Bitcoin's のアイデンティティ危機は終わった。何年もの間、機関投資家はBTCをデジタルゴールドとして扱い、価値保存のためにコールドウォレットで眠らせ、ゆっくりと値上がりを待つだけで、収益を一切生まない受動的資産として位置付けてきた。

しかし2025年、このナラティブは根本的に変化した。ビットコインは、もはや不活性な資本ではなく、オンチェーンのデプロイ戦略、構造化されたレンディング枠組み、機関投資家向け財務管理を通じて、意味のある利回りを生み出す「生産的インフラ」として捉えられつつある。

この変化をもたらしたのは投機的熱狂ではない。インフラの成熟だ。規制の明確化、機関投資家向けカストディソリューション、コンプライアンス対応の利回りプロトコルが収束し、企業財務部門、資産運用会社、政府系ファンドがビットコイン保有分を、セキュリティやコンプライアンスを損なうことなく収益化戦略へ投入できる仕組みを解放した。これはビットコインの「第二幕」であり、アクセスと蓄積のフェーズから、資本を積極的に運用するフェーズへの移行を意味する。

なぜ今なのか。ビットコインETFはアクセスの問題を解決した。2025年第3四半期までに、現物ビットコインETFには307億ドル超の純流入が集まり、BTCは伝統的ポートフォリオにとって「当たり前の資産クラス」に変わった。しかし、パッシブなエクスポージャーだけでは機会費用の問題は解決しない。すでに2,000億ドル超のBTCが機関投資家に保有されている状況で、数億ドル単位のビットコインを抱える機関は、他の財務資産と同等のリターンを求める圧力にさらされている。利回り運用は次のフロンティアであり、それを支えるインフラはついに実用段階に入った。

機関投資家がビットコイン利回りを求める理由

コーポレートファイナンスは単純な原則で動いている。「資本は働かせなければならない」。ポートフォリオマネージャーは資産をローテーションし、ポジションをヘッジし、デュレーションを最適化し、可能な限り利回りを抽出する。にもかかわらず、多くの機関保有ビットコインは完全に遊休状態で、年10〜50ベーシスポイントにも及ぶカストディコストを発生させながら、一切の収益を生んでいない。

ここにパラドックスがある。調査データでは、機関投資家の83%が2025年に暗号資産の配分を増やす計画を持つ一方で、その大半は保有分を生産的に運用する仕組みを欠いている。4〜5%の利回りを生むマネーマーケットファンドや、予測可能なリターンをもたらす短期債に慣れた財務担当者にとって、コールドストレージで眠るビットコインは、たとえ価格上昇の可能性があっても「無利息口座」に資本を駐車しているのと同じ感覚だ。

この機会費用は、もはや看過できない水準になりつつある。ある財務責任者はこう語る。「ビットコインをカストディしているだけなら、そのコストとして10〜50ベーシスポイントを失っている。その分をゼロにしたいのは当然だ」。プレッシャーの源泉はリターン最大化だけではない。ポートフォリオ効率、競争上のポジショニング、そしてビットコインを投機的な準備資産ではなく、ワーキングキャピタルとして機能させ得ることを示す責任がある。

受動的保有は、複数の方向から挑戦を受けている。第一に、規制の明確化が主要な障壁を取り除いた。2025年のSECスタッフ会計速報121号の撤廃により、銀行が顧客の暗号資産を保有する際のバランスシート上のインセンティブが改善され、CLARITY法のような枠組みがカストディ業務に法的な確実性を与えた。第二に、機関投資家向けインフラが成熟した。カストディプロバイダーは7,500万〜3億2,000万ドル規模の保険を提供し、マルチパーティ計算(MPC)によるセキュリティや、受託者責任に耐えうるコンプライアンス体制を備えている。

第三に、競争が激化している。これまでビットコイン積み上げ戦略で先行してきた企業財務部門は、保有分から追加的な価値をどう抽出するかを検討しはじめている。Bernsteinのアナリストは、今後5年間で世界の上場企業がビットコインに割り当てる資金は現在の約800億ドルから最大3,300億ドルに達し得ると予測する。採用が拡大するにつれ、利回り運用をマスターした機関は、単に保有するだけの機関に対して戦略的優位性を手にする。

供給サイドと利回り機会

ビットコインのアーキテクチャは、独特の利回りダイナミクスを生む。ステーキング報酬を得るバリデータが存在するProof of Stakeチェーンとは異なり、ビットコインのProof of Workモデルにはネイティブな利回りメカニズムがない。ネットワークのセキュリティはステーキングではなくマイニングから来ており、半減期によって新規供給は段階的に減少していく。2024年4月の半減期でブロック報酬は3.125 BTCに減り、今後6年間で約70万BTCが新たに供給される見込みだ。

