to reclaim. Each attempt to rally back toward that level faces selling pressure, creating a pattern of lower highs that technical analysts interpret as trend deterioration. Without renewed institutional buying through ETFs to absorb both daily mining supply and existing holder selling, Bitcoin faces the prospect of testing lower support levels.

最直接的風險,是若機構賣壓持續或加劇,比特幣價格將面臨持續下行壓力。比特幣在十月超過126,000美元的高點成為近期頂部,至今市場尚未能重新企及。每一次試圖反彈至此區間都遇到賣壓,形成技術分析所謂的「波段高點下移」型態。若無新的機構買盤透過ETF吸收每日礦工產出與舊持有人的賣壓,比特幣恐將測試更低的支撐區。

The $100,000 to $105,000 range represents the first major support zone where buyers might emerge in sufficient size to stabilize prices. This level coincides with several technical factors: the 200-day moving average, previous consolidation areas that may now serve as support, and psychological importance as a round number. However, if institutional selling intensifies or if macro conditions deteriorate further, this support could fail, opening the possibility of deeper corrections toward $90,000 or even the $80,000 levels that marked prior local highs.

十萬至十萬五千美元區間,是首個有機會出現足夠買盤以穩定價格的主要支撐帶。這一價格區疊合了數個技術面因素:200日移動均線、過去的整理區,如今都可能成為支撐,同時也是市場關注的整數心理防線。然而,若機構賣壓加重或宏觀環境進一步惡化,這層支撐也有失守的可能,屆時可能會下修到九萬,甚至是曾經的地方高點八萬美元。

Volatility represents another significant consequence of reduced institutional participation. Large institutional buyers provide market stability through patient, price-insensitive accumulation based on strategic allocation decisions. When these participants exit, markets become more susceptible to sharp moves driven by smaller, more price-sensitive traders and leveraged speculators. The $1 billion in liquidations that occurred during October's market correction illustrates this dynamic - when prices fall, stop-losses trigger and leveraged long positions face forced selling, creating cascading declines that exacerbate volatility.

波動性則是機構參與減少帶來的另一重大後果。大型機構買家通常透過具策略性的長線累積進場,不會受短期價格波動影響,有助於穩定市場。當這些玩家退出後,市場更容易受到規模較小、短期對價格高度敏感的交易者及槓桿投機者的衝擊。十月市場修正期間出現的10億美元強平就反映了這一現象——當價格下跌時,停損觸發及槓桿多單被強制賣出,產生連鎖下殺,造成波動進一步放大。

Increased volatility creates challenges for institutional adoption even beyond the immediate market turbulence. Pension funds, endowments, and other conservative institutional investors require relatively predictable risk characteristics for position sizing and risk management. When volatility spikes, these participants reduce position sizes or avoid the asset entirely, creating a negative feedback loop where reduced institutional participation increases volatility, which further deters institutional participation.

波動加劇不僅使短期市場震盪擴大,對於機構持續採納比特幣更形成長期阻力。退休基金、捐贈基金及其他保守型機構投資人,配置部位與風控時都要求較能預期的風險特徵。一旦波動飆升,這些機構馬上縮減持倉或完全退出該資產,形成「機構退出-波動升高-機構更不願參與」的負向循環。

Market depth and liquidity suffer when large buyers withdraw. Order books on exchanges become thinner, meaning that large transactions face greater price impact. Bid-ask spreads widen, increasing execution costs for all market participants. This liquidity deterioration particularly affects institutional-sized trades, potentially creating a vicious cycle where poor execution quality discourages institutional participation, which further degrades liquidity.

當大型買家撤出時,市場深度與流動性都會惡化。交易所的掛單簿會變得單薄,意即大單成交時價格衝擊放大。買賣價差擴大,導致所有參與者的成交成本上升。這種流動性下滑,對機構級的大額交易傷害最大,甚至可能形成惡性循環──成交品質不佳讓機構不願參與,進而導致流動性進一步惡化。

The shift in price discovery mechanisms represents a structural change with lasting implications. Research shows Bitcoin ETFs dominate price discovery approximately 85% of the time since their launch, meaning that institutional flows through these regulated products drive short-term price formation more than spot exchange activity. When ETF flows turn negative, price discovery shifts back toward fragmented spot exchanges where trading is often more speculative and less informed by fundamental allocation decisions. This transition can increase noise in price signals and reduce market efficiency.

價格發現機制的轉變代表結構性、長遠的改變。研究顯示,比特幣ETF自發行以來有約85%時間主導價格發現,亦即透過這些監管產品的機構資金流,比現貨交易所對短線價格形成的影響更大。當ETF資金流轉為淨流出,價格發現又回歸到碎片化、以投機主導的現貨市場,其交易行為較少反映資產配置等基本面。這種轉換造成價格信號雜音加大、市場效率下降。

The scarcity premium that Bitcoin commands faces erosion if institutional demand remains weak. Bitcoin's value proposition rests significantly on its status as a scarce, supply-capped asset that institutions increasingly adopt as a strategic reserve or portfolio diversifier. When the most sophisticated market participants signal through their selling

若機構需求持續低迷,比特幣作為稀缺資產而擁有的溢價也將面臨侵蝕。比特幣的價值主張很大程度建立在其有限供給以及越來越多機構將其列為戰略儲備或多元化投資組合的一部分。當最具專業度的市場參與者,透過賣出行為發出警訊時...that they no longer find Bitcoin attractive at current valuations, it challenges the narrative that scarcity alone justifies premium pricing. This psychological shift can prove more damaging than immediate price weakness, as it undermines the fundamental thesis driving long-term investment.

