穩定幣發行商已悄悄成為美國短期國債的最大持有者之一,截至2025年中,Circle、Tether及其他主要機構共持有超過1,200億美元的國庫券及相關工具。本專題調查深入解析,業界對穩定數位美元的追求如何促成去中心化金融與聯準會貨幣操作之間的直接資金管道。

當Circle公布其2024年7月儲備審證報告時,加密觀察家注意到,三年前還難以置信的情景正真實上演。作為市值第二大的穩定幣USDC幕後公司,Circle宣布其儲備基金規模達286億美元,其中281億美元投資於短期期美國國債和與聯準會的隔夜逆回購協議,剩下5億美元則存放於受監管的金融機構現金存款。

這樣的儲備結構已不再僅僅是審慎管理,更展現出穩定幣產業已質變為美國國債的特殊資金通道,這條管道多數運作於傳統銀行監管體系之外,並由持有穩定幣者幾乎零利息的存款與國債收益率之間的利差,創造上百億美元收入。

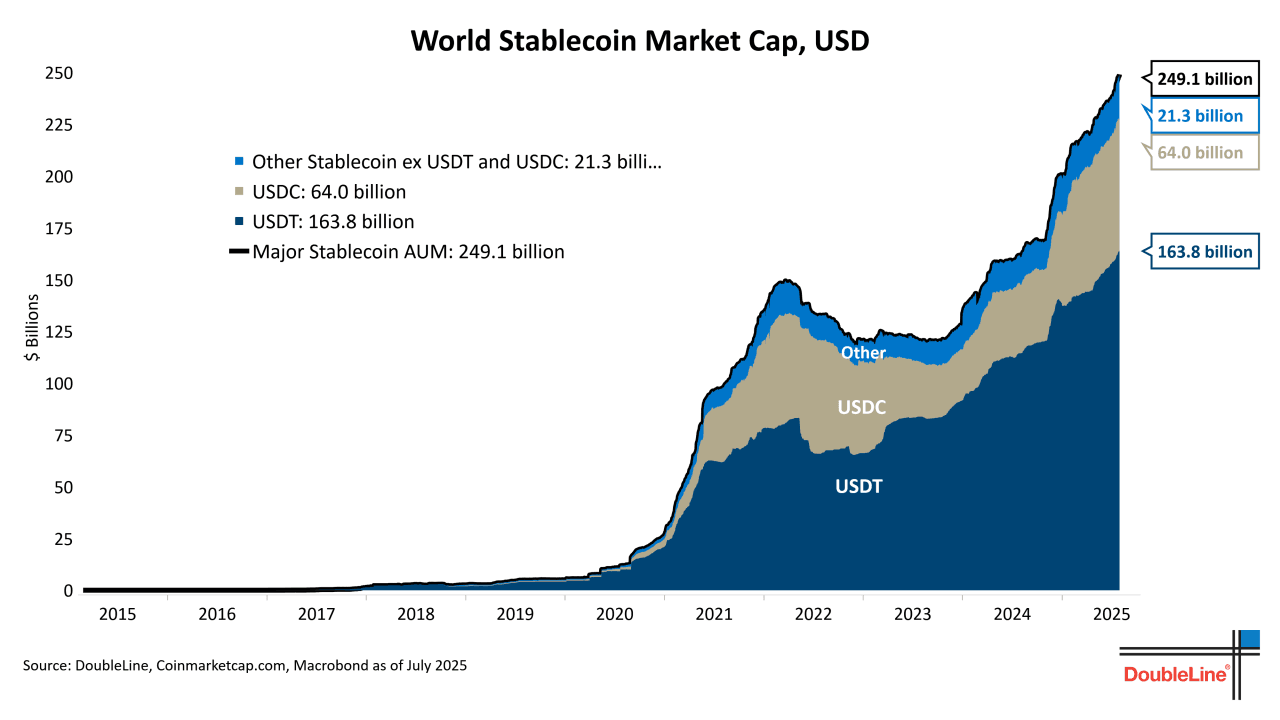

數據頗為驚人。全球市值最大、2024年10月流通量約1,200億美元的USDT發行商Tether,於2024年第2季透明度報告中披露,其儲備中約有84.5%為現金、現金等價物及短期美國國庫券。按此規模,僅Tether本身就已跻身美國國債前二十名持有者,甚至超越許多主權國家所持有的國債規模。

這種模式在整個穩定幣生態中一再上演。Paxos這家受監管信託公司,同時發行USDP並在BUSD停止發行前管理其儲備,早於2021年便將儲備全面轉向國債。即使是追求其他穩定機制的新進者,如Ethena Labs,於2023年底推出合成穩定幣USDe,雖採無方向性衍生品策略,在負資金費率時段仍以國庫券作為部分儲備。

穩定幣儲備集中於國債並非巧合,而是反映一項徹底重塑加密貨幣與傳統金融關係的經濟現實:在實務上,穩定幣已成為無保險的貨幣市場基金,具備即時兌換功能,運行於區塊鏈之上,並依靠資本成本(幾乎為零,因多數穩定幣不支付利息)與短期國債無風險收益率的利差獲利。

其影響早已超越加密領域。2024年上半年穩定幣淨新發行量增長約400億美元(見CoinGecko數據),資金大舉流入國庫券市場,壓縮票據收益率並影響回購市場動態。反之,當加密市場下挫引發大量穩定幣贖回時,發行商不得不拋售數十億美元的國債頭寸,可能加劇貨幣市場波動。穩定幣業已實質介入美國貨幣政策傳導管線,產生的回饋機制如今才開始引起央行關注與研究。

以下將深入探討這場低調的變現化進程、誰最受益、產生何種風險,以及為什麼加密資產基礎設施與政府債券市場的融合,是數位金融領域最具影響性卻被忽略的發展之一。本故事將涉及儲備管理技術、收益模式、代幣化國債產品崛起及監管機制如何追不上跨界創新—金融證券、貨幣及支付系統界線正逐漸模糊。

穩定幣與「儲備」

要理解穩定幣如何成為國債敞口的載體,首先必須釐清什麼是穩定幣、它們如何維持錨定,以及「儲備」在此脈絡下的意義。

基本上,穩定幣是一種旨在將價格錨定某基準資產(最常見為美元)的加密貨幣。不同於比特幣、以太幣這些價格因市場波動而浮動的幣種,穩定幣力求永遠以每枚1美元左右的價格交易。穩定特性讓它們在加密市場中用於交易對、波動時的暫時價值儲存、去中心化金融協議結算機制,甚至日益成為跨境支付工具。

然而,錨定機制決定了穩定幣的風險輪廓與儲備構成。產業歷經三大類模型,每類穩定機制各自有不同的維持方式。

法幣儲備型穩定幣為市場主流並且是本文討論核心。這類穩定幣承諾可1:1兌換美元(或其他法幣),並主張等值儲備存於現金與高度流動性證券。USDC、USDT、USDP等都屬於這一類。

用戶把美元存入發行商(可經授權夥伴),發行商相應鑄造等量代幣。當用戶要求贖回時,歸還代幣即可取回美元。理論上,儲備始終等於或大於未償代幣供應保證每一持有人可以兌換面值。

關鍵問題在於:這些儲備到底是什麼資產?早期穩定幣主要將資金存於銀行現金帳戶,但此模式對發行商經濟效益低落。在接近零利率環境下,現金存款產生的收益微乎其微。維護銀行合作關係需大量運營資源。更重要的是,持有大筆用戶資產而無收益,發行商須承擔全部營運及監管成本。

這種經濟現實推動其資金配置轉向短天期證券。至2021年底,主流法幣穩定幣皆優先將儲備投向隔夜和短期國庫券、逆回購協議及僅以國債為標的的貨幣市場基金。這些工具可在利率攀升時提供顯著收益(2023年3個月期國庫券收益率超過5%),兼具即日或隔日流動性、幾乎沒信用風險(國家擔保),且相較企業債或商業票據監管寬鬆。

發行商每月(有時為每季)發表的審證報告,雖詳盡程度各異,仍提供了儲備構成的窗口。Circle由德勤會計師事務所出具報告,細分國債依存續期、隔夜逆回購、特定銀行現金存放。Tether的審核則由BDO Italia負責,早期資訊較粗略、近年漸趨透明,現在已能看到國庫券、貨幣市場基金及其他資產的比例。

以紐約信託公司身分運作的Paxos,則受更嚴格披露要求,需在每月報告中標示國債精確的CUSIP識別碼。

演算法穩定幣則企圖透過市場機制及激勵系統而非法幣儲備來維持錨定。TerraUSD (UST)於2022年5月脫鉤爆發死亡螺旋、一舉蒸發約400億美元,凸顯此機制巨大風險。

UST透過與姐妹幣LUNA的演算法關聯維持穩定,信心崩解時產生連環清算。這場災難直接促使產業全面轉向超額抵押或法幣儲備模式,也讓監管機構對演算法型穩定幣更趨審慎。

合成或加密資產質押型穩定幣則以加密資產作為抵押,通常需超額抵押。由MakerDAO創建的DAI率先採用此模式:用戶需抵押價值至少150%等值的以太幣等資產,方可鑄造DAI。若抵押價下跌低於門檻,系統會強制清算以維持儲備。近年來此模型更進化融入現實世界資產,MakerDAO將代幣化國債納入DAI的儲備,就顯示即便加密原生模式也開始向國債靠攏。

現今主導市場的法幣儲備型穩定幣,儲備結構直接決定錨定的安全性及商業經濟模式。發行商需… sufficient liquidity to process redemptions quickly (which argues for overnight instruments and cash), but they also want to maximize yield on reserves (which argues for slightly longer-duration securities). This tension has largely been resolved in favor of short-dated Treasury exposure, typically overnight to 3-month maturities, which offers attractive yields while maintaining next-day liquidity.

充足的流動性可讓贖回請求能夠迅速處理(因此傾向於使用隔夜工具和現金),但同時也希望能最大化儲備的收益率(這又傾向於持有久期略長的證券)。這種拉鋸基本上已經由短期美國國債配置取得平衡,通常持有隔夜至三個月到期的美債,在維持隔夜流動性的同時,也能獲得具吸引力的收益。

The attestation process itself deserves scrutiny. These are not full audits in most cases. Attestations involve accountants examining whether the stated reserves exist at a specific point in time, but they typically do not verify the continuous adequacy of reserves, test internal controls, or assess the quality and liquidity of all assets.

保證程序本身值得檢視。在大多數情況下,這些都不是完整的審計。保證僅涉及會計師查核在某一特定時間點聲明的儲備是否存在,但通常並不驗證儲備在整個期間的持續充足、測試內部控制,或評估所有資產的品質與流動性。

Some critics argue this creates gaps in transparency. A company could theoretically optimize its balance sheet just before an attestation date, present favorable numbers, and then adjust positions afterward. However, the trend has been toward more frequent attestations and greater detail, particularly as regulatory pressure increases.

有些批評者認為,這會造成透明度上的缺口。一家公司理論上可以在保證日前優化其資產負債表,呈現有利的數字,之後再調整部位。不過隨著監管壓力增加,保證頻率和內容詳盡程度的趨勢都有所提升。

Understanding this foundation is essential because the shift from cash to Treasuries in stablecoin reserves represents more than a technical portfolio adjustment. It represents the crypto industry's integration into the apparatus of government debt monetization, with all the systemic implications that entails.

了解這個基礎至關重要,因為穩定幣儲備從現金轉向美國國債,不僅僅是技術層面的投資組合調整,它其實代表加密產業正逐步納入政府債務貨幣化機制之中,而這背後也有其系統性影響。

The Mechanics of Yield: How Treasury Exposure Generates Return

收益的運作機制:持有美債如何產生回報

The transformation of stablecoin reserves from cash to Treasury instruments created a straightforward yet highly lucrative business model: capture the spread between the near-zero interest rate paid to stablecoin holders and the risk-free rate on government securities. Understanding exactly how this yield generation works requires examining the specific instruments and market operations that stablecoin issuers employ.

穩定幣儲備從現金轉為美國國債工具,孕育出一種直接卻極具利潤的商業模式:即賺取穩定幣持有人近乎零利息和政府證券無風險利率之間的利差。要精確理解這項收益如何產生,必須檢視穩定幣發行商實際運用的工具和市場操作。

Treasury Bill Purchases represent the most direct approach. A Treasury bill is a short-term debt obligation issued by the U.S. government with maturities ranging from a few days to 52 weeks. Unlike bonds, bills are sold at a discount to their face value and do not pay periodic interest. Instead, investors earn returns through the difference between the purchase price and the par value received at maturity. For example, if a 3-month Treasury bill with a $1,000 face value sells for $987.50, the buyer earns $12.50 in yield over three months, equivalent to approximately 5% annualized.

購買美國國庫券是最直接的方式。國庫券是美國政府發行的短期債務,期限從數天到52週不等。與債券不同的是,國庫券以低於面值的價格發行,且不定期支付利息。而投資人靠購買價格與到期時領回面值的差額獲取報酬。例如,面值1,000美元的三個月國庫券以987.50美元售出,持有人在三個月後賺取12.50美元的收益,年化約為5%。

Stablecoin issuers can purchase Treasury bills directly through primary dealers or on secondary markets. When Circle holds $28 billion in Treasury securities, those positions represent outright purchases of bills across various maturities, typically weighted toward shorter dates to maintain liquidity. The yield on these positions flows directly to Circle's bottom line, since USDC holders receive no interest on their holdings.

穩定幣發行商可以透過一級交易商或二級市場直接購買國庫券。當Circle持有280億美元的美國國債時,這些部位就是直接購入、分布於不同到期日的國庫券,通常偏向短天期以維持流動性。這些部位產生的收益會直接成為Circle的營收,因為USDC持有人並不獲得任何利息。

In a 5% rate environment, $28 billion in Treasury bills generates approximately $1.4 billion in annual gross interest income. After deducting operational costs, regulatory compliance expenses, and redemption-related transactions, the net margin remains substantial. This explains why stablecoin issuance became such an attractive business once interest rates rose from near-zero levels in 2022-2023.