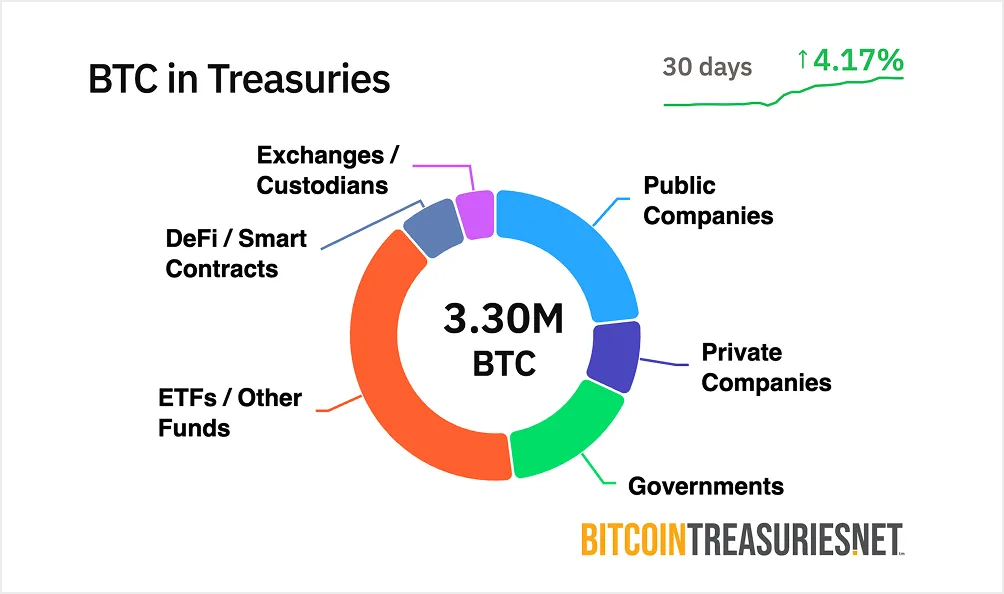

この希少性モデルは、価値保存手段としてのビットコインの強みだ。その一方で、実務家が「アイドルBTC問題」と呼ぶ現象を生み出す。2,000億ドル超のビットコインが機関の財務に滞留し、一切の収益を生んでいない。時価総額1.3兆ドルの資産が巨大なロックドキャピタルになっているにもかかわらず、利回り戦略として生産的に運用されているのは2%未満だと業界では見積もられている。

機会は構造的だ。ビットコインのボラティリティは大きく低下しており、2023年比で75%減少し、シャープレシオ0.96は今や金に匹敵する水準となった。この成熟により、ビットコインはこれまで国債や社債に限られていた「債券型」の戦略にも適合し始めている。機関投資家はBTCをハイベータな投機ではなく、そのリスクプロファイルに見合うリターンを生むべき正当な財務資産として見るようになっている。

Bitcoin DeFiのロック総額(TVL)は過去12ヶ月で228%急増しており、オンチェーン利回りのためのインフラ拡充を示している。しかし、その多くはEthereumやサイドチェーン上のラップドビットコインであり、ネイティブなデプロイではない。ビットコインの市場規模と利回りインフラの間にあるギャップは、大きな機会を生み出している。コンポーザブルなプロトコルが成熟し、規制フレームワークが固まるにつれ、機関投資家向けビットコイン利回り市場は次のサイクルで数千億ドル規模に達する可能性がある。

機関投資家のデプロイメント枠組みとオンチェーンインフラ

ビットコインを利回り目的でデプロイするには、単なるレンディングプロトコル以上のものが必要だ。機関投資家は、カストディソリューション、監査可能なトレイル、規制コンプライアンス、そして受託者責任に耐える透明なリスクフレームワークを求める。こうした要件を支えるインフラは、2025年にかけて劇的に進化した。

オンチェーンレンディングは、最もストレートなデプロイ手段だ。約440億ドルのTVLを持つAaveのようなオーバーコラテラル型レンディングプロトコルは、機関投資家がビットコイン、通常はラップドBTC(wBTC)を預け入れ、借り手から変動金利の利回りを得ることを可能にする。金利は利用率に応じて3〜7%のレンジで変動し、借入需要が高まる局面ではより高いレートとなる。

メカニズム自体は比較的シンプルだ。企業財務部門がwBTCをレンディングプールに預け入れる。流動性を必要とする借り手は、ローン価値の150〜200%に相当する担保を差し入れる。スマートコントラクトは担保不足のポジションを自動清算し、貸し手を保護する。機関投資家は借り手が支払う利息をビットコイン建てで受け取り、Morphoのようなプロトコルはこのモデルを最適化し、ゼロ手数料の借入を提供しつつ、ボールト戦略によって貸し手の利回りを最大化することで63億ドル超のTVLを確保している。

利回りを生むトレジャリーは、より構造化されたアプローチだ。プロトコルと直接対話する代わりに、機関投資家は企業財務向けに設計されたマネージド利回り商品を通じてビットコインをデプロイできる。Coinbase Asset Managementは2025年5月にCoinbase Bitcoin Yield Fundを立ち上げ、米国外の機関投資家向けに、ビットコイン建てで年率4〜8%のネットリターンを目標としている。このファンドが戦略実行、リスク管理、コンプライアンスといったオペレーションの複雑さをすべて担い、投資家はBTCでのサブスクライブと償還を行うだけでよい。