當他們在目前的估值下不再覺得比特幣具有吸引力時,這就對「單靠稀缺性就能支撐溢價價格」的說法造成挑戰。這種心理層面的轉變,甚至可能比價格短期下跌更具破壞性,因為它動搖了長期投資背後的核心論述。

Corporate treasury companies face acute risks if institutional demand remains subdued and Bitcoin prices fail to advance. As documented earlier, these companies accumulated significant debt loads while building Bitcoin positions, creating fixed obligations that must be serviced regardless of market conditions. If Bitcoin consolidates or declines while institutional demand remains weak, treasury companies lose their ability to issue equity at premiums to NAV, blocking their primary capital-raising mechanism. This scenario could force distressed selling from overleveraged entities, adding to downward price pressure precisely when markets can least absorb it.

企業財務公司若在機構需求持續低迷、比特幣價格無法走高的情況下,將面臨嚴峻風險。如先前所述,這些公司在建立比特幣持倉時累積了大量債務,產生了不論市況如何都必須履行的固定責任。如果比特幣價格盤整甚至下跌,同時機構需求又疲弱,這些財務公司就會喪失以高於淨資產價值(NAV)發股集資的能力,等同切斷其主要融資管道。如此局面下,槓桿過高的機構可能被迫賤價拋售,加劇價格下行壓力,而這時市場承接力又最為薄弱。

The mining industry confronts similar pressures. With debt loads approaching $13 billion and many firms carrying interest expenses exceeding operating revenues, miners require sustained high Bitcoin prices to remain profitable. If prices decline while operational costs remain elevated, less efficient miners face bankruptcy, potentially reducing network hashrate and security. While Bitcoin's difficulty adjustment mechanism compensates for hashrate changes over time, severe miner distress could create temporary network vulnerability or perception problems that undermine confidence.

礦業同樣面臨壓力。債務規模逼近130億美元,許多礦工的利息支出已超過營業收入,礦業公司必須依靠高檔比特幣價格才能維持獲利能力。如果價格下跌、經營成本又高漲,效率較差的礦工將面臨破產,可能導致全網算力與安全性下降。儘管比特幣的難度調整機制會逐步補償算力變化,但若礦工普遍陷入困境,仍可能造成短暫網路安全隱憂及信心危機。

Distribution channel risks emerge if wealth management platforms and financial advisors become less enthusiastic about Bitcoin ETF allocation following performance disappointments. The institutional adoption story depends partly on Bitcoin ETFs gaining acceptance across major brokerage platforms and wirehouses. While some firms like Morgan Stanley began allowing advisor access, many major platforms including Merrill Lynch, Wells Fargo, and UBS still restrict proactive pitching of cryptocurrency products. Extended underperformance or continued outflows could delay or reverse progress toward broader platform acceptance, limiting the potential addressable market for ETF products.

如果理財平台與財務顧問在比特幣ETF表現不佳後,對配置的熱忱降低,將帶來分銷通路風險。機構參與的故事有賴比特幣ETF被主要券商平台和財富管理公司廣泛接受。雖然部分業者如摩根士丹利已開放顧問接觸,但美林、富國銀行與瑞銀等多家大型平台至今仍限制主動推廣加密貨幣產品。若表現持續落後、資金外流不止,可能拖延甚至扭轉ETF產品擴大市場的進展,進一步壓縮可觸及的潛在市場。

Regulatory risks intensify during periods of market stress. Policymakers and regulators often respond to volatility and consumer losses by implementing restrictions or additional oversight. While spot Bitcoin ETF approval represented regulatory progress, sustained market weakness accompanied by retail investor losses could trigger renewed skepticism about cryptocurrency products' appropriateness for mainstream portfolios. This risk becomes particularly acute if leveraged products or complex derivatives contribute to market dislocations that generate negative headlines.

市場動盪時,監管風險也會升高。決策者及監管機構常透過加強監理或施加限制來回應市場波動與消費者損失。雖現貨比特幣ETF核准象徵監管進展,若市場持續疲弱、散戶損失擴大,將引發外界對加密貨幣產品適不適合主流資產組合的再度質疑。特別是如果槓桿型商品或複雜衍生品加劇市場失靈並引發負面新聞,這項風險會更趨嚴重。

However, not all consequences of reduced institutional demand portend disaster. Market consolidation following rapid appreciation serves healthy functions in price discovery and shakeout of weak holders. Bitcoin has repeatedly demonstrated resilience through drawdowns of 30%, 50%, or even 70% before resuming uptrends and surpassing prior peaks. The current situation may represent normal volatility within an ongoing bull market rather than a fundamental regime change.