當利率為5%時,280億美元的國庫券每年可產生約14億美元的總利息收入。即便扣除營運成本、合規支出及贖回相關費用,淨利潤仍相當可觀。這也解釋了為何自2022-2023年利率由接近零的水準升起後,發行穩定幣成為如此有吸引力的生意。

Reverse Repurchase Agreements offer an alternative mechanism, particularly for overnight positions. In a reverse repo transaction, the stablecoin issuer effectively lends cash to a counterparty (typically a primary dealer or the Federal Reserve itself) in exchange for Treasury securities as collateral. The transaction includes an agreement to reverse the trade the next day at a slightly higher price, with the price differential representing the interest earned.

逆回購協議則提供另一種途徑,特別適用於隔夜的頭寸。在逆回購交易中,穩定幣發行商等於是將資金借給對手方(通常是一級交易商或聯準會本身),以獲取美國國債作為抵押。這種交易在隔天以較高價格反向結清,價差即為獲得的利息。

The Federal Reserve's overnight reverse repo facility (ON RRP) became particularly important for stablecoin issuers. This facility allows eligible counterparties to deposit cash with the Fed overnight and receive interest at the overnight reverse repo rate, with Treasury securities provided as collateral. While stablecoin issuers cannot access the ON RRP directly (eligibility is limited to banks, government-sponsored enterprises, and money market funds), they can access it indirectly by investing in government money market funds that participate in the facility.

聯準會的隔夜逆回購機制(ON RRP)對穩定幣發行商尤其重要。此機制允許合資格對手方隔夜將資金存入聯準會,以美國國債作為抵押並獲取隔夜逆回購利息。雖然穩定幣發行商無法直接參與ON RRP(僅限銀行、政府機構與貨幣市場基金),但可透過投資有資格參與的政府貨幣市場基金間接參與。

The advantage of reverse repo is perfect liquidity: these are genuinely overnight positions that can be unwound daily to meet redemption demands. The disadvantage is that overnight rates are typically lower than rates on term bills. Issuers therefore maintain a mix, using reverse repo for their liquidity buffer while investing the remainder in term Treasury bills to capture higher yields.

逆回購的優點就是流動性極佳:這是真正的隔夜部位,每日可全數贖回以應付兌付需求。缺點則是隔夜利率通常低於定期國庫券。因此,發行商會混合配置,利用逆回購作為流動性緩衝,其餘資金則投入定期國庫券以獲得較高收益。

Money Market Funds serve as another vehicle for Treasury exposure, particularly Treasury-only government money market funds. These funds invest exclusively in Treasury securities and related repurchase agreements. They offer professional management, diversification across maturities, and typically maintain a stable $1.00 net asset value, making them functionally equivalent to cash for liquidity purposes while generating yield.

貨幣市場基金是另類的國債曝險工具,尤其是專門投資於國庫券的政府型貨幣市場基金。這些基金只投資於美國國債及國債相關回購協議,提供專業管理、部位到期多元化,且通常維持1美元淨值,兼具現金流動性與收益特性。

Circle has explicitly structured part of its reserve holdings through the Circle Reserve Fund, managed by BlackRock. This fund invests exclusively in cash, U.S. Treasury obligations, and repurchase agreements secured by U.S. Treasuries (Circle Reserve Fund documentation). By utilizing an institutional money market fund, Circle gains several advantages: professional portfolio management, economies of scale in transaction costs, automatic diversification across maturities and instruments, and enhanced liquidity management through same-day redemption features.

Circle明確將部分儲備透過Circle儲備基金布局,由貝萊德管理。該基金專門投資於現金、美國國債及由美國國債擔保的回購協議(相關文件亦有載明)。使用機構級貨幣市場基金,Circle 可獲得多項優勢:專業管理、交易規模效益、到期日和工具上的自動分散,以及透過同日贖回功能強化流動性管理。

The mechanics work as follows: Circle deposits a portion of USDC reserves into the Reserve Fund, receives shares valued at $1.00 each, and earns a yield that fluctuates with overnight and short-term Treasury rates. The fund manager handles all securities purchases, maturities, and rollovers. When Circle needs cash for USDC redemptions, it redeems fund shares on a same-day basis, converting them back to cash. This arrangement allows Circle to maintain the liquidity characteristics of a cash deposit while earning Treasury-like yields.

運作流程如下:Circle將部分USDC儲備存入儲備基金,換取每單位面值1美元的基金份額,並獲得隨即期及短天期美債利率而波動的收益。基金經理負責所有證券的買入、到期與再投資運作。Circle有贖回需求時,可於同日贖回基金份額換回現金。這種安排讓Circle同時兼具現金存款的流動性及美債投資的收益。

Tri-Party Repurchase Agreements add another layer of sophistication. In a tri-party repo, a third-party custodian (typically a clearing bank like Bank of New York Mellon or JPMorgan Chase) sits between the cash lender and the securities borrower, handling collateral management, margin calculations, and settlement. This reduces operational burden and counterparty risk for both parties.

三方回購協議則更為進階。在三方回購中,一個第三方託管銀行(通常如紐約梅隆銀行或摩根大通等清算銀行)介於現金出借方和證券借方之間,負責抵押品管理、保證金計算與結算相關業務,降低雙方的營運負擔和對手方風險。

For stablecoin issuers, tri-party repo arrangements allow them to lend cash against high-quality Treasury collateral with daily mark-to-market margining and automated collateral substitution. If a counterparty faces financial stress, the custodian can liquidate the Treasury collateral and return cash to the lender. These arrangements typically offer higher yields than ON RRP while maintaining strong liquidity and safety characteristics.

對穩定幣發行商來說,三方回購機制讓他們以高品質的美國國債作為抵押、每日市價計算保證金且自動替換抵押品的情況下出借資金。倘若對手方出現財務壓力,託管銀行可即時變現國債抵押品並返還現金。這種安排在保持高度流動性及安全性的同時,通常也能提供高於ON RRP的收益。

Securities Lending represents a more advanced strategy that some larger issuers may employ. In a securities lending arrangement, an entity that owns Treasury securities lends them to other market participants (typically broker-dealers or hedge funds seeking to short Treasuries or meet delivery obligations) in exchange for a lending fee. The borrower posts collateral, usually cash or other securities, worth slightly more than the lent securities.

證券借貸則是部分大型發行商可能會採用的進階策略。在證券借貸安排中,持有美國國債的人將國債出借予市場其他參與者(通常是想放空美債或需履行交割義務的券商、對沖基金等),以換取借券費。借方需提供價值略高於所借證券的抵押品,通常是現金或其他證券。

For a stablecoin issuer, this creates a double yield opportunity: earn interest on the Treasury securities themselves, plus earn lending fees by making those securities available to the lending market. However, securities lending introduces additional operational complexity and counterparty risk. If a borrower defaults and the collateral is insufficient to replace the lent securities, the lender faces losses. Most stablecoin issuers have avoided securities lending given the reputational risks and regulatory scrutiny, though it remains theoretically possible.

對穩定幣發行商而言,這創造了雙重收益機會:除了美國國債本身的利息,還能透過借出這些證券收取借券費。不過,證券借貸伴隨較高營運複雜性與對手方風險。如果借方違約且抵押品不足以彌補損失,出借方會蒙受損失。基於聲譽風險與監管審查,大多數穩定幣發行商多未採用此策略,但理論上仍屬可行。

Treasury ETFs and Overnight Vehicles provide additional options for reserve deployment. Short-term Treasury ETFs like SGOV (iShares 0-3 Month Treasury Bond ETF) or BIL (SPDR Bloomberg 1-3 Month T-Bill ETF) offer instant liquidity through exchange trading while maintaining Treasury exposure. An issuer could theoretically hold these ETFs in a brokerage account and sell shares during market hours to meet redemption demands, though most prefer direct Treasury holdings or money market funds due to the potential for ETF prices to trade at small premiums or discounts to net asset value.

美債ETF與隔夜型工具則是儲備運用的其他選項。如SGOV(iShares 0-3個月美債ETF)或BIL(SPDR彭博1-3月期國庫券ETF)等短天期國債ETF,可透過交易所即時變現,又能維持美債曝險。發行商理論上可將這些ETF持於券商帳戶,並於交易時段賣出籌集贖回資金。不過,大多數發行商還是較偏好直接持有國債或貨幣市場基金,因ETF價格有時會相對淨值出現小幅溢價或折價。

The Flow of Funds in practice follows a clear path:

資金流動實務流程如下:

- A user deposits $1 million with an authorized Circle partner or directly with Circle through banking channels

- 用戶透過授權Circle合作夥伴或銀行渠道,存入100萬美元

- Circle mints 1 million USDC tokens and delivers them to the user's wallet

2. Circle鑄造100萬枚USDC並發送到用戶錢包 - Circle receives $1 million in cash in its operating accounts

3. Circle獲得100萬美元現金進入其營運帳戶 - Circle's treasury operations team immediately deploys this cash into the reserve fund: perhaps $100,000 stays in overnight reverse repo for immediate liquidity, while $900,000 purchases Treasury bills maturing in 1-3 months

4. Circle資金管理團隊隨即把現金投入儲備體系:可能有10萬美元留於隔夜逆回購作為即時流動性,90萬美元則購買1至3個月期的國庫券 - Those Treasury positions generate yield - perhaps $45,000 annually at 5% rates

5. 這些美債部位產生收益——在5%利率環境下,年收益約45,000美元 - When the user later wants to redeem, they return 1 million USDC tokens to Circle

6. 當用戶之後要贖回時,把100萬顆USDC還給Circle - Circle destroys (burns) the tokens and returns $1 million to the user

7. Circle燒毀這些USDC代幣,並退還100萬美元給用戶 - To fund this redemption, Circle either uses its cash buffer or sells Treasury bills on secondary markets, receiving same-day or next-day settlement

8. 為了支付此贖回,Circle要嘛動用現金緩衝,要嘛在二級市場出售國庫券,當天或隔天完成結算

The user receives exactly $1 million back - no interest, no fees (beyond any fees charged by intermediaries). Circle keeps the entire $45,000 in interest income generated during the period

用戶取回的正好是100萬美元——沒有利息,沒有額外費用(中間商的費用除外)。Circle則保留該期間產生的全部4.5萬美元利息收入the capital was deployed. This is the fundamental economics of the fiat-backed stablecoin model in a positive interest rate environment.

資本已經部署。這正是法幣支持穩定幣模型在正利率環境下的基本經濟原理。

Yield Striping and Maturity Laddering optimize this process. Stablecoin issuers don't simply dump all reserves into a single Treasury bill maturity. Instead, they construct laddered portfolios with staggered maturities: perhaps 20% in overnight positions, 30% in 1-week to 1-month bills, 30% in 1-3 month bills, and 20% in 3-6 month bills. This laddering ensures that some positions mature weekly, providing regular liquidity without requiring asset sales. It also allows issuers to capture higher yields on the term portion of the curve while maintaining sufficient overnight liquidity.

**殖利率分層(Yield Striping)和到期梯形配置(Maturity Laddering)**最佳化了這個流程。穩定幣發行商並不會把所有儲備都投入同一到期日的美國國債,而是建構不同到期日分散的投資組合:可能 20% 配置於隔夜部位,30% 配置於 1 週至 1 個月期國債,30% 配於 1-3 個月期國債,20% 配於 3-6 個月期國債。這種梯形配置確保每週都有部分部位到期,提供定期流動性,且無需拋售資產。同時,發行商也能在保有足夠隔夜流動性的情況下,捕捉不同期間的較高收益。

The practical result is that major stablecoin issuers have become sophisticated fixed-income portfolio managers, operating treasury desks that would be familiar to any corporate treasurer or money market fund manager. They monitor yield curves, execute rollovers as bills mature, manage settlement timing, maintain relationships with primary dealers, and optimize the tradeoff between yield and liquidity on a continuous basis.

實務上,主要的穩定幣發行商已成為專業的固定收益投資組合經理人,操作著類似企業財務長或貨幣市場基金經理熟悉的資金桌。他們會監控殖利率曲線,隨著國債到期進行資金再配置,管理結算時間,維持與一級交易商的關係,並持續最佳化殖利率與流動性之間的權衡。

This infrastructure represents a profound shift from crypto's early ethos of decentralization and disintermediation. The largest "decentralized" finance protocols now depend on centralized entities operating traditional fixed-income portfolios denominated in U.S. government debt. The returns from this model have proven too compelling to resist.

這種基礎設施代表著與加密貨幣早期去中心化與去中介化精神的重大轉變。最大的「去中心化」金融協議,現在卻仰賴於以美國國債為主、由中心化機構操作的傳統固定收益投資組合。這種模式帶來的回報已經證明誘惑難擋。

Who Earns What: The Economics

誰賺什麼:經濟結構

The revenue model behind Treasury-backed stablecoins is deceptively simple: issuers capture nearly all the yield generated by reserves, while users receive a stable claim on dollars with zero or minimal interest. However, the full economics involve multiple parties extracting value at different points in the chain, and understanding these splits is crucial to grasping the incentive structure driving the sector's growth.

以國債做為儲備的穩定幣其收益模式看起來非常簡單:發行商幾乎捕捉了所有由儲備產生的收益,而用戶則獲得穩定、接近零(或沒有)利息的美元債權。然而,這個完整經濟體系其實涉及多個環節有不同角色抽取價值,了解這些分配對於理解這個產業成長背後的激勵結構至關重要。

Issuer Margins constitute the largest share of economic rent. Consider Circle as a worked example. With approximately $28 billion in USDC reserves deployed predominantly in Treasury securities and reverse repo agreements as of mid-2024, and with short-term rates averaging around 5% in that environment, Circle's gross interest income would approximate $1.4 billion annually. Against this, Circle faces several categories of costs.