こうした商品は、大きな転換点を示している。以前は、企業財務部門が利回りを得るには社内に暗号資産の専門知識が必要だった。いまや運用会社が、ビットコインデプロイメントを、なじみのあるファンド構造、四半期レポーティング、受託者監督を備えた「ターンキーソリューション」としてパッケージ化している。ファンドは、すべての手数料と費用控除後のリターンを目標としており、パフォーマンスは透明で、伝統的な債券商品との比較も容易だ。

固定利回りモデルと変動利回りモデルの違いは、リスクを考えるうえで重要である。 management。変動利回り戦略では、リターンが市場環境に連動します。需要が高いときには貸出金利が上昇し、閑散期には低下します。これに対して固定利回り商品は、ストラクチャードノートやデリバティブ戦略を通じて、利用率に依存しないあらかじめ決められたリターンを提供します。Fixed structures often use covered call writing or basis trading により予測可能なインカムストリームを生み出しますが、ビットコインが大きく値上がりした場合のアップサイドは通常、上限が設けられます。

これらの戦略を支えるインフラは、ますます高度になっています。BitGo、Anchorage Digital、BNY Mellon のようなカストディ事業者は現在、マルチパーティ計算によるセキュリティ、規制遵守、保険カバーを備えた機関投資家向けソリューションを提供しています。これらのカストディアンは、ハードウェアセキュリティモジュールや分散鍵管理といった革新により、2022年以降の成功した侵害事例を80%削減しました。

コンプライアンスと監査要件は、もはや後回しにはされていません。主要なプロトコルは EU の MiCA など世界的な報告基準と統合し、機関投資家が進化する規制要件を満たせるようにしています。四半期ごとの監査では準備金証明が公開され、ガバナンスフレームワークはマルチシグ DAO を用いてプロトコルパラメータを管理し、トランザクションの透明性により担保状況をリアルタイムでモニタリングできます。

実世界での導入は急速にスケールしています。MicroStrategy(現在の Strategy)がビットコインのトレジャリー蓄積を先駆けて行った一方で、他の企業はより積極的な運用へと向かっています。Jiuzi Holdings は10億ドル規模のビットコイン・トレジャリープログラムを発表し、その中で利回り戦略をトレジャリーマネジメントの枠組みに明示的に組み込んでいます。GameStop が 2025年3月に、転換社債の発行を通じてビットコインを準備資産に加えると発表したことは、小売業者でさえストラクチャードなビットコインエクスポージャーを模索していることを示しています。

蓄積から運用へのシフトは、Strategy の進化に最も顕著に表れています。同社は 2025年7月時点で 628,000 BTC 超を保有しており、世界最大の企業ビットコイン保有者となっています。Strategy の中核となるプレイブックは依然として資本調達を通じた取得ですが、同社は利回りメカニズムの検討を開始しています。2027年までに 840億ドルの資本調達を目標とする「42/42」計画では、同社の巨額保有分に対してリターンを生み出し得る運用戦略がますます想定されています。