但機構需求減弱的後果並非全是災難性的。經過快速上漲後的市場整理,對價格發現及淘汰弱手反而有正面功能。比特幣過去多次經歷30%、50%甚至70%的跌幅,最終總能恢復多頭並創新高。目前的情勢,很可能只是牛市中的正常波動,而非基本格局的逆轉。

The compression of corporate treasury NAV premiums, while painful for equity holders, creates a cleaner foundation for sustainable growth. Companies now trading near NAV offer direct Bitcoin exposure without paying premiums for questionable added value. This reset separates disciplined operators from promotional entities, potentially strengthening the sector long-term even if near-term pain persists.

企業財務公司NAV溢價被壓縮,對持股人固然難受,但卻有助建立更健全的長期成長基礎。如今股價接近NAV的公司,投資人無須為可疑的附加價值支付溢價,便可獲得比特幣曝險。這輪調整有助於優質經營者與炒作派公司分道揚鑣,即便短期痛苦,長線對產業反而有益。

The ultimate consequence of sustained institutional demand weakness depends on whether alternative buyer groups emerge to fill the gap. Retail investors, sovereign entities exploring Bitcoin reserves, continued accumulation by existing believers, or renewed institutional interest following consolidation could all provide demand support. The coming months will reveal whether the late 2025 institutional retreat represents a worrying exodus or merely a pause before the next wave of adoption.

長期機構需求若持續疲弱,最終影響取決於是否有其他買方出現彌補落差。不論是散戶、考慮儲備比特幣的主權機構、現有信仰者的持續買進,或是整理過後機構回籠,都可能補足需求。接下來幾個月,市場將看清2025年末機構退場究竟是令人擔憂的出逃潮,還是下一波採用浪潮到來前的暫時歇息。

Forward Outlook: What Needs to Happen for Demand to Catch Up

展望未來:需求要追上供給,還需要哪些條件?

Reversing the current dynamic where institutional demand lags Bitcoin's mining supply requires analyzing the catalysts that could restore or accelerate ETF inflows and corporate treasury accumulation. Several potential developments could shift the supply-demand balance back toward demand dominance, though their likelihood and timing remain uncertain.

要扭轉目前機構需求落後於比特幣產量的局面,必須探討哪些催化劑能恢復或加速ETF資金流入、企業財務部位擴增。有幾項可能的發展方向有機會讓需求再度領先供給,但發生的機率與時機點尚不明朗。

Macroeconomic conditions represent the most powerful potential catalyst. A clear Federal Reserve pivot toward sustained monetary easing would reduce the opportunity cost of holding non-yielding Bitcoin and improve risk appetite across institutional portfolios. If inflation pressures moderate while economic growth remains resilient, creating a "Goldilocks" environment for risk assets, institutional allocators would likely increase cryptocurrency exposure. Rate cuts combined with ending quantitative tightening could inject new liquidity into markets that historically flows partly into Bitcoin and cryptocurrency markets.

總體經濟情勢是最有力的潛在催化劑。如果聯準會明確轉向長期貨幣寬鬆,無息資產如比特幣的持有機會成本將降低,機構資產組合的風險偏好也會提升。如通膨壓力減緩、經濟仍具韌性,形塑出「金髮女孩」型的風險資產環境,機構配置加密貨幣的意願將大增。降息並結束縮表可為市場輸入新流動性,其歷來部分資金都會進入比特幣及加密貨幣市場。

Regulatory clarity could unlock substantial pent-up institutional demand currently sidelined by compliance constraints. Comprehensive cryptocurrency legislation establishing clear classification frameworks, custody standards, and regulatory oversight would remove a major impediment to institutional participation. While spot Bitcoin ETF approval represented significant progress, many potential allocators await more definitive guidance before committing substantial capital. If Congress passes comprehensive crypto legislation or regulators issue clear guidance, it could trigger a wave of previously restricted institutional buying.

監管明確化也有機會釋放因合規考量而被冷凍的大量機構需求。若有定義清楚的加密貨幣法律、託管標準與監督機制,機構參與最大的障礙便會消除。現貨比特幣ETF獲准雖是重大突破,但不少潛在投資人仍在等更明確的官方指引後才會投入大量資本。美國國會若立法、監管機構也發布明確規範,將有望引發新一波原本受限資金的機構進場。

Geographic diversification of Bitcoin ETF offerings could expand the addressable market significantly. U.S. ETFs currently dominate flows, but similar products in major markets like Europe, Asia, and emerging economies could tap new institutional capital pools. Some jurisdictions already offer cryptocurrency ETPs, but expanded product availability in major financial centers would broaden access. If sovereign wealth funds, pension systems, or insurance companies in additional jurisdictions gain regulatory clearance for Bitcoin exposure, it would diversify and potentially expand demand beyond current U.S.-dominated flows.