發行商利潤構成經濟租(Economic Rent)中最大的一塊。例如 Circle,截至 2024 年中,其 USDC 儲備大約有 280 億美元,主要投入國債與逆回購協議,當時短債利率約為 5%,等於 Circle 的年總利息收入約為 14 億美元。但相對地,Circle 也承擔多種成本。

Operational expenses include technology infrastructure to maintain the blockchain integrations across multiple networks (Ethereum, Solana, Arbitrum, and others), staff costs for engineering and treasury operations, and customer support for authorized partners and large clients. Regulatory and compliance costs have grown substantially, encompassing legal expenses, attestation fees paid to accounting firms, licenses and regulatory registrations in multiple jurisdictions, and ongoing compliance monitoring. Banking relationship costs include fees paid to custodian banks, transaction costs for deposits and redemptions, and account maintenance fees at multiple banking partners to maintain operational resilience.

營運費用包括:維護多條區塊鏈整合的科技基礎設施(如 Ethereum、Solana、Arbitrum 等),工程與財務團隊的人事費用,並為授權夥伴與大型客戶提供客戶支持。合規成本也大幅提高,包括法律支出、會計公司查核費用、多地區的執照與註冊,還有持續的合規監控。銀行關係成本則包括支付給託管銀行的費用、儲值與贖回的交易成本,以及多家銀行賬戶的維護費用以確保營運韌性。

Redemption-related costs occur when users convert USDC back to dollars. While many redemptions can be met from incoming issuance flows, significant net outflows require selling Treasury securities before maturity. This triggers bid-ask spreads in secondary markets and potential mark-to-market losses if interest rates have risen since purchase. During the March 2023 banking crisis when USDC experienced approximately $10 billion in redemptions over several days, Circle had to liquidate substantial Treasury positions, likely incurring millions in trading costs and market impact.

有關贖回的成本則是當用戶把 USDC 換回美元時產生。雖然許多贖回可以藉由新發行來平衡,但若有明顯的資金淨流出,就必須提前賣出國債。這會產生二級市場的買賣差價,以及若利率上升、產生未實現損失的風險。在 2023 三月銀行危機 時,USDC 在幾天內出現約 100 億美元贖回,Circle 被迫拋售大筆國債,疑似因此承受數百萬美元的交易成本與市場衝擊。

Industry analyst estimates suggest that well-run stablecoin issuers operating at scale achieve net profit margins in the range of 70-80% on interest income during elevated rate environments (Messari Research, "The Stablecoin Economics Report," 2024). Applying this to Circle's $1.4 billion in gross interest would imply net profits approaching $1 billion annually - a remarkable return for what is essentially a money market fund with a fixed $1.00 share price that never pays distributions to shareholders.

產業分析師估算,經營良好且具有規模的穩定幣發行商,在高利率環境下,其利息收入的淨利潤率可達 70-80%(參考 Messari Research, "The Stablecoin Economics Report," 2024)。這意味著 Circle 在 14 億美元總利息收入下,每年淨利接近 10 億美元——這對本質上不分紅、價格固定 1 美元的貨幣市場基金來說,是非常驚人的回報。

Tether's economics are even more striking due to its larger scale. With approximately $120 billion in circulation and similar reserve composition, Tether would generate roughly $6 billion in annual gross interest income in a 5% rate environment. Tether has historically disclosed less detailed expense information, but its profit attestations have confirmed extraordinary profitability. In its Q1 2024 attestation, Tether reported $4.5 billion in excess reserves (assets beyond the 1:1 backing requirement) accumulated from years of retained earnings (Tether Transparency Report, Q1 2024). This excess represents years of yield capture flowing to the company's bottom line rather than to token holders.

Tether 的經濟規模更為驚人。其流通量約 1,200 億美元、儲備結構類似,以 5% 利率環境估算,Tether 年度總利息收入約 60 億美元。Tether 一向較少揭露詳細成本資訊,但其盈餘聲明顯示出極高的獲利能力。於 2024 年第一季聲明中,Tether 公布其累計有 45 億美元超額儲備(超過 1:1 支持要求的資產),這些來自多年累積未分配收益(Tether Transparency Report, Q1 2024),這些超額儲備代表這些利息收益都流向公司本身而非代幣持有人。

Returns to Holders are explicitly zero for traditional stablecoins like USDC and USDT. This is a feature, not a bug, of the business model. Issuers have strongly resisted adding native yield to their tokens for several reasons. Paying interest would make stablecoins more obviously securities under U.S. law, triggering full SEC regulation and registration requirements. It would reduce the enormous profit margins that make the business attractive to operators and investors. And it would complicate the use cases; stablecoins function as transaction media and numeraires precisely because their value is stable and simple - adding variable interest rates would introduce complexity.

持有者收益對於像 USDC 與 USDT 這類傳統穩定幣來說就是 0。這並不是缺陷,而是商業模式的設計。發行商堅決拒絕在代幣中添加原生收益有多個原因:給予利息會讓穩定幣依據美國法律更明確地成為有價證券,觸發 SEC 的全面監管和註冊;也會降低這些業者與投資人極高的利潤空間;而且會讓使用情境變複雜——穩定幣正因其價值穩定且簡單得以成為交易媒介與計價單位,若加入浮動利率不利於這個特性。

However, a category of yield-bearing stablecoins has emerged to capture the opportunity issuers were leaving on the table. These tokens either distribute yield generated by reserves to holders or appreciate in value over time relative to dollars. Examples include:

不過,也出現了一類帶收益的穩定幣,試圖抓住被發行商「讓出」的這塊機會。這些代幣要麼將儲備產生的收益分配給持有者,要麼對照美元逐步增值。例子包括:

sUSDe (Ethena's staked USDe) distributes yield from Ethena's Delta-neutral perpetual futures strategy and Treasury holdings to stakers, with annual percentage yields that have ranged from 8-27% depending on funding rates and Treasury exposures.

**sUSDe(Ethena 的質押版 USDe)**將 Ethena 的無方向期貨策略與國債持倉產生的收益分配給質押者,年化收益率依據資金利率與國債配置,曾落在 8%-27% 之間。

sFRAX (Frax's staked version) accumulates yield from Frax Protocol's automated market operations and RWA holdings.

**sFRAX(Frax 的質押版)**累積自 Frax 協議自動化市場操作與現實世界資產(RWA)頭寸產生的收益。

Mountain Protocol's USDM passes through Treasury yields to holders after fees, effectively operating as a tokenized Treasury money market fund with explicit yield distribution.

Mountain Protocol 的 USDM則扣除費用後將國債收益直接分配給持有者,本質上就是具明確收益分配的代幣化國債貨幣市場基金。

The economics of these yield-bearing variants differ fundamentally. By distributing yield, they sacrifice the issuer's ability to capture the full spread, but they gain competitive advantages in attracting capital and DeFi integrations. Whether yield-bearing stablecoins can achieve the scale of zero-yield alternatives remains an open question, but their existence demonstrates market demand for returns on dollar-denominated crypto holdings.

這些帶收益穩定幣的經濟結構與傳統型有根本差異。透過發放收益,他們犧牲了發行商獨佔全部價差的能力,但可以在吸引資本與 DeFi 整合上獲得競爭優勢。帶收益的穩定幣能否長遠達到零收益版本的市佔,目前仍是未知數,但這類產品的存在明顯反映出市場對美元計價加密資產投資報酬的需求。

Custodian and Banking Fees extract another layer of value. Stablecoin issuers must maintain relationships with qualified custodians - typically large banks with trust charters or specialized digital asset custodians regulated as trust companies. These custodians charge fees for holding assets, processing transactions, providing attestation support, and maintaining segregated accounts.

託管與銀行費用則是另一個價值抽取層。穩定幣發行商必須與合格託管機構保持合作——通常是具有信託執照的大型銀行,或是有受監管數位資產信託公司。這些託管機構會因保管資產、處理交易、查核以及維護獨立賬戶等服務收取費用。

Custodian fee structures vary but typically include basis point fees on assets under custody (perhaps 2-5 basis points annually on Treasury holdings), per-transaction fees for deposits and withdrawals, and monthly account maintenance fees. For a $28 billion reserve portfolio, even modest 3 basis point fees amount to $8.4 million annually. These costs are material in absolute terms though small relative to the issuer's yield capture.

託管費結構視情況而異,但通常會針對託管資產每年收取 2-5 個基點(bps)的費用,以及每筆存取款交易的手續費與月度賬戶維護費。以 280 億美元儲備組合、僅以 3 個基點計算,每年光這筆費用就達 840 萬美元。雖然相對發行商的全體利差不高,但在絕對金額上仍相當可觀。

Banking partners also charge fees for operating the fiat on-ramps and off-ramps. When a user deposits dollars to mint stablecoins, that transaction typically flows through a bank account, triggering wire fees or ACH costs. Redemptions trigger similar charges. For retail users, intermediaries may charge additional spreads or fees beyond what the issuer charges.

銀行合作方同樣會針對法幣進出收取費用。當用戶存入美元鑄造穩定幣時,通常需要經銀行賬戶,這會產生電匯或 ACH 手續費;贖回時同理。對一般零售用戶還可能被中介增加額外價差或手續費。

Market Maker Profits emerge in the secondary market for stablecoins. While stablecoins theoretically trade at $1.00, actual trading prices fluctuate based on supply and demand across decentralized exchanges. Market makers profit from these spreads by providing liquidity on DEXs and CEXs, buying below $1.00 and selling above, or arbitraging price differences across venues.

做市商利潤則在穩定幣的二級市場出現。雖然理論上穩定幣維持 1 美元,但實際在去中心化或中心化交易所受到供需影響價格有波動。做市商透過在 DEX/CEX 增加流動性、逢低買入(低於 1 美元時)逢高賣出(高於 1 美元時)、或多市場套利來賺取價差。

During periods of stress, these spreads widen significantly. In March 2023 when USDC briefly depegged to $0.87 due to Silicon Valley Bank exposure concerns, sophisticated traders who understood the situation bought USDC at a discount and redeemed directly with Circle at par, earning instant 15% returns (though bearing the risk that Circle might not honor redemptions at par if banking problems worsened). These arbitrage opportunities are self-limiting; they attract capital that pushes prices back toward peg.

在市場壓力大時,交易價差會顯著拉大。例 2023 年 3 月,USDC 因矽谷銀行曝險疑慮短暫脫鉤至 0.87 美元,精明的交易員買進折價 USDC,再用 1:1 向 Circle 贖回美元,立即獲得 15% 短期收益(前提是 Circle 能在銀行危機下仍以面值贖回)。這種套利機會自我修正,因會吸引資本將價格拉回錨定水位。

Protocol and DAO Treasury Revenue accrues to DeFi protocols that integrate stablecoins into their operations. When stablecoins are deposited into lending protocols like Aave or Compound, these protocols earn spreads between borrowing and lending rates. When stablecoins are used to mint other synthetic assets or provide liquidity in automated market makers, fees flow to liquidity providers and protocol treasuries.

協議與 DAO 庫藏收益則累積於將穩定幣整合入其運作流程的 DeFi 協議。當穩定幣存入 Aave、Compound 等借貸協議時,該協議賺取借貸利差;用穩定幣作為鑄造其他合成資產或做市的流動性時,相關手續費會流向流動性提供者和協議庫藏。

Some protocols have begun to recognize that holding large stablecoin reserves in their treasuries means forgoing substantial yield. This has driven interest in tokenized Treasury products that allow DAOs to earn yield on dollar-denominated holdings while maintaining on-chain composability. MakerDAO's move to integrate over $1 billion in tokenized Treasury

部分協議已開始意識到,把大量穩定幣庫存在自己金庫中,代表放棄了龐大利息收益。這推動了可讓 DAO 在維持鏈上可組合性的同時,為美元計價庫存賺取收益的代幣化國債產品興起。MakerDAO 整合超過 10 億美元代幣化國債的舉動……exposure into DAI's backing represents one manifestation of this trend (Spark Protocol documentation, 2024).

DAI 支持資產的曝險是此趨勢的一種體現(Spark Protocol documentation, 2024)。

Investor Returns flow to the venture capital and equity investors backing stablecoin issuers. Circle raised over $1 billion from investors including Fidelity, BlackRock, and others before filing for a public offering. These investors will realize returns through eventual liquidity events, with valuations based on the recurring revenue streams from reserve management. At a 70% net margin on $1.4 billion in annual revenue, Circle's stablecoin operations could generate $1 billion in annual net income, potentially supporting a multi-billion dollar valuation.

投資人報酬主要流向支持穩定幣發行商的創投和股權投資人。Circle 在申請公開上市前,已從富達(Fidelity)、貝萊德(BlackRock)等投資人籌集超過 10 億美元。這些投資人將透過未來的流動性事件實現獲利,其估值主要來自儲備管理所產生的經常性營收。以 70% 淨利率以及年度 14 億美元收入計算,Circle 的穩定幣業務每年可產生 10 億美元淨利,足以支持數十億美元的公司估值。

The overall economics reveal a highly concentrated value capture model. The issuer retains the vast majority of economic surplus (perhaps 70-80% of gross yield), custodians and market makers capture small percentages, and the end users who deposit the capital receive nothing beyond the utility of holding stable dollars on blockchain rails. This distribution may prove unstable over time as competition increases and users demand yield, but in the current market structure, it remains remarkably persistent.

整體經濟模式顯示,價值捕捉極為集中。發行方保留了絕大多數經濟剩餘(約 70-80% 的總收益),託管方與做市商僅分得極小比例,而最終存入資本的用戶除了在區塊鏈上持有穩定美元的效用外,並未獲得其他收益。隨著競爭加劇及用戶對收益的需求提升,這種分配結構未來可能變得不穩定,但在現有市場架構下,這種現象仍相當持久。

What makes this model particularly attractive is its scalability and capital efficiency. Once the infrastructure is built, incremental USDC or USDT issuance requires minimal additional cost but generates linear increases in interest income. A stablecoin issuer at $50 billion scale has few advantages in treasury management over one at $150 billion scale, suggesting that competition will concentrate around a handful of dominant players who can leverage their scale advantages in regulatory compliance, banking relationships, and network effects.

