Every day, more than five trillion dollars moves through the global banking system, flowing through networks built decades ago when transactions required telex machines and paper confirmations.

The SWIFT messaging system, launched in 1973, still underpins most international money movement. Payments snake through chains of correspondent banks, each taking hours or days to process transactions that exist only as messages bouncing between proprietary databases. Reconciliation happens in batches. Settlement waits for business hours. The machinery of global finance, for all its sophistication, runs on infrastructure designed for a pre-internet world.

Yet beneath this legacy architecture, something fundamental is changing. Not through flashy public blockchains or viral crypto tokens, but through quiet, methodical work happening inside the world's largest banks. Citigroup CEO Jane Fraser and JPMorgan CEO Jamie Dimon have both placed tokenized deposits and blockchain infrastructure at the center of their institutions' strategic roadmaps for cross-border payments and treasury modernization. These are not experimental side projects. They represent a complete rebuild of how money moves between institutions.

Citi launched its Token Services platform in September 2023, converting institutional clients' deposits into digital tokens for instant cross-border payments available around the clock. JPMorgan followed with its JPMD deposit token in June 2025, deploying it on Coinbase's Base blockchain to offer institutional clients round-the-clock settlement with interest-bearing capabilities. Deutsche Bank joined Partior's blockchain-based settlement platform as a euro and dollar settlement bank in May 2025, expanding a network that already connects some of Asia's largest financial institutions.

The language sounds technical, almost mundane: "tokenized deposits," "distributed ledger technology," "atomic settlement." But the implications reach to the core of how the global financial system functions. This is not another story about tokenized deposits versus stablecoins, or banks trying to compete with crypto. This is about the foundational plumbing of international finance being rebuilt, transaction by transaction, using programmable money on shared ledgers.

The transformation is happening now, with real money moving through real systems. JPMorgan's blockchain platform has processed more than 1.5 trillion dollars in transactions since 2020, with daily volumes exceeding two billion dollars. Citi's payments business processes five trillion dollars across more than 90 countries daily, and the bank is systematically integrating blockchain capabilities into this massive infrastructure.

Unlike the public drama of cryptocurrency markets, this revolution arrives through enterprise agreements, regulatory approvals, and careful integration with existing systems. The contrast is stark: while DeFi protocols promised to disrupt banks from outside, tokenized deposits represent banks rebuilding themselves from within, using the same blockchain technology but deploying it within regulated, permissioned environments designed for institutional scale.

Jane Fraser described Citi's blockchain stack as a potential "killer app" for liquidity management, capturing the strategic imperative driving this transformation. In an era when corporate treasurers expect instant information and real-time control, when supply chains operate globally around the clock, when capital markets demand immediate settlement, the traditional banking infrastructure shows its age. Tokenized deposits offer not just incremental improvement but a fundamental architectural upgrade: always-on availability, programmable automation, atomic settlement, and transparent reconciliation.

The question is not whether this transformation will happen. Major banks have already committed hundreds of millions of dollars and thousands of hours of development work. The question is what this new infrastructure means for the broader financial system, how it will be regulated, what bottlenecks remain, and ultimately, whether SWIFT-era correspondent banking will become as obsolete as telex machines.

This article examines that transformation in depth, moving beyond surface-level comparisons to explore the technical, operational, regulatory, and strategic dimensions of tokenized deposits. By understanding what is actually being built and why it matters, we can glimpse the architecture of 21st-century finance taking shape beneath the surface of today's markets.

What Are Tokenized Deposits, Really?

Before examining how tokenized deposits transform banking infrastructure, we must understand precisely what they are and what distinguishes them from superficially similar instruments. The terminology can confuse even sophisticated market participants, so clarity matters.

A tokenized deposit is a digital representation of a commercial bank liability recorded on a distributed ledger or blockchain. When a corporate client holds a tokenized deposit, they maintain a claim against a licensed depository institution, exactly as they would with a traditional bank account. The critical difference lies not in the legal relationship or the nature of the liability, but in how that liability is represented, transferred, and programmed.

Think of it this way: traditional bank deposits exist as entries in proprietary databases maintained by individual banks. When money moves between accounts at different institutions, messages must flow through networks like SWIFT to instruct corresponding database updates. Multiple parties update their own ledgers independently, creating reconciliation challenges and settlement delays. Tokenized deposits, by contrast, exist as digital tokens on a shared ledger that multiple authorized institutions can access simultaneously. The token itself is the definitive record of the liability, and transfers happen by updating that shared ledger rather than exchanging messages between separate systems.

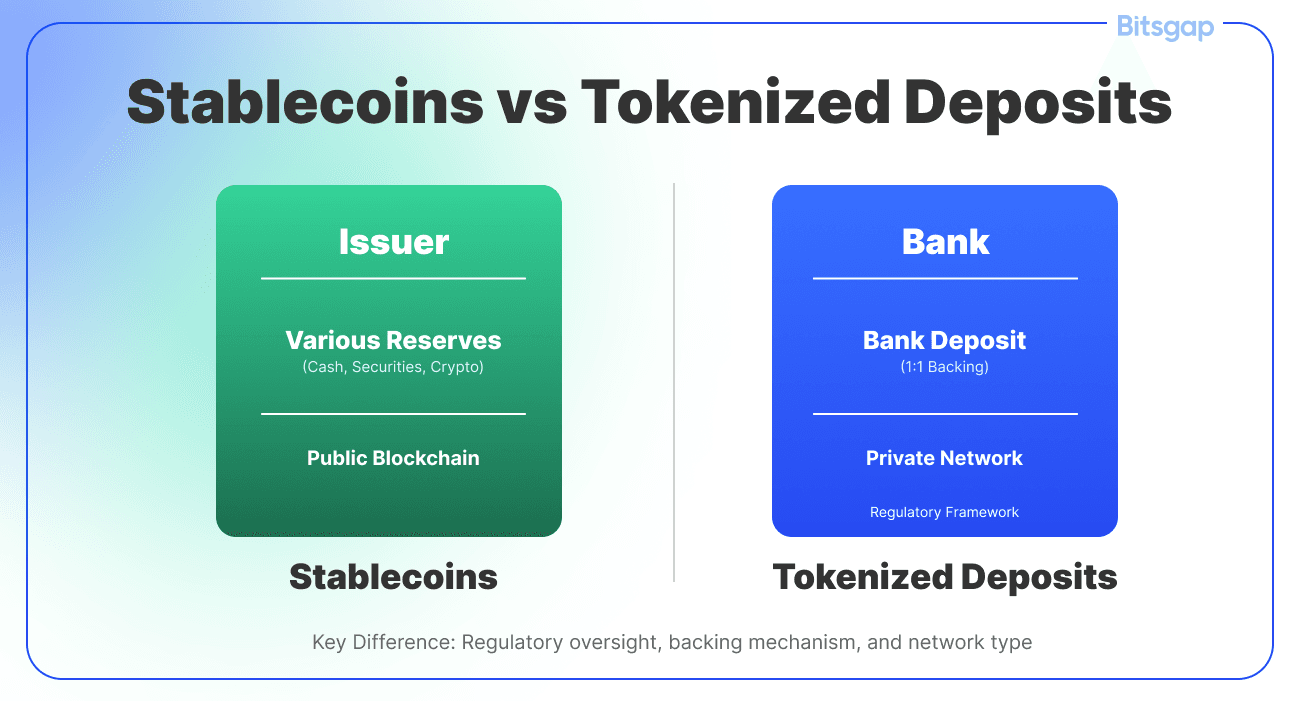

The distinction from stablecoins is crucial, though frequently misunderstood. Stablecoins are typically issued by nonbank entities like Circle or Paxos, pegged to the dollar, and backed by short-term Treasury instruments and cash reserves held separately from the issuer's operating assets. They circulate on public or permissioned blockchains and can transfer peer-to-peer without bank intermediation. The reserves backing stablecoins are held separately from the issuer's balance sheet, often in special purpose vehicles or trust structures designed to protect holders if the issuer fails.