比特幣ETF的地理多元化將大幅拓展市場容量。目前美國ETF主導資金流向,但若歐洲、亞洲或新興市場出現類似產品,有望觸及新一層的機構資本。目前部分地區已有加密貨幣ETP,但若大型金融中心的相關商品進一步擴大,也能擴增可接觸對象。若其他國家的主權財富基金、退休基金或保險公司取得比特幣配置的監管許可,則需求將超越當前美國主導的格局,產生更多元化與擴張性。

Product innovation within the ETF structure could attract different investor segments. The launch of options on Bitcoin ETFs, enhanced yield products, or actively managed cryptocurrency strategies might appeal to institutional participants seeking more nuanced exposure than simple spot holdings. If major ETF sponsors introduce products targeting specific use cases - income generation, downside protection, tactical trading - they could capture demand from allocators who find pure spot exposure unattractive.

ETF結構中的產品創新也能吸引不同型態的投資人。例如推出比特幣ETF選擇權、加強收益型產品、或主動管理型加密資產策略,這些都可滿足機構對更細緻曝險的偏好。如果大型ETF業者針對「收益」、「下檔保護」、「策略交易」等特定用途開發產品,就能滿足不愛單純現貨曝險的資金,吸收更多活水。

Corporate adoption beyond treasury companies could provide incremental demand. If major corporations outside the crypto industry begin allocating meaningful portions of cash reserves to Bitcoin, as Strategy pioneered, it would signal broader acceptance and potentially trigger competitive adoption. The model works best when companies can issue equity at premiums to NAV, so renewed market enthusiasm would likely accompany any expansion of this trend. Sovereign adoption would prove even more significant - if nations establish Bitcoin reserves beyond El Salvador and the Central African Republic, the supply impact could prove substantial given the scale of potential allocations.

企業界(不僅限於企業財務公司)採用比特幣也可帶來增量需求。若有主流產業公司(如Strategy率先示範)將現金儲備的一部分分配到比特幣,這將象徵業界接受度提升,甚至引發同業競相跟進。這種模式在公司仍能以高於NAV發股集資時效果最好,因此行情回溫將有助趨勢擴大。若主權國家超越薩爾瓦多與中非共和國,建立比特幣儲備,規模化的配置將對供給面產生巨大衝擊。

Improved miner economics could paradoxically help by reducing selling pressure. If Bitcoin miners successfully transition to sustainable business models incorporating AI and HPC revenue alongside mining, their dependence on selling newly mined Bitcoin would decrease. This transition would effectively remove some daily supply from markets even without increased demand, tightening the supply-demand balance. The success of this pivot remains uncertain given the massive debt loads miners accumulated, but positive developments would improve market structure.

礦工經營情況改善,也可能以減少拋售壓力的方式帶來正面循環。若比特幣礦業能成功轉型,發展AI與高效運算等新收益來源,對於新挖比特幣的拋售依賴就會下降。即使需求不變,這樣也等於市場上日供給量減少,供需平衡將收緊。由於礦工債務負擔龐大,此路徑是否成功仍待觀察,但若態勢轉佳,市場結構將受益。

Technical factors could catalyze renewed buying if Bitcoin establishes clear support at current levels. Traders and algorithms watching for reversal signals might initiate buying if Bitcoin successfully tests and holds $105,000-$110,000 support multiple times, creating a basing pattern that technical analysts interpret as accumulation. Momentum-following strategies that sold on breakdown below key levels would reverse to buying if Bitcoin reclaims important technical thresholds, potentially creating self-reinforcing upward momentum.

技術面因素也可能成為新一輪買盤催化劑。如果比特幣在現有價位多次成功守住$105,000~$110,000支撐,形成技術派認定的築底型態,則追蹤買盤及程式交易將可能進場。習慣動能交易的策略,過去跌破關鍵價位時賣出,若比特幣重回重要技術水位,這類策略也將反手買進,引發自我強化的上漲動能。

Scenario analysis helps frame possible outcomes over coming months. In a base case scenario, institutional demand remains roughly flat at current subdued levels, matching or slightly trailing mining supply. Bitcoin consolidates in a range between $95,000 and $115,000, with neither sustained uptrend nor significant breakdown. This outcome would require macro conditions remaining stable without dramatic improvement or deterioration, regulatory status quo continuing, and no major catalysts emerging to shift sentiment dramatically.

情境分析有助預先估量未來幾個月的各種可能結果。若以基準情境觀察,機構需求大致持平、略遜於新產出,則比特幣將在$95,000至$115,000區間橫向整理,既無明顯多頭延伸,也尚無重大崩跌。要出現這種走勢,前提是總體環境維持穩定、監管現狀不變,且未有重大催化劑劇烈改變市場情緒。

An optimistic scenario envisions renewed institutional interest driven by improving macro conditions, positive regulatory developments, or successful technical basing. ETF inflows resume at levels exceeding mining supply, perhaps reaching 2-3 times daily

樂觀情境下,若宏觀環境改善、監管利多或者技術面順利築底,機構資金將重新大舉進場。此時ETF的資金流入量將再度超過新生成的比特幣,甚至可能達到每日供應量的2到3倍。production as occurred in May 2025. Bitcoin breaks above $125,000 resistance and extends to new all-time highs in the $140,000-$160,000 range by mid-2026. This outcome would restore the favorable supply-demand dynamics that powered 2024-2025's rally and validate the bullish adoption narrative.