此一模式特別具有吸引力的原因,在於其可擴展性與資本效率。一旦基礎設施建置完畢,新增 USDC 或 USDT 發行的邊際成本極低,但利息收入卻隨發行量線性增加。發行規模達 500 億美元的穩定幣發行商,在資產管理方面和 1,500 億美元規模的業者相比優勢有限,這意味著競爭將集中於極少數能運用規模優勢於法規遵循、銀行關係及網路效應的領導業者。

The consequence is an industry structure that resembles money market funds but with dramatically different economics. Traditional money market funds operate on extremely thin margins, competing for assets by maximizing yields passed to investors. Stablecoin issuers capture orders of magnitude more profit per dollar of assets because they do not compete on yield. This dislocation cannot persist indefinitely as the market matures, but for now, it represents one of the most profitable business models in finance.

其結果,是產業結構類似貨幣市場基金,但經濟模型迥異。傳統貨幣市場基金薄利經營,主要靠提升投資人收益來爭取資產規模;穩定幣發行商則因不必在收益上競爭,每美元資產能捕捉遠高於傳統基金的利潤。長遠來看,隨產業成熟,這種脫鉤現象難以持續,但目前來說,這是金融領域最賺錢的商業模式之一。

On-Chain and Off-Chain Convergence: Tokenized T-Bills, RWAs, and DeFi

鏈上與鏈下的融合:國庫券代幣化、RWA 與 DeFi

The evolution of stablecoins from pure cash reserves to Treasury-backed instruments represents the first phase of crypto's integration with government debt markets. The emergence of tokenized Treasury products and real-world asset (RWA) protocols represents the second phase - one that promises to deepen these linkages while creating new forms of composability and systemic connectivity.

穩定幣從純現金儲備發展到國庫券支持,標誌著加密貨幣與政府債券市場整合的第一階段。隨著國庫券代幣化產品及真實世界資產(RWA)協議的出現,這是整合的第二階段—不僅深化這些連結,也創造出新的可組合性與系統連通性形式。

Tokenized Treasury Bills bring U.S. government debt directly onto blockchain networks, creating native crypto assets that represent ownership of specific Treasury securities. Unlike stablecoins, which aggregate reserves and promise redemption at par, tokenized Treasuries represent direct fractional ownership of underlying securities, similar to how securities are held in brokerage accounts.

國庫券代幣化將美國國債直接帶到區塊鏈網絡上,產生代表特定國庫券所有權的原生加密資產。它不同於穩定幣(僅將資產集合並承諾按面值兌換),而是讓持有者擁有底層證券的部分直接所有權,類似於在券商帳戶下的持有方式。

Several models have emerged for Treasury tokenization. The first approach involves custodial wrappers where a regulated entity purchases Treasury bills, holds them in custody, and issues blockchain tokens representing beneficial ownership. Examples include:

國庫券代幣化出現了數種模式。第一種是託管包裝形式,由受監管實體購買國庫券,託管後再發行代表受益權的區塊鏈代幣。範例如下:

Franklin Templeton's BENJI (launched on Stellar and Polygon) allows investors to purchase tokens representing shares in the Franklin OnChain U.S. Government Money Fund. Each token represents a proportional claim on a portfolio of Treasury securities and government repo agreements, with the fund operating under traditional money market fund regulations but with blockchain-based share registration and transfer capabilities.

Franklin Templeton 的 BENJI(部署於 Stellar 與 Polygon)允許投資人購買代表 Franklin OnChain 美國政府貨幣市場基金股份的代幣。每單位代幣對應一籃國庫券與政府回購協議的比例所有權,該基金受傳統貨幣市場基金規範管理,但股份登記和轉讓皆可在區塊鏈上進行。

Ondo Finance's OUSG provides exposure to short-term Treasury securities through a tokenized fund structure. Ondo partners with traditional fund administrators and custodians to hold the underlying securities while issuing ERC-20 tokens on Ethereum that represent fund shares. The fund pursues a short-duration Treasury strategy similar to money market funds, allowing holders to earn Treasury-like yields with the convenience of on-chain holdings.

Ondo Finance 的 OUSG通過代幣化基金架構,讓投資人可參與短期美國國庫券。Ondo 與傳統基金管理人和託管方合作,持有底層證券,並於 Ethereum 上發行 ERC-20 代幣代表基金股份。該基金致力於短天期國債策略,讓持有人能在鏈上便利的同時獲得國債類收益。

Backed Finance's bIB01 tokenizes a BlackRock Treasury ETF, creating a synthetic representation that tracks short-duration Treasury exposure. By wrapping existing ETF shares rather than directly holding securities, this approach reduces regulatory complexity while providing crypto-native access to government debt yields.

Backed Finance 的 bIB01將貝萊德國庫券 ETF 代幣化,製造出追蹤短天期國庫券敞口的合成資產。這種將現有 ETF 股票包裹成代幣,而非直接持有證券本身的方法,能降低監管複雜度,並為加密原生投資人提供國債收益選擇。

MatrixDock's STBT (Short-Term Treasury Bill Token) represents direct ownership of Treasury bills held by regulated custodians. Investors can purchase STBT tokens using stablecoins or fiat, and the tokens accrue value based on the underlying Treasury yields. This model aims to provide something closer to direct securities ownership rather than fund shares.

**MatrixDock 的 STBT (短期國庫券代幣)**代表由受監管託管方持有的國庫券直接所有權。投資人可用穩定幣或法幣購買 STBT 代幣,該代幣根據底層國庫券收益自動增值。此模式目標是讓持有人更接近於直接持有國庫券,而非僅僅擁有基金股份。

The technical mechanics involve several layers. At the base sits the actual Treasury security, purchased and held by a regulated custodian or fund manager. A smart contract layer mints tokens representing ownership interests in these securities. Transfer restrictions and KYC/AML checks are typically implemented either through permissioned blockchains, token whitelisting, or on-chain identity verification protocols. Value accrual mechanisms vary; some tokens increase in value over time (like Treasury bills themselves), while others pay periodic distributions to holders.

技術上,這些產品結構多層設計。基礎層是受監管託管方或基金經理購買且持有的國庫券。智能合約層則負責鑄造代表所有權的代幣。通常會透過許可制區塊鏈、代幣白名單或鏈上身份驗證,來實施轉帳限制及 KYC/AML 審查。價值累積方面,有些代幣隨時間自動增值(類似國庫券本身),有些則定期發放收益給持有人。

The legal structures also vary significantly. Some tokenized products operate as registered investment funds under traditional securities law, others as private placement offerings limited to accredited investors, and still others as regulated trust products where tokens represent beneficial interests. This legal diversity creates challenges for DeFi integration and cross-border use, since different structures face different restrictions on transferability and eligible holders.

法律架構方面也有很大差異。有些代幣化產品屬於傳統證券法下的註冊投資基金,有些則僅限合格投資人的私募產品,還有些設定為監管信託商品,由代幣代表受益權。此種法律多元性對於 DeFi 整合及跨境應用產生挑戰,因為不同結構面臨不同的轉讓限制和合格持有人條件。

DeFi Integration is where tokenized Treasuries become truly consequential. Traditional stablecoins operate as separate assets from DeFi protocols; USDC on Aave is lent and borrowed, but the underlying Treasury reserves remain locked in Circle's custodial accounts, not composable with other protocols. Tokenized Treasuries, by contrast, can potentially serve as collateral in lending protocols, provide liquidity in decentralized exchanges, back synthetic assets, and integrate into more complex financial primitives.

DeFi 整合才是國庫券代幣化的真正關鍵。傳統穩定幣作為獨立資產與 DeFi 協議互動,例如 USDC 在 [Aave] 被放貸、借用,其底層國庫券儲備仍鎖定於 Circle 的託管帳戶,無法與其他協議可組合利用。但國庫券代幣化則可望作為借貸協議的抵押品、為 DEX 提供流動性、支持合成資產,或整合到更多複雜的金融原語中。

MakerDAO's integration of RWA vaults exemplifies this convergence. In 2023-2024, MakerDAO (now operating under the Sky brand) progressively increased its exposure to tokenized real-world assets, particularly short-term Treasury exposure through partners like BlockTower and Monetalis. These RWA vaults allow MakerDAO to deploy DAI treasury holdings into yield-generating off-chain assets, with the returns helping to maintain DAI's peg and fund DAO operations. The mechanism works through legal structures where specialized entities purchase Treasuries using capital borrowed from MakerDAO in exchange for collateral and payment of interest.

MakerDAO 納入 RWA 保險庫就是鏈上鏈下融合的實例。2023-2024 年,[MakerDAO](現以 Sky 為品牌)逐步提高對國庫券等真實世界資產的代幣化曝險,尤其透過 BlockTower、Monetalis 等夥伴取得短期國債曝險。這些 RWA 保險庫讓 MakerDAO 可以將 DAI 國庫資產配置到帶來收益的鏈下資產,其報酬有助於維持 DAI 錨定與 DAO 營運。運作上,透過專業實體用 MakerDAO 出借的資金購買國庫券,並以質押與利息支付作為對價。

Ethena Labs' USDe demonstrates another integration model. USDe maintains its dollar peg through Delta-neutral perpetual futures positions (being long spot crypto and short an equivalent amount of perpetual futures contracts) which generate yield from funding rate payments. However, when funding rates turn negative (meaning shorts pay longs), this strategy becomes yield-negative. To address this, Ethena allocates a portion of its backing to Treasury bills during such periods, effectively toggling between on-chain derivatives yield and off-chain Treasury yield based on market conditions (Ethena documentation). This dynamic allocation would be difficult to implement without tokenized or easily accessible Treasury products.

Ethena Labs 的 USDe示範了另一種整合模型。USDe 仰賴中性對沖的永續合約部位(做多現貨加密資產、做空等額永續合約),借由資金費率報酬維持美元錨定。但當資金費率轉為負值(即做空方需支付利息予做多方),該策略將產生負收益。為解決此問題,Ethena 於該時期將部分資產配置到國庫券上,實現根據市場條件在鏈上衍生品收益與鏈下國債收益間切換(Ethena 官方文檔)。若沒有國庫券代幣化或易於存取的國債產品,這種動態分配將難以落實。

Frax Finance has pursued a more aggressive RWA strategy through its Frax Bond system (FXB), which aims to create on-chain representations of various maturity Treasury bonds. The goal is to build a yield curve of tokenized Treasuries on-chain, allowing DeFi protocols to access not just short-term money market rates but also longer-duration government yields. This would enable more sophisticated fixed-income strategies in DeFi, though implementation has faced regulatory and technical challenges.

Frax Finance 透過其 Frax Bond 系統(FXB)運行更積極的 RWA 策略,旨在將不同到期期限的國債數位化上鏈。其目標為建立國庫券代幣的鏈上收益曲線,使 DeFi 協議可直接取得不僅僅是短天期的貨幣市場利率,還包含更長期的政府債券收益。此舉將讓 DeFi 可發展更進階的固定收益策略,雖然在法規和技術面仍存落地難題。

Aave Arc and Permissioned DeFi Pools represent another convergence point. Recognizing that regulated institutional investors cannot interact with fully permissionless protocols, Aave launched Arc (and later, Aave institutions-focused initiatives) to create whitelisted pools where only KYC-verified participants can lend and borrow. Tokenized Treasuries can potentially serve as collateral in such pools, allowing institutions to gain leverage against government securities holdings while remaining within regulatory boundaries. This creates a bridge between traditional finance and DeFi, mediated by tokenized Treasury products.

Aave Arc 與許可制 DeFi 池是又一種融合案例。因合規機構投資人無法和完全去中心化協議直接互動,Aave 推出 Arc(及後續針對機構的方案),設計僅限 KYC 通過者參與的白名單池。國庫券代幣在此可望作為抵押品,讓機構能對政府證券持倉進行槓桿操作並同時符合法規規定,搭起傳統金融與 DeFi 間的橋樑。

The legal and technical differences between custodied Treasuries backing stablecoins and tokenized Treasuries are substantial. When Circle holds $28 billion in Treasuries backing USDC, those securities exist as conventional holdings at custodian banks, registered in Circle's name or in trust for USDC holders. They are not divisible, not directly transferable on-chain, and not usable as collateral outside of Circle's own operations. USDC holders have a contractual claim to

**穩定幣背後由託管國庫券與國庫券代幣化之間,在法律與技術層面有極大差異。當 Circle 持有 280 億美元作為 USDC 儲備的國庫券時,這些證券是以傳統託管方式存在於銀行名下(Circle 名下或為 USDC 持有人設立信託)。這些國庫券無法分割,也無法直接在鏈上轉移,更不能作為 Circle 業務外的抵押品。USDC 持有人僅擁有合約層面的請求權,**redemption at par, but no direct property interest in the underlying Treasuries.