Tokenized deposits work differently. They are issued directly by regulated commercial banks and represent actual deposit liabilities on those banks' balance sheets, making them fundamentally bank money rather than a separate asset class. When you hold a JPMorgan tokenized deposit, you have a direct claim on JPMorgan Chase Bank, N.A., subject to FDIC insurance limits and all the protections afforded to traditional depositors. Each unit of JPMD is fully backed by a corresponding fiat deposit, ensuring parity between on-chain representation and off-chain liability.

This distinction matters enormously for regulation, risk, and functionality. Tokenized deposits fall squarely within existing banking law. They require no new regulatory category because they are simply a different technological implementation of an established instrument: the bank deposit. Banks issuing tokenized deposits already hold banking licenses, submit to comprehensive prudential supervision, maintain capital and liquidity buffers, and face regular examinations by banking regulators. The regulatory clarity is built in.

Central bank digital currencies represent yet another category. CBDCs are liabilities of central banks rather than commercial banks, placing them at the apex of the monetary hierarchy. A retail CBDC would theoretically give every citizen a direct account at the Federal Reserve or European Central Bank, fundamentally restructuring the banking system by disintermediating commercial banks from payment services. A wholesale CBDC would serve only as settlement medium between financial institutions, much like central bank reserves function today but with different technical characteristics.

The Regulated Liability Network concept explored by the New York Federal Reserve and major banks envisions a system supporting both wholesale central bank digital currency and commercial bank deposit tokens on a shared distributed ledger. This design recognizes that monetary systems need both central bank money for final settlement and commercial bank money for credit creation and customer relationships.

Electronic money tokens, regulated under frameworks like the EU's E-Money Directive and now MiCA, occupy adjacent territory. E-money represents prepaid stored value, typically issued by specialized e-money institutions rather than full-service banks. The regulatory requirements differ somewhat from deposit-taking institutions, and the business models tend to focus on payments rather than comprehensive banking relationships.

The ledger architecture for tokenized deposits varies across implementations but shares common features. Most major bank initiatives use permissioned blockchains or distributed ledger technology where only authorized nodes can participate in transaction validation and ledger maintenance. Citi Token Services uses a private, Ethereum-based blockchain, while JPMorgan deployed JPMD on Base, Coinbase's public Ethereum-based blockchain, but limited access through permissioned controls.

The permissioned approach serves multiple purposes. It ensures that only identified, authorized institutions participate in the network, supporting know-your-customer and anti-money-laundering compliance. It allows banks to maintain control over governance, operational procedures, and technical standards. It enables higher transaction throughput than public blockchains typically achieve. And it provides the operational finality and reversibility mechanisms that regulated financial systems require when dealing with errors, fraud, or legal orders.

From the client's perspective, tokenized deposits can operate almost invisibly. Citi designed its Token Services so clients don't need to set up separate wallets or hold tokens in accounts they must manage independently. The tokenization happens at the infrastructure layer, enabling new capabilities without forcing clients to adopt entirely new operational models. A corporate treasurer can instruct a payment through familiar interfaces, and the underlying technology handles the blockchain transactions transparently.

This design philosophy reflects a pragmatic recognition: large corporations and institutional clients care about functionality, not technology for its own sake. They want faster settlement, better liquidity management, programmable automation, and transparent reconciliation. Whether those benefits arrive through distributed ledgers, traditional databases, or some hybrid matters less than whether the system is reliable, cost-effective, and compatible with their existing operations.

The ownership structure reinforces the banking paradigm. Traditional banks maintain custody of the underlying fiat deposits represented by tokens. The tokens themselves are bearer instruments in a technical sense, meaning possession of the cryptographic keys controls the tokens. However, the tokens only exist on permissioned ledgers where all participants are known and authorized. You cannot simply send a tokenized deposit to an anonymous wallet on a public blockchain. The tokens move only within controlled environments between identified counterparties.

This closed-loop architecture addresses one of the fundamental tensions in digital money design: the conflict between programmability and regulatory compliance. Stablecoins on public blockchains can move anywhere, to anyone, at any time. This creates obvious compliance challenges. Tokenized deposits trade some of that permissionless flexibility for regulatory clarity and institutional compatibility. They are programmable money for the regulated financial system rather than for the open internet.

The regulatory classification flows naturally from this structure. Under the GENIUS Act passed by the U.S. Senate in 2025, deposit tokens issued by regulated banks are explicitly recognized as distinct from stablecoins issued by nonbank entities. Banks issuing deposit tokens operate under their existing banking charters and supervision. They need no separate "stablecoin license" because they are not issuing stablecoins; they are simply using new technology to represent traditional deposit liabilities.

Understanding what tokenized deposits are and are not provides the foundation for assessing their impact. They are not a new form of money but a new technology for representing existing money. They are not crypto assets seeking regulatory approval but regulated banking products using blockchain technology. They are not alternatives to the banking system but tools for upgrading it. This distinction shapes everything that follows: how tokenized deposits function, how they are regulated, what advantages they provide, and what challenges they face.

From SWIFT to Smart Contracts: How Money Movement Is Changing

The transformation from legacy payment rails to blockchain-based settlement represents more than a technology upgrade. It fundamentally reimagines how financial institutions coordinate, how transactions achieve finality, and how global liquidity flows.

To understand the magnitude of this change, we must first examine what is being replaced. The SWIFT network, formally the Society for Worldwide Interbank Financial Telecommunication, does not actually move money. It moves messages about money. When a corporation in New York instructs its bank to pay a supplier in Frankfurt, that instruction becomes a SWIFT message transmitted from the sending bank to the receiving bank, possibly passing through intermediary correspondent banks along the way.

Each institution in this chain maintains its own ledger. The SWIFT message instructs them to update those ledgers, debiting one account and crediting another. But the actual movement of funds between banks happens through separate settlement mechanisms: correspondent banking relationships where banks maintain accounts with each other, or through central bank settlement systems like Fedwire in the United States or TARGET2 in Europe.

This architecture introduces multiple friction points. Messages travel separately from settlement. Different institutions update different databases, creating reconciliation requirements. Transactions queue in batches processed during business hours. Cross-border payments may traverse multiple correspondent banks, each adding time, cost, and operational risk. Foreign exchange conversion happens through separate trades that must be coordinated with the underlying payment. Throughout the process, money sits in nostro and vostro accounts, trapped as pre-funded liquidity that cannot be used for other purposes.

The result is a system characterized by latency, opacity, and inefficiency. A traditional cross-border payment might take days to settle, passing through multiple intermediaries in a hub-and-spoke model that adds time and costs at each step. Senders and recipients see limited information about transaction status. Banks tie up enormous amounts of capital in correspondent account balances. Errors require manual intervention to unwind transactions already recorded across multiple separate systems.

None of this would matter if global commerce operated on a nine-to-five schedule in a single time zone with occasional cross-border transactions. But modern business runs continuously across all time zones with supply chains spanning multiple countries and currencies. The disconnect between how commerce operates and how payment systems function creates enormous friction.

Tokenized deposit systems address these limitations through several key innovations, all enabled by the shared ledger architecture. First and most fundamentally, they combine messaging and settlement into a single atomic operation. When a tokenized deposit transfers from one party to another on a shared ledger, both the instruction and the settlement happen simultaneously. There is no separate message instructing a separate settlement. The transfer of the token is the settlement.