如2025年5月生產週期所示。比特幣突破$125,000阻力位,並在2026年年中升至$140,000-$160,000創下歷史新高。這種情境將恢復推動2024-2025年牛市的有利供需動能,並驗證積極的採用故事。

A pessimistic scenario sees institutional outflows accelerating rather than reversing, potentially driven by macroeconomic deterioration, regulatory setbacks, or systematic failures among corporate treasury companies. Demand falls to 50-75% of daily mining supply, forcing Bitcoin to clear excess supply through price declines. The cryptocurrency tests $80,000-$90,000 support, potentially breaking below these levels if selling pressure intensifies. This outcome would require significant negative catalysts - recession, hawkish Fed pivot, major regulatory crackdown, or cascading treasury company failures.

悲觀情境則是機構資金流出加速而非逆轉,可能因為宏觀經濟惡化、監管受挫,或企業金庫公司系統性失敗所推動。需求下降至每日挖礦供應的50-75%,迫使比特幣以價格下跌來消化過剩供應。加密貨幣測試$80,000-$90,000支撐位,若賣壓加劇甚至可能跌破此區間。這種情境需出現重大負面催化劑——如經濟衰退、聯準會鷹派轉向、重大監管打擊,或金庫公司連環倒閉。

Probabilities for these scenarios remain inherently uncertain and depend on developments across multiple dimensions. Market participants should monitor several key indicators to assess which scenario is materializing:

這些情境的機率本質上仍不確定,並依賴多面向的發展。市場參與者應關注幾項關鍵指標,以評估哪一種情境正在成形:

ETF flow data provides the most direct real-time signal of institutional demand. Daily and weekly flow reports reveal whether the late October selling represented a temporary adjustment or marks the beginning of sustained institutional exodus. If flows stabilize near neutral or return to modest inflows, it suggests consolidation rather than breakdown. If outflows accelerate or persist for multiple consecutive weeks, pessimistic scenarios gain credibility.

ETF資金流數據 提供機構需求最直接的即時信號。每日及每週流量報告可揭示十月底拋售是暫時調整,或是持續機構撤出開端。若資金流穩定在接近中性或恢復小幅淨流入,意味著市場處於盤整而非崩盤。若資金淨流出加速或連續多週維持,悲觀情境則更具說服力。

On-chain metrics reveal whether long-term holders remain committed or begin distributing. The percentage of Bitcoin supply unmoved for 6+ months, currently around 75%, indicates conviction among existing holders. If this metric declines substantially, suggesting long-term holders selling, it would signal weakening fundamental support. Exchange reserves and the pattern of transfers to or from exchanges provide insight into whether holders prepare to sell or continue accumulating for long-term storage.

鏈上數據指標 可反映長期持有者是否仍然堅守或開始分批賣出。未動過6個月以上的比特幣供應占比,目前約為75%,顯示現有持有者的信心。若這項指標大幅下滑,意即長期持有者賣出,則顯示基本面支撐轉弱。交易所儲備及其轉進或轉出模式,也有助判斷持有者是在準備賣出還是繼續長期囤積。

Corporate treasury behavior indicates whether the digital asset treasury model retains viability. If treasury companies resume Bitcoin purchases following NAV compression, it suggests the model adapts and survives. If purchases remain frozen or companies begin selling holdings to service debt, it indicates structural problems that could force liquidations.

企業金庫行為 表明數位資產金庫模式是否仍具活力。若金庫公司在NAV(淨值)壓縮後恢復購買比特幣,代表該模式可調適並存活。若購買行為持續凍結或公司開始出售持幣支付債務,則反映結構性問題,可能導致被迫清算。

Miner selling pressure reveals whether producers add to or reduce market supply beyond new issuance. Tracking miner wallet balances shows whether newly mined coins immediately reach exchanges or remain in miner treasuries. Increased miner selling would compound institutional demand weakness, while miner holding would partially offset reduced ETF buying.

礦工賣壓 可觀察生產者除了新發行外,是否增添市場供應。追蹤礦工錢包餘額,可知新挖比特幣是否立即進入交易所或留於礦工金庫。若礦工拋售增多,將加深機構需求疲弱的影響;若礦工選擇持有,則可部分抵銷ETF買盤減少的影響。

Macroeconomic conditions and Fed policy remain the dominant external force. Fed communications, inflation data, employment reports, and market pricing of future rate cuts all provide insight into the macro backdrop for risk assets. Improving conditions that boost equity markets typically support Bitcoin, while deteriorating macro environments create headwinds.

宏觀經濟情勢與聯準會政策 仍是最關鍵的外部因素。聯準會政策措辭、通膨數據、就業報告、未來降息機率的市場定價等,皆反映風險資產的總體背景。若環境改善帶動股市上漲,通常也利多比特幣,而宏觀景氣惡化則構成阻力。

Regulatory developments in major jurisdictions could prove decisive. Congressional action on comprehensive crypto legislation, SEC rule-makings, international regulatory coordination, or sovereign adoption announcements all could significantly impact institutional appetite for Bitcoin exposure.