利回り手法と戦略タイプ

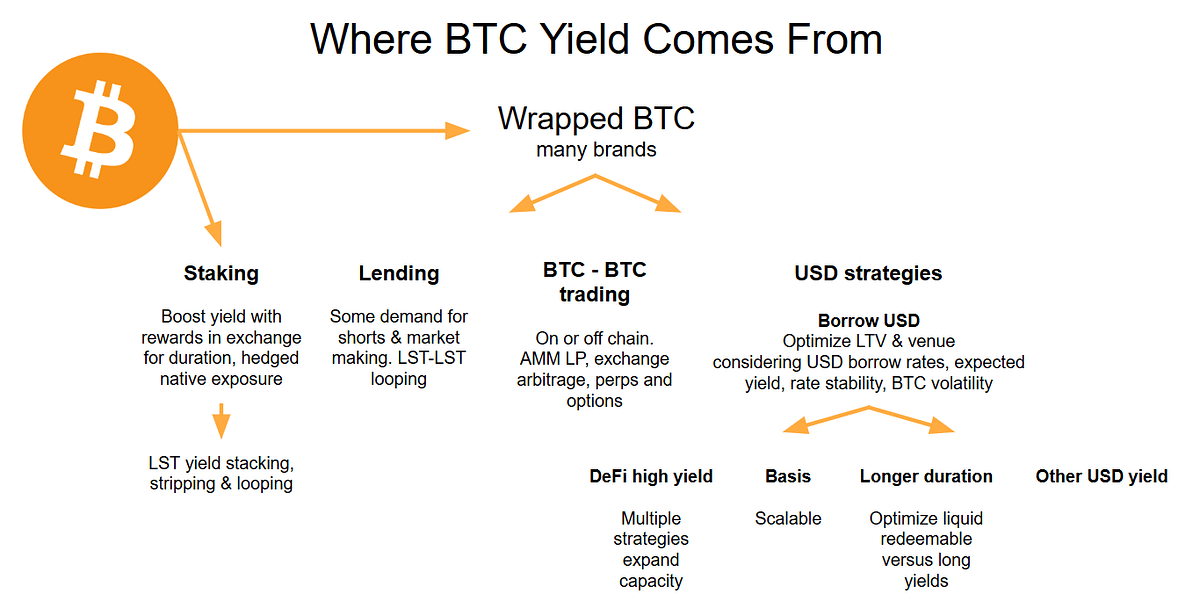

ビットコイン利回りを生み出すメカニズムは、いくつかの明確なカテゴリーに分類され、それぞれ異なるリスクプロファイル、オペレーション要件、リターン特性を持ちます。

マーケット・ニュートラル戦略は、ビットコイン価格への方向性エクスポージャーを取らずに利回りを生み出します。Basis trading involves buying spot Bitcoin and simultaneously shorting futures contracts、つまり現物ビットコインを買う一方で同時に先物をショートし、両ポジション間の価格差を捕捉します。安定した市場環境では、このスプレッドは通常、年率 5〜10% 程度の利回りをもたらします。この戦略はデルタ・ニュートラルであり、ビットコインが上昇しても下落しても、現物と先物価格の収束から利益を得ます。

実行には、現物市場と先物取引所の両方へのアクセスが必要です。例えば、ある機関投資家はカストディアンを通じて 1,000 万ドル分の現物ビットコインを購入し、CME や Binance のようなプラットフォームで同等ノーション額の先物をショートします。先物の満期が近づくにつれて、その価格は現物に収束し、機関投資家はこのベーシスを利益として確保します。Automated bots optimize rate capture 一方で、ボラティリティが高い局面ではスリッページを避けるために実行スピードが極めて重要です。

資金調達レート・アービトラージは類似の仕組みですが、期日付き先物ではなく永久スワップを利用します。In bull markets, perpetual swap longs pay shorts a funding rate、強気相場ではパーペチュアルスワップのロングがショートに対して資金調達レートを支払うことが多く、その水準は年率 2〜5% に達することがあります。機関投資家は現物ビットコインをロングしつつ、パーペチュアルコントラクトをショートすることで、定期的なファンディング支払いを受け取ります。この戦略には継続的なモニタリングが必要であり、弱気局面ではファンディングレートがマイナスに転じ、利益を生んでいた取引が損失要因となる可能性があります。

カバードコール戦略は、機関投資家のビットコイン保有において最も広く採用されている利回りメカニズムです。The approach involves holding Bitcoin while selling call options against those holdings、つまりビットコインを保有しながらその保有分に対してコールオプションを売却し、BTC がストライク価格を超えて上昇した場合のアップサイドを上限とする代わりにプレミアム収入を得ます。Bitcoin's historically high implied volatility - often exceeding 46% により、ビットコインのオプションプレミアムは伝統的資産と比べて大きくなる傾向があります。

メカニクスは比較的単純です。100 BTC を保有するトレジャリーが、現行価格の 10% 上にストライクを設定し、満期30日のコールオプションを売却するとします。ビットコインが満期までストライクを下回れば、機関投資家はプレミアムをそのまま獲得し、その水準は通常ポジション価値の月あたり 2〜3% 程度です。ビットコインがストライクを上回る水準まで上昇すれば、ポジションはコールされますが、機関投資家はストライク価格に加え受け取ったプレミアム分の利益を確保できます。BlackRock filed for the iShares Bitcoin Premium ETF in September 2025、これはビットコイン利回り獲得のためのカバードコール戦略に対するメインストリーム機関投資家の関心を示しています。

デメリットは機会費用です。During strong bull markets, covered call strategies historically lag their underlying asset、強いブルマーケットでは、ストライク価格でアップサイドが制限されるため、カバードコール戦略は基礎資産のパフォーマンスを下回ってきました。例えば、2024年初頭に 100,000 ドルのストライクでコールを売却したビットコイン保有者は、BTC がその水準を大きく上回って上昇した際の相当な値上がり益を取り逃がしたことになります。より保守的な実装では、現行価格より 5〜15% 上のアウト・オブ・ザ・マネー・ストライクを用いることで、一定のアップサイドエクスポージャーを維持しつつ有意なプレミアム収入を得ることを目指します。

現在では、カバードコール戦略をパッケージ化した ETF 商品が複数登場しており、個人投資家と機関投資家の双方がアクセスできるようになっています。The NEOS Bitcoin High Income ETF launched in October 2024, delivering a 22% dividend yield はビットコインエクスポージャーに対するレイヤードなコール売りを通じて 22% の配当利回りを提供しています。The Roundhill Bitcoin Covered Call Strategy ETF seeks 4-8% net returns は、シンセティックなロングポジションと週次のコール売りを組み合わせて、4〜8% のネットリターンを目標としています。これらの商品は、高度なオプション戦略が制度的なスケールで運用できることを示しています。

ストラクチャードレンディングおよびボールト戦略は、より複雑な実装を表します。Ribbon Finance のような DeFi オプションボールトは、カバードコールの実行を自動化し、dynamically selecting strike prices based on volatility and optimizing returns、ボラティリティに基づきストライクを動的に選択してリターンを最適化し、アルゴリズムによる管理を行います。Yields range from 5-10% annually、利回りは年率 5〜10% のレンジで推移し、プロトコル側がストライクの選定、ロール管理、プレミアム回収などの運用上の複雑さをすべて処理します。