This atomic settlement property eliminates many failure modes inherent in message-based systems. You cannot have a situation where the message is received but settlement fails, or where settlement occurs differently than the message instructed. Either the entire transaction succeeds or the entire transaction fails. The shared ledger provides a single source of truth that all parties can see simultaneously.

Citi's Token Services enables institutional clients to complete cross-border payments instantly, around the clock, transforming processes that traditionally took days into transactions completed in minutes. The speed improvement is dramatic but understates the deeper change. More important than speed alone is the combination of speed with finality and transparency. Parties know immediately that settlement has occurred and can see proof on the shared ledger.

JPMorgan's Kinexys Digital Payments system, formerly JPM Coin, provides similar capabilities, processing roughly two billion dollars in daily transactions with near-instant settlement available 24/7. The system supports multiple currencies and integrates with JPMorgan's foreign exchange services to enable on-chain FX settlement. This means a corporate client can instruct a payment in one currency to a counterparty receiving a different currency, and the entire transaction including FX conversion settles atomically on the blockchain.

The operational implications are profound. Consider a multinational corporation managing cash across dozens of subsidiaries in different countries. Under traditional correspondent banking, moving funds between subsidiaries requires navigating multiple payment rails with different operating hours, settlement times, and fees. Liquidity gets trapped in transit and in buffers maintained to ensure subsidiaries can meet local obligations.

With tokenized deposits on a shared ledger, the same corporation can move funds between subsidiaries continuously and instantly. Clients can now pay disbursements to counterparties without the need for prefunding, optimizing liquidity management and reducing transaction costs. A treasury department can maintain a more centralized liquidity pool and deploy funds precisely where and when needed rather than maintaining expensive buffers in each location.

The network effects matter enormously here. JPMorgan processes transactions reaching multiple billions of dollars on some days after introducing programmability to the network. Citi's payments business handles five trillion dollars daily across more than 90 countries, including 11 million instant transactions. As more counterparties join these tokenized networks, the utility increases dramatically. A closed-loop system connecting only a single bank's clients provides limited benefit. A network connecting hundreds of institutions and thousands of corporate clients fundamentally changes liquidity dynamics.

Partior's blockchain-based settlement platform exemplifies this network approach, providing real-time atomic clearing and settlement for participating banks using tokenized commercial bank and central bank liabilities. The platform supports Singapore dollars, U.S. dollars, and euros through founding correspondent banks including DBS, JPMorgan, and Standard Chartered. Deutsche Bank completed its first euro-denominated cross-border payment on Partior in collaboration with DBS, executing the transaction across different financial market infrastructures and demonstrating how blockchain can complement existing systems.

The Partior model is instructive because it shows how tokenized deposits can create shared infrastructure while preserving banks' individual client relationships and regulatory compliance obligations. Financial institutions connect to Partior to make instant interbank cross-border payments 24/7, resolving longstanding inefficiencies including settlement delays, high costs, and limited transaction transparency. Nium became the first fintech to join the Partior network, giving its clients access to 24/7 instant payments without requiring another API integration, demonstrating how the network can extend beyond traditional banks to encompass the broader financial ecosystem.

Smart contracts add another dimension by enabling programmable settlement logic. In traditional systems, conditional payments require manual processes or complex escrow arrangements. Smart contracts allow parties to encode business logic directly into the payment instruction. A payment can be programmed to execute automatically when specified conditions are met: delivery confirmation, regulatory approval, or completion of a related transaction.

Citi's Token Services can optimize trade finance by replacing letters of credit and bank guarantees with smart contracts that automatically release payments once set conditions are met. In pilot testing, international shipping company Maersk transferred tokenized deposits to instantly pay service providers, compacting process times from days to minutes.

The trade finance use case illustrates the power of combining atomicity with programmability. Traditional trade finance involves complex coordination between multiple parties: importer, exporter, banks in different countries, shipping companies, customs authorities, and insurance providers. Documents must be verified, goods must be inspected, title must transfer, and payment must release, all according to carefully sequenced conditions. The coordination happens through a combination of legal agreements, physical documents, and manual verification.

Smart contracts can encode much of this logic and execute it automatically when conditions are verified. The verification itself can happen through oracle services that feed external data onto the blockchain, or through tokenization of the underlying assets and documents. When the bill of lading is tokenized and transferred, confirming receipt of goods, the smart contract can automatically release payment. Settlement happens atomically: the buyer receives the tokenized bill of lading representing ownership of the goods, and the seller receives payment, simultaneously and irreversibly.

This atomic delivery-versus-payment capability extends beyond trade finance. JPMorgan's Kinexys Digital Assets platform launched a Tokenized Collateral Network application enabling the transfer of tokenized ownership interests in money market fund shares as collateral for the first time on blockchain. The system supports frictionless transfer of collateral ownership without the complexity of moving assets through traditional means. The platform has already enabled more than 300 billion dollars in intraday repo transactions by providing short-term borrowing in fixed income through the exchange of cash for tokenized collateral.

The repo market provides a compelling example of how atomic settlement reduces risk. In traditional repo transactions, there is a brief window where one party has transferred securities but not yet received cash, or vice versa. This creates settlement risk that participants must manage through margins, collateral agreements, and credit limits. Atomic settlement on a shared ledger eliminates this risk entirely. Securities and cash transfer simultaneously in an indivisible transaction. Either both sides complete or neither does.

Foreign exchange settlement benefits similarly. Standard Chartered completed euro-denominated cross-border transactions between Hong Kong and Singapore using Partior's global unified ledger infrastructure, becoming the first euro settlement bank to use the platform. FX settlement risk, where a bank might pay out one currency before receiving the other, represents one of the largest intraday risk exposures in financial markets. Payment-versus-payment settlement on blockchain networks can eliminate this risk.

Partior is developing payment-versus-payment capabilities for FX settlement, which offers significant promise in reducing settlement risk especially for non-mainstream currencies. Other planned features include intraday FX swaps, cross-currency repos, and programmable enterprise liquidity management, all building on the atomic settlement foundation.

The technical implementation varies across platforms but shares common patterns. Transactions are submitted to the network, validated according to predefined rules, executed atomically, and recorded on the shared ledger. The validation can check balances, verify signatures, ensure compliance with payment limits or regulatory requirements, and confirm that smart contract conditions are met. The ledger update happens only if all validations pass, ensuring transaction integrity.

Throughput, latency, and finality present important technical considerations. Public blockchains like Ethereum mainnet currently process 15-30 transactions per second with block times of 12-13 seconds, insufficient for global payment systems handling millions of transactions daily. JPMorgan chose Base for JPMD deployment partly because it offers sub-second, sub-cent transactions, dramatically better performance than Ethereum mainnet. Layer 2 scaling solutions and permissioned blockchains can achieve much higher throughput, with some systems processing thousands of transactions per second.

Finality, the point at which a transaction becomes irreversible, varies across blockchain designs. Some systems provide probabilistic finality where the chance of reversal decreases exponentially as more blocks build on top of a transaction. Others provide deterministic finality where transactions are final as soon as they are confirmed. For institutional payments, deterministic finality is strongly preferred because participants need certainty that settlement is complete and cannot be unwound except through deliberate counterparty action.

Security represents another critical dimension. Blockchain systems must protect against both external attacks and internal malfeasance. External attacks might target the network infrastructure, cryptographic keys, or smart contract code. Internal malfeasance could involve node operators, bank employees, or compromised client credentials. Permissioned networks can implement stronger access controls and identity verification than public blockchains, reducing certain attack vectors while introducing different governance challenges around who controls the network and under what rules.