以 token 方式發行的美國國債則不同,代表對基金或資產層級的直接持有權益。持有 Franklin 的 BENJI 代幣,即擁有該基⾦投資組合的部分實益權,類似於持有傳統貨幣市場基金的股份。這種持有權益在符合法規的前提下可轉讓、可作為其他協議的擔保品,並有機會直接兌換為底層證券,而不僅僅是現金。

這些差異造就了截然不同的風險輪廓與應用場景。穩定幣因維持穩定的 1 美元價值且避免市價波動,仍是支付與交易用途的首選。相對地,Token 化國債價格會隨利率變動與已累積利息而有輕微波動,使其作為支付媒介較不理想,但更適合用作抵押品或投資工具。兩者屬於互補而非競爭關係。

Token 化帶來的監管影響 在許多法域仍不明朗。在美國,代表基金股份的 Token 化國債很可能被歸類為證券,需要依據《投資公司法》與《證券法》登記或申請豁免。美國證券交易委員會(SEC)針對此類產品的合規結構指引有限,因此造成法律不確定性,進而拖緩機構採用速度。在歐洲,《加密資產市場(MiCA)》法規將大多數 Token 化國債歸類為資產參照型代幣,須取得授權及管理準備金,類似穩定幣;若屬於證券另有不同要求。

更廣泛的趨勢已經明顯:加密產業正打造越來越精細的結構,來表示並交易美國政府債務。穩定幣發行機構最初僅將儲備資金停泊於美債,如今已演化為多元路徑,嘗試將國債直接鏈上化、整合至 DeFi 協議,甚至重現傳統固定收益市場的殖利率曲線與期限結構。

未來最終可能形成一套平行金融系統,鏈上大多數美元計價資產最終都繞回國債敞口,讓加密市場運作深度依賴美國政府債券市場的穩定性。

穩定幣資金流對聯準會操作與美國國債市場的影響

穩定幣儲備投入國債市場的規模如今已大到足以對利率、回購市場動態以及聯準會政策傳導產生可觀察影響。理解這些反饋迴路,對評估金融穩定性和潛在監管介入機會至關重要。

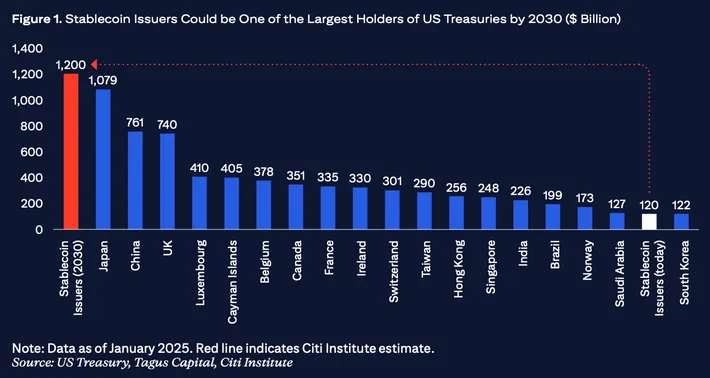

規模與背景:截至 2024 年中,主要法幣掛鉤的穩定幣總市值已超過 1,500 億美元,依公開儲備組成資料(整合自 Circle、Tether 及其他發行方報告),約有 1,200~1,300 億美元直接或間接持有於美國國庫券與相關貨幣市場工具。對照之下,1,300 億美元約為美國短期國庫券市場(截至 2024 年第二季約 $5.5 兆美元)總規模的 2~3%。雖未到主導地位,但一旦出現資金快速流入或流出,已足以產生關鍵影響。

相比之下,1,300 億美元已高於許多主權財富基金的國債部位,超越不少國家的外匯存底,更接近大型貨幣市場基金集團的資產規模。當穩定幣淨增發於數月內增加 400~500 億美元(如 2024 年初狀況),這樣的資金流入於短期國債市場的需求,相當於中型央行同期間的購債能量。

對國債孳息的需求效應:當穩定幣增發加速,發行方必須在數日或數週內,將新增加的法幣投入國庫券與回購協議,以賺取收益並維持儲備充足。這波對短天期國債的旺盛需求會壓低利率(殖利率)。原理很直觀:在供給固定下的購買力提升,推高價格、壓低殖利率。

這個效果,尤其在非常短天期市場最顯著,特別是隔夜與一週到期的國債,因為穩定幣發行者會保留最高流動性。2023-2024 強勁成長期,觀察家曾注意到最短天期的國庫券利率以及隔夜回購利率持續下行,即便聯準會貨幣政策利率維持在 5.25~5.5%。雖然受多重因素影響,但穩定幣需求明確壓縮利差。

這也造成一種矛盾:當利率越高,穩定幣發行者收益也越高,誘發更大發行動能;但這股新增資金流入本身會將短天期國債收益率壓低,削弱自身獲利空間。這種正負反饋回路雖具自我限制性,但在市場利率設定上創造了新動態。

回購市場的交互作用:美國金融體系的隔夜與期限回購市場,是銀行、對沖基金等機構以國債做為擔保品進行現金拆借的核心“水管”。聯準會的反向回購機制(ON RRP,對方將現金存入聯準會隔夜)與回購機制(聯準會以國債質押放款)共同形成整體貨幣市場的利率地板與天花板。

穩定幣發行者倚賴回購協議作為儲備投資,已然直接融入這個生態。當 Circle 或 Tether 投資數十億於隔夜反向回購時,本質上是在供給本可能由貨幣市場基金或其他現金充裕機構供給的資金。這原則上會對隔夜回購利率產生上行壓力(因現金供給增加),但受限於聯準會 ON RRP 機制以固定利率提供充足對手方,使這種影響會被部分吸收。

而更顯著的影響,會在市場壓力時期出現。若穩定幣大規模被贖回,發行者需短時間內從回購市場回收現金,可能抽離數十億規模的資金,進而減少其他回購市場參與者可獲現金。

例如2023 年 3 月 USDC 脫鉤事件,三天內大約 100 億美元贖回,Circle 為籌措現金大規模拋售回購與國債部位。這類被動賣壓可能在流動性最吃緊時,進一步放大回購市場波動。

聯準會政策傳導效應:聯準會政策利率不僅影響穩定幣收益結構,也進一步反饋到國債市場。當聯準會升息,穩定幣發行者的利差利潤增加(儲備收益提高,對持幣人支付為零),因此更有誘因大量發行,推動市值成長,增加短天期國債需求,部份抵消聯準會收緊貨幣時意欲拉升利率的效果。

相反地,若聯準會降息至零附近,穩定幣發行者幾乎拿不到任何國債孳息,營運誘因大幅下降,或許放慢發行腳步,甚至減少供給,部分使用者亦會尋求更高收益資產,可能出現贖回潮、減少對國債的需求。

這帶來一個順循環現象:當利率高時,穩定幣對國債需求最高(聯準會緊縮時);當利率低時,需求最低(寬鬆時)。這種現象部分抵銷聯準會政策效果,在緊縮時意外支撐短端國債,在寬鬆時抽離支撐。

市場結構與集中風險:現實中,幾家少數發行方集中管理著龐大穩定幣儲備,透過數個核心託管銀行運作,這造成潛在脆弱點。例如 Tether 如果必須在短時間拋售上百億美元國債,勢必對市場深度與價格造成衝擊。回顧2008 年金融危機時,貨幣市場基金遭遇大規模贖回即大量被動賣出國債,導致波動放大;未來穩定幣也可能類似。

這種集中也體現在託管體系。多數穩定幣資金僅由少數幾家銀行及信託公司託管。若這些機構出現營運問題或受監管限制,可能影響多家穩定幣同時提取儲備,觸發贖回瓶頸。2023 年 3 月矽谷銀行倒閉事件,Circle 存有大額資金,其中一小部分 USDC 儲備受影響,惟市場恐慌觸發價值脫鉤及百億規模贖回,正是連動鏈結風險實例。

加密市場壓力時的波動放大:穩定幣贖回動態與加密市場週期高度關聯。當加密幣價大跌,交易者會迅速轉向穩定幣,increasing issuance. When they recover, traders redeem stablecoins to buy crypto, reducing issuance. When confidence breaks entirely, users may exit crypto completely, redeeming stablecoins for fiat and removing billions from the system.

發行量持續增加。當市場復甦時,交易者會將穩定幣贖回,購買加密貨幣,導致發行量減少。當信心完全崩潰時,用戶可能會完全退出加密貨幣市場,將穩定幣兌換成法幣,將數十億資金撤出整個系統。

These cyclical flows create corresponding volatility in Treasury demand. A $50 billion reduction in stablecoin supply over several months translates to $50 billion in Treasury selling, occurring during periods when crypto markets are likely already experiencing stress. If crypto stress coincides with broader financial stress, this forced Treasury selling would occur when market liquidity is most challenged, potentially amplifying problems.

這些循環流動造成了國債需求的相應波動。幾個月內穩定幣供應減少500億美元,意味著國債也出現500億美元的賣壓,往往發生在加密市場已經承受壓力的時候。如果加密市場壓力與更廣泛的金融壓力同時出現,這種被迫拋售國債就會在市場流動性最脆弱時發生,可能進一步加劇問題。

The converse is also true: during crypto bull markets when stablecoin issuance surges, tens of billions in new Treasury demand emerges from a non-traditional source, potentially distorting price signals and rate structures in ways that confuse policymakers trying to read market sentiment.

反之亦然:在加密牛市期間,穩定幣發行激增,來自非傳統來源的數百億美元國債需求浮現,有可能扭曲價格信號及利率結構,使企圖解讀市場情緒的決策者感到困惑。

Cross-Border Capital Flows: Unlike traditional money market funds which primarily serve domestic investors, stablecoins are global by nature. A user in Argentina, Turkey, or Nigeria can hold USDT or USDC as a dollar substitute, effectively accessing U.S. Treasury exposure without directly interacting with U.S. financial institutions. This creates channels for capital flow that bypass traditional banking surveillance and balance of payments statistics.

**跨境資本流動:**與主要服務本國投資人的傳統貨幣市場基金不同,穩定幣天生具有全球性。阿根廷、土耳其或尼日利亞的用戶可以將USDT或USDC作為美元替代品持有,實質上獲得美國國債的敞口,而無需與美國金融機構直接互動。這形塑出繞過傳統銀行監管與國際收支統計的資本流動通道。

When global users accumulate billions in stablecoins, they are indirectly accumulating claims on U.S. Treasury securities, funded by capital outflows from their home countries. This demand for dollar-denominated stores of value supports both the dollar and Treasury markets, but it occurs outside formal channels that central banks and regulators traditionally monitor. During currency crises or capital control periods, stablecoin adoption can accelerate, creating sudden spikes in demand for Treasuries that market participants may struggle to explain using conventional models.

當全球用戶累積數十億美元的穩定幣時,他們也間接累積美國國債的請求權,這筆資金來自本國的資本外流。對美元計價價值儲存工具的需求,不僅支撐了美元,也支撐國債市場,但這是在央行及監管單位傳統上難以監控的正式通道之外進行。當貨幣危機或資本管制時期來臨,穩定幣採用速度可能加快,造成國債需求激增,傳統模型難以解釋這種現象。

The integration of stablecoins into monetary plumbing is still in early stages, but the direction is clear: crypto has created a new channel for transmitting monetary policy, distributing government debt, and mobilizing global dollar demand, with feedback effects that central banks and treasury departments are only beginning to study systematically.

穩定幣融入貨幣體系的過程仍在初期,但方向已趨明朗:加密貨幣創造了傳導貨幣政策、分配政府債務與動員全球美元需求的新管道,其反饋效果才剛開始受到央行及財政部門的系統研究。

Risks: Concentration, Runs, and Maturity Transformation

風險:集中度、擠兌與期限錯配

The fusion of stablecoin infrastructure and Treasury exposure creates multiple categories of risk, some familiar from traditional money markets and others unique to crypto-native systems. Understanding these risks is essential because a major stablecoin failure could have ripple effects extending far beyond crypto markets.

穩定幣基礎設施與國債敞口的融合創造出多種類型的風險,其中有些沿襲自傳統貨幣市場,有些則是加密原生系統獨有。理解這些風險至關重要,因為若主要穩定幣發生嚴重失敗,所引發的漣漪效應將遠不止於加密市場。

Run Dynamics and Redemption Spirals represent the most immediate danger. Stablecoins promise instant or near-instant redemption at par, but their reserves are invested in securities that may take days to liquidate at full value. This maturity mismatch creates classic run vulnerability: if a large percentage of holders simultaneously attempt to redeem, the issuer may be forced to sell Treasury securities into falling markets, realize losses, and potentially break the peg.

擠兌動態與贖回螺旋是眼前最嚴峻的風險。穩定幣承諾可立即或幾乎立即以面值贖回,但其儲備通常投資於有價證券,完全變現可能需時數日。這種期限錯配帶來典型擠兌脆弱性:若大量持有人同時要求贖回,發行方就必須在下跌的市場中拋售國債,承受損失,甚至可能導致匯率脫鉤。

The mechanism differs from bank runs in important ways. Banks face legal restrictions on how quickly they can be drained; wire transfers and withdrawal limits impose friction. Stablecoins can be transferred instantly and globally, 24/7, with no practical limits beyond blockchain congestion. A loss of confidence can trigger redemptions at digital speed. During the March 2023 USDC event, approximately $10 billion redeemed in roughly 48 hours - a burn rate that would challenge any reserve manager.

這一運作機制和銀行擠兌存在重要差異。銀行有法規限制資金流失速度、電匯和提領額度亦設有摩擦因素;而穩定幣可實現全球24/7即時轉移,實際上只有區塊鏈壅塞才會構成障礙。一旦信心喪失,贖回可爆發「數位級速度」。以2023年3月USDC事件為例,約100億美元在48小時內被贖回,這種速度足以讓任何儲備經理面臨巨大挑戰。

The TerraUSD collapse in May 2022 demonstrated how quickly confidence can evaporate in crypto markets. UST lost its peg over a few days, triggering a death spiral where redemptions begat price declines which begat more redemptions. While fiat-backed stablecoins have stronger backing than algorithmic stablecoins, they are not immune to similar dynamics if doubt emerges about reserve adequacy or liquidity.

2022年5月TerraUSD崩潰事件證明了加密市場信心蒸發的速度。UST在短短數日即失去錨定,引發死亡螺旋——贖回導致價格下跌,下跌又加速贖回。儘管法幣支撐型穩定幣的背書比算法型穩定幣更強,但若外界對其儲備充足性或流動性產生懷疑,仍無法完全避免類似情況。

The structure of stablecoin redemptions creates additional pressure. Typically, only large holders and authorized participants can redeem directly with issuers, while smaller holders must sell on exchanges. During stress events, exchange liquidity can dry up, causing stablecoins to trade at discounts to par even while direct redemptions remain available. This two-tiered structure means retail holders may experience losses even if institutional holders can redeem at par, creating distributional inequities and accelerating panic.

穩定幣贖回機制本身也帶來額外壓力。一般來說,僅大型持有人或授權參與者可直接向發行方贖回,小型持有人必須在交易所賣出。在壓力事件中,交易所流動性可能枯竭,導致穩定幣即便仍可直接以面值贖回,但在場外交易卻出現折價。這種雙層結構讓散戶即便機構投資人可平價贖回本位,也可能承受損失,加劇分配不均並助長恐慌。

Liquidity Mismatch arises from the fundamental tension between instant redemption promises and day-to-day settlement cycles in Treasury markets. While Treasury bills are highly liquid, executing large sales and receiving cash still requires interaction with dealer markets and settlement systems that operate on business-day schedules. If redemptions spike on a weekend or during market closures, issuers may face hours or days during which they cannot fully access reserves to meet outflows.