プット売りボールトは逆方向に機能します。機関投資家がビットコインのプットオプションを売却し、プレミアムを受け取る一方で、オプションが行使された場合にはより低いストライク価格で BTC を買い取る義務を負います。This strategy generates 4-8% yields が、調整局面において割安な水準でビットコインを取得できる可能性があります。リスクとしては、機関投資家がストライク価格に相当するステーブルコイン担保を維持しなければならず、本来他で運用できたはずの資本が拘束される点が挙げられます。

CeFi プラットフォームを通じたビットコイン担保レンディングは、異なるリスクプロファイルを持つ、より保守的な利回りを提供します。Regulated platforms like BitGo and Fidelity Digital Assets now offer 2-5% annual yields、BitGo や Fidelity Digital Assets のような規制されたプラットフォームは現在、審査済みの機関投資家に対するビットコイン貸付で年率 2〜5% の利回りを提供しています。これらのプラットフォームは、2022年の CeFi 崩壊後、より厳格な担保要件、借り手審査、透明性基準を導入し、機関投資家の受託者責任を満たす水準へと再構築されました。

リスクとリターンのトレードオフは本質的です。マーケット・ニュートラル戦略は、低めの利回り(2〜10%)である一方、価格方向へのエクスポージャーは最小限です。カバードコールは高いインカム(5〜15%)を生み出せますが、値上がり益に上限があります。DeFi レンディングは二桁利回りをもたらす可能性がありますが、スマートコントラクトリスクやカウンターパーティリスクが伴います。機関投資家のアロケーターは、自らの投資方針に戦略選択を適合させる必要があります。保守的な年金基金は規制された CeFi レンディングを好み、一方でよりアグレッシブなトレジャリーは DeFi ボールトやデリバティブ戦略へのデプロイを選択し得ます。

インフラ、リスクおよびコンプライアンス上の課題

利回り獲得は、機関投資家が無視できないオペレーション上の複雑さをもたらします。ビットコイン運用を支えるインフラは、カストディ、セキュリティ、コンプライアンス、リスク管理に関する厳格な要件を満たさなければならず、多くのリテール向けプロトコルはこの水準に達していません。

カストディは依然として基盤です。機関投資家は、ビットコインをデプロイすることはできず、またその意思もありません…プロトコルが資産の管理権を放棄したり、秘密鍵を露出したりすることを要求する。 Leading providers use multi-party computation (MPC) technology は、鍵の断片を複数の当事者に分散させ、単一の主体が一方的に資金へアクセスできないようにする。MPC prevents insider theft even if one key fragment is compromised のとおり、完全な鍵を再構成するには複数の独立した当事者の協調が必要なため、たとえひとつの鍵断片が侵害されても内部犯行による盗難を防止できる。

Cold storage, multi-signature wallets, and hardware security modules は、機関投資家向けカストディの中核を成す。コールドウォレットは秘密鍵をオフラインかつインターネットから隔離して保管し、リモート攻撃を防ぐ。マルチシグ承認は、複数の認可された当事者がトランザクションに署名することを要求し、単一障害点を排除する。HSM は耐タンパ性の暗号保護を提供し、物理的な盗難や内部不正から鍵を保護する。

監査可能性と透明性は譲れない要件である。機関投資家は、担保状況、清算リスク、資金フローに対するリアルタイムの可視性を必要とする。Leading protocols publish quarterly proof-of-reserve audits は第三者によって検証され、準備金が発行残高と一致していることを保証する。すべての発行(ミント)、焼却(バーン)、取引データはオンチェーンで公開検証可能であるべきであり、機関投資家は事業者の開示だけに依存せずに、プロトコルの支払能力を独自に検証できるようにする必要がある。

ガバナンス管理は、不正なトランザクションを防ぎ、プロトコルリスクを管理する。Multi-signature DAOs collectively manage parameter changes により、単一の当事者が担保率や清算閾値などの重要な変数を変更できないようにする。機関投資家は、パラメータ変更に対するタイムロック、緊急停止メカニズム、セキュリティインシデント対応のための明確なエスカレーション手順を備えた正式なガバナンスフレームワークを求めている。

規制遵守は、枠組みの進化とともにますます複雑になっている。Markets in Crypto-Assets Regulation (MiCA) in the EU and Securities and Exchange Commission guidance in the U.S. は、カストディ基準、マネーロンダリング対策要件、報告義務を定めている。ニューヨーク州金融サービス局は暗号資産カストディに関する具体的な基準を示しており、機関投資家向けサービスを提供する前に、機関はこれらの規制枠組みへの準拠を実証することが求められる。

ビットコイン利回りの運用に伴うリスクは大きく、積極的な管理が不可欠である。再担保設定(リハイポセケーション)—顧客資産を複数回貸し出すこと—は、集中型レンディングにおいて依然として懸念事項だ。機関は、カストディアンが 1:1 の準備金を維持し、ストレス環境下でシステミックリスクを生みうる開示されていない再担保設定に関与していないことを検証しなければならない。