主要司法管轄區的監管進展 可能起決定性作用。國會全面加密法案、SEC新規、國際監管協調,或主權國家採納等,都可能顯著影響機構對比特幣配置的意願。

Investors and market participants face decisions about positioning given this uncertainty. Conservative approaches suggest reducing exposure or maintaining tight stop-losses until demand-supply balance improves. Aggressive strategies might view current prices as opportunities to accumulate, betting that temporary demand weakness will reverse once macro conditions improve. Balanced approaches might maintain positions while hedging downside risk through options or position sizing appropriate to elevated uncertainty.

面對這一不確定性,投資人與市場參與者必須決定如何佈局。保守做法建議減少曝險或設置嚴格停損,等待供需平衡改善。進取策略則把目前價格視為加碼機會,押注需求疲軟只是暫時,一旦宏觀環境改善便會反轉。折衷做法則在持續持倉的同時,以期權或適度控制部位來對沖下行風險。

The central question remains whether Bitcoin's long-term adoption trajectory remains intact despite short-term institutional demand weakness. If Bitcoin represents a legitimate emerging reserve asset and uncorrelated portfolio component, temporary periods where ETF flows disappoint should present buying opportunities rather than reasons for concern. However, if institutional retreat signals that Bitcoin failed to deliver on promises of mainstream financial adoption, current weakness might mark a more significant setback requiring years to overcome.

關鍵問題依舊是,比特幣的長期普及路徑是否會因短期機構需求疲弱而受損。若比特幣真的是一項新興儲備資產及非高度相關的投資組合成分,ETF短暫失靈應被視為買點而非憂慮。然而,若機構撤退顯示比特幣未能實現主流金融採納的承諾,現在的疲弱可能意味著更嚴重的挫折,需數年方能克服。

Historical perspective suggests patience. Bitcoin has weathered numerous periods of declining demand, adverse headlines, and price drawdowns of 50% or more, only to recover and reach new all-time highs. The cryptocurrency's longest-duration bear market lasted roughly 18 months from the 2021 peak to late 2022's bottom, and that period included spectacular failures like Terra/Luna, Three Arrows Capital, Celsius, FTX, and others that current conditions don't approach in severity.

從歷史視角看,耐心為上。比特幣曾多次經歷需求下滑、負面新聞、甚至超過50%的價格腰斬,最終總能復甦並創新高。其最長空頭時期為2021年高點到2022年底谷底,約18個月,期間還有Terra/Luna、三箭資本、Celsius、FTX等慘烈事件,當時情勢遠甚於現今。

The supply-demand framework developed by Rudd and Porter suggests that Bitcoin's fixed supply creates conditions where even modest sustained demand can drive substantial long-term price appreciation. Their modeling indicates that daily withdrawals from liquid supply equivalent to 1,000-4,000 BTC - easily achievable by ETFs during strong periods - could push Bitcoin toward six- or seven-figure prices over 5-10 year horizons if maintained. The challenge is whether institutional demand resumes at levels that enable this trajectory or whether the late 2025 slowdown represents the high-water mark of institutional adoption's first wave.

Rudd和Porter所建立的供需模型指出,比特幣固定供應意味就算僅有小規模持續買盤,也能帶動長線大幅升值。他們的模型顯示,每天從流動供應中撤出的1,000-4,000顆BTC(在強勢ETF周期輕易達成),足以讓比特幣在5-10年內衝上六位數甚至七位數價格,前提是這種需求能持續下去。關鍵挑戰是,機構需求是否能重回足以推動這條軌跡的水準,還是2025年末的放緩其實已是首波機構採納的高峰。

Ultimately, the forward path depends on Bitcoin proving it offers sufficient utility - whether as an inflation hedge, portfolio diversifier, decentralized alternative to traditional finance, or digital store of value - to justify sustained institutional allocation despite volatility and regulatory uncertainty. The coming months will provide crucial data points revealing whether institutional conviction in Bitcoin's value proposition withstands its first significant test since spot ETFs introduced this powerful but volatile new demand channel.

最終,未來的道路將取決於比特幣能否證明其效用充足——無論作為抗通膨工具、投資組合多元化成分、去中心化金融替代方案,還是數位價值儲存方式——使機構得以在波動與監管不確定性下仍堅持配比。未來幾個月將產生關鍵數據,揭示機構對比特幣價值主張的信念能否通過這個現貨ETF推出以來最大的考驗。

Final thoughts

最後思考

Bitcoin's journey through 2025 has tested the fundamental proposition underlying its multi-trillion-dollar valuation: that programmed scarcity, by itself, justifies premium pricing and ongoing institutional adoption. The cryptocurrency's fixed supply schedule represents an elegant and immutable feature of its design, distinguishing Bitcoin from fiat currencies subject to inflationary monetary policies and even from gold whose annual mine supply responds to price incentives. The April 2024 halving reduced new issuance to approximately 450 BTC daily, creating mathematical scarcity that Bitcoin advocates argue must drive long-term value appreciation as adoption grows.