流動性錯配源自於即時贖回承諾 vs. 國債市場每日結算週期的本質矛盾。雖然國債流動性高,大量拋售並收回現金仍需要和券商市場、結算系統互動,這些只在工作日運作。如果贖回高峰發生在週末或市場關閉時段,發行商可能有數小時至數天無法完全動用儲備回應資金流出。

Stablecoin issuers manage this through liquidity buffers - portions of reserves held in overnight instruments or cash. However, determining the right buffer size involves guesswork about tail-risk redemption scenarios. Too small a buffer leaves the issuer vulnerable; too large a buffer sacrifices yield. The March 2023 USDC event suggested that even sizable buffers may prove insufficient during confidence crises.

穩定幣發行方會用流動性緩衝資產——如隔夜工具或現金—來因應,但要決定多大比例才算合適,需對「極端尾端贖回」情境進行預測。流動緩衝過小,風險升高;持有過大,收益受損。2023年3月USDC事件顯示,即使是相當大的緩衝,在信心危機時也可能不夠。

Mark-to-Market vs. Amortized Cost Accounting creates transparency and valuation challenges. Treasury bills held to maturity return par value regardless of interim price fluctuations, but bills sold before maturity realize market prices. If interest rates rise after an issuer purchases bills, those bills decline in market value, creating unrealized losses.

市價評價 vs. 攤銷成本會計造成透明度與估值挑戰。國債如果持有至到期,可以拿回面值,無論中途市價如何浮動;但如果提前賣出,就只能按當前市價。若購買後利率上升,國債市價下跌,即產生未實現損失。

Stablecoin attestation reports typically value reserves using amortized cost or fair value approaches. Amortized cost assumes bills will be held to maturity and values them based on purchase price adjusted for accruing interest. Fair value marks positions to current market prices. In stable conditions, these methods produce similar results, but during interest rate volatility, gaps can emerge.

穩定幣審計報告通常是用攤銷成本或公允價值來計價。攤銷成本法假設會持有至到期,依購買成本加累積利息評價。公允價值則以當前市價計算。市場穩定時二者相差不大,但利率劇烈波動時差距就會出現。

If an issuer holds $30 billion in Treasury bills at amortized cost but interest rates have risen such that the fair value is only $29.5 billion, which number represents the "true" reserve value? If forced selling occurs, only $29.5 billion may be realizable, creating a $500 million gap. Some critics argue that stablecoins should mark all reserves to market value and maintain over-collateralization buffers to absorb such gaps, but most issuers use cost-basis accounting and claim 1:1 backing without additional buffers.

如果發行方以攤銷成本持有300億美元國債,但由於利率上升,市價僅剩295億美元,那麼哪一個才是「真實」儲備價值?如果被迫拋售,最多只能換回295億,產生5億差額。有批評認為穩定幣應以市價計價全部儲備並維持超額抵押緩衝來吸收落差,但大多數發行方採用成本會計並主張1:1儲備,且無額外緩衝。

Counterparty and Custodial Concentration poses operational risks. Stablecoin reserves are held at a small number of banking and custody institutions. If one of these institutions faces regulatory intervention, technological failure, or bankruptcy, access to reserves could be impaired. The Silicon Valley Bank failure in March 2023 demonstrated this risk; USDC's exposure was only about 8% of reserves, but even that limited exposure triggered sufficient uncertainty to cause a temporary depeg.

對手方及託管機構集中風險構成營運層面的威脅。穩定幣儲備集中於少數銀行及託管機構。若其中之一遭遇監管介入、技術故障、或倒閉,資金存取就會受阻。2023年3月矽谷銀行倒閉就是例證;USDC儲備曝險僅約8%,但也引發足夠的不確定性,導致短暫脫鉤。

More broadly, the crypto custody industry remains young and evolving. Operational risks include cyber attacks on custodian systems, internal fraud, technical failures that impair access to funds, and legal complications in bankruptcy or resolution scenarios. While traditional custody banks have decades of institutional experience, the crypto custody space includes newer entrants with shorter track records.

更廣義來看,加密貨幣託管業仍在發展初期。營運風險包括託管系統遭受網攻、內部詐騙、技術失靈導致資金無法進出、或破產及清算時的法律糾紛。傳統託管銀行有數十年的經驗,但加密貨幣託管則有許多新進玩家,歷史紀錄較短。

Regulatory and Jurisdictional Arbitrage creates risks from inconsistent oversight. Stablecoin issuers are chartered in various jurisdictions with different regulatory approaches. Circle operates as a money transmitter in the U.S. with varying state-level licenses. Tether is registered in the British Virgin Islands with less stringent disclosure requirements. Paxos operates as a New York trust company with strong regulatory oversight. This patchwork means that similar products face different rules, disclosure standards, and supervisory intensity.

監管與司法套利產生於監管不一致。不同穩定幣發行方位於不同司法管轄區,各自面臨不同監理方式。Circle以「金錢轉移業者」身份在美國運營,持有各州不同牌照;Tether註冊於英屬維京群島,揭露要求相對寬鬆;Paxos則作為紐約信託公司營運,監管嚴格。這種拼湊式格局使得類似產品面對不同規則、揭露標準與監管強度。

The potential for regulatory arbitrage is obvious: issuers may locate in jurisdictions with lighter oversight while serving global users, externalizing risks to the broader system. If a crisis emerges, the lack of clear regulatory authority and resolution frameworks could create coordination problems and delay effective responses.

這種監管套利的機會顯而易見:發行方可以設立在低監管地區,服務全球用戶,把風險外部化到更廣泛體系。一旦危機發生,欠缺明確監管權責與處理框架,可能導致協調困難及延遲有效回應。

Contagion Channels to Traditional Finance run in both directions. If a major stablecoin fails, forced liquidation of billions in Treasuries could disrupt repo markets and money market funds, particularly if the liquidation occurs during a period of broader market stress. The selling would affect prices and liquidity, creating mark-to-market losses for other Treasury holders and potentially triggering margin calls and additional forced selling.

傳統金融的傳染途徑是雙向的。若某主流穩定幣失敗,被迫拋售數十億國債可能擾亂回購市場及貨幣市場基金,尤其是在大環境本就緊張時。這將影響價格和流動性,讓其他國債持有人產生市值虧損,進而觸發追加保證金和進一步拋售。

Conversely, stress in traditional finance can contaminate stablecoins. Banking system problems can impair stablecoin issuers' access to custodied reserves, as occurred with Silicon Valley Bank. A broader banking crisis could create cascading failures across multiple stablecoin custodians simultaneously. Money market fund problems could impair the funds that some stablecoin issuers use for reserve management.

反過來,傳統金融的壓力也會波及穩定幣。銀行體系問題可能限制發行商對託管儲備的存取,如矽谷銀行案例。若出現更大規模的銀行危機,則可能多家託管機構同時出現連鎖失效。貨幣市場基金問題也可能損及部分穩定幣發行商所依賴的儲備管理基金。

Historical Analogies provide sobering context. The Reserve Primary Fund "broke the buck" in September 2008 when its holdings of Lehman Brothers commercial paper became worthless, triggering redemptions across the entire money market fund industry. The Fed ultimately intervened with lending programs to stabilize the sector, but not before significant damage occurred.

歷史類比值得警惕。2008年9月,Reserve Primary Fund發生「跌破面值」事件,其持有的雷曼兄弟商業票據變為廢紙,引發整個貨幣市場基金產業大規模贖回。最終聯準會出手穩定市場,但重大損失已然發生。

Earlier, in the 1970s,money market funds experienced periodic runs as investors questioned the value of underlying commercial paper holdings during corporate debt crises. These events led to regulatory reforms including stricter portfolio rules, disclosure requirements, and eventual SEC oversight under the Investment Company Act.

貨幣市場基金在企業債危機期間,因投資人質疑其基礎商業本票資產的價值,而經歷了週期性的擠兌事件。這些事件促使監管機構進行改革,包括更嚴格的投資組合規則、資訊揭露要求,以及最終納入《投資公司法》下由美國證券交易委員會(SEC)監管。

Stablecoins today resemble money market funds circa 1978: rapidly growing, lightly regulated, increasingly systemic, and operating under voluntary industry standards rather than comprehensive regulatory frameworks. The question is whether stablecoins will experience their own "breaking the buck" moment before regulation catches up, or whether proactive regulatory intervention can avert such an event.

如今的穩定幣類似於1978年前後的貨幣市場基金:快速成長、管理鬆散、系統性風險日益提高,並運作於自願性產業標準之下,而非全面性的監管架構。問題在於,穩定幣會否在監管跟上之前,出現屬於它們自己的「脫鉤」時刻,還是監管機關主動介入能預防此類事件。

Maturity Transformation and Credit Intermediation creates additional concerns if stablecoins evolve toward lending practices. Currently, most major stablecoins invest only in government securities and repo, avoiding credit risk. However, economic incentives push toward credit extension: lending to creditworthy borrowers generates higher yields than Treasuries, increasing issuer profitability.

期限轉換與信用中介若穩定幣朝向放貸演變,將引發更多疑慮。現階段,大部分主流穩定幣僅投資於政府證券及回購協議,避免接受信用風險。然而,經濟動機會推動發債:借貸給具信用的借款人帶來比國債更高的收益,進一步提升發行者的獲利能力。

Some stablecoin issuers have experimented with or discussed broader reserve compositions including corporate bonds, asset-backed securities, or even loans to crypto companies. If this trend accelerates, stablecoins would begin performing bank-like credit intermediation - taking deposits (issuing stablecoins) and making loans (investing in credit products) - but without bank-like regulation, capital requirements, or deposit insurance.

部分穩定幣發行商曾經試驗或討論過更廣泛的準備金組合,包括公司債券、資產擔保證券,甚至是對加密公司放款。若這樣的趨勢加速,穩定幣將開始履行類銀行式的信用中介職能——即吸收存款(發行穩定幣)、進行放款(投資信用產品)——但卻沒有銀行所需的監管、資本要求或存款保險。

This would amplify all the risks discussed above while adding credit risk: if borrowers default, reserve values decline, potentially below the value of outstanding stablecoins. Historical experience suggests that entities performing bank-like functions without bank-like regulation tend to fail catastrophically during stress events, from savings and loans in the 1980s to shadow banks in 2008.

這樣的發展將放大前述所有風險,並增加信用風險:若借款人違約,準備金價值下降,甚至低於流通中的穩定幣總額。歷史經驗顯示,履行銀行職能而沒有銀行監管的機構,通常在壓力事件中會以災難性方式失敗,從1980年代的儲貸機構到2008年的影子銀行皆是明證。

Transparency Deficits persist despite improvements in attestation frequency and detail. Most stablecoin attestations remain point-in-time snapshots rather than continuous audits. They typically do not disclose specific counterparties, detailed maturity profiles, concentration metrics, or stress-testing results. This opacity makes it difficult for holders, market participants, and regulators to assess true risk levels.

資訊透明度不足依舊存在,儘管在查核頻率及細節上已有改進。大多數穩定幣的查核報告仍是特定時點的快照,而非連續性的審計。這些報告通常不會揭露具體交易對手、詳細到期結構、集中度指標或壓力測試結果。這種不透明,使得持有人、市場參與者及監管機關難以評估實際的風險程度。

Moreover, the attestation standards themselves vary. Some reports are true attestations by major accounting firms following established standards. Others are unaudited management disclosures. The lack of standardized, comprehensive, independently audited reporting makes comparison difficult and creates opportunities for issuers to present reserve compositions in misleading ways.

此外,查核標準本身亦不一致。部分報告由大型會計師事務所依既定標準出具,為真正的查核;其他則僅為未經審計的公司自行揭露。缺乏標準化、全面性、由獨立第三方審核的報告,不但不利於比較,也讓發行商有機會用誤導性的方式呈現準備金組成。

The overall risk profile suggests that while stablecoins backed primarily by short-term Treasuries are dramatically safer than algorithmic or poorly-collateralized alternatives, they are not risk-free. They remain vulnerable to runs, liquidity mismatches, operational failures, and contagion effects. The migration toward Treasury exposure reduced but did not eliminate these risks, and the growing scale of the sector increases the systemic stakes if something goes wrong.

總體風險輪廓顯示,使用短期國庫券作為主要擔保的穩定幣固然遠比演算法式或擔保不足的選項安全,但並非毫無風險。它們仍然面臨擠兌、流動性錯配、運營失誤及連鎖感染等風險。雖然轉向國債有助於降低部分風險,但並未完全消除,且隨著產業規模擴大,潛在的系統性影響亦日益增大。

Who Regulates What: Legal and Supervisory Gaps

誰來監管什麼:法律與監督缺口

The regulatory landscape for stablecoins remains fragmented across jurisdictions and unsettled within them, creating uncertainty for issuers, users, and the broader financial system. Understanding this landscape is crucial because regulatory decisions will determine whether stablecoins evolve into well-supervised components of the monetary system or remain in a gray zone vulnerable to sudden restrictions.

穩定幣的監管格局在不同司法轄區之間仍然破碎且未定形,這對發行商、用戶和更廣大的金融系統都帶來不確定性。釐清這個格局非常關鍵,因為監管決策將決定穩定幣究竟能否逐步發展為貨幣體系中受嚴密監督的一員,還是繼續處於容易遭遇突發限制的灰色地帶。

United States Regulatory Patchwork: No comprehensive federal framework for stablecoins existed as of late 2024, leaving issuers to navigate a complex mosaic of state, federal, and functional regulators. The Securities and Exchange Commission (SEC) has asserted that many crypto assets are securities subject to federal securities laws, but has taken inconsistent positions on whether stablecoins constitute securities. The SEC's primary concern with stablecoins relates to whether they represent investment contracts or notes under the Howey test and other securities definitions.