The comparison with public blockchain infrastructure highlights different design philosophies optimized for different use cases. Blockchain eliminates the need for multiple intermediaries by creating direct payment corridors, with transactions often completed in minutes rather than days. Public blockchains prioritize permissionless access, censorship resistance, and decentralized control. Permissioned networks prioritize transaction throughput, regulatory compliance, and operational governance. Neither is inherently superior; they serve different purposes for different users.

For institutional financial services, the permissioned approach currently dominates because it better aligns with regulatory requirements, risk management practices, and business models based on trusted relationships rather than trustless protocols. Public blockchains succeed where openness and censorship resistance provide fundamental value, as in cryptocurrency markets or certain decentralized finance applications. The question is not which is better in absolute terms but which better fits specific use cases and constraints.

As tokenized deposit infrastructure matures, hybrid models may emerge that bridge permissioned and public networks. A corporation might maintain tokenized deposits on a bank's permissioned blockchain for most treasury operations but interact with public DeFi protocols through controlled gateways for specific purposes. Interoperability between networks, discussed in later sections, will determine how fluid such interactions can become.

The trajectory is clear even if the endpoint remains uncertain: money movement is shifting from message-based correspondent banking toward direct settlement on shared ledgers. SWIFT will not disappear overnight, and traditional correspondent banking relationships will persist for many purposes. But the gravitational center of global payments infrastructure is migrating toward tokenized deposits on blockchains that combine instant settlement with programmable logic and 24/7 availability. This represents not just faster legacy systems but a fundamentally different architecture for how financial institutions coordinate and how money moves through the global economy.

The 24/7 Bank: Why Always-On Finance Changes Everything

The transition from batch processing to continuous real-time operation represents one of the most significant operational transformations in modern banking. Yet this shift remains underappreciated, perhaps because the implications extend far beyond technology into organizational culture, risk management, and business models.

Traditional banking operates on business-day schedules with defined cut-off times. Payments received after cut-off wait until the next processing cycle. Cross-border transactions must navigate multiple time zones and local business hours. Securities settlements typically occur T+2 or T+1, creating a gap between trade execution and final settlement. Treasury departments managing global operations maintain buffers to ensure subsidiaries have adequate funds during local business hours, even if that means leaving capital idle overnight or over weekends in one location while other locations face shortages.

This batch-processing model made sense when transactions required manual intervention, when computers were too expensive to run continuously, and when global commerce moved more slowly. None of these constraints remain relevant today. Corporate supply chains operate continuously. Financial markets never truly close, with trading venues open somewhere at all hours. Global corporations need to move money whenever business requires it, not when bank processing schedules permit.

Tokenized deposits enable true 24/7 banking because the shared ledger infrastructure operates continuously and transactions settle immediately regardless of calendar or clock. Partior's 24/7 blockchain network complements and interoperates with real-time local currency payment and RTGS systems, which may not operate continuously. A treasurer in New York can move funds to a subsidiary in Singapore on a Sunday afternoon, instantly and with immediate finality. The transaction does not queue for Monday morning processing or wait for correspondent banks in relevant time zones to open for business.

The operational implications ripple through corporate treasury management in multiple dimensions. First and most obviously, liquidity management becomes dramatically more efficient. Without 24/7 capability, corporations must maintain liquidity buffers in each location to cover potential needs during periods when funds cannot be moved from other locations. With continuous availability, treasury can maintain more centralized pools and deploy funds precisely when and where needed.

Consider a global manufacturer with operations across Asia, Europe, and the Americas. Without real-time global payments, the treasurer might maintain 100 million dollars in aggregate liquidity spread across regional pools to ensure each location can meet payroll, pay suppliers, and handle unexpected needs. With instant 24/7 transfers, the same corporation might operate with 70 million dollars in liquidity, maintaining a smaller central pool and regional buffers, moving funds reactively in response to actual needs rather than proactively maintaining expensive buffers against hypothetical needs.

The 30 million dollars in released liquidity can be deployed more productively: paying down debt, investing in operations, or earning returns in higher-yielding instruments. Over time and across thousands of corporations, this efficiency creates significant value simply by reducing idle capital.

Interest optimization follows naturally. In batch-processing environments, funds moved Friday afternoon might not reach the destination account until Monday, losing two days of potential interest earnings. With instant settlement, funds earn appropriate returns continuously without time lost in transit. For large corporations managing billions in liquidity, even small improvements in interest efficiency accumulate to substantial amounts.

Jane Fraser noted that while banks can offer 24/7 tokenized money, many corporate treasuries aren't ready for always-on operations. This observation highlights a crucial point: technology capabilities outpace organizational readiness. A corporation receiving instant payments on Saturday night must have systems to detect, record, and respond to those transactions. Treasury management systems, enterprise resource planning software, and accounting systems must adapt to continuous rather than batch operations.

The human dimension matters equally. Traditional treasury operations staff work business hours because that's when payments process. Continuous operations raise questions about after-hours monitoring, exception handling, and decision-making. Do corporations need 24/7 treasury operations centers? Can automated systems handle most situations with human oversight available on call? How do organizations balance the efficiency of continuous operations against the human capital costs of staffing around the clock?

Different organizations will answer these questions differently based on their scale, industry, and operational model. A global manufacturing company with continuous production across time zones might embrace 24/7 treasury operations naturally as an extension of existing operational patterns. A professional services firm with more predictable payment patterns might choose to batch transactions for processing during business hours even if the underlying technology supports continuous settlement.

The risk management implications extend beyond operational readiness. Continuous settlement changes the nature of credit risk, market risk, and operational risk in subtle but important ways. Intraday credit risk decreases because settlement happens continuously rather than building up throughout the day to settle in batches. But continuous operations create new vectors for error or fraud that might propagate immediately rather than being caught during batch reconciliation.

Smart contract automation introduces both opportunities and risks. On one hand, automated execution reduces manual errors and ensures consistent application of business logic. On the other hand, programming errors in smart contracts can cause systematic failures affecting many transactions. The May 2010 "flash crash" in U.S. equity markets, triggered by automated trading algorithms, illustrates how automation can create or amplify certain failure modes even as it eliminates others.

Reconciliation and accounting represent another major operational dimension. In batch-processing environments, reconciliation happens at defined intervals when transaction batches complete. Accounting systems record transactions in daily or periodic journals. Citi's Token Services provides automated reconciliation, reducing the manual effort required when different institutions update separate ledgers. The shared ledger provides a single source of truth that all parties can see, eliminating many traditional reconciliation challenges where institutions must compare their separate records to identify and resolve discrepancies.

Yet continuous settlement also means continuous accounting. Rather than recording a day's transactions in a single journal entry, accounting systems must process and record transactions as they occur throughout the day and night. Enterprise resource planning systems must integrate with blockchain payment systems to capture transaction data in real time and update financial records accordingly. The technical integration is solvable, but it requires substantial system upgrades and process redesign.

The 24/7 operational model also affects how banks manage their own balance sheets. Traditional banks plan intraday liquidity based on predictable patterns of payment flows during business hours. Continuous operations mean continuous liquidity needs without the natural breaks that allow rebalancing. Unlike traditional stablecoins, deposit tokens could be covered by deposit insurance in the future as well as interest-bearing, suggesting that banks might pay interest on tokenized deposits. Interest-bearing tokenized deposits would function much like traditional interest-bearing accounts but with continuous accrual and instant availability, further blurring the lines between different bank products.

Collateral management follows similar patterns. JPMorgan's Tokenized Collateral Network enables the transfer of tokenized ownership interests in money market fund shares as collateral, supporting more dynamic collateral management where parties can adjust positions continuously rather than waiting for specific settlement windows. This capability is particularly valuable in repo markets and derivatives trading where collateral requirements fluctuate with market prices and position changes.