カウンターパーティのデフォルトは最も明白なリスクである。レンディングプラットフォームが支払い不能に陥った場合、担保の取り決めにかかわらず、預金者はビットコインの一部または全部を失う可能性がある。The 2024 surge in crypto hacking incidents, with approximately $2.2 billion stolen は、高度なプラットフォームであっても依然として脆弱であることを示している。機関は、複数のカストディアンやプロトコルに分散し、壊滅的損失につながりうる集中リスクを回避すべきである。

資産と負債の流動性ミスマッチは、ボラティリティの高い局面でストレスを生みうる。もし機関が即時償還可能なレンディングプロトコルにビットコインを預け入れた一方で、そのプロトコルが資産を固定期間で貸し出している場合、デュレーション・ミスマッチが生じる。市場混乱時には、プロトコルが償還請求に応じるだけの流動性を確保できない可能性があり、償還遅延や停止を余儀なくされる。Institutions should clarify redemption terms upfront and maintain liquid reserves により、オペレーション上のニーズに対応できるようにすべきである。

ラップドビットコインとネイティブビットコインの違いは、リスク評価において重要である。Wrapped Bitcoin (wBTC) represents the vast majority of Bitcoin in DeFi であり、BitGo のようなカストディアンが保有する実際のビットコインに 1:1 で裏付けられた、Ethereum 上の ERC-20 トークンとして機能する。Over $10 billion in wBTC circulates across Ethereum-based protocols により、BTC 保有者は Ethereum 上でレンディング、トレーディング、イールドファーミングにアクセスできる。

The wBTC model relies on a federated custody structure において、複数の機関がマーチャントおよびカストディアンとして機能する。quarterly audits verify 1:1 backing とはいえ、機関はカストディアンが準備金を不適切に運用したり、支払い不能に陥ったりしないことを信頼しなければならない。この中央集権性は、Rootstock や Lightning Network のようなレイヤー 2 ソリューション上のネイティブビットコインであれば回避できる可能性があるが、それらのエコシステムは利回りインフラがはるかに未成熟である。

スマートコントラクトリスクは、あらゆる DeFi 運用に適用される。十分な監査を受けたプロトコルでも、悪意ある攻撃者に悪用されうる脆弱性を含みうる。Institutions should prioritize protocols with multiple independent audits from firms like OpenZeppelin, Spearbit, and Cantina、6 桁から 7 桁規模の報奨金を提供するバグバウンティプログラム、ストレス環境下での実績ある運用履歴を持つプロトコルを優先すべきである。

コンプライアンスおよび監査フレームワークは、機関のリスク委員会を満足させなければならない。実現利回りと想定利回りの差異は透明である必要がある—一部のプロトコルは、実際のキャッシュ利回りではなくトークン報酬を含めた高い APY を宣伝している。スリッページ、取引コスト、ガス代は、高頻度戦略においてリターンを大きく侵食しうる。逆境相場における最大損失を示すドローダウン分析は、機関がワーストケースシナリオを理解するのに役立つ。

The institutional crypto custody market is projected to grow at 22% CAGR to $6.03 billion by 2030 と予測されており、コンプライアンス認証されたソリューションへの需要が成長要因となっている。しかし、その成長は、インフラプロバイダーがこれらのリスクとコンプライアンスの課題をスケールに応じて解決できるかどうかにかかっている。

What This Means for Corporate Treasuries and Institutional Allocation

パッシブ保有からアクティブ運用へのシフトは、企業の財務担当者がビットコインエクスポージャーを捉える方法を根本的に変える。BTC を単なるインフレヘッジや投機的値上がり狙いとして見るのではなく、他の流動性資産と同等のリターンを生み出す運転資本として扱うことが可能になる。

5 億ドルの現金同等物を管理する企業の財務担当者を考えてみよう。従来、この資本は 4~5% の利回りを生むマネーマーケットファンドや、予測可能なリターンをもたらす短期コマーシャルペーパーに置かれてきた。ここで、そのポートフォリオの 10%—5,000 万ドル—をビットコインに配分したとする。ゼロ利回りでは、その BTC はカストディコストを負担しながらも収入を生まない。しかし、年率 4~6% を生む保守的な利回り戦略に投入すれば、そのポジションはビットコインエクスポージャーを維持しつつ、有意な財務収入に貢献する。

The transformation of digital asset treasuries into working capital は、いくつかの戦略的な変化を可能にする。第一に、ビットコインはベンダーとの契約や B2B 決済で機能しうる。グローバルに事業を展開する企業は、サプライヤー契約を BTC 建てで締結し、為替換算コストと決済時間を削減するオンチェーン決済レールを利用できる。ビットコイン準備金から得られる利回りは、運転資本の一部をデジタル資産で保有することによるボラティリティリスクを相殺する。

第二に、財務部門は流動性管理のための担保としてビットコインを利用できる。キャッシュを調達するために BTC を売却してしまうと、課税イベントが発生し、将来の値上がり益を逃す可能性があるが、代わりにビットコインをステーブルコインローンや与信枠の担保として差し入れることができる。Over-collateralized lending allows treasuries to access 50-75% of their Bitcoin's value により、長期的な BTC エクスポージャーを維持しながら、その価値の 50~75% の流動性にアクセスできる。