**美國監管拼圖:**截至2024年底,美國尚未有涵蓋穩定幣的聯邦層級綜合性監管架構,發行商只能在州政府、聯邦及功能性監管機關的複雜拼湊中尋找依據。美國證券交易委員會(SEC)宣稱許多加密資產為證券,適用聯邦證券法,但在穩定幣是否構成證券這一點,立場並不一致。SEC主要關切穩定幣是否依《豪威測試》與其他證券定義,應視為投資契約或票據。

For yield-bearing stablecoins that promise returns to holders, the securities characterization becomes stronger. The SEC has suggested that such products likely require registration as investment companies under the Investment Company Act of 1940, subjecting them to comprehensive regulation including portfolio restrictions, disclosure requirements, and governance rules. Non-yield-bearing stablecoins like USDC and USDT occupy murkier territory; the SEC has not definitively classified them but has not exempted them either.

對於承諾收益的穩定幣,證券屬性更為強烈。SEC曾表示,這類產品很可能需依1940年《投資公司法》登記為投資公司,納入投組限制、資訊揭露、治理規範等全方位監理。不產生收益的穩定幣,如USDC及USDT,則處於更模糊的地帶;SEC尚未明確分類,也未正式豁免監理。

The Commodity Futures Trading Commission (CFTC) asserts jurisdiction over stablecoins to the extent they are used in derivatives markets or meet the definition of commodities. CFTC Chairman Rostin Behnam has advocated for expanded CFTC authority over spot crypto markets, which could include stablecoins used as settlement instruments on derivatives platforms.

商品期貨交易委員會(CFTC)則主張,若穩定幣被用於衍生品市場或符合理財商品定義,其有權針對之。CFTC主席Rostin Behnam提倡擴大CFTC對加密現貨市場的監管權限,這也包括作為衍生品平台結算工具的穩定幣。

The Office of the Comptroller of the Currency (OCC) oversees banks and has issued guidance suggesting that national banks may issue stablecoins and provide custody services for them, but with significant restrictions and supervisory expectations. The OCC's 2021 interpretive letters indicated that banks could use stablecoins for payment activities and hold reserves for stablecoin issuers, but these positions faced subsequent uncertainty under changing OCC leadership.

貨幣監理署(OCC)負責監管銀行,並提出指引指出全國性銀行可以發行穩定幣及提供託管服務,但伴隨相當多的限制和監理預期。OCC於2021年發表解釋函說明,銀行可以使用穩定幣進行支付,並可為穩定幣發行人持有準備金,但隨著OCC領導層的更迭,這些立場後續變得不確定。

State regulators maintain their own frameworks. New York's BitLicense regime regulates virtual currency businesses operating in the state, including stablecoin issuers serving New York residents. The New York Department of Financial Services requires licensees to maintain reserves equal to or exceeding outstanding stablecoin obligations, hold reserves in qualified custodians, and submit to regular examinations. Paxos operates under New York trust company charter, subjecting it to full banking-style supervision by New York regulators.

州級監管機構則有自有體系。紐約的BitLicense制度規範在當地經營的虛擬貨幣業者,也包括服務紐約居民的穩定幣發行商。紐約金融服務局(NYDFS)要求持牌機構持有與流通穩定幣等值或更多的準備金,且存放於合格託管機構,並接受定期審查。Paxos即以紐約信託公司牌照運營,須接受紐約監管單位的完整銀行型監督。

Other states have developed money transmitter licensing frameworks that may apply to stablecoin issuers. The challenge is that requirements vary dramatically: some states require reserve segregation and regular attestations, while others impose minimal standards. This creates regulatory arbitrage opportunities and uneven protection for users depending on where an issuer is located.

其他州則設有金錢傳輸執照制度,可能適用於穩定幣發行商。問題在於,各州要求差異極大:有的需要準備金隔離及定期查核,有的則標準極低。這使監管套利空間大增,也導致用戶保障程度因發行地區而異。

Federal Legislative Efforts: Multiple stablecoin bills were introduced in the U.S. Congress during 2022-2024, though none achieved passage as of late 2024. These proposals generally aimed to establish federal licensing for stablecoin issuers, impose reserve requirements, mandate regular attestations or audits, and create clear supervisory authority (either at the Fed, OCC, or a new agency).

**聯邦立法努力:**2022至2024年間,美國國會提出多項穩定幣法案,但截至2024年底尚未有立法通過。這些提案通常致力於建立穩定幣發行人的聯邦執照制度,要求持有準備金、定期查核或審計,以及賦予聯邦儲備、OCC或新設機關明確監督權責。

Key provisions in various bills included requirements that reserves consist only of highly liquid, low-risk assets (typically defined as cash, Treasuries, and repo); prohibition on lending or rehypothecation of reserves; monthly public disclosure of reserve compositions; and capital or surplus requirements. Some versions would have limited stablecoin issuance to banks and federally supervised institutions, effectively prohibiting non-bank issuers like Tether from operating in the U.S. market.

各法案的主要條款包括:準備金必須僅由高流動性低風險資產(如現金、國債、回購協議)構成;嚴禁將準備金進行放貸或再質押;每月公開披露準備金組成結構;制定資本或餘額要求。部分版本甚至將穩定幣發行權限限定於銀行及聯邦合規機構,形同禁止Tether等非銀行發行商在美國市場運作。

The regulatory disagreements centered on whether stablecoin issuers should be treated as banks (requiring federal charters and comprehensive supervision), as money transmitters (requiring state licenses and lighter supervision), or as an entirely new category with sui generis regulation. Banking regulators generally favored stringent oversight comparable to banks, while crypto industry advocates pushed for lighter-touch frameworks that would not impose bank-level capital requirements or examination intensity.

監管分歧主要在於穩定幣發行人應視為銀行(需取得聯邦銀行執照,落實全面監理)、金錢傳輸業者(需州級牌照,監督較輕),還是劃分為全新類別另設監管體系。銀行監理機關普遍主張比照銀行嚴格監督,加密產業則力促較輕度監理,避免銀行等級的資本及查核標準。

European Union - Markets in Crypto-Assets (MiCA): The EU's MiCA regulation, which began taking effect in phases during 2023-2024, created the world's first comprehensive framework for crypto asset regulation, including detailed rules for stablecoins (termed "asset-referenced tokens" and "e-money tokens" under MiCA).

**歐盟—加密資產市場監管(MiCA):**歐盟的MiCA規範於2023至2024年分階段生效,創下全球第一個涵蓋加密資產、包含穩定幣(MiCA下稱「資產參照型代幣」及「電子貨幣代幣」)的全面性監管框架。

Under MiCA, issuers of asset-referenced tokens must be authorized by competent national authorities, maintain reserves backing tokens at least 1:1, invest reserves only in highly liquid and low-risk assets, segregate reserves from the issuer's own assets, and undergo regular audits. For e-money tokens (which reference only a single fiat currency), the requirements align more closely with existing e-money regulations in the EU, potentially allowing established e-money institutions to issue them under existing licenses with some modifications.

按照MiCA,資產參照型代幣發行人必須經國家主管機關許可,維持至少1:1的準備金比例,且準備金僅能投資於高流動性、低風險資產,同時須與公司自有資產隔離並接受定期稽核。對於僅追蹤單一法定貨幣的電子貨幣代幣,MiCA規範則更貼近原有歐盟電子貨幣監管,已在歐盟領牌的電子貨幣機構,經若干調整後可直接發行此類代幣。

MiCA also imposes significant holder rights including redemption at par, disclosure obligations regarding reserve composition and valuation methodologies, and governance requirements. Perhaps most significantly, MiCA limits the ability of non-EU stablecoins to circulate in the EU unless their issuers comply with comparable regulatory standards and are authorized by EU authorities. This could theoretically restrict Tether and other non-compliant stablecoins from being offered to EU users, though enforcement mechanisms and transition timelines remain somewhat unclear.

MiCA亦賦予持有人重大的權益,包括按面值贖回權、準備金組成及估值方法的揭露義務、治理要求等。最重要的是,MiCA限制非歐盟穩定幣在歐盟流通,除非發幣商符合等效監管標準並獲得歐盟授權。理論上,這可能排除Tether等不符規範的穩定幣在歐盟市場流通,但具體執行情形與銜接期仍待釐清。

**United Kingdom

英國Approach:** 英國採取了一種混合方式,將穩定幣視為受監管代幣中的獨立類別,同時建基於現行的電子貨幣與支付服務監管規範之上。金融行為監管局(FCA)與英格蘭銀行發佈了聯合諮詢文件,建議讓穩定幣發行商接受與系統性支付系統相當的監督,包括審慎要求、運營韌性標準與儲備管理規則。

英國的監管框架區分未獲支撐的加密資產(不在監管範圍內)、主要用於支付的穩定幣(需接受更嚴格監管)、以及作為投資產品的穩定幣(可能適用證券監管)。英格蘭銀行亦探討了某些穩定幣是否可能被指定為系統性支付系統,令其接受央行的直接監管。

英國的相關提案一般要求儲備資產必須託管於破產隔離結構中,每日以公允價值計價,且只可由高品質流動資產組成。英格蘭銀行亦已表態,對於具系統性重要性的穩定幣,其儲備資產應直接存放於中央銀行,或必須可迅速無市場風險轉換為中央銀行儲備的形式。

國際協調: 金融穩定委員會(FSB)、國際清算銀行(BIS)及其他相關國際組織,已制定穩定幣監管的政策建議。這些建議大致強調幾項原則,包括相同風險、相同監管(執行銀行類職能的穩定幣須遵守銀行等級規範);全面監管穩定幣生態圈中的所有主體(發行者、託管人與驗證方);強健的儲備要求與資訊揭露;及跨境監理機關間的合作。

然而挑戰在於國際標準僅為非強制建議,需經各國主管機關推動落實。各司法轄區將這些原則轉化為國內法的方式差異甚大,造成監管割裂與套利現象持續。

揭露及透明度規定: 相對收斂的一個領域在於資訊揭露。多數主流監管提案皆要求每月或每季公開披露儲備組成,且需具備足夠細節,使外界得以進行有效分析。內容通常包括資產類型、到期結構、交易對手集中度指標及評價方法的細項。

然而,對於什麼才是「足夠」的資訊揭露,不同司法轄區標準迥異。有些要求須經公認會計準則下的完整稽核;有些僅接受資產存在性的時點性聲明(Attestation),未必覆蓋控管與持續遵循;亦有部分僅接受未稽核的公司聲明。這些落差導致市場無法迅速分辨哪些穩定幣真正達到高標。

清算與倒閉機制: 多數監理體系普遍未明確訂定穩定幣發行商倒閉時的處理框架。若 Tether 發生資不抵債,誰對儲備資產具有法律主張權?順序如何?程序為何?持有者是否像破產清算中的一般債權人一樣依比例求償,抑或有些司法轄區給予他們類似存戶的優先權?

同樣地,若一個系統性穩定幣雖仍具償付能力但遭遇擠兌,央行是否會像對待銀行那樣提供流動性支持?主管機關是否能採取暫時凍結贖回的緊急措施?未有明確指引之下,極端情境爆發時恐加劇不安。

國債通證化問題: 監理機關面對國債通證化產品時挑戰突出。這些產品是否需依照傳統證券的規範進行註冊並提供公開說明書?是否與傳統國債持有權充份接近,因此可享有豁免?可否自由嵌入 DeFi 協議,還是必須受限於受許可的封閉環境?

美國證交會(SEC)未有明確完整指引,致使國債通證化發行商僅能保守設計產品(僅限合格投資人、依規則D豁免、加強轉讓管制等)以降低監管風險。這限制了創新,也妨礙國債通證化產品在 DeFi 世界中實現最大效用的可組合性與開放性。

監理能力挑戰: 即使監管制度已建立,監理機關往往仍缺乏足夠資源、人才與科技能力,有效監督本土加密業務。檢查一家傳統銀行需懂本信貸審查、利率風險管理、放款組合等;檢查一間穩定幣發行商則需理解區塊鏈技術、密碼防護技術、分散式帳本會計、智能合約風險,以及 7x24 小時全球數位資產業態的獨特運營特質。

各國監督機關正在延攬具備加密技術背景的人才並積極建構內部能量,但一切尚需時日。監理願景與實質監督能力之落差,意味著合規問題在危機爆發前仍可能長期未被發現。

總體而言,目前監管呈現逐步趨嚴並朝收斂發展,仍有諸多缺漏、不一致與未明確處。方向明確:大型司法轄區正逐步將系統性穩定幣類比於受監理金融機構對待。但時程、具體規範內容、以及執法方式,仍充滿不確定性,導致業者持續面臨合規挑戰,使用者則承受風險。

個案研究與實證

觀察特定穩定幣發行商及其儲備策略,更能具體呈現以上論述中的多重動態。這些案例不僅展現多元策略,更顯現對國債曝險的共通趨勢。

Circle 及 USDC:透明度領先者

Circle Internet Financial 於 2018 年推出 USD Coin,與 Coinbase 合作並依 Centre Consortium 治理架構運作。Circle 從一開始就將 USDC 定位為 Tether 以外、強調透明度與合規合作的選擇,特別強調接受監管與完整的資產聲明。

USDC 儲備的演變亦體現產業的趨勢。最初,其儲備主要為存放於多家 FDIC 保險銀行的現金。至 2021 年初,Circle 開始將部分儲備轉為美國短天期國債和 Yankee 定存。Cirle 主張此組合能同時帶來收益與流動性,並維持安全。

然而,Circle 也因未公開說明各類資產佔比及商業本票的資信品質而遭詬病。在監管機構與加密社群的壓力下,Circle 於 2021 年 8 月公告 其將 USDC 儲備全面轉為現金與美國短天期國債,完全淘汰商業本票及其他公司債部位。

到了 2023 年 9 月,Circle 已完成此轉換。每月聲明顯示,接近 100% 儲備資產為 Circle Reserve Fund(由 BlackRock 管理,專投國債與國債回購)及存放於受監理銀行的現金。2023 年 10 月聲明顯示,儲備總額約 246 億美元,對應 246 億美元流通 USDC,其中約 238 億為儲備基金,現金約 8 億(Circle Reserve Report, October 2023)。