For derivatives markets specifically, continuous settlement and collateral management could significantly reduce counterparty risk. Current practice involves posting initial margin and variation margin at defined intervals, creating windows where market movements might exceed margin buffers. Continuous margining and settlement would close those windows, though at the cost of increased operational complexity.

The cultural and organizational implications should not be underestimated. Banking historically operated on routines synchronized with business hours and settlement calendars. Traders, treasury officers, operations staff, and risk managers organized their days around market opens and closes, payment deadlines, and settlement cycles. Moving to continuous operations disrupts these rhythms and requires organizations to rethink how they structure work, distribute responsibilities, and maintain oversight.

Some institutions will embrace this transformation enthusiastically, seeing competitive advantage in superior liquidity management and client service. Others will move reluctantly, pushed by client demands and competitive pressure but struggling with legacy systems and organizational inertia. The pioneers will likely be global institutions already operating across multiple time zones with continuous-operation cultures, while smaller regional banks might maintain more traditional operational patterns for longer.

Client education represents yet another challenge. Corporate treasurers understand batch processing and business-day conventions because they have operated within those constraints for decades. Explaining the benefits of 24/7 settlement, demonstrating how to use new capabilities, and helping clients redesign their own treasury processes to take full advantage all require sustained effort. Fraser's comment about corporate readiness for always-on operations likely reflects this educational and change management challenge as much as technological concerns.

The regulatory implications deserve attention as well. Banking regulations developed when institutions operated during business hours with defined settlement cycles. How do reserve requirements, capital buffers, liquidity coverage ratios, and stress test scenarios adapt to continuous operations? Should regulators expect different operational risk profiles from 24/7 banks? These questions lack definitive answers but will shape how continuous settlement integrates with prudential regulation.

Looking forward, the always-on bank represents not merely a faster version of existing banking but a qualitatively different operational model. The implications extend from technology infrastructure through accounting systems, risk management frameworks, organizational structures, client relationships, and regulatory expectations. Early adopters will discover which changes create competitive advantage and which introduce new challenges. Followers will learn from pioneers' experience but risk falling behind as client expectations shift toward continuous service and instant settlement.

The transformation is irreversible not because the technology compels it but because client needs demand it. Once corporate treasurers experience instant cross-border settlement and continuous liquidity management, they will not willingly return to batch processing and business-hour constraints. The 24/7 bank becomes the new baseline expectation, forcing the entire industry to adapt or risk losing clients to more agile competitors.

Technical Infrastructure and Interoperability

The promise of tokenized deposits depends fundamentally on the technical infrastructure supporting them: the blockchain architectures, smart contract platforms, interoperability layers, and APIs that enable institutions to deploy programmable money at scale. Understanding this infrastructure reveals both the capabilities currently available and the challenges that remain.

Most major tokenized deposit implementations use permissioned distributed ledger technology, though specific choices vary. Citi's Token Services operates on a private, Ethereum-based blockchain, giving the bank full control over network participation and governance while benefiting from Ethereum's mature tooling and development ecosystem. JPMorgan deployed JPMD on Base, Coinbase's public Ethereum layer-2 blockchain, but implemented permissioned access controls so only authorized institutional clients can use the tokens.

The Ethereum Virtual Machine has become something of a standard for smart contract execution even in permissioned environments. Developers familiar with Solidity, the dominant smart contract programming language, can deploy code to Ethereum-based permissioned chains with minimal adaptation. This talent availability and tooling maturity gave Ethereum-derived architectures significant advantages despite the platform's well-known limitations around transaction throughput and fees on public mainnet.

Other enterprise blockchain platforms like Hyperledger Fabric, Corda, and Quorum offer alternative architectures optimized for permissioned use cases. Hyperledger Fabric uses a modular architecture where components for identity management, consensus, and ledger storage can be customized for specific needs. Corda focuses on financial services use cases with built-in support for complex financial agreements and privacy-preserving data sharing. Quorum, developed by JPMorgan and later spun out, extends Ethereum with enterprise features including transaction privacy and permissioned networks.

The choice between platforms involves tradeoffs across multiple dimensions. Ethereum-based systems benefit from extensive developer communities, mature tooling, and interoperability with Ethereum-native applications. Purpose-built enterprise platforms like Hyperledger and Corda offer better privacy controls, higher transaction throughput, and financial-services-specific features but less extensive ecosystems. Public blockchain deployment with permissioned layers, as JPMorgan chose for JPMD, combines aspects of both: leveraging public infrastructure and tooling while maintaining control over access and usage.

Consensus mechanisms vary as well. Public blockchains like Ethereum use proof-of-stake or proof-of-work to achieve decentralized consensus among untrusted validators. Permissioned networks can use simpler and faster consensus algorithms like practical Byzantine fault tolerance variants or Raft because all validators are known and authorized. The consensus choice affects transaction finality, throughput, and resilience but matters less to end users who simply want reliable settlement.

Smart contract capabilities enable the programmable aspects of tokenized deposits. Contracts can encode conditional logic: execute payment only if certain conditions are met, split payments among multiple recipients according to defined formulas, or trigger secondary transactions automatically when primary transactions complete. The power comes from combining these capabilities: a trade finance smart contract might verify delivery confirmation through an oracle service, automatically execute payment from buyer to seller, trigger a secondary payment from seller to shipping company, and update trade documentation, all atomically and automatically.

Security in smart contract development remains challenging. Code vulnerabilities can create exploits that drain funds or disrupt operations. Even well-audited contracts sometimes contain subtle flaws discovered only after deployment. Financial institutions deploying tokenized deposits must invest heavily in code audits, formal verification where practical, and operational safeguards including circuit breakers that can halt activity if anomalies are detected.

Interoperability represents perhaps the greatest technical challenge facing tokenized deposit infrastructure. Each bank's implementation exists on a separate blockchain or private ledger. If you had a separate Citi Coin and a Wells Fargo Coin, there's a good chance they'd use different technologies, creating interoperability challenges for using distributed ledger technology for interbank payments. Transactions within a single institution's blockchain settle efficiently, but moving value between different institutions' systems requires bridges or intermediary layers.

Several approaches to cross-chain interoperability have emerged. Atomic swaps enable direct exchange of tokens between blockchains using cryptographic techniques that ensure either both sides complete or neither does. Wrapped tokens involve locking tokens on one blockchain and minting equivalent tokens on another, with a custodian managing the locked collateral. Cross-chain messaging protocols like Chainlink's Cross-Chain Interoperability Protocol enable blockchains to exchange data and instructions, allowing smart contracts on one chain to trigger actions on another.

Circle's Cross-Chain Transfer Protocol represents another interoperability approach, enabling native USDC to move between supported blockchains without wrapped tokens. While designed for Circle's stablecoin rather than bank-issued tokenized deposits, the protocol demonstrates technical patterns that could apply more broadly. Users burn USDC on the source chain and mint equivalent USDC on the destination chain, with Circle's infrastructure ensuring atomicity and finality.

Partior's approach differs by creating a shared settlement layer that multiple banks use rather than connecting separate bank blockchains. Partior's unified ledger enables real-time atomic clearing and settlement, providing instant liquidity and transparency by using programmable shared infrastructure rather than sequential processing in legacy payment systems. Banks participating in Partior can settle with each other directly on the shared ledger rather than exchanging tokens between separate systems.

The network effects of these different interoperability models vary significantly. Atomic swaps work peer-to-peer but require both parties to be online simultaneously and become complex for multi-party transactions. Wrapped token approaches centralize risk with the custodian managing locked collateral. Cross-chain messaging protocols create dependencies on oracle services and message relay infrastructure. Shared settlement layers like Partior require participants to agree on common governance and technical standards.

For institutional use cases, trust-based interoperability solutions may prove more practical than fully trustless bridges. Banks already maintain correspondent banking relationships backed by legal agreements and credit lines. Extending these relationships to include interoperability between tokenized deposit systems adds technical capabilities without fundamentally changing the trust model. A bank might agree to accept another bank's tokenized deposits at par with minimal friction because existing agreements and capital relationships already support that trust.

API layers provide another critical infrastructure component, enabling existing banking systems to interact with blockchain-based tokenized deposit infrastructure. Citi designed its Token Services for seamless integration with clients' existing systems, avoiding the need for clients to adopt entirely new platforms or interfaces. Clients can instruct payments through familiar banking channels, with the bank's systems translating those instructions into blockchain transactions behind the scenes.

This API approach reflects pragmatic recognition that wholesale replacement of existing corporate treasury systems is unrealistic. Large corporations run complex ERP environments, custom treasury management platforms, and payment processing systems representing decades of investment and configuration. Successful tokenized deposit adoption requires working with this installed base rather than demanding replacement.

Latency in tokenized deposit systems generally falls far below traditional correspondent banking but varies by implementation. Partior carried out end-to-end settlements involving both U.S. and Singapore dollars in under two minutes, dramatically faster than traditional cross-border settlement but still longer than the near-instant settlement possible in single-blockchain environments. The difference reflects interoperability overhead and validation requirements when transactions cross institutional boundaries.

For many institutional use cases, settlement in minutes rather than seconds makes little practical difference. The critical threshold is same-day settlement with sufficient speed that transactions can complete within operational timeframes. Instant settlement provides obvious benefits for time-sensitive situations, but the jump from multi-day to sub-hour settlement captures most of the practical value for treasury management applications.

Throughput represents another important dimension. Base blockchain offers sub-second, sub-cent transactions, providing the performance required for high-volume payment applications. Permissioned enterprise blockchains can achieve even higher throughput because they optimize for that goal without the decentralization constraints of public blockchains. The relevant question is whether throughput meets or exceeds the transaction volumes the institution expects to handle, not whether the blockchain matches payment card network speeds of thousands of transactions per second.

Privacy-preserving technologies address concerns about transaction visibility on shared ledgers. Institutions may hesitate to use shared blockchains where all participants can potentially see all transactions, even if identities are pseudonymous. Zero-knowledge proofs enable proving transaction validity without revealing transaction details. Ring signatures and mixing protocols obscure transaction graphs. Confidential transactions hide amounts while enabling validation that inputs equal outputs.

JPMorgan published a whitepaper demonstrating a proof-of-concept exploring on-chain privacy, identity, and composability, recognizing these as major themes for continued blockchain evolution in institutional contexts. Enhanced privacy measures are crucial for enabling broader adoption without compromising commercial confidentiality or exposing competitive information.

The governance of blockchain infrastructure matters enormously for institutional adoption. Who controls the network? Who can join as a node operator or validator? How are technical upgrades decided and implemented? What happens when disputes arise or transactions need reversal due to errors or fraud? Public blockchains answer these questions through decentralized governance, albeit often with challenges around coordination and plutocratic voting power. Permissioned networks must establish explicit governance frameworks.

Partior is backed by a consortium of global banks including DBS, JPMorgan, Standard Chartered, and Deutsche Bank, creating a multi-party governance model where major participants collectively control the network's evolution. This approach balances the need for coordination and standards with the desire to avoid single-institution control that could introduce conflicts of interest.

Network resilience and business continuity require careful consideration. Blockchain networks must continue operating even if individual nodes fail, network partitions occur, or deliberate attacks target infrastructure. Permissioned networks with a limited number of known validators can achieve strong resilience through redundancy and geographic distribution. The tradeoff is that network operation depends on the validators remaining operational and properly motivated to maintain service.

Operational reversibility presents a particular challenge. Traditional payment systems allow transactions to be reversed or recalled in certain circumstances: errors, fraud, or legal orders. Blockchain systems designed for immutability resist reversal by architecture. Financial institutions need mechanisms to handle exceptional situations while preserving the finality that makes blockchain settlement attractive. Solutions typically involve permissioned capabilities allowing authorized parties to mint new tokens offsetting erroneous transfers rather than literally reversing blockchain transactions.

The technical infrastructure for tokenized deposits continues evolving rapidly. Current implementations provide sufficient capabilities for initial deployment and pilot programs, but scaling to full production across diverse use cases will require ongoing development. Standards for interoperability, identity management, privacy preservation, and cross-chain settlement remain works in progress. The industry must balance the benefits of customization for specific needs against the imperative of compatibility and standardization enabling network effects.

Ultimately, the technical infrastructure matters insofar as it enables the functional capabilities institutions and their clients require: fast settlement, programmable logic, continuous availability, transparent reconciliation, and interoperability across institutions and networks. The specific blockchain platforms, consensus mechanisms, and interoperability protocols are means to these ends rather than ends in themselves. As the technology matures and standards emerge, the infrastructure should become increasingly invisible to end users who simply experience superior payment and liquidity management capabilities without needing to understand the underlying blockchain mechanics.

Compliance and Regulation: Built for the Regulated World

One of the most significant advantages tokenized deposits hold over many cryptocurrency alternatives is how naturally they fit within existing regulatory frameworks. While crypto markets often struggle with regulatory uncertainty, tokenized deposits emerged from regulated banks operating under established supervision, making compliance integration a design feature rather than an afterthought.

Traditional banking regulation divides oversight across multiple dimensions: prudential regulation ensuring banks remain safe and sound, conduct regulation governing how banks treat customers, and functional regulation covering specific activities like payments or securities services. Banks issuing tokenized deposits already operate under comprehensive supervision across all these dimensions. The blockchain technology introduces new operational characteristics but does not fundamentally alter the legal nature of the deposit or the regulatory obligations surrounding it.

In the United States, banks issuing tokenized deposits operate under the supervision of their primary federal regulator: the Office of the Comptroller of the Currency for national banks, the Federal Reserve for state member banks and bank holding companies, or the Federal Deposit Insurance Corporation for state non-member banks. These regulators examine banks regularly, assess capital adequacy, review risk management practices, and enforce compliance with banking laws. Tokenized deposits simply represent another product offering subject to this existing supervision.

The Office of the Comptroller of the Currency clarified its position on bank crypto activities through interpretive letters beginning in 2020, confirming that national banks may provide custody services for crypto assets, use stablecoins for payment activities, and operate nodes on blockchain networks. The GENIUS Act, passed by the Senate in June 2025 and signed into law in July 2025, established a federal regulatory framework for payment stablecoins while explicitly recognizing deposit tokens issued by regulated banks as distinct from stablecoins issued by nonbank entities.

The GENIUS Act requires payment stablecoin issuers to hold at least one dollar of permitted reserves for every stablecoin issued, with permitted reserves limited to coins, currency, insured deposits, short-dated Treasury bills, repos backed by Treasury bills, government money market funds, and central bank reserves. Issuers must submit periodic reports of outstanding stablecoins and reserve composition, certified by executives and examined by registered public accounting firms, with those having more than 50 billion dollars in outstanding stablecoins required to provide audited annual financial statements.

The GENIUS Act explicitly states that payment stablecoins issued by permitted issuers are not securities under federal securities laws or commodities under the Commodity Exchange Act, removing them from SEC and CFTC jurisdiction. For banks issuing tokenized deposits, this classification provides clarity: deposit tokens are bank products supervised by banking regulators, not novel crypto assets requiring new regulatory approaches.