第三に、利回り運用は資本配分におけるオプショナリティを生み出す。ビットコイン保有から年率 5% を稼ぐ財務部門は、そのリターンを事業投資、自社株買い、あるいは追加のビットコイン取得に再投資できる。複数年にわたる複利効果は、パッシブ保有と比較して総リターンを大きく高める。

心理的な変化も同様に重要である。ビットコインを投機的な資産と見なしていた CFO や取締役会は、今やそれを生産的な資産と見始めている。Survey data showing 83% of institutional investors planning increased crypto allocations は、ビットコインが「一攫千金」ではなく受託者責任を満たしうる存在になりつつあるという自信の高まりを反映している。利回り運用は、クリプトネイティブな熱狂と、機関投資家のリスク管理要件との間のギャップを埋めるブリッジとなる。

ビットコインが収益を生むようになると、ポートフォリオの行動も変化する。債券や国債に匹敵する利回りを得られるのであれば、財務部門は準備金のより大きな割合を BTC に配分するかもしれない。保守的な 2~3% の配分が、リスク調整後リターンが大きなエクスポージャーを正当化する場合には 5~10% に拡大しうる。Bernstein's projection of $330 billion in corporate Bitcoin allocations by 2030 はこのダイナミクスを前提としており、イールドインフラが成熟するにつれて、ビットコインに対する機関投資家の需要が比例して増加すると想定している。

その含意は、企業の財務部門を超えて、年金基金、財団、政府系ファンドにまで及ぶ。これらの機関は、分散投資、利回りの創出、下方リスクの抑制を厳格に求めるマンデートの下で、数兆ドル規模の資産を運用している。ビットコインの伝統的資産との相関性と、成熟しつつあるイールドインフラの組み合わせにより、ポートフォリオ分散の手段としての魅力が高まりつつある。ファミリーオフィスはすでにポートフォリオの25%を暗号資産に配分しており、コンプライアンスの枠組みが固まるにつれて、より大きな機関投資家の資金も後に続く可能性が高い。

クリプト市場全体の見通しとインプリケーション

ビットコイン利回りのデプロイメントの軌道は、今後3〜5年で暗号資産市場を再形成しうるいくつかの展開を示唆している。

インフラのスケーリングは、最も差し迫った進化である。ビットコイン DeFi のロック総額(TVL)は昨年比で228%成長した が、それでもなおビットコインの時価総額全体から見ればごく一部にすぎない。プロトコルの成熟と機関投資家の採用が加速すれば、オンチェーンにおけるビットコイン TVL は数十億から数千億規模へと拡大しうる。このスケーリングには、ユーザー体験の改善、L2 ソリューション上でのガス代最適化、監査やバグバウンティを通じた継続的なセキュリティ強化が必要となる。

市場が成熟するにつれて、ビットコインベース商品のイールドカーブが出現する可能性がある。現在、利回りは戦略、プロトコル、市場環境によって大きく異なる。時間の経過とともに、機関投資家の資金フローが、3ヶ月物ビットコイン貸出金利、6ヶ月物ベーシストレード利回り、1年物ストラクチャードノートのリターンといった、より予測可能なターム構造を形成しうる。これらのイールドカーブは、プライシングの透明性を提供し、ビットコインを中核的な債券代替資産として用いた、より洗練されたポートフォリオ構築を可能にする。

規制の枠組みも、ビットコイン利回りを特に対象とする形で進化し続けるだろう。現行のガイダンスは主にカストディと現物取引に焦点を当てているが、機関向けイールド商品がスケールするにつれ、貸出、デリバティブ、ストラクチャードプロダクトに関する固有の枠組みが導入される可能性が高い。明確な規制は不確実性を取り除くことで採用を加速させうる一方、過度に制限的なルールは、活動をオフショアあるいは透明性の低い構造へと追いやるリスクもある。

ビットコインそのものに関するナラティブも、価値の保存手段から生産的な担保資産へとシフトしつつある。Bitcoin is infrastructure, not digital gold はこの転換を捉えている。BTC を貴金属のような静的資産と比較するのではなく、機関投資家はますます、貸出、決済、担保化、利回り創出を支える多用途なインフラとしてビットコインを見るようになっている。この捉え方は、「資本市場において資産はリターンを生み出すべきものであり、単に値上がりを待つ存在ではない」という実際の機能に、より適合している。

DeFi と伝統的金融(TradFi)との関係において、ビットコイン利回りは最も信頼性の高いブリッジを生み出す。機関投資家のアロケーターは、担保、金利、リスクプレミアムを理解している。彼らは、よく分からないプロトコル上でガバナンストークンをファーミングするよりも、5%でビットコインを貸し出す方がはるかに安心できる。ビットコイン DeFi インフラが監査証跡、コンプライアンスフレームワーク、規制されたカストディといった TradFi の基準を採用するにつれて、オンチェーン金融と伝統的金融の区別はあまり意味を持たなくなる。資本は、リスク調整後リターンが最も高いところへ流れるだけだ。