此組合於 2024 年持續穩定。2024 年 7 月聲明顯示,總儲備約 286 億美元,其中 281 億存於 BlackRock 管理的國債基金及回購,現金則有 5 億存於合作銀行如 Bank of New York Mellon 及 Citizens Trust Bank(Circle Reserve Report, July 2024)。

這帶來明顯指標性意涵:Circle 的商業模式現已完全依賴於國債投資收益,同時對 USDC 持有人不支付利息。在 5% 利率環境下,約 280 億美元儲備每年可產生約 14 億美元毛利息收入。扣除營運成本(以 Circle 的技術、合規及銀行費用,合理估約 2-4 億),USDC 事業每年可帶來約 10 億美元淨利,純粹來自「零成本資本」與國債利差。

Circle 強調透明度,雖領先業界,實際上仍有若干疑慮。每月聲明為時點性資訊,非連續稽核,亦未公開儲備基金內國債到期結構、回購交易對手曝險、流動性細項假設等。但 Circle 已建構出業界最嚴謹揭露制度,也成為監管機關主要參照標竿。

Tether 及 USDT:具爭議的巨頭

Tether Limited 於 2014 年推出 USDT,為首款主流穩定幣,起初宣傳完全由銀行帳戶中的美元支持。多年來,Tether 頻遭外界質疑其儲備充足性、透明度與公司治理。批評者指出,Tether 未完全備兌、儲備與 Bitfinex 等關聯實體混同、且誤導市場其儲備組成。

這些爭議最終導致 2021 年 2 月與紐約州檢察官辦公室的和解。Tether 同意支付 1850 萬美元罰款並停止與紐約居民的交易活動,更重要的是,承諾透過每季公開報告準備金組成來加強透明度。

Tether隨後的準備金披露顯示其結構發生了巨大變化。2021年第二季的查證報告顯示,僅有約10%的準備金由現金及銀行存款構成,約65%為商業票據及定存,12%則為公司債及貴金屬,其餘則為其他資產(Tether Transparency Report, Q2 2021)。這種結構引發重大疑慮:Tether持有數百億美元、來源不明的商業票據,潛在包含中國房地產開發商與其他高風險信用。

在監管機關及市場參與者的壓力下,Tether開始逐步轉向更安全的資產。到2022年第四季,Tether報告指出,其超過58%的準備金為美國國庫券,另有24%為貨幣市場基金(主要投資於國庫券及回購),約10%為現金及銀行存款,少部分則為其他資產(Tether Transparency Report, Q4 2022)。

這一趨勢持續到2023-2024年。2024年第二季的查證報告顯示,Tether的準備金組成進一步偏向政府證券:約845億美元的準備金中,有84.5%屬於現金、現金等價物、隔夜逆回購及短期美國國庫券(Tether Transparency Report, Q2 2024)。Tether披露其持有超過970億美元的美國國庫券,成為全球最大的國庫券持有者之一。

Tether此一模式帶來的獲利能力極為驚人。以970億美元的國庫券、約5%收益率計算,Tether每年幾乎可產生近50億美元的總利息收入。Tether於2024年第一季查證中披露其超額準備金超過45億美元(即資產超過1:1準備要求),這反映了多年來所累積的利差收益全部流向Tether股東,而非USDT持有人(Tether Q1 2024 attestation)。

然而,Tether的透明度仍遜於Circle。Tether是以季度報告而非每月報告,且以查證取代完整審計,對於國庫券持倉和銀行往來揭露細節較少,對公司結構或治理更是鮮有說明。Tether註冊地為英屬維京群島,且其所有權結構公開資訊有限,這些情況即使準備金披露有所提升,仍令外界有疑慮。

Circle與Tether的對比,凸顯產業一項關鍵張力:Tether較輕的監管途徑讓其得以維持主導及極大化獲利,而Circle的合規優先策略則雖有利於未來監管,但會犧牲部分短期優勢。

Ethena Labs 與 USDe:合成美元的實驗

Ethena Labs是新一代穩定幣設計的代表,於2023年底發行USDe。USDe定位為「合成美元」,不靠法幣準備,而是以Delta中性衍生品策略及多元化資產作為支持。

其機制定於持有現貨加密貨幣(主要為比特幣與以太幣)的多頭部位,以及等值的永續合約空頭部位。這些部位彼此平衡時,幣價變動將互相抵消:例如比特幣漲10%,現貨多頭賺10%,空頭則虧10%,整體美元價值保持穩定。該策略的收益來自永續合約市場的資金費率,通常多頭會支付空頭該費率,進而成為Ethena的收益來源。

然而,空頭資金費率在熊市時可能轉為負值,使得該策略變為成本而非收益。為此,Ethena將美國國庫券納入USDe的支持策略。在負資金費率或風險管理需時,Ethena會直接或透過代幣化國庫券產品將資本配置於國庫券(Ethena documentation, 2024)。

截至2024年年中,USDe流通量已超過30億美元,儘管推出僅短短數月,已成為排名前列的穩定幣之一。其資產組成因市場狀況而動態調整,但Ethena已公開持有數十億美元國庫券作為儲備策略,輔助核心Delta中性衍生品部位。

Ethena這種方式本質上與純法幣支持的穩定幣有根本差異。USDe持有人不享有Ethena直接兌換保證,而是依靠套利機制及市場力量來維持價格鉤定。Ethena亦提供帶收益型產品sUSDe,將資金費率及國庫券受益回饋用戶,2024年年化收益率約為8-27%,視市場狀況而定。

Ethena一案顯示,即便是創新且原生於加密的穩定幣模型,也傾向於將國庫券納入,以進行風險管理及收益增長。國庫券在USDe的資產支持中,於衍生品市場不利時提供穩定性,亦帶來額外收益,強化該產品的經濟可行性。

Paxos信託公司與受監管穩定幣

Paxos信託公司,由紐約金融服務局核發有限目的信託公司牌照,是主要穩定幣發行商中最受嚴格監管的一家。Paxos除自發USDP穩定幣,也曾在2023年前管理Binance USD(BUSD)儲備。

受信託執照監管,Paxos須接受全面銀行式監督,包括定期稽核、資本要求、嚴格資產隔離規則以及詳盡的資訊申報義務。Paxos每月均發佈由獨立會計師事務所出具的查證聲明,揭露其儲備投資組合中每個證券的確切CUSIP碼,達到前所未有的透明度。

Paxos的準備金策略始終強調國庫券部位。2023-2024年間的每月報告均顯示,USDP支持資產幾乎100%為FDIC保險銀行現金或短期美國國庫證券。例如2023年11月查證,明列每檔國庫券的CUSIP、到期日及面額,總額約為5.2億美元,完全支持市面上5.2億美元USDP(Paxos attestation, November 2023)。

Paxos的監管模式展現出在傳統金融監管下運營的優勢與侷限。優點包括明確的法律地位、機構用戶面對的監管清晰度,以及來自全面監督的信譽保證。侷限則在於較高的合規成本、經營彈性受限,以及相對不受限競爭對手的靈活度和淨利。

BUSD案例亦提供監管風險之警示。In February 2023, the New York Department of Financial Services ordered Paxos to cease minting new BUSD tokens due to unspecified regulatory concerns, even though BUSD reserves appeared fully backed.

此舉導致BUSD逐步退場,該幣最高曾流通超過160億美元。突如其來的監管干預證明,即使是完全合規的穩定幣業務也難免監管不確定性,且可能很短時間內被命令關停。

代幣化國庫券應用:Franklin Templeton 與 Ondo

Franklin Templeton於2023年推出BENJI代幣,代表Franklin OnChain美國政府貨幣基金的股份,標誌著傳統金融巨擘涉足代幣化國庫券領域。BENJI代幣於Stellar和Polygon區塊鏈流通,代表按比例持有由傳統貨幣市場基金管理的國庫券及政府回購協定組合的權益。

截至2024年底,Franklin OnChain基金資產雖尚不算龐大但有持續成長,體現機構投資人希望透過區塊鏈工具參與國庫券收益。該基金結構提供監管明確性(依照投資公司法登記)及傳統基金保障,同時具備區塊鏈基礎的轉帳與結算能力。

Ondo Finance的代幣化國庫券產品,尤其是OUSG,同樣吸引了數億美元來自加密原生用戶,這些投資人希望在不離開加密生態的情況下持有國庫券。這類產品讓DeFi協議及加密財庫,在鏈上就能賺取政府收益,並享有資產可組合與透明之優點。

上述案例共同反映出幾股一致趨勢:無論穩定幣型態或業務模式為何,轉向國庫券的現象幾乎是普遍且持續的;驅動該趨勢的經濟誘因強大且不變;透明度與合規程度分歧甚大,但標準正逐步提升;而以國庫券為核心的儲備體系帶來的超高獲利,仍不斷吸引新競爭者及資金進駐本領域。

情境規劃與前瞻指標

要理解穩定幣-國庫券整合的可能未來,需要檢視幾種替代演變路徑及相應的訊號。下列四大情境涵蓋了從善意整合到系統性壓力的可能性。

情境一:良性整合與機構採納

在此樂觀版本中,穩定幣經全面監管,正式成為貨幣體系組成要素,既獲得正當性又設有充分保障。這一過程可能Unfold as follows:

Major jurisdictions implement coordinated stablecoin regulations by 2025-2026 that establish clear licensing requirements, comprehensive reserve rules mandating Treasury and cash-only backing, regular audits by independent firms, and explicit resolution frameworks. Bank regulators permit federally chartered banks to issue stablecoins under appropriate guardrails, bringing traditional financial institutions into the market alongside crypto-native issuers.

主要司法管轄區於2025至2026年間實施協調性的穩定幣監管,建立明確的發牌要求、全面性的準備金規則(強制要求僅以美國國債及現金作為儲備)、定期由獨立公司進行審計,以及明確的解決框架。銀行監管機構允許聯邦特許銀行在適當的風險控管下發行穩定幣,使傳統金融機構能與加密原生發行方一同進入市場。

The Federal Reserve potentially develops a framework for stablecoin issuers to maintain reserve accounts directly at the Fed, similar to how money market funds access the overnight reverse repo facility. This would eliminate much of the custody risk and create direct liquidity channels between stablecoins and the central bank. Some central bank researchers have explored whether systemically important stablecoins might eventually be treated as components of the monetary base, with implications for monetary policy implementation.

聯邦準備理事會(Fed)有可能為穩定幣發行方制訂框架,允許其直接在聯準會開設儲備賬戶,類似貨幣市場基金接觸隔夜逆回購機制。這將大幅減少託管風險,並在穩定幣與中央銀行之間建立直接的流動性通道。一些央行研究人員亦曾探討,系統性重要穩定幣日後是否會被視為貨幣基礎的一部分,進而對貨幣政策的執行產生影響。

Traditional asset managers increasingly offer tokenized Treasury products, creating deeper liquidity for on-chain government debt markets. Pension funds, insurance companies, and corporate treasuries begin allocating portions of cash management portfolios to yield-bearing stablecoins or tokenized Treasuries, viewing them as efficient alternatives to traditional money market funds.

傳統資產管理機構日益推出代幣化國債產品,為鏈上政府債券市場帶來更深的流動性。退休基金、保險公司及企業財庫開始分配部分現金管理組合至可產生收益的穩定幣或代幣化國債,視其為傳統貨幣市場基金的高效替代品。

DeFi protocols integrate tokenized Treasuries as core collateral assets, creating on-chain yield curves and fixed-income markets that rival traditional bond markets in sophistication while offering 24/7 settlement and global accessibility. This integration effectively extends U.S. Treasury market infrastructure to a global, digital-native user base.

去中心化金融(DeFi)協議將代幣化國債整合為核心抵押資產,於鏈上建立收益曲線及固定收益市場,不僅與傳統債券市場的複雜程度相媲美,更提供全年無休結算與全球化可及性。這種整合實質上將美國國債市場基礎設施延伸至全球的數位原生用戶群。

In this scenario, stablecoin supply could grow from current levels around $150-180 billion to potentially $500 billion or more by 2028-2030, with the majority backed by Treasuries. This would make the stablecoin sector comparable in size to some of the largest money market fund complexes, representing perhaps 5-8% of outstanding Treasury bills. Market impacts would remain manageable because growth occurs gradually and within a clear regulatory framework that provides transparency and confidence.

在這種情境下,穩定幣供應量有機會從目前約1,500~1,800億美元,於2028至2030年成長至5,000億美元以上,其中多數將以美國國債作為支持。屆時穩定幣規模將可與全球最大貨幣市場基金規模比擬,約占在外流通國庫券5~8%。由於增長是循序漸進並在清晰監管架構下進行,市場影響仍在可控範圍,亦具備透明度與信心基礎。

Indicators to watch for this scenario:

- Passage of comprehensive federal stablecoin legislation in the U.S. or full implementation of MiCA in the EU with broad compliance

- Major banks receiving regulatory approval to issue stablecoins or announce tokenized Treasury products

- Federal Reserve research papers or speeches explicitly discussing stablecoins as monetary system components

- Growth in tokenized Treasury market size exceeding $50-100 billion, indicating institutional adoption

- Stable or compressing spreads between stablecoin Treasury holdings yields and traditional money market fund yields, suggesting maturing market structure

此情境觀察指標:

- 美國通過全面性聯邦穩定幣立法,或歐盟MiCA法規全面落實並廣泛遵循

- 主要銀行獲監管批准發行穩定幣或宣布推出代幣化國債產品

- 聯準會相關研究報告或演講明確將穩定幣視為貨幣體系組成部分

- 代幣化國債市場規模成長至500~1,000億美元以上,顯示機構級採用

- 穩定幣國債持有收益率與傳統貨幣市場基金利差趨穩甚至縮小,顯示市場結構成熟

Scenario 2: Regulatory Clampdown and Fragmentation

情境二:監管打壓與市場分裂

In this scenario, regulators conclude that stablecoins pose unacceptable risks to financial stability and monetary sovereignty, triggering restrictive regulatory responses that fragment the market and force structural changes.

在此情境下,監管機構認定穩定幣對金融穩定與貨幣主權構成不可接受的風險,因而引發嚴格監管措施,導致市場分裂並迫使結構性改變。