All stablecoin issuers under the GENIUS Act must comply with the Bank Secrecy Act, implementing anti-money-laundering and counter-terrorist-financing measures. Banks already maintain robust BSA compliance programs as a core regulatory requirement, giving them infrastructure advantage over nonbank stablecoin issuers building compliance capabilities from scratch.

The know-your-customer requirements embedded in banking regulation align naturally with permissioned blockchain architectures. Distributed ledger systems used for tokenized deposits maintain know-your-customer, anti-money-laundering, and counter-terrorist-financing checks as integrated components of the infrastructure. When a transaction initiates, the system validates that all parties are properly identified and authorized before allowing execution. This contrasts sharply with public cryptocurrency systems where pseudonymous addresses can receive funds without identity verification, creating ongoing regulatory friction.

Transaction monitoring and suspicious activity reporting become more straightforward on shared ledgers where all participants can see relevant transactions. Rather than piecing together activity across multiple correspondent banks and jurisdictions, a tokenized deposit network provides transparent transaction history visible to relevant authorities. Banks can implement automated monitoring tools examining blockchain data continuously, flagging unusual patterns for investigation.

The GENIUS Act requires stablecoin issuers to possess technical capability to seize, freeze, or burn payment stablecoins when legally required and to comply with lawful orders. Permissioned blockchain architectures can implement such controls through administrative smart contracts allowing authorized parties to lock or transfer tokens in response to legal process. This capability is essential for law enforcement and sanctions enforcement but challenging to implement in truly decentralized systems.

Sanctions compliance illustrates both the advantages and challenges of tokenized deposits. Office of Foreign Assets Control regulations prohibit transactions with sanctioned entities, and banks must screen all payments against sanctions lists. The GENIUS Act explicitly subjects stablecoin issuers to Bank Secrecy Act obligations including sanctions compliance, requiring sanctions list verification. Tokenized deposit systems can implement automated sanctions screening before transaction execution, blocking prohibited transfers before they settle rather than identifying violations after the fact.

However, the programmability of tokenized deposits creates potential compliance challenges. If a smart contract automatically executes payments based on conditions without human review, how do banks ensure each automated payment complies with sanctions requirements? The answer requires embedding compliance checks within smart contract logic or limiting automation to low-risk scenarios with sufficient human oversight. This tension between automation efficiency and compliance assurance will require ongoing attention as smart contract sophistication increases.

The European Union's regulatory approach has evolved rapidly, with MiCA providing comprehensive framework for crypto assets. MiCA's provisions covering asset-referenced tokens and e-money tokens took effect on June 30, 2024, imposing strict reserve requirements, whitepaper disclosures, and authorization processes for stablecoin issuers. Crypto Asset Service Providers must begin applying for licenses starting January 2025, with an 18-month grandfathering period allowing existing providers to continue while transitioning to full compliance.

MiCA divides stablecoins into e-money tokens backed by single fiat currencies and asset-referenced tokens backed by multiple assets. E-money tokens face requirements similar to electronic money under existing EU e-money directives, requiring issuers to be licensed in the EU, maintain fully backed reserves, and publish detailed disclosures. Issuers must maintain at least 30 percent of reserves in highly liquid assets, with all reserves held in EU financial institutions.

Both GENIUS Act and MiCA require regulated stablecoin issuers to hold reserves in conservative one-for-one ratios against all stablecoins in circulation, with deposits held in bankruptcy-protected structures. Both frameworks entitle holders to redemption at par and impose obligations on exchanges and service providers handling stablecoins. The convergence between U.S. and EU approaches, despite different starting points and political contexts, reflects shared policy goals around consumer protection, financial stability, and regulated money.

For banks issuing tokenized deposits in multiple jurisdictions, the proliferation of regulations creates compliance complexity but not fundamental uncertainty. Banks operate across borders routinely, managing compliance with different regulatory regimes as part of normal operations. The key advantage is that tokenized deposits generally fit within existing banking regulation rather than requiring entirely new frameworks.

Asia-Pacific jurisdictions have taken varied approaches. Singapore's Monetary Authority of Singapore backed Partior's development and praised it as "a global watershed moment for digital currencies, marking a move from pilots and experimentations towards commercialization and live adoption". Singapore has established itself as a supportive jurisdiction for financial innovation while maintaining strong regulatory oversight, creating an attractive environment for blockchain-based financial services.

Hong Kong similarly positioned itself as a digital asset hub, though maintaining careful regulatory controls. Hong Kong's Stablecoin Ordinance, passed in May 2025, requires all stablecoin issuers backed by the Hong Kong dollar to obtain licenses from the Hong Kong Monetary Authority, maintain high-quality liquid reserve assets equal to par value of stablecoins in circulation, and submit to strict requirements including AML/CFT compliance and regular audits.

Japan's regulatory approach emphasizes consumer protection and financial stability, with the Financial Services Agency maintaining stringent oversight of crypto activities. Tokenized deposits issued by licensed banks would fall under existing banking regulation, though specific guidance continues developing as the technology matures.

The regulatory landscape remains dynamic, with frameworks continuing to evolve as regulators observe market developments and industry practices. However, the fundamental regulatory advantage of tokenized deposits is already clear: they work within established legal and regulatory structures rather than challenging them. Comptroller of the Currency Jonathan Gould stated that the GENIUS Act "will transform the financial services industry" and that "the OCC is prepared to work swiftly to implement this landmark legislation", indicating regulatory receptiveness to facilitating tokenized deposit adoption.

The on-chain transparency of blockchain systems provides regulators with new oversight tools. Rather than requesting reports or conducting examinations based on samples, regulators could potentially observe all transactions on permissioned networks in real time. This surveillance capability raises privacy concerns but offers unprecedented regulatory visibility into financial activity. The balance between transparency for oversight and confidentiality for commercial operations will require ongoing negotiation as blockchain adoption expands.

One significant area requiring continued regulatory development involves the treatment of smart contracts within banking law. When a smart contract automatically executes a payment based on programmed conditions, who bears liability if the outcome differs from what parties intended? How should courts interpret smart contract code when disputes arise? Should banks be held to the same standards for smart contract execution as for manual transaction processing? These questions lack definitive answers, and different jurisdictions may develop different precedents.

Cross-border regulatory harmonization would significantly benefit tokenized deposit development, but achieving such harmonization has proven elusive even in traditional banking. The Basel Committee on Banking Supervision coordinates international banking regulation but allows substantial national discretion. The Financial Stability Board published recommendations on global stablecoin arrangements including cross-border collaboration, transparent disclosures, and compliance with AML/CFT measures, providing high-level principles but leaving implementation details to national authorities.

For tokenized deposits to realize their full potential for global liquidity management, regulatory frameworks must enable cross-border flows while preserving national policy autonomy and preventing regulatory arbitrage. This tension between integration and sovereignty characterizes international financial regulation generally and will shape tokenized deposit regulation specifically.

Data localization requirements illustrate the challenge. Some jurisdictions require financial data to be stored within their borders, complicating global blockchain networks that inherently distribute data across multiple nodes potentially in multiple countries. Technical solutions like partitioned ledgers or encryption can address some concerns, but regulatory acceptance varies.

The Digital Operational Resilience Act in the EU represents another regulatory development affecting tokenized deposits. DORA mandates incident reporting, risk management systems, and strong cybersecurity measures for financial entities including crypto asset service providers. Banks deploying tokenized deposits must ensure their blockchain infrastructure meets operational resilience standards, including the ability to continue operations during outages, recover from failures, and respond to cyber attacks.