比特幣在2025年的進程嚴格考驗了其數兆美元市值背後的基本論點:單憑編程稀缺,就足以支撐高溢價定價與持續的機構採納。比特幣的固定發行時程是其設計中優雅且不可更改的特徵,讓它與受通膨貨幣政策影響的法定貨幣截然不同,甚至與每年供應會隨價格變動的黃金也有所區隔。2024年4月減半後,比特幣的每日新發行量降至約450顆,帶來數學上的稀缺性,擁護者認為這勢必隨普及度成長而推動長線價值。

Yet the experience of late 2025 demonstrates that scarcity alone provides insufficient support for prices when demand fails to materialize at expected levels. For the first time in seven months, institutional demand through spot Bitcoin ETFs and corporate treasury accumulation fell below the pace of daily mining supply. This crossing point, confirmed on November 3, 2025, represents a potentially significant inflection in Bitcoin's market structure and challenges the complacent assumption that limited supply automatically translates to ever-increasing prices.

然而,2025年下半年的經驗證明,當需求未達預期時,單靠稀缺無法支撐價格。七個月以來首次,現貨比特幣ETF與企業金庫累積帶來的機構需求低於每日挖礦供應速度。這個於2025年11月3日確認的關鍵交叉,可能標誌著比特幣市場結構的重大轉折,也對「供給有限就會自動推高價格」的想法提出警告。

The supply side of Bitcoin's equation has performed exactly as designed. The halving occurred on schedule, cutting issuance with mathematical precision. Miners continue securing the network despite compressed economics, though the massive debt accumulation required to maintain operations introduces concerning fragilities. The protocol's supply schedule extends predictably into the distant future, with each successive halving further reducing new issuance until the final Bitcoin is mined around 2140. This supply reliability stands as one of Bitcoin's core features and differentiators.

比特幣供應端如設計般精準運作。減半如期發生,帶來數學上的精準減發。即便礦工經濟壓縮,他們仍持續維護網路安全,儘管維持營運需承擔巨額負債也造成潛在脆弱性。協議中供給走勢預期可延續至遠未來,每次減半均再進一步減少新發行,最終比特幣將於2140年左右挖完。這種供應穩定性正是比特幣的核心特色與差異化所在。

The demand side has proven far less predictable. The spot Bitcoin ETF launch in January 2024 initially delivered on promises of mainstream institutional access, with billions flowing into these products and absorption rates exceeding mining output by multiples. This dynamic powered Bitcoin's appreciation from the $40,000s to above $126,000, validating the thesis that accessible institutional products would unlock substantial pent-up demand. However, the reversal to net outflows through late October, totaling $1.67 billion since October 11 and culminating in $600 million weekly outflows, demonstrated how quickly institutional sentiment can shift.

但需求端就難以預測得多。2024年1月現貨比特幣ETF的推出,初期實現了對主流機構可介入的承諾,資金湧入數十億美元、吸收能力多倍於挖礦新產出,令比特幣價格自四萬元區間拉升至超過$126,000,驗證了開放機構資產品能釋放巨大遞延需求的論述。然而,十月底以來開始的資金淨流出,累計自10月11日以來$16.7億美元,單週更達$6億美元,顯示機構情緒翻轉的速度之快。

The corporate treasury channel that provided complementary demand also weakened substantially. NAV premiums collapsed across the digital asset treasury sector, blocking the capital-raising mechanism these companies used to acquire Bitcoin. With 188 treasury companies holding substantial positions and many facing significant debt obligations, this demand source may provide limited support until market conditions improve enough to restore equity issuance capabilities.

企業金庫這條補充需求管道也同樣大幅轉弱。數位資產金庫產業的NAV溢價崩潰,導致公司無法透過增資配股來籌措購幣資金。目前有188間金庫企業持有大額部位,不少又背負沉重債務,在市場回暖、再度開放股票融資前,這條需求來源恐難望有力支撐。

The implications for investors and market participants are sobering. Bitcoin's scarcity creates potential for supply shocks and dramatic price appreciation when demand growth meets or exceeds supply growth. However, the inverse scenario - where

這對投資人及市場參與者而言,是個警惕。比特幣的稀缺性確實能在需求增長大於供給增長時,引發供應衝擊和劇烈升值。但反之——demand growth lags or reverses - introduces downside risk that scarcity itself cannot prevent. The academic frameworks that model Bitcoin price trajectories demonstrate this symmetry: fixed supply amplifies both upside from demand growth and downside from demand contraction.

當需求成長趨緩甚至反轉時,會帶來稀缺性本身無法抵禦的下行風險。學術框架在塑造比特幣價格的走勢時展現出這種對稱性:固定供給不僅會放大需求增長帶來的上行空間,也同樣強化需求萎縮時的下行壓力。

Market structure considerations suggest increased importance of monitoring institutional flows. Given that Bitcoin ETFs now dominate price discovery approximately 85% of the time, these products function as the primary transmission mechanism between institutional capital allocation decisions and Bitcoin spot prices. When ETF flows reverse, they directly remove demand from markets while simultaneously signaling deteriorating institutional confidence. This creates both mechanical selling pressure and psychological headwinds that can become self-reinforcing.