資本市場には、ビットコイン建て、あるいはオンチェーンで決済される新たな金融商品が登場しうる。企業は BTC で償還される転換社債を発行するかもしれない。各国政府はビットコイン建ての短期国債を提供するかもしれない。国際貿易の決済システムが、ビットコインレールへと移行する可能性もある。これらの発展はいずれも、ビットコインが単なる資産ではなく「マネー」として機能するに足る流動性と生産性を備えるよう、イールドインフラが整備されることを前提としている。

注目すべき主要なシグナルには、大規模な機関向け利回りプログラムのローンチが含まれる。大手年金基金がビットコイン利回り戦略を発表すれば、そのアプローチが他の何百という機関投資家にとって正当化される。政府系ファンドがビットコイン準備資産をストラクチャードイールド商品にデプロイすれば、最も保守的な資本プールでさえ BTC 利回りを許容可能とみなしていることを示す。こうしたマイルストーンが1つ達成されるごとに、次の波の機関採用に対する障壁は下がっていく。

ビットコインベースのプロトコルにおけるオンチェーン TVL は、デプロイメント活動の直接的な指標となる。現在の推計では、生産的な資本として運用されているビットコインは全体の2%未満にすぎない。これが5〜10%へと伸びれば、新規デプロイメントで数千億ドル規模となり、インフラの改善、利回り競争によるスプレッド縮小、ビットコインを正当なトレジャリー資産として受け入れる風潮の広がりを引き起こす可能性が高い。

利回りの分類を明確にする規制フレームワークは、大きな不確実性を取り除くだろう。ビットコインの貸出は証券取引に該当するのか。カバードコール戦略は特定の登録義務を引き起こすのか。国境をまたぐビットコイン利回り商品は、源泉徴収税をどのように扱うべきか。これらの問いへの答えが、機関投資家による利回りデプロイメントがニッチのままにとどまるのか、標準的な慣行となるのかを左右する。

ビットコイン価格のボラティリティと利回り創出との関係は、興味深いダイナミクスを生む。高いボラティリティはオプションプレミアムを押し上げ、カバードコール戦略の収益性を高める。一方で、低いボラティリティは、貸出用の担保としてのビットコインの魅力を高め、借入需要や貸出金利を押し上げる可能性がある。機関投資家にとって最適な利回り環境となるボラティリティ水準は、価格上昇にとって最適な水準とは異なるかもしれず、最大の値上がり益を求めるホルダーと、インカム最適化を図る利回り投資家との間に緊張関係を生みうる。

最後に

ビットコインが、遊休の準備資産から生産的な資本インフラへと変貌しつつあることは、暗号資産の機関採用ストーリーの中でも、最も重要な展開の一つである。アクセスはフェーズ1であり、ETF と規制されたカストディによって解決された。利回りはフェーズ2であり、それを支えるインフラはすでに稼働している。

機関投資家のアロケーターにとって、その含意は明確だ。ビットコイン保有分を遊ばせておく必要はない。保守的な貸出戦略、市場中立的なデリバティブポジション、ストラクチャードイールド商品などを通じて、伝統的な債券資産に匹敵するリターンを生み出すメカニズムが利用可能になっている。リスクプロファイルは異なり、インフラもまだ若いが、基本的なビルディングブロックはすでに整っている。

企業の財務担当者は、ビットコインを投機的エクスポージャーではなく、運転資本として扱えるようになった。生み出される利回りはカストディコストを相殺し、ポートフォリオを分散させ、資本配分に関するオプショナリティを生む。より多くの企業がデプロイメントの成功事例を示せば、このモデルは産業や地域を超えて広がっていく可能性が高い。

市場参加者は何に注目すべきか。大規模な機関向け利回りプログラムの発表は、メインストリームでの受容を示すシグナルとなる。ビットコインベースのプロトコルにおけるオンチェーン TVL の成長は、実際のデプロイメント活動を示す。貸出、デリバティブ、ストラクチャードプロダクトを巡る規制フレームワークの明確化は、より広範な採用に向けた障壁を取り除く。これらの指標を総合的に見ることで、ビットコイン利回りがニッチ戦略にとどまるのか、標準的な機関投資プラクティスとなるのかを判断できる。

この進化が重要なのは、ビットコインにまつわるナラティブが、その採用の軌道を形作るからである。もし BTC が依然として「デジタルゴールド」—静的で、値上がりはするが本質的には不活性な資産—として捉えられ続けるならば、機関投資家による配分は限定的なままだろう。保守的なポートフォリオは、利回りを生まない資産を大量には保有しない。しかし、ビットコインが予測可能なリスク調整後リターンを生み出せる生産的インフラとして認識されるようになれば、機関投資家が取りうる市場規模は劇的に拡大する。

ビットコインの次の機関採用フェーズは、利回りデプロイメントが持続可能で、スケーラブルで、かつコンプライアンスに適合した形で機能するかどうかにかかっている。初期の証拠は、インフラが急速に成熟しつつあり、機関投資家の需要が強く、規制フレームワークも適法な利回り創出を支援する方向へと進化していることを示している。この転換をいち早くマスターした機関にとって、その戦略的優位性は非常に大きなものとなりうる。