Looking forward, the regulatory environment for tokenized deposits will likely remain broadly favorable given that banks operate under established supervision and that tokenized deposits simply represent technological evolution rather than regulatory revolution. Specific rules will continue developing as regulators gain experience with blockchain-based banking and as industry practices mature. The fundamental compatibility between tokenized deposits and existing regulatory frameworks means regulatory development will refine approaches rather than determine whether tokenized deposits are permissible at all.

This regulatory integration represents a critical advantage over less regulated crypto alternatives. While regulatory clarity sometimes seems to constrain innovation, it also enables institutional adoption at scale. Corporate treasurers, financial institutions, and large-scale users need regulatory certainty to deploy new technologies for mission-critical operations. Tokenized deposits provide that certainty in a way that truly decentralized cryptocurrencies cannot, making them far more viable for transforming mainstream financial infrastructure rather than creating parallel systems outside traditional finance.

The Real Competition: Stablecoins, CBDCs, and Tokenized Deposits

The digital currency landscape comprises multiple overlapping categories: tokenized deposits issued by commercial banks, stablecoins issued by nonbank entities, central bank digital currencies issued by monetary authorities, and e-money tokens issued by specialized institutions. Understanding the distinctions between these categories and their relative advantages for different use cases illuminates which forms of digital money will prevail in various contexts.

The comparison begins with the issuer and the nature of the liability. Tokenized deposits are issued by licensed commercial banks and represent claims on those banks, backed by the bank's full balance sheet subject to capital and liquidity regulations. Stablecoins are typically issued by nonbank entities and backed by reserves held separately from the issuer's operating assets, often in special purpose vehicles or trust structures. Central bank digital currencies would be issued by central banks and represent direct claims on central bank liabilities, placing them at the apex of the monetary hierarchy alongside physical cash and bank reserves.

The backing and reserve structure varies accordingly. Tokenized deposits require no separate reserves because they are simply representations of existing bank deposits that are themselves backed by the bank's asset portfolio and capital buffer. When a bank issues a tokenized deposit, it is not creating new money but rather tokenizing existing deposit liabilities. Stablecoin issuers under frameworks like the GENIUS Act must maintain full reserve backing with permitted reserves including cash, insured deposits, Treasury bills, repos, money market funds, and central bank reserves. CBDCs would be backed by central bank balance sheets comprising primarily government securities, foreign exchange reserves, and in some cases gold.

The regulatory treatment reflects these structural differences. Under the GENIUS Act, banks issuing deposit tokens operate under their existing banking charters and supervision, while nonbank stablecoin issuers must obtain approval as qualified payment stablecoin issuers either at the federal or state level. Federal and state regulators must issue tailored capital, liquidity, and risk management rules for stablecoin issuers, though the legislation exempts them from the full regulatory capital standards applied to traditional banks. CBDCs would operate under central bank mandates and oversight, with the specific regulatory framework depending on the CBDC design.

Access and distribution models differ significantly. Tokenized deposits are available only to customers of the issuing bank and typically restricted to institutional and corporate clients rather than retail users. Stablecoins can be distributed broadly, depending on the issuer's business model and regulatory constraints. Some stablecoins target institutional users exclusively, while others seek mass retail adoption. CBDCs could take various forms: retail CBDCs providing digital central bank money to all citizens, wholesale CBDCs serving only as settlement medium between financial institutions, or hybrid models with different access tiers.

Programmability varies by implementation rather than category. Both tokenized deposits and stablecoins can embed smart contract logic, though permissioned tokenized deposit networks may offer more sophisticated programmability given tighter integration with banking infrastructure. Most CBDC designs explored to date emphasize basic payment functionality over advanced programmability, though this reflects policy choices rather than technical limitations.

The critical differentiator for many institutional users is counterparty risk. Tokenized deposits carry the risk of the issuing bank, mitigated by deposit insurance up to applicable limits, capital requirements, and regulatory supervision. For large deposits exceeding insurance limits, the risk depends on the bank's creditworthiness and the resolution regime that would apply if the bank failed. Stablecoins carry different risk profiles depending on their structure. The GENIUS Act requires stablecoin holders to have first priority claims on the reserve assets in bankruptcy, providing some protection, but credit risk differs from direct bank deposit risk. CBDCs would carry minimal credit risk given that central banks can create money to meet obligations, though extreme situations like currency crises or sovereign defaults could affect even CBDCs.

Yield characteristics differ as well. The GENIUS Act prohibits permitted payment stablecoin issuers from paying interest or yield to stablecoin holders, limiting stablecoins to non-yielding assets. This restriction aims to prevent stablecoins from competing directly with bank deposits for funding. Tokenized deposits can be interest-bearing or non-interest-bearing depending on the bank's product design, functioning like traditional deposit products. Deposit tokens could potentially be interest-bearing, and JPMorgan's JPMD offers the ability to pay interest to holders, giving tokenized deposits flexibility that stablecoins lack. Most retail CBDC designs contemplate non-interest-bearing currency substitutes, though wholesale CBDCs might pay interest similar to bank reserves.

The interoperability and network effects present another key dimension. Stablecoins circulating on public blockchains can move freely between wallets and interact with decentralized finance protocols, providing broad interoperability within crypto ecosystems but limited integration with traditional financial infrastructure. Tokenized deposits operate primarily within banking networks, interoperating well with existing financial systems but requiring specific bridges or partnerships to interact with public blockchain environments. CBDCs could theoretically interoperate with either private banking systems or public crypto networks, depending on design choices, though most proposals emphasize compatibility with existing financial infrastructure over crypto integration.

Scalability varies by implementation. Public blockchain stablecoins face the throughput and latency constraints of the underlying blockchain, though layer-2 solutions and alternative chains have dramatically improved performance. Tokenized deposits on permissioned blockchains can achieve higher throughput because the validator set is limited and optimized for performance rather than decentralization. Wholesale CBDCs would likely use permissioned infrastructure achieving similar performance to tokenized deposits. Retail CBDCs face greater scalability challenges given the need to serve entire populations with potentially billions of transactions daily.

Privacy considerations differ as well. Stablecoins on public blockchains offer pseudonymous privacy: transactions are visible but addresses are not directly linked to identities. Some privacy-focused stablecoins use zero-knowledge proofs or other techniques to enhance privacy. Tokenized deposits on permissioned networks provide more privacy from public view but less privacy from banks and regulators who can see all transactions. CBDCs raise significant privacy concerns, with retail CBDCs potentially giving central banks unprecedented visibility into all citizens' spending, creating surveillance risks that have generated political opposition in many jurisdictions.

For cross-border payments specifically, each category has different strengths. Stablecoins can move across borders essentially instantly on public blockchains without requiring correspondent banking relationships, though regulatory constraints and AML/KYC requirements limit this advantage in practice. Tokenized deposits enable fast cross-border settlement within banking networks but require participating banks to establish relationships or use intermediary platforms. CBDCs could facilitate cross-border payments through various mechanisms including bilateral agreements between central banks, multilateral platforms, or interoperability protocols, though implementation remains largely conceptual.

The use cases where each category excels reveal different strategic niches. Stablecoins work well for open crypto ecosystems where users want to transact without necessarily holding relationships with specific banks. They serve crypto-native users, decentralized finance applications, and scenarios where the flexibility of public blockchains provides value despite regulatory uncertainties. Tokenized deposits excel in institutional treasury management, corporate payments, and contexts where banking relationships, regulatory clarity, and integration with existing financial infrastructure matter more than permissionless access. CBDCs would serve monetary policy objectives, provide payment infrastructure resilience, and potentially extend financial inclusion, but face political and technical challenges that have slowed adoption.