市場結構考量顯示,監控機構資金流向的重要性日益提升。由於比特幣 ETF 目前大約有 85% 的時間主導了價格發現過程,這些產品已成為機構資本配置決策與比特幣現貨價格之間的主要傳導機制。當 ETF 資金流轉向淨流出時,不僅直接抽離市場需求,也同時釋放出機構信心下滑的信號。這會產生機械性的賣壓以及心理層面的阻力,而這種狀況往往會自我強化。

The forward trajectory depends on factors largely outside Bitcoin's protocol control. Macroeconomic conditions, particularly Federal Reserve policy and broader risk appetite, influence institutional willingness to allocate to volatile, non-yielding assets. Regulatory developments in major jurisdictions can either unlock new institutional participation or introduce additional barriers. Technological improvements in custody, execution, and product structures may reduce friction and expand addressable markets. None of these factors relate to Bitcoin's fixed supply, yet all profoundly impact demand and thus price.

未來發展的關鍵大多取決於比特幣協定本身無法左右的因素。總體經濟環境,特別是聯準會的政策和市場整體風險偏好,會影響機構是否願意配置高波動且無孳息的資產。主要司法管轄區的監管發展可能為機構參與打開新門戶,或帶來額外阻礙。託管、交易執行和產品結構的技術進步,有助於降低摩擦、擴大潛在市場。這些因素都與比特幣固定供給無關,卻對需求與價格產生深遠影響。

For long-term investors, the current episode reinforces several lessons. First, Bitcoin remains a high-volatility asset whose price can decline substantially even from elevated levels, regardless of supply constraints. Second, institutional adoption through ETFs represents genuine progress for mainstream acceptance but introduces new volatility sources as institutions prove more fickle than ideologically committed retail holders. Third, the interaction between fixed supply and variable demand creates asymmetric outcomes - massive gains during demand surges and significant drawdowns during demand droughts.

對長期投資人而言,這次經驗帶來幾點啟示。首先,比特幣仍然是高波動性的資產,即使價格在高檔,也隨時可能出現巨幅下跌,供給限制並非萬靈丹。第二,ETF 促成的機構參與是主流化的真正進展,但也引入與過去散戶不同的新波動來源——機構對比特幣的持有態度較易變動。第三,固定供給與變動需求的交互作用會帶來非對稱結果——在需求激增時創造巨量利潤,需求枯竭時則伴隨重大虧損。

The thesis supporting long-term Bitcoin investment has not fundamentally changed. The cryptocurrency remains the largest, most secure, and most widely recognized digital asset, with growing infrastructure, improving regulatory clarity, and expanding institutional access. Its supply schedule remains immutable and its scarcity property intact. However, realizing the value that scarcity theoretically creates requires sustained demand growth from institutions, corporations, and individuals who find Bitcoin sufficiently compelling to allocate meaningful capital despite its volatility and uncertainty.

支持長期投資比特幣的基本論點並未根本改變。這種加密貨幣依然是規模最大、最安全、最廣為人知的數位資產,基礎建設持續擴大,監管環境更加明朗,機構進入的門檻也逐步降低。其供給排程不變,稀缺性特徵依舊。不過,僅有稀缺性並不足以自動產生價值——還需要來自機構、企業及個人的持續需求增長,使他們即使在面對波動與不確定性時,仍願意投入可觀資金。

The current supply-demand disconnect may mark an important turning point where the market separates sustainable institutional adoption from speculative excess. If Bitcoin weathers this period of reduced institutional demand and eventually attracts renewed interest at higher price levels, it would strengthen the case for Bitcoin as a maturing asset class finding its place in diversified portfolios. If instead institutional retreat persists or accelerates, it would challenge assumptions about Bitcoin's inevitability and mainstream adoption pace.

目前供需失衡的情形,可能正標誌著市場區分可持續的機構採納與短期投機泡沫的關鍵轉折點。如果比特幣經得起這一波機構需求萎縮,並最終能在更高價位重新吸引興趣,這將有力證明比特幣正逐步成為多元投資組合中的成熟資產類別。反之,如果機構退出的趨勢持續甚至加劇,則會動搖比特幣必然被主流接受的假設與發展速度。

The cryptocurrency has survived numerous crises and bear markets through its 16-year history, repeatedly recovering to surpass prior peaks. Whether 2025's institutional demand weakness represents another cyclical challenge Bitcoin will overcome or a more structural setback remains to be determined. The answer will emerge through the daily flow data, on-chain metrics, and price action of coming months as the market digests the reality that scarcity, while necessary, requires sustained demand to translate into sustained value appreciation. The Bitcoin story continues, but its next chapter will be written by the institutional allocators whose enthusiasm has proven more variable than the fixed supply schedule they once found so compelling.

這種加密貨幣在 16 年歷史中已歷經多次危機與熊市,每次都能反彈突破過去高點。至於 2025 年機構需求低迷究竟是比特幣又一次週期性的挑戰,還是結構性的阻礙,仍有待驗證。最終答案將透過未來幾個月的資金流向、鏈上數據及價格走勢逐步揭曉——市場必須消化「稀缺性雖然重要,但要實現價值增長還需有持續的需求」這一現實。比特幣的故事仍在繼續,而其下一章則取決於這些熱忱遠不如固定供給排程穩定的機構資本配置